Marktgröße, Marktanteil und Trends für Industriearmaturen bis 2034

Marktgröße und Prognose für Industriearmaturen (2021–2034), globaler und regionaler Marktanteil, Trend- und Wachstumschancenanalyse. Berichtsabdeckung: Nach Typ (Kugelhähne, Absperrklappen, Sicherheitsventile, Regelventile, Rückschlagventile, Kegelventile und Sonstige), Größe (bis 5 Zoll, 6–5 Zoll, 16–24 Zoll und über 25 Zoll), Klasse (150, 300, 400, 600, 800, 900, 1500 und 2500) und Branche (Öl und Gas, LNG, Wasseraufbereitung, Energie, Chemie und Petrochemie und Sonstige).

- Status : Veröffentlicht

- Berichtscode : TIPMC00002517

- Kategorie : Fertigung und Bau

- Anzahl der Seiten : 310

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : April 20, 2026

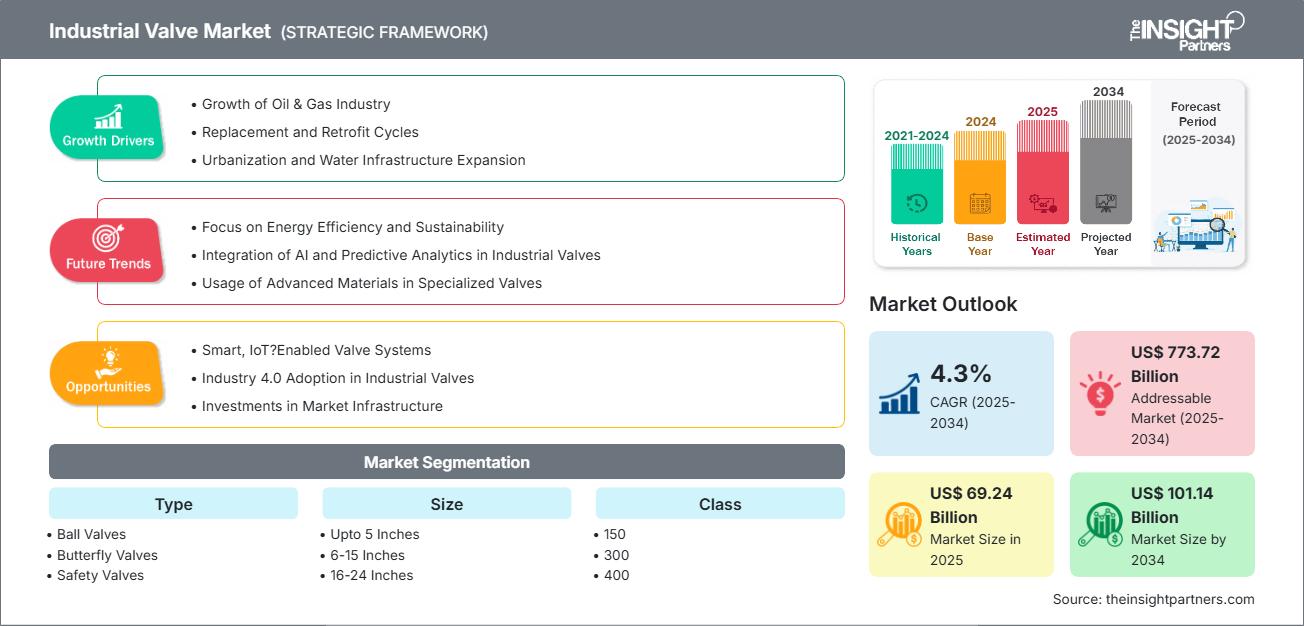

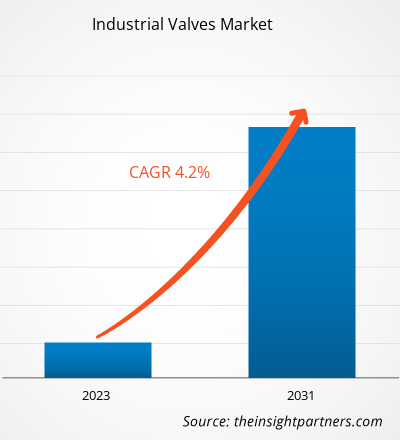

Der Markt für Industriearmaturen wird bis 2034 voraussichtlich ein Volumen von 101,14 Milliarden US-Dollar erreichen, gegenüber 69,24 Milliarden US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Zeitraum 2026–2034 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 4,3 % verzeichnen wird.

Marktanalyse für Industriearmaturen

Der Markt wird durch Faktoren wie die zunehmende Industrialisierung, den Ausbau der Infrastruktur, die Einführung von Automatisierungs- und Industrie-4.0-Technologien, steigende Energieeffizienz- und Nachhaltigkeitsstandards sowie die Erneuerung veralteter Infrastruktur angetrieben. Die wachsende Nachfrage aus Schwellenländern, verbunden mit Investitionen in fortschrittliche und leistungsstarke Ventillösungen, beflügelt das Marktwachstum zusätzlich.

Marktübersicht für Industriearmaturen

Der Markt für Industriearmaturen umfasst die Entwicklung, Herstellung und den Vertrieb von Ventilen zur Steuerung, Regelung und Lenkung des Durchflusses von Flüssigkeiten, Gasen und Suspensionen in verschiedenen Industriezweigen. Ventile sind eine entscheidende Komponente industrieller Systeme für einen sicheren, effizienten und zuverlässigen Betrieb. Kugelventile, Schieberventile, Absperrventile, Absperrklappen, Rückschlagventile und Regelventile gehören zu den gängigsten Ventiltypen. Jeder Ventiltyp besitzt spezifische Eigenschaften, die für bestimmte Durchflussregelungsanwendungen, Drücke und Temperaturen optimiert werden können.

Der Wert von Industriearmaturen liegt in ihrer Fähigkeit, die Systemintegrität zu gewährleisten, Leckagen zu verhindern, den Druck in Prozessen zu regulieren und einen effizienten Prozessablauf zu ermöglichen. Armaturen sind äußerst vielseitig und werden in großem Umfang in der Öl- und Gasindustrie, der Petrochemie, der Energieerzeugung, der Wasser- und Abwasserwirtschaft, der Chemie-, Pharma- sowie der Lebensmittel- und Getränkeindustrie eingesetzt. In diesen Branchen spielen Armaturen eine entscheidende Rolle für die Betriebssicherheit, die Produktqualität und die Einhaltung von Umweltauflagen.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für Industriearmaturen: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Treiber und Chancen des Marktes für Industriearmaturen

Markttreiber:

- Wachstum der Öl- und Gasindustrie: Industriearmaturen spielen eine entscheidende Rolle bei der Regulierung, Lenkung und Kontrolle des Flüssigkeits- und Gasflusses in verschiedenen Phasen der Energieerzeugung und -verteilung.

- Austausch- und Modernisierungszyklen: Ventile unterliegen Verschleiß, Korrosion und Leistungsverschlechterung, was die Sicherheit, Effizienz und die Einhaltung moderner Normen beeinträchtigen kann. Daher investieren Unternehmen verstärkt in den Austausch von Ventilen, um die Betriebssicherheit zu gewährleisten.

- Urbanisierung und Ausbau der Wasserinfrastruktur: Mit dem Wachstum der Städte und der Zunahme der Bevölkerung steigt auch der Bedarf an zuverlässiger Wasserversorgung, Abwasserentsorgung und Abwassersystemen.

- Anforderungen an Automatisierung und Prozesseffizienz: Trends in der industriellen Automatisierung gehen hin zu einer verstärkten Nutzung von betätigten und intelligenten Kugelventilen, um die betriebliche Effizienz zu steigern und manuelle Eingriffe zu reduzieren.

- Strenge Umwelt- und Sicherheitsvorschriften: Regierungen schreiben Emissionskontrolle und Leckageverhütung vor und drängen die Industrie zur Einführung fortschrittlicher, hochintegrierter Ventilsysteme.

Marktchancen:

- Intelligente und IoT-fähige Ventilsysteme: Intelligente Ventile integrieren fortschrittliche Sensoren, maschinelles Lernen und Konnektivität, um eine präzise Steuerung von Durchfluss, Druck und Ressourcenverteilung zu ermöglichen.

- Einführung von Industrie 4.0 bei Industriearmaturen: Die Integration intelligenter Systeme, Sensoren und fortschrittlicher Datenanalysen im Rahmen von Industrie 4.0 ermöglicht es den Herstellern, Produktionsprozesse zu optimieren, die Produktqualität zu verbessern und das Risiko menschlicher Fehler zu reduzieren.

- Investitionen in die Marktinfrastruktur: Schwellenländer – insbesondere im asiatisch-pazifischen Raum – bieten aufgrund umfangreicher Kapitalinvestitionen in Infrastrukturprojekte erhebliche Chancen für den Markt für Industriearmaturen.

- Modernisierung von Pipelines und Ausbau der Infrastruktur: Der Ersatz veralteter Infrastruktur und die Installation neuer Pipelines schaffen eine stetige, langfristige Nachfrage.

- Kundenspezifische Lösungen und anwendungsspezifische Lösungen: Die steigende Nachfrage nach maßgeschneiderten Ventilen für Nischenbranchen (Halbleiter, Spezialchemikalien) bietet margenstarke Möglichkeiten.

Marktbericht für Industriearmaturen: Segmentierungsanalyse

Der Markt für Industriearmaturen ist in verschiedene Kategorien unterteilt, um ein detailliertes Verständnis von Typ, Größe, Klasse und Branchenspezifikationen zu ermöglichen:

Nach Typ:

- Kugelhahn: Kugelhähne werden aufgrund ihrer einfachen Bauweise, Zuverlässigkeit und starken Dichtungsleistung in industriellen Anwendungen häufig eingesetzt.

- Absperrklappe: Absperrklappen sind Vierteldrehventile, die sich durch ihre kompakte Bauweise, ihr geringes Gewicht und ihre Kosteneffizienz auszeichnen. Sie werden häufig in der Wasserverteilung, der Abwasserbehandlung, in HLK-Anlagen und in bestimmten chemischen Prozessen eingesetzt.

- Sicherheitsventile: Sicherheitsventile sind kritische Bauteile, die Anlagen, Systeme und Personal durch automatische Druckentlastung schützen. Sie finden breite Anwendung in Branchen wie der Öl- und Gasindustrie, der Energieerzeugung, der chemischen Industrie und der Fertigungsindustrie, wo Druckaufbau zu gefährlichen Situationen führen kann.

- Regelventile: Regelventile dienen der Regulierung von Durchfluss, Druck, Temperatur und Füllständen in industriellen Prozessen. Sie spielen eine entscheidende Rolle in Automatisierungssystemen, indem sie auf Signale von Steuerungen reagieren und die Prozessbedingungen in Echtzeit anpassen.

- Rückschlagventile: Rückschlagventile sind Ventile, die den Durchfluss von Flüssigkeiten in eine Richtung ermöglichen und gleichzeitig einen Rückfluss verhindern. Sie arbeiten automatisch ohne manuelle Eingriffe und nutzen Druckunterschiede zum Öffnen und Schließen.

- Kegelventile: Kegelventile sind Vierteldrehventile, die einen zylindrischen oder konischen Kegel zur Steuerung des Flüssigkeitsdurchflusses verwenden. Sie zeichnen sich durch ihre einfache Konstruktion, schnelle Bedienung und dichte Absperrung aus.

- Sonstige: Das Segment „Sonstige“ im Markt für Industriearmaturen umfasst eine Vielzahl spezialisierter Ventile wie Schieber, Membranventile, Nadelventile und Quetschventile. Diese Ventile sind für spezifische Anwendungsanforderungen konzipiert, die von gängigen Ventiltypen möglicherweise nicht vollständig abgedeckt werden.

Nach Größe:

- Bis zu 5 Zoll

- 6-15 Zoll

- 16-24 Zoll

- Über 25 Zoll

Nach Klassen:

- 150

- 300

- 400

- 600

- 800

- 900

- 1500

- 2500

Nach Branchen:

- Öl und Gas

- LNG

- Wasseraufbereitung

- Strom und Energie

- Chemie und Petrochemie

- Andere

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Lateinamerika

- Naher Osten und Afrika

Umfang des Marktberichts zu Industriearmaturen

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 69,24 Milliarden US-Dollar |

| Marktgröße bis 2034 | 101,14 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2025 - 2034) | 4,3 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2025–2034 |

| Abgedeckte Segmente |

Nach Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte im Bereich Industriearmaturen: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Industriearmaturen wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile der Produkte. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Kundenbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

Marktanteilsanalyse für Industriearmaturen nach Regionen

Der asiatisch-pazifische Raum – ein wichtiger Standort der Automobilindustrie – verzeichnet das schnellste Marktwachstum. Schwellenländer in Lateinamerika, dem Nahen Osten und Afrika bieten zahlreiche ungenutzte Chancen für Anbieter von Industriearmaturen.

Der Markt für Industriearmaturen weist in den verschiedenen Regionen unterschiedliche Wachstumsraten auf. Nachfolgend finden Sie eine Zusammenfassung der Marktanteile und Trends nach Regionen:

1. Nordamerika

- Starke Investitionen in die Öl- und Gasinfrastruktur, die Schiefergasexploration und die Modernisierung von Pipelines treiben die Nachfrage nach Industriearmaturen an. Die zunehmende Automatisierung, intelligente Ventile und strenge Umweltauflagen beschleunigen das Marktwachstum zusätzlich.

- Der zunehmende Fokus auf die Modernisierung der Wasser- und Abwasseraufbereitung sowie die Erneuerung veralteter Infrastruktur fördern die Verbreitung von Ventilen. Digitalisierungstrends, darunter IIoT-fähige Überwachungssysteme, verbessern Effizienz, Sicherheit und vorausschauende Wartung branchenübergreifend.

2. Europa

- Strenge Umweltauflagen und Dekarbonisierungsziele treiben die Einführung fortschrittlicher Ventile in Projekten für erneuerbare Energien, Wasserstoff und Emissionskontrollsystemen voran, insbesondere in den Bereichen Chemie, Energieerzeugung und industrielle Verarbeitung.

- Der Ausbau von Initiativen zur Energiewende, darunter Offshore-Windkraft und grüner Wasserstoff, treibt die Nachfrage an. Der Fokus auf hohe technische Standards und Lebenszykluseffizienz fördert die Einführung intelligenter, korrosionsbeständiger und energieeffizienter Ventiltechnologien.

3. Asien-Pazifik

- Die rasante Industrialisierung, Urbanisierung und der Ausbau der Infrastruktur in Ländern wie China und Indien führen zu einer großen Nachfrage nach Industriearmaturen in den Bereichen Energie, Wasseraufbereitung, Öl und Gas sowie im verarbeitenden Gewerbe.

- Steigende Investitionen in intelligente Fabriken und Automatisierungstechnologien fördern die Verbreitung intelligenter Ventile. Darüber hinaus unterstützen ein wachsendes Umweltbewusstsein und strengere regulatorische Vorgaben das Wachstum in den Bereichen Abwassermanagement und saubere Energieanwendungen.

4. Süd- und Mittelamerika

- Die Ausweitung der Öl- und Gasexploration, insbesondere der Offshore-Projekte, treibt die Nachfrage nach Ventilen an. Auch das Wachstum des Bergbausektors trägt maßgeblich dazu bei, da dieser robuste Ventile für den Umgang mit abrasiven und Hochdruckumgebungen benötigt.

- Die Verbesserung der Infrastruktur in der Wasseraufbereitung und im Energiesektor fördert die Akzeptanz. Steigende ausländische Investitionen und die schrittweise Modernisierung der Industrie begünstigen die Einführung automatisierter und effizienter Ventilsysteme in Schwellenländern.

5. Naher Osten und Afrika

- Die Dominanz des Öl- und Gassektors, einschließlich der Expansionen im Upstream- und Downstream-Bereich, bleibt der Haupttreiber. Megaprojekte in den Bereichen Raffinerien, Petrochemie und Pipelines erhöhen die Nachfrage nach langlebigen, leistungsstarken Industriearmaturen erheblich.

- Steigende Investitionen in Entsalzungsanlagen und Wasserinfrastruktur aufgrund von Wasserknappheit fördern die Verbreitung von Ventilen. Diversifizierungsbestrebungen in erneuerbare Energien und Industriesektoren schaffen darüber hinaus neue Möglichkeiten für fortschrittliche Ventiltechnologien.

Hohe Marktdichte und starker Wettbewerb

Der Wettbewerb ist aufgrund der Präsenz etablierter Unternehmen wie Emerson Electric Co (USA), Flowserve Corp (USA) und SLB Limited (USA) stark. Regionale und spezialisierte Anbieter wie Crane Co (USA) und KITZ Corporation (Japan) tragen ebenfalls zur Wettbewerbslandschaft in den verschiedenen Regionen bei.

Ein stark wettbewerbsorientiertes Umfeld zwingt Unternehmen dazu, einzigartige Produkte und Dienstleistungen anzubieten, darunter:

- Vertikale Integration und Skalierung

- Technologische Partnerschaft

- Geografischer Fußabdruck

Chancen und strategische Schritte

- Konsolidierung durch Fusionen und Übernahmen

- Investitionen in Automatisierung

- Diversifizierung in wachstumsstarke Branchen

- Nachhaltigkeit und umweltfreundliche Lösungen

Die wichtigsten Unternehmen auf dem Markt für Industriearmaturen sind:

- Emerson Electric Co (USA)

- Flowserve Corp (USA)

- SLB Limited (USA)

- Crane Co (USA)

- KITZ Corporation (Japan)

- Velan Inc (Kanada)

- Spirax Group plc (UK)

- The Weir Group PLC (Schottland)

- Circor International Inc (USA)

- Neway Valve (Suzhou) Co.,Ltd (China)

Weitere im Rahmen der Studie analysierte Unternehmen:

- KSB SE & Co. KGaA

- AVK Holdings

- Die Lee Company

- RED-WHITE VALVE CORP.

- Alsco Industrieprodukte

- JLX-Ventil

- Curtiss-Wright

- LUMACO HYGIENEVENTILE

- IPEX Unternehmensgruppe

- Xylem, Inc.

- Motion Industries, Inc.

- Schenck Process Holding GmbH

- Alfa Laval Inc.

- EBARA Technologies, Inc.

- Pentair

- Stäubli International AG

- Barnes Group Inc.

- TRIVACO Tristate Valves & Controls, Inc

- Bi-Torq Ventilautomatisierung

- PARKER HANNIFIN CORP

Hinweis: Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge geordnet.

Neuigkeiten und aktuelle Entwicklungen auf dem Markt für Industriearmaturen

- Crane Fluid Systems unterstützt die Sanierung von 7 Millbank in London: Im Dezember 2025 unterstützte Crane Fluid Systems die Sanierung von 7 Millbank in London und lieferte Skanska UK ein umfassendes Sortiment an Ventilen und technischen Lösungen für das Projekt.

- Emerson stellt das Anderson Greenwood Druckbegrenzungsventil Typ 84 vor: Im Februar 2025 präsentierte die Emerson Electric Co. das Anderson Greenwood Druckbegrenzungsventil Typ 84, das speziell zum Schutz von Tanks und Behältern für Wasserstoff und andere Hochdruckgasanwendungen entwickelt wurde. Dank der thermoplastischen Dichtung aus Arlon 3000XT und der Spindel aus Edelstahl ASME SA-479 Typ S21800 bietet das Druckbegrenzungsventil Typ 84 herausragende Dichtheit, Beständigkeit gegen Versprödung, optimale Dichtheit, hohe Zuverlässigkeit und lange Lebensdauer.

Marktbericht für Industriearmaturen: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für Industriearmaturen (2021–2034)“ bietet eine detaillierte Analyse des Marktes und deckt folgende Bereiche ab:

- Marktgröße und Prognose für Industriearmaturen auf globaler, regionaler und Länderebene für alle abgedeckten Segmente

- Trends im Markt für Industriearmaturen sowie Dynamiken wie Treiber, Hemmnisse und wichtige Chancen

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für Industriearmaturen: Wichtige Trends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Rahmenbedingungen und aktuelle Marktentwicklungen

- Branchenlandschafts- und Wettbewerbsanalyse mit Marktkonzentration, Heatmap-Analyse, führenden Akteuren und aktuellen Entwicklungen im Markt für Industriearmaturen

- Detaillierte Unternehmensprofile

Nivedita ist eine versierte Forschungsexpertin mit über 9 Jahren Erfahrung in Marktforschung und Unternehmensberatung. Sie ist derzeit als Projektmanagerin im IKT-Bereich bei The Insight Partners tätig und verfügt über umfassende Fachkenntnisse in der Leitung und Durchführung von syndizierten, kundenspezifischen, abonnementbasierten und beratenden Forschungsaufträgen in unterschiedlichen Technologiesektoren.

Mit einer nachgewiesenen Erfolgsbilanz bei der Bereitstellung datengestützter Analysen und umsetzbarer Erkenntnisse war Nivedita maßgeblich an mehreren kritischen Projekten beteiligt. Ihre Arbeit umfasst die vollständige Projektabwicklung – vom Verständnis der Kundenziele über die Analyse von Markttrends bis hin zur Ableitung strategischer Empfehlungen. Sie hat umfassend mit führenden IKT-Unternehmen zusammengearbeitet und ihnen geholfen, Marktchancen zu erkennen und Branchenveränderungen zu meistern.

Nivedita hat einen MBA in Management vom IMS, Dehradun. Vor ihrem Eintritt bei The Insight Partners sammelte sie wertvolle Erfahrungen bei MarketsandMarkets und Future Market Insights in Pune, wo sie verschiedene Forschungspositionen innehatte und sich ein solides Fundament in Branchenanalyse und Kundenbindung erarbeitete.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends