استراتيجيات سوق الدقيق العضوي، وأفضل اللاعبين، وفرص النمو، والتحليل والتنبؤ بحلول عام 2031

البيانات التاريخية : 2020-2022 | سنة الأساس : 2023 | فترة التنبؤ : 2024-2031حجم سوق الدقيق العضوي وتوقعاته (2020-2030)، والحصة العالمية والإقليمية، والاتجاهات، وفرص النمو. يغطي التقرير: حسب نوع المنتج (دقيق القمح، دقيق الشوفان، دقيق الذرة، دقيق الأرز، وغيرها)، والفئة (تقليدي وخالي من الغلوتين)، وقنوات التوزيع (السوبر ماركت والهايبر ماركت، ومتاجر التجزئة، وتجارة التجزئة عبر الإنترنت، وغيرها).

- تاريخ التقرير : Apr 2024

- رمز التقرير : TIPRE00017870

- الفئة : المأكولات والمشروبات

- الحالة : نُشرت

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 223

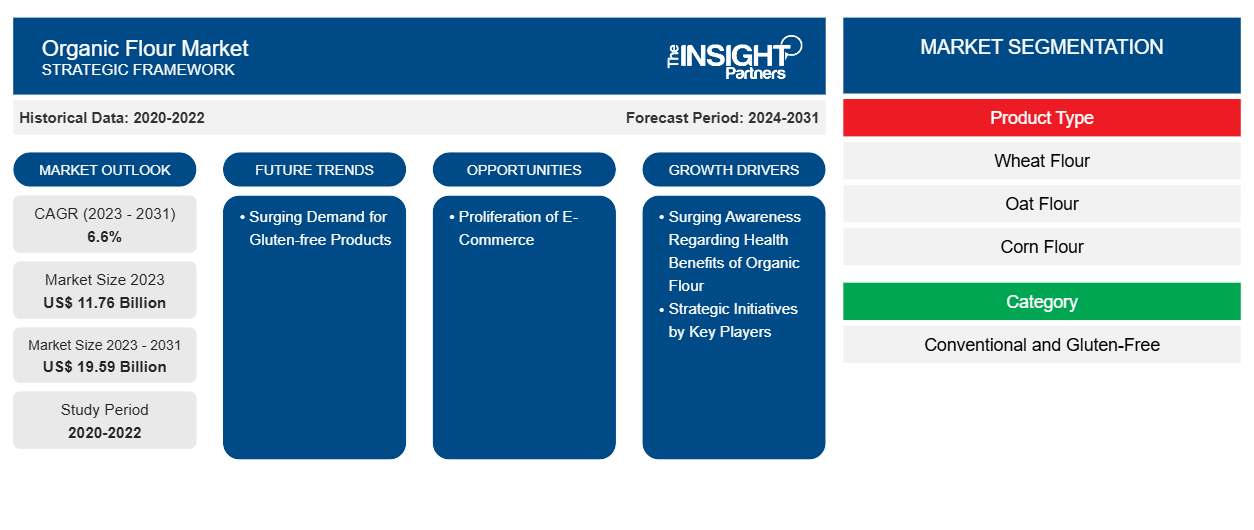

من المتوقع أن ينمو حجم سوق الدقيق العضوي من 11.76 مليار دولار أمريكي في عام 2023 إلى 19.59 مليار دولار أمريكي بحلول عام 2031؛ ومن المتوقع أن يسجل معدل نمو سنوي مركب بنسبة 6.6٪ من عام 2023 إلى عام 2031.

رؤى السوق ووجهة نظر المحلل:

وقد ارتفع الطلب على الدقيق العضوي بشكل كبير مع تزايد وعي المستهلكين بصحتهم والبحث عن المنتجات العضوية. ويتم إنتاج الدقيق العضوي من الحبوب المزروعة بدون مبيدات حشرية سامة أو أسمدة صناعية أو تقنيات الهندسة الوراثية. وقد ارتفع الطلب عليه بسبب تفضيلات المستهلكين المتزايدة لمنتجات غذائية أكثر صحة وصديقة للبيئة ومنتجة بطريقة أخلاقية. بالإضافة إلى ذلك، ساهمت القيمة الغذائية الغنية والفوائد الصحية المحتملة للأطعمة العضوية في زيادة الطلب. وهذا الارتفاع هو جزء من الاتجاه الأكبر في صناعة الأغذية العضوية، والتي شهدت نموًا كبيرًا في السنوات الأخيرة. بالإضافة إلى ذلك، وبسبب الوعي المتزايد بالاستدامة البيئية، يختار العديد من المستهلكين المنتجات العضوية لدعم ممارسات زراعية أكثر صداقة للبيئة تعطي الأولوية لصحة التربة والتنوع البيولوجي. وعلاوة على ذلك، تساهم الرغبة في دعم المزارعين المحليين والمنتجين الصغار وتوفير الشفافية في إنتاج الغذاء في زيادة الطلب على الدقيق العضوي.

محركات النمو والتحديات:

ومن المتوقع أن تساهم المبادرات الاستراتيجية مثل عمليات الدمج والاستحواذ والشراكات وإطلاق الحملات وإطلاق المنتجات التي يقوم بها مختلف اللاعبين في السوق لتعزيز مواقعهم والاستفادة من الفرص الناشئة في زيادة حجم سوق الدقيق العضوي . على سبيل المثال، في عام 2020، استحوذت شركة ADM على حصة 50٪ المتبقية في شركة طحن الدقيق العضوي البريطانية Gleadell Agriculture Ltd. وقد مكن هذا الاستحواذ شركة ADM من توسيع حضورها في سوق الدقيق العضوي وتعزيز قدرات سلسلة التوريد الخاصة بها. كما تلعب عمليات إطلاق الحملات التي تهدف إلى زيادة الوعي وتثقيف المستهلكين حول فوائد الدقيق العضوي دورًا حيويًا في دفع نمو السوق. غالبًا ما يستثمر اللاعبون الرئيسيون في الحملات التسويقية التي تسلط الضوء على المزايا الغذائية للدقيق العضوي والاستدامة البيئية ومعايير الجودة. تساعد هذه الحملات في خلق الطلب وتشكيل تفضيلات المستهلكين وتمييز منتجات الدقيق العضوي عن البدائل التقليدية. تشمل هذه الحملات الإعلانات الرقمية والعروض الترويجية على وسائل التواصل الاجتماعي والمحتوى التعليمي لزيادة وعي المستهلكين بمزايا استخدام الدقيق العضوي في الخبز والطهي.

إن إطلاق المنتجات أمر لا غنى عنه للحفاظ على القدرة التنافسية وتلبية تفضيلات المستهلكين المتطورة في سوق الدقيق العضوي. يبتكر اللاعبون الرئيسيون باستمرار ويقدمون منتجات دقيق عضوي جديدة مصممة خصيصًا لاحتياجات غذائية محددة وتفضيلات ذوق ومناسبات. على سبيل المثال، تلبي أنواع الدقيق العضوي الخالية من الغلوتين احتياجات المستهلكين الذين يعانون من عدم تحمل الغلوتين أو الحساسية تجاهه، في حين تجذب أنواع الدقيق المتخصصة مثل دقيق اللوز أو دقيق جوز الهند المستهلكين المهتمين بالصحة الذين يبحثون عن مكونات خبز بديلة. على سبيل المثال، في عام 2021، قدمت شركة Hodgson Mill خطًا جديدًا من الدقيق العضوي، بما في ذلك دقيق القمح الكامل العضوي والدقيق العضوي متعدد الأغراض ودقيق المعجنات العضوي، لتلبية احتياجات المستهلكين الذين يبحثون عن بدائل عضوية لاحتياجاتهم في الخبز وإظهار التزام شركة Hodgson Mill بتلبية الطلب المتزايد على خيارات الدقيق العضوي. كما تدخل العديد من الشركات السوق العضوية من خلال إطلاق منتجات مثل الدقيق العضوي.

ومن المتوقع أن تعمل الامتثالات التنظيمية المرتبطة بالدقيق العضوي مثل المعايير الصارمة وعمليات الاعتماد التي تفرضها السلطات التنظيمية، بما في ذلك وزارة الزراعة الأمريكية واللائحة العضوية للاتحاد الأوروبي، على كبح نمو سوق الدقيق العضوي العالمي. ويستلزم الحصول على شهادة عضوية عمليات تفتيش شاملة وتوثيق والالتزام بممارسات الزراعة العضوية المحددة، وكلها تتطلب وقتًا واستثمارًا ماليًا كبيرًا من المنتجين. ويمكن أن تعمل هذه العملية الشاقة كرادع للمنتجين الأصغر حجمًا أو أولئك الذين لديهم موارد محدودة، مما يعوق القدرة على الدخول أو التوسع في سوق الدقيق العضوي.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق الدقيق العضوي: رؤى استراتيجية

-

احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

تقسيم التقرير ونطاقه:

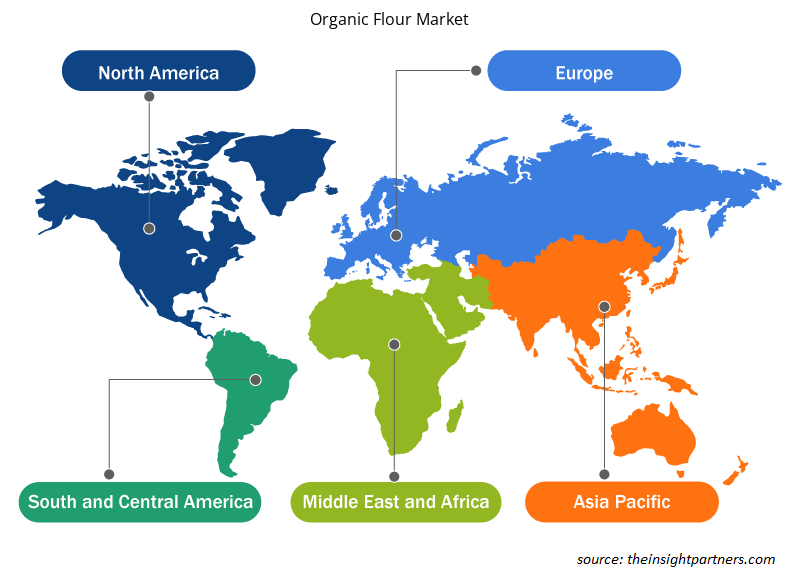

تم إجراء "تحليل سوق الدقيق العضوي العالمي" من خلال النظر في القطاعات التالية: نوع المنتج والفئة وقناة التوزيع والجغرافيا. بناءً على نوع المنتج، يتم تقسيم سوق الدقيق العضوي إلى دقيق القمح ودقيق الشوفان ودقيق الذرة ودقيق الأرز وغيرها. بناءً على الفئة، يتم تقسيم السوق إلى تقليدي وخالي من الغلوتين. حسب قناة التوزيع، يتم تقسيم السوق إلى محلات السوبر ماركت والهايبر ماركت ومتاجر التجزئة وتجارة التجزئة عبر الإنترنت وغيرها. يركز النطاق الجغرافي لتقرير سوق الدقيق العضوي على أمريكا الشمالية (الولايات المتحدة وكندا والمكسيك) وأوروبا (ألمانيا وفرنسا وإيطاليا والمملكة المتحدة وروسيا وبقية أوروبا) ومنطقة آسيا والمحيط الهادئ (أستراليا والصين واليابان والهند وكوريا الجنوبية وبقية منطقة آسيا والمحيط الهادئ) والشرق الأوسط وأفريقيا (جنوب أفريقيا والمملكة العربية السعودية والإمارات العربية المتحدة وبقية منطقة الشرق الأوسط وأفريقيا) وأمريكا الجنوبية والوسطى (البرازيل والأرجنتين وبقية أمريكا الجنوبية والوسطى).

التحليل القطاعي:

بناءً على نوع المنتج، يتم تقسيم السوق إلى دقيق القمح ودقيق الشوفان ودقيق الذرة ودقيق الأرز وغيرها. بناءً على النوع، من المتوقع أن يحتفظ قطاع الخالي من الغلوتين بحصة كبيرة في سوق الدقيق العضوي بحلول عام 2030. تم تصميم الدقيق الخالي من الغلوتين للأفراد المصابين بمرض الاضطرابات الهضمية أو حساسية الغلوتين وأولئك الذين يختارون نظامًا غذائيًا خاليًا من الغلوتين. ارتفع الطلب على منتجات الادعاءات الخالية من الغلوتين بشكل كبير بسبب الانتشار المتزايد للاضطرابات المرتبطة بالغلوتين واتجاه أوسع نطاقًا يهتم بالصحة. وفقًا لـ Beyond Celiac، يعاني 1 من كل 133 أمريكيًا، أو حوالي 1٪ من السكان، من مرض الاضطرابات الهضمية في الولايات المتحدة. أدى الوعي بمرض الاضطرابات الهضمية إلى دفع العديد من المستهلكين إلى البحث عن بدائل خالية من الغلوتين، مما أدى إلى إنشاء سوق كبيرة للمنتجات التي تلبي القيود الغذائية. علاوة على ذلك، أدى تصور أن الخيارات الخالية من الغلوتين قد تكون أكثر صحة إلى توسيع قاعدة المستهلكين إلى ما هو أبعد من أولئك الذين يعانون من حالات طبية، مما ساهم في النمو المستدام لسوق الدقيق العضوي لقطاع الخالي من الغلوتين.

التحليل الإقليمي:

بناءً على الجغرافيا، تم تقسيم السوق إلى خمس مناطق رئيسية - أمريكا الشمالية وأوروبا وآسيا والمحيط الهادئ وأمريكا الجنوبية والوسطى والشرق الأوسط وأفريقيا. من حيث الإيرادات، سيطرت أمريكا الشمالية على حصة سوق الدقيق العضوي العالمية. بلغت قيمة السوق في أمريكا الشمالية حوالي 2900 مليون دولار أمريكي في عام 2023. ومن المتوقع أن ينمو سوق الدقيق العضوي في منطقة آسيا والمحيط الهادئ بأعلى معدل نمو سنوي مركب خلال الفترة المتوقعة. تشهد منطقة آسيا والمحيط الهادئ تحضرًا سريعًا وأنماط حياة مستهلكة متغيرة. يسعى المستهلكون الحضريون إلى الدقيق العضوي كمكون أساسي للخبز المصنوع منزليًا والمعجنات وغيرها من السلع المخبوزة. كما تسارع التحول نحو الخبز المنزلي بسبب عوامل مثل جائحة كوفيد-19، مما دفع المزيد من المستهلكين إلى استكشاف الطهي والخبز في المنزل. ونتيجة لذلك، نما الطلب على الدقيق العضوي كمكون متعدد الاستخدامات ومغذي للخبز بشكل كبير في منطقة آسيا والمحيط الهادئ، مما دعم توسع السوق.

تعد منطقة آسيا والمحيط الهادئ موطنًا لمناظر طبيعية زراعية متنوعة وممارسات زراعية تقليدية، مما يوفر فرصًا واسعة لإنتاج الدقيق العضوي. وقد شهدت دول مثل الهند والصين وأستراليا ارتفاعًا في مبادرات الزراعة العضوية المدعومة بسياسات حكومية تروج للزراعة المستدامة وبرامج الشهادات العضوية. وقد أدى هذا الاهتمام المتزايد بالزراعة العضوية إلى زيادة توافر الحبوب العضوية والدقيق المنتج في المنطقة. إن الوعي المتزايد بالصحة والعافية يدفع نمو سوق الدقيق العضوي في منطقة آسيا والمحيط الهادئ.

وتشكل أوروبا مساهماً رئيسياً آخر، إذ تستحوذ على أكثر من 30% من حصة السوق العالمية. ويشعر المستهلكون في مختلف أنحاء أوروبا بقلق متزايد إزاء سلامة الغذاء والاستدامة البيئية وتأثير الممارسات الزراعية على الصحة العامة. وقد أدى هذا إلى تفضيل متزايد للمنتجات العضوية، بما في ذلك الدقيق. ويسعى المستهلكون في أوروبا بنشاط إلى الحصول على الدقيق العضوي المنتج بدون مبيدات حشرية أو مبيدات أعشاب صناعية أو كائنات معدلة وراثياً، معتبرين أنه خيار أكثر أماناً وصديقاً للبيئة من الدقيق التقليدي. ويعود هذا التحول نحو الدقيق العضوي أيضاً إلى أنماط حياة المستهلكين المتغيرة وتفضيلاتهم الغذائية، حيث يختار العديد من الأوروبيين خيارات غذائية أكثر صحة وطبيعية.

رؤى إقليمية حول سوق الدقيق العضوي

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق الدقيق العضوي طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق الدقيق العضوي والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق الدقيق العضوي

نطاق تقرير سوق الدقيق العضوي

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2023 | 11.76 مليار دولار أمريكي |

| حجم السوق بحلول عام 2031 | 19.59 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2023 - 2031) | 6.6% |

| البيانات التاريخية | 2020-2022 |

| فترة التنبؤ | 2024-2031 |

| القطاعات المغطاة |

حسب نوع المنتج

|

| المناطق والدول المغطاة |

أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

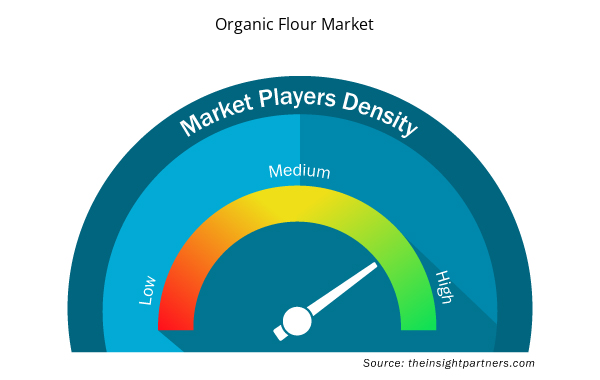

كثافة اللاعبين في سوق الدقيق العضوي: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق الدقيق العضوي نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق الدقيق العضوي هي:

- شركة هوم تاون للأغذية

- الأطعمة الطبيعية من بوبس ريد ميل

- شركة كينج آرثر للخبز

- كورو

- شركة Betterbody Foods

- شركة FWP ماثيوز المحدودة

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق الدقيق العضوي

تطورات الصناعة والفرص المستقبلية:

يمكن أن تساعد توقعات سوق الدقيق العضوي أصحاب المصلحة في التخطيط لاستراتيجيات النمو الخاصة بهم. فيما يلي المبادرات التي اتخذها اللاعبون الرئيسيون العاملون في سوق الدقيق العضوي:

- في عام 2022، أعلنت شركة GCMMF الرائدة في مجال الألبان، والتي تسوق منتجاتها تحت العلامة التجارية Amul، عن دخولها سوق الأغذية العضوية بإطلاق دقيق القمح العضوي. أول منتج تم إطلاقه في هذه المحفظة هو "دقيق القمح الكامل العضوي من Amul".

المنافسة والشركات الرئيسية:

تعد شركة Hometown Food Company، وBob's Red Mill Natural Foods، وBetterbody Foods C/O، وFWP Matthews Ltd، وShipton Mill Ltd، وW and H Marriage and Sons Limited، وGilchesters Organics، وAnita's Organic Grain & Flour Mill Ltd من بين اللاعبين البارزين الذين تم عرضهم في تقرير سوق الدقيق العضوي. يركز اللاعبون العاملون في السوق العالمية على توفير منتجات عالية الجودة لتلبية طلب العملاء. كما يتبنون استراتيجيات مختلفة مثل إطلاق منتجات جديدة وتوسيع القدرات والشراكات والتعاون من أجل البقاء قادرين على المنافسة في السوق.

حابي محلل أبحاث سوق متمرس، يتمتع بخبرة 8 سنوات في قطاع الكيماويات والمواد، بالإضافة إلى خبرته في قطاعي الأغذية والمشروبات والسلع الاستهلاكية. وهو مهندس كيميائي من معهد فيشواكارما للتكنولوجيا (VIT)، وقد اكتسب معرفةً عميقةً في مجالات الكيماويات الصناعية والتخصصية، والدهانات والطلاءات، والورق والتغليف، ومواد التشحيم، والمنتجات الاستهلاكية.

تشمل كفاءات حابي الأساسية تقدير حجم السوق والتنبؤ به، ووضع معايير تنافسية، وتحليل الاتجاهات، والتفاعل مع العملاء، وكتابة التقارير، وتنسيق الفريق، مما يجعله بارعًا في تقديم رؤى عملية ودعم اتخاذ القرارات الاستراتيجية.

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق الدقيق العضوي

احصل على عينة مجانية ل - سوق الدقيق العضوي