Markt für biomedizinische Sensoren – Erkenntnisse durch globale und regionale Analyse – Prognose bis 2031

Marktgröße und Prognose für biomedizinische Sensoren (2021–2031), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalyse: Nach Typ (kabelgebunden und drahtlos), Sensortyp (Temperatur-, Druck-, Bildsensoren, biochemische Sensoren, Trägheitssensoren, Bewegungssensoren, Elektrokardiogramm und andere Sensortypen), Produkt (invasive Sensoren und nichtinvasive Sensoren), Anwendung (medizinische Diagnostik, klinische Therapie, Bildgebung und persönliche Gesundheitsversorgung) und Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00019633

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : December 24, 2024

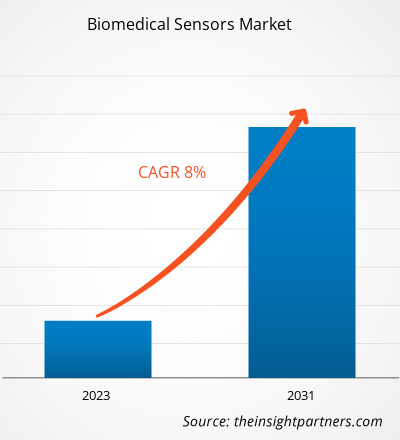

Der Markt für biomedizinische Sensoren soll von 9,97 Milliarden US-Dollar im Jahr 2023 auf 21,11 Milliarden US-Dollar im Jahr 2031 wachsen; für den Zeitraum 2023–2031 wird ein durchschnittliches jährliches Wachstum von 8,0 % erwartet. Die Integration von Überwachungstechnologien in Smartphones und drahtlose Geräte ist ein entscheidender Trend auf dem Markt für biomedizinische Sensoren.

Marktanalyse für biomedizinische Sensoren

Viele private und staatliche Organisationen sammeln Gelder, um die biomedizinische Forschung zu unterstützen. Die Finanzierung zielt darauf ab, die kollaborative Forschung zwischen Fakultäten in den Bereichen Biomedizin und Ingenieurwesen zu erleichtern, wobei der Schwerpunkt auf der Entwicklung biomedizinischer Geräte, Sensoren und Systeme liegt. Im April 2023 wurde das Forschungsprojekt SmartCare: HbA1c Self-Monitoring Technology, das vom National Institute for Health Research (NiHR i4i Connect) mit einem Zuschuss in Höhe von 186,7 Millionen US-Dollar finanziert wird, mit dem Hauptziel ins Leben gerufen, ein Diabetes-Diagnosetool experimentell zu validieren, das sich auf verschiedene Blutbiomarker konzentriert. Dr. Iasonas Triantis vom Forschungszentrum für Biomedizintechnik an der School of Science and Technology wurde zum Principal Investigator (PI) der Studie ernannt. Ebenso vergab die Novo Nordisk Foundation im Februar 2024 großzügig einen Zuschuss von 21,37 Millionen US-Dollar für die Gründung des Copenhagen Center for Biomedical Quantum Sensing. Mit dieser Initiative wird der Bereich der Biomedizin und Gesundheitswissenschaften mit dem Aufkommen der Quantensensortechnologie einen großen Wandel erleben. Diese Spitzentechnologie verspricht, die Diagnose und Prävention von Krankheiten mit beispielloser Präzision zu revolutionieren. Im Rahmen dieser internationalen Forschungszusammenarbeit wollen Wissenschaftler neuartige Quantensensorprinzipien und -techniken entwickeln, die zur Früherkennung von Krankheiten eingesetzt werden können.

Marktübersicht für biomedizinische Sensoren

Das Wachstum des Marktes für biomedizinische Sensoren wird Faktoren wie der zunehmenden Verbreitung von IoT-basierten medizinischen Geräten, der wachsenden Nachfrage nach häuslicher medizinischer Versorgung, der wachsenden Zahl geriatrischer Menschen, technologischen Fortschritten in der Medizingerätebranche und steigenden Gesundheitsausgaben weltweit zugeschrieben. Der Markt für biomedizinische Sensoren ist in Nordamerika, Europa, den asiatisch-pazifischen Raum, den Nahen Osten und Afrika sowie Süd- und Mittelamerika unterteilt. Nordamerika hält den größten Marktanteil, und der asiatisch-pazifische Raum wird voraussichtlich zwischen 2023 und 2031 die schnellste durchschnittliche jährliche Wachstumsrate verzeichnen. Die USA werden voraussichtlich den größten Anteil des Marktes für biomedizinische Sensoren haben. Das Marktwachstum in den USA wird den Bemühungen führender Anbieter biomedizinischer Sensoren zugeschrieben, ihre primären Produktionsstandorte aufzubauen, der steigenden Zahl akuter und chronischer Erkrankungen in der Bevölkerung und den technologischen Fortschritten im Gesundheitssektor dieses Landes.IoT-based medical devices, burgeoning demand for home-based medical care, surging geriatric population, technological advancements in the medical device industry, and rising expenditure on healthcare across the world. The biomedical sensors market is segmented into North America, Europe, Asia Pacific, the Middle East & Africa, and South & Central America. North America holds the largest share of the market, and Asia Pacific is expected to record the fastest CAGR during 2023–2031. The US is estimated to account for the largest share of the biomedical sensors market. Market growth in the US is attributed to the efforts made by leading biomedical sensor vendors to establish their primary manufacturing bases, rising incidences of acute and chronic diseases among the population, and technological advancements in the healthcare sector in this country.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für biomedizinische Sensoren: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Treiber und Chancen auf dem Markt für biomedizinische Sensoren

Steigende Zahl von Zivilisationskrankheiten begünstigt den Markt

Verschiedene Faktoren wie Stress, Fettleibigkeit, Bewegungsmangel, Mangelernährung sowie Tabak- und Alkoholkonsum tragen zur zunehmenden Verbreitung lebensstilbedingter Krankheiten bei, darunter auch Herz-Kreislauf-Erkrankungen (CVDs). Laut dem Bericht „Heart Disease and Stroke Statistics—2023“ der American Heart Association war die koronare Herzkrankheit im Jahr 2021 die häufigste Form der Herzerkrankung und forderte in diesem Jahr 375.476 Todesopfer. Schätzungsweise 5 % der Erwachsenen ab 20 Jahren leiden an einer koronaren Herzkrankheit (CAD). Daher besteht angesichts der steigenden Zahl von Lebensstilkrankheiten ein erhöhter Bedarf an biomedizinischen Sensoren, die zur regelmäßigen Gesundheitsüberwachung eingesetzt werden können. Moderne CVD-Biosensoren und Überwachungs-Bioelektronik, die in der jüngsten Vergangenheit eingeführt wurden und entweder tragbar oder implantierbar sind, haben die kontinuierliche Messung von Herzmarkern ermöglicht.CVDs). According to the "Heart Disease and Stroke Statistics—2023" report by the American Heart Association, coronary heart disease was the most prevalent form of heart disease in 2021, claiming the lives of 375,476 individuals that year. Nearly 5% of adults aged 20 and above are estimated to have CVD biosensors and monitoring bioelectronics introduced in the recent past, either wearable or implantable, have enabled the continuous measurement of cardiac markers.

Technologische Fortschritte bei biomedizinischen Sensoren werden den Markt in Zukunft stärken

Technologische Fortschritte bei biomedizinischen Sensoren durch die Integration von Mikro- und Nanotechnologie führen zur Einführung kompakter, robuster, innovativer und kostengünstiger Sensoren, die an die genetische Ausstattung jedes Einzelnen angepasst werden können. Diese Sensoren sollen Alarme auslösen, wenn sie unvorhersehbare Werte aufzeichnen, das Blut auf das Vorhandensein toxischer Stoffe untersuchen und Medikamente direkt in den Blutkreislauf einbringen. Steigende Investitionen in die Entwicklung und behördliche Zulassung solcher fortschrittlichen Sensoren dürften den Markt für biomedizinische Sensoren in den kommenden Jahren ankurbeln. Darüber hinaus führen neue Anwendungen biomedizinischer Sensoren im Bereich der Nanotechnologie und kontinuierliche Innovationen zur Entwicklung fortschrittlicher nichtinvasiver sensorbasierter medizinischer Verfahren. Im Februar 20201 entwickelten Forscher von Missouri S&T ein sauerstoffempfindliches Pflaster, das auf einen flexiblen Einwegverband gedruckt ist, der mit einem Smartphone verbunden werden kann. Dieser intelligente Verband könnte eine Fernüberwachung zur Früherkennung von Erkrankungen wie Druckgeschwüren ermöglichen und so eine sofortige Behandlung oder Intervention ermöglichen.

Segmentierungsanalyse des Marktberichts für biomedizinische Sensoren

Wichtige Segmente, die zur Ableitung der Marktanalyse für biomedizinische Sensoren beigetragen haben, sind Typ, Sensortyp, Produkt und Anwendung.

- Der Markt für biomedizinische Sensoren ist je nach Typ in kabelgebundene und kabellose Sensoren unterteilt. Das kabellose Segment hatte im Jahr 2023 einen größeren Marktanteil.

- Nach Sensortyp ist der Markt in Temperatur-, Druck-, Bildsensoren, biochemische Sensoren, Trägheitssensoren, Bewegungssensoren, Elektrokardiogramm und andere Sensortypen unterteilt. Das Temperatursegment hatte im Jahr 2023 den größten Marktanteil.

- Produktbezogen ist der Markt in invasive und nichtinvasive Sensoren unterteilt. Das Segment der nichtinvasiven Sensoren hatte im Jahr 2023 einen größeren Marktanteil.

- Basierend auf der Anwendung ist der Markt in medizinische Diagnostik, klinische Therapie, Bildgebung und persönliche Gesundheitsfürsorge segmentiert. Das Segment der medizinischen Diagnostik hatte im Jahr 2023 den größten Marktanteil.

Marktanteilsanalyse für biomedizinische Sensoren nach Geografie

Der geografische Umfang des Marktberichts für biomedizinische Sensoren ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Süd- und Mittelamerika. Nordamerika dominiert den globalen Markt für biomedizinische Sensoren. Laut der Weltgesundheitsorganisation (WHO) erleiden jedes Jahr fast 30 Millionen Menschen einen Schlaganfall. Die American Heart Association gibt an, dass bis 2035 schätzungsweise mehr als 130 Millionen Menschen in den USA an einer Art von Herz-Kreislauf-Erkrankung (CVD) leiden werden. Die steigende Prävalenz von CVDs wird daher der Dominanz Nordamerikas auf dem Weltmarkt zugeschrieben.

Regionale Einblicke in den Markt für biomedizinische Sensoren

Die regionalen Trends und Faktoren, die den Markt für biomedizinische Sensoren im gesamten Prognosezeitraum beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie für biomedizinische Sensoren in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Holen Sie sich die regionalspezifischen Daten für den Markt für biomedizinische Sensoren

Umfang des Marktberichts zu biomedizinischen Sensoren

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2023 | 9,97 Milliarden US-Dollar |

| Marktgröße bis 2031 | 21,11 Milliarden US-Dollar |

| Globale CAGR (2023 - 2031) | 8,0 % |

| Historische Daten | 2021-2022 |

| Prognosezeitraum | 2023–2031 |

| Abgedeckte Segmente |

Nach Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmerdichte: Der Einfluss auf die Geschäftsdynamik

Der Markt für biomedizinische Sensoren wächst rasant, angetrieben durch die steigende Nachfrage der Endnutzer aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung von Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten auf dem Markt für biomedizinische Sensoren tätigen Unternehmen sind:

- Cognifit

- Mango-Gesundheit

- Buntball

- Ayogo Health Inc

- Fitbit, Inc.

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für biomedizinische Sensoren

Neuigkeiten und aktuelle Entwicklungen zum Markt für biomedizinische Sensoren

Der Markt für biomedizinische Sensoren wird durch die Erhebung qualitativer und quantitativer Daten aus Primär- und Sekundärforschung bewertet, die wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken umfasst. Nachfolgend sind einige der wichtigsten Entwicklungen auf dem Markt für biomedizinische Sensoren aufgeführt:

- Abbott hat Bigfoot Biomedical übernommen, ein Unternehmen, das über Fachwissen in der Entwicklung intelligenter Insulinmanagementsysteme für Diabetiker verfügt. Das von Bigfoot Biomedical entwickelte intelligente Insulinmanagementsystem Bigfoot Unity verwendet vernetzte Insulinpen-Kappen und sein Betrieb basiert auf Daten der integrierten kontinuierlichen Glukoseüberwachung (iCGM) und Anweisungen des Gesundheitsdienstleisters. (Quelle: Abbott, Pressemitteilung, 2023)

- Onera Health hat sein erstes Onera Biomedical Lab-on-Chip auf den Markt gebracht. Das biomedizinische Sensorsystem auf einem Chip ist für die Erfassung und Verarbeitung mehrerer Biosignale konzipiert und eignet sich für eine breite Palette tragbarer Gesundheitsgeräte sowie Anwendungen. Es bietet viele Lösungen und Möglichkeiten für Innovationen in den Bereichen Medizin, Wellness und Fitness. (Quelle: Onera Technologies BV, Pressemitteilung, 2022)

Marktbericht zu biomedizinischen Sensoren – Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für biomedizinische Sensoren (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Marktgröße und Prognose für biomedizinische Sensoren auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt sind

- Markttrends für biomedizinische Sensoren sowie Marktdynamik wie Treiber, Einschränkungen und wichtige Chancen

- Detaillierte PEST/Porters Five Forces- und SWOT-Analyse

- Marktanalyse für biomedizinische Sensoren mit Abdeckung wichtiger Markttrends, globaler und regionaler Rahmenbedingungen, wichtiger Akteure, Vorschriften und aktueller Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse, die die Marktkonzentration, Heatmap-Analyse, prominente Akteure und aktuelle Entwicklungen auf dem Markt für biomedizinische Sensoren umfasst

- Detaillierte Firmenprofile

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends