Knochenzementmarkt, Knochenzementmarktgröße, Knochenzementmarktanteil, Knochenzementmarktprognose, Knochenzementmarktwachstum, Knochenzementmarktanalyse Marktanalyse und Prognose nach Größe, Anteil, Wachstum, Trends CAGR von 5,70 %

Marktgröße und Prognose für Knochenzement (2021 – 2031), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalyse: Nach Typ [Polymethylmethacrylat (PMMA)-Zement, Calciumphosphat-Zement (CPC) und Glaspolyalkenoat-Zement (GPC)], Anwendung (Arthroplastik, Kyphoplastie und Vertebroplastie), Endbenutzer [Krankenhäuser, ambulante Operationszentren (ASCs) und Kliniken] und Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPHE100000838

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : February 15, 2025

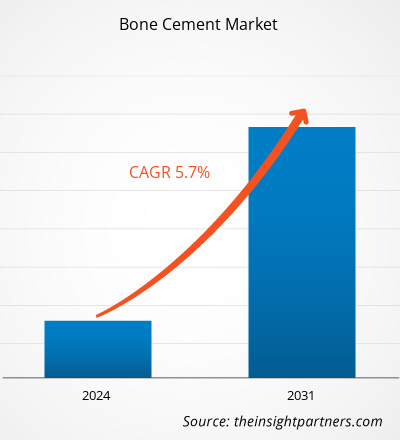

Der Markt für Knochenzement soll von 1,23 Milliarden US-Dollar im Jahr 2023 auf 1,92 Milliarden US-Dollar im Jahr 2031 wachsen. Für den Zeitraum 2023–2031 wird eine durchschnittliche jährliche Wachstumsrate (CAGR) von 5,70 % erwartet.Mit Antibiotika angereicherter Knochenzement wird voraussichtlich weiterhin ein wichtiger Trend auf dem Markt bleiben.

Knochenzement Marktanalyse

Der Wettbewerb zwischen den derzeitigen Anbietern wird sich verstärken, da der Schwerpunkt verstärkt auf der Entwicklung von Knochenzement mit überlegenen Eigenschaften, hoher Qualität und Sicherheit liegt, wie etwa mit Antibiotika angereicherter Knochenzement für Arthroplastik und orthopädische Gelenkfixierungen. Darüber hinaus wächst der Markt aufgrund der zunehmenden Akzeptanz von Verfahren wie Kyphoplastie, Arthroplastik und Vertebroplastie, was das Marktwachstum deutlich steigern dürfte. Darüber hinaus wird erwartet, dass der Markt aufgrund des steigenden Bedarfs an orthopädischem Knochenzement und Gussmaterialien, insbesondere bei älteren Menschen, wächst.

Knochenzement Marktübersicht

Die hohe Häufigkeit von Osteoporose, der steigende Bedarf an Kyphoplastie, Arthroplastik und Vertebroplastie sowie die stark zunehmende Alterung der Bevölkerung tragen alle zur Expansion des Marktes bei. Darüber hinaus haben die Unternehmen ihr Wachstum durch verschiedene anorganische und organische Entwicklungsinitiativen gefördert. Unternehmen haben verschiedene organische Strategien zur Expansion ihrer Geschäfte eingesetzt, beispielsweise Produkteinführungen. Unternehmen haben anorganische Taktiken wie Partnerschaften, Fusionen und Übernahmen eingesetzt.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Knochenzementmarkt: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Treiber und Chancen auf dem Knochenzementmarkt

Steigende Prävalenz von Osteoporose führt zu einer Zunahme von Arthroplastik-, Kyphoplastie- und Vertebroplastie-Eingriffen und begünstigt das Marktwachstum

Das Risiko von Knochenbrüchen wird durch Osteoporose erhöht. Die Zahl der Osteoporosefälle hat in den letzten Jahren zugenommen. So gibt die Internationale Osteoporose-Stiftung an, dass fast jede zweite der befragten Frauen bereits einen osteoporosebedingten Bruch erlitten hat, was diese Brüche zu einem ernsthaften Gesundheitsproblem macht. In Großbritannien leiden etwa vier Millionen Menschen an Osteoporose.

Große Chancen in Entwicklungsregionen

Die Zunahme von Kyphoplastie-, Arthroplastik- und Vertebroplastieoperationen dürfte den Absatz von Knochenzement steigern. Führende Branchenteilnehmer erweitern ihre Produktionskapazitäten und ihre Vertriebsnetze, um ihren Marktanteil in Entwicklungsländern zu erhöhen. Für bedeutende Knochenzementproduzenten werden Wachstumsaussichten in den Schwellenmärkten in Südkorea, Mexiko, Brasilien und Indien erwartet. Die alternde Bevölkerung, die hohe Osteoporoseprävalenz, das steigende verfügbare Einkommen, bessere Gesundheitssysteme und der Ausbau des Medizintourismus in diesen Ländern schaffen lukrative Möglichkeiten. Der asiatisch-pazifische Raum hat sich zu einem flexiblen und geschäftsfreundlichen Zentrum entwickelt. Die meisten Teilnehmer richten ihre Aufmerksamkeit auf die Schwellenmärkte, da die Märkte in den USA und Europa reifen. Die Modernisierung der neuesten Technologien in den Schwellenländern hängt weitgehend von erheblichen Investitionen in die Gesundheits- und Biowissenschaftsforschung ab. Dies wiederum verstärkt die Neigung zur Verwendung von Knochenzement.kyphoplasty, arthroplasty, and

Knochenzement Marktbericht Segmentierungsanalyse

Wichtige Segmente, die zur Ableitung der Knochenzementmarktanalyse beigetragen haben, sind Typ, Anwendung und Endbenutzer.

- Nach Typ ist der Knochenzementmarkt in Polymethylmethacrylat-Zement (PMMA), Calciumphosphat-Zement (CPC) und Glaspolyalkenoat-Zement (GPC) unterteilt. Das Segment Polymethylmethacrylat-Zement (PMMA) hatte im Jahr 2023 den größten Marktanteil.

- Nach Anwendung wird der Markt in Arthroplastik, Kyphoplastie und Vertebroplastie unterteilt. Das Segment Arthroplastik hatte im Jahr 2023 den größten Marktanteil.

- Nach Endverbraucher ist der Markt in Krankenhäuser, ambulante Operationszentren (ASCS) und Kliniken unterteilt. Das Krankenhaussegment hatte im Jahr 2023 den größten Marktanteil.ASCS), and clinics. The hospitals segment held the largest share of the market in 2023.

Knochenzement Marktanteilsanalyse nach Geografie

Der geografische Umfang des Marktberichts für Knochenzement ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Süd- und Mittelamerika.

Der Markt für Knochenzement in den USA hat den größten Marktanteil unter den nordamerikanischen Ländern. Die steigende Zahl an Osteoporosefällen ist der Hauptfaktor, der die Expansion dieses Marktes vorantreibt. In den letzten Jahren wurden zahlreiche Partnerschaften und Joint Ventures zur Ausweitung des US-Marktes für Knochenzement gemeldet. So hat beispielsweise die Kyphon Products Division, eine Abteilung des Spinal- und Biologics-Geschäfts von Medtronic, mit der Einführung des Knochenzements KYPHON ActivOs 10 mit Hydroxylapatit auf dem US-Markt einen bedeutenden Meilenstein erreicht. Mit der Markteinführung dieses Produkts bietet Medtronics Zementportfolio Chirurgen nun eine Alternative zur Behandlung von Patienten mit Wirbelkompressionsfrakturen (VCFs). Daher wird die jüngste Einführung des Knochenzementmarkts in den USA wahrscheinlich das Wachstum des Landes fördern.

Zahlreiche kanadische Unternehmen verfolgen unterschiedliche Ansätze, um die Knochenzementindustrie auszubauen. Die Marktteilnehmer haben verschiedene nachhaltige Strategien umgesetzt, darunter Produkteinführungen, geografische Expansion, Fusionen und Übernahmen sowie strategische Zusammenarbeit. Stryker beispielsweise hat Simplex-Knochenzement eingeführt, um Implantate in verschiedenen orthopädischen und traumachirurgischen Eingriffen zu fixieren.

Regionale Einblicke in den Knochenzementmarkt

Die regionalen Trends und Faktoren, die den Knochenzementmarkt während des Prognosezeitraums beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch Knochenzementmarktsegmente und die Geografie in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Knochenzementmarkt

Umfang des Marktberichts zu Knochenzement

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2023 | 1,23 Milliarden US-Dollar |

| Marktgröße bis 2031 | 1,92 Milliarden US-Dollar |

| Globale CAGR (2023 - 2031) | 5,70 % |

| Historische Daten | 2021-2022 |

| Prognosezeitraum | 2024–2031 |

| Abgedeckte Segmente |

Nach Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmerdichte: Der Einfluss auf die Geschäftsdynamik

Der Markt für Knochenzement wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung von Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten auf dem Knochenzementmarkt tätigen Unternehmen sind:

- Zimmer Biomet

- DePuy Synthes

- Smith & Neffe

- DJO Global, Inc

- Arthrex, Inc

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Knochenzementmarkt

Neuigkeiten und aktuelle Entwicklungen zum Knochenzementmarkt

Der Knochenzementmarkt wird durch die Erhebung qualitativer und quantitativer Daten nach Primär- und Sekundärforschung bewertet, die wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken umfasst. Nachfolgend sind einige der Entwicklungen auf dem Knochenzementmarkt aufgeführt:

- OsteoRemedies(R) LLC, ein orthopädisches Unternehmen, das sich auf die Bereitstellung einfacher Lösungen für komplexe Erkrankungen konzentriert, hat die FDA-Zulassung für erweiterte Indikationen für den SPECTRUM(R) GV Knochenzement bekannt gegeben. Die erweiterte Indikation umfasst die Fixierung von Revisionskomponenten für Hüftarthroplastiken, die in der zweiten Phase einer zweistufigen Revision implantiert werden, nachdem die anfängliche Infektion abgeklungen ist. (Quelle: OsteoRemedies(R) LLC, Pressemitteilung, April 2024)

- Zimmer Biomet gewann einen Fall vor der US-amerikanischen International Trade Commission, in dem das Unternehmen beschuldigt wurde, Geschäftsgeheimnisse von Heraeus für Knochenzement gestohlen zu haben. Dabei handelt es sich um eine Verbindung, mit der die Lücke zwischen einem künstlichen Gelenk und einem Knochen gefüllt wird. Die Kommission lehnte den Antrag der Heraeus Holding ab, die Einfuhr von in Frankreich hergestelltem Refobacin-Knochenzement zu blockieren, der mit dem Produkt PALACOS von Heraeus konkurriert. (Quelle: Zimmer Biomet, Pressemitteilung, Januar 2021)

Marktbericht zu Knochenzement – Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für Knochenzement (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Knochenzementmarktgröße und -prognose auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt sind

- Knochenzement-Markttrends sowie Marktdynamik wie Treiber, Einschränkungen und wichtige Chancen

- Detaillierte PEST/Porters Five Forces- und SWOT-Analyse

- Marktanalyse für Knochenzement, die wichtige Markttrends, globale und regionale Rahmenbedingungen, wichtige Akteure, Vorschriften und aktuelle Marktentwicklungen umfasst.

- Branchenlandschaft und Wettbewerbsanalyse, die die Marktkonzentration, Heatmap-Analyse, prominente Akteure und aktuelle Entwicklungen für den Knochenzementmarkt umfasst

- Detaillierte Firmenprofile

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends