Markt für Knochenersatzmaterialien in der Zahnmedizin: Trends, Nachfrage und Wachstumsaussichten bis 2034

Marktgröße und Prognose für Knochenersatzmaterialien in der Zahnmedizin (2021–2034), globaler und regionaler Marktanteil, Trend- und Wachstumschancenanalyse. Berichtsabdeckung: Nach Typ (Allotransplantat, Autotransplantat, Xenotransplantat, synthetisches Knochentransplantat und Sonstige), Anwendung (Alveolenerhaltung, Kieferkammaufbau, Regeneration von Parodontaldefekten, Implantat-Knochenregeneration und Sonstige), Endnutzer (Krankenhäuser, Kliniken und Sonstige) und Geografie (Nordamerika, Europa, Asien-Pazifik, Naher Osten und Afrika sowie Süd- und Mittelamerika).

- Status : Veröffentlicht

- Berichtscode : TIPRE00022571

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 329

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : April 14, 2026

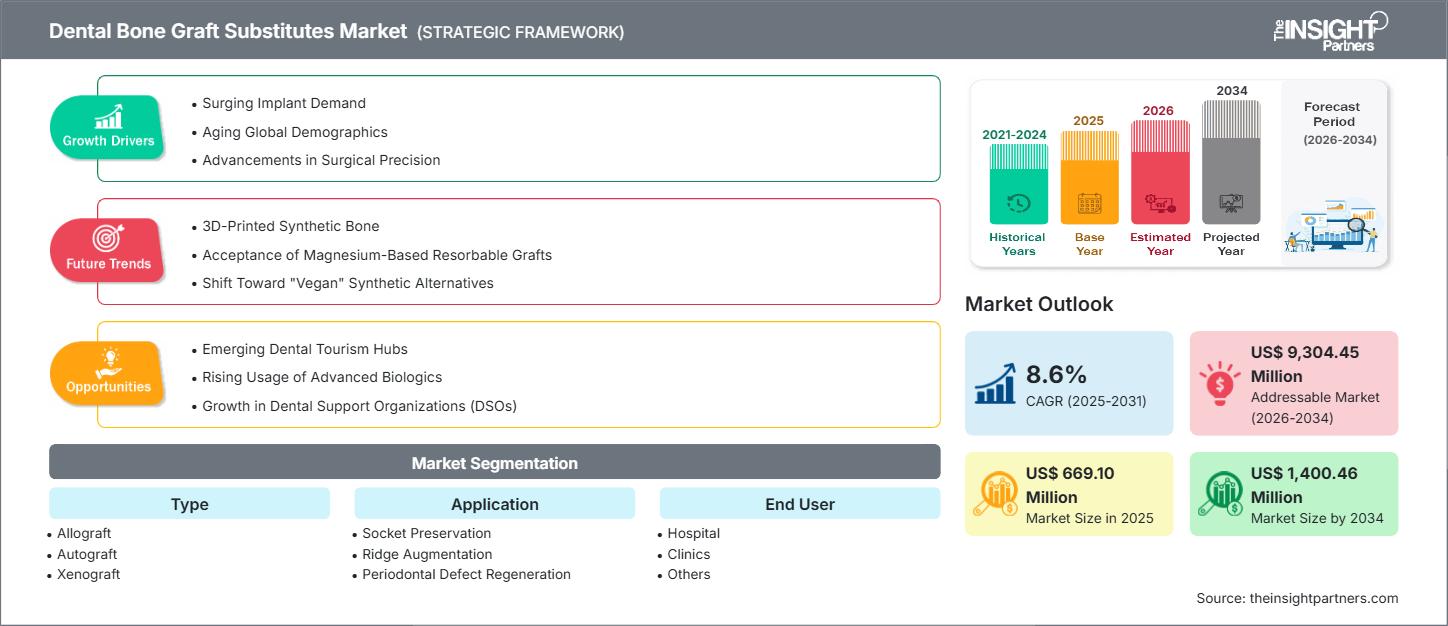

Der Markt für Knochenersatzmaterialien in der Zahnmedizin wird bis 2034 voraussichtlich ein Volumen von 1.400,5 Millionen US-Dollar erreichen, gegenüber 669,1 Millionen US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Zeitraum 2026–2034 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 8,6 % verzeichnen wird.

Marktanalyse für Knochenersatzmaterialien in der Zahnmedizin

Das Marktwachstum wird durch die steigende Nachfrage nach Implantaten, die alternde Weltbevölkerung und Fortschritte in der chirurgischen Präzision angetrieben. Darüber hinaus dürften neu entstehende Zentren für Zahntourismus, der zunehmende Einsatz moderner Biologika und das Wachstum zahnärztlicher Versorgungszentren (DSOs) zahlreiche neue Möglichkeiten eröffnen.

Marktübersicht für Knochenersatzmaterialien in der Zahnmedizin

Der Markt für Knochenersatzmaterialien in der Zahnmedizin erlebt einen enormen Boom. Diese Materialien werden zur Substitution menschlicher Knochen bei Zahnimplantaten, zur Parodontalregeneration und bei komplexen oralchirurgischen Eingriffen eingesetzt. Der Markt entwickelt sich um die verschiedenen Materialarten, die bei Autografts, Allografts, Xenografts und synthetischen Transplantaten verwendet werden. Jedes dieser Materialien bietet Vorteile hinsichtlich Biokompatibilität, Osteokonduktivität und Regenerationsfähigkeit. Zu den neuesten Entwicklungen auf diesem Gebiet zählen 3D-gedruckte Gerüste, Kombinationstherapien und mit Wachstumsfaktoren angereicherte Transplantate. Diese eröffnen nicht nur neue Anwendungsgebiete, sondern beschleunigen auch den Heilungsprozess der Patienten. Dadurch werden Knochenersatzmaterialien zu einem fundamentalen Bestandteil moderner regenerativer Zahnmedizin.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für Knochenersatzmaterialien in der Zahnmedizin: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen für dentale Knochentransplantat-Ersatzstoffe

Markttreiber:

- Steigende Nachfrage nach Implantaten: Die zunehmende Akzeptanz von Zahnimplantaten als primäre Wahl bei Zahnverlust ist ein wesentlicher Faktor für die erhöhte Nachfrage nach Knochenersatzmaterialien, da das Vorhandensein von ausreichend Knochen für den Erfolg der Implantation und die langfristige Stabilität von entscheidender Bedeutung ist.

- Alternde Weltbevölkerung: Der allmähliche Anstieg der älteren Bevölkerung, die anfälliger für Zahnverlust und Zahnfleischerkrankungen ist, ist einer der Gründe für die zunehmende Anwendung von Zahntransplantationsverfahren, nicht nur in der rekonstruktiven Zahnheilkunde, sondern auch bei der allgemeinen Wiederherstellung der Mundgesundheit weltweit.

- Fortschritte in der chirurgischen Präzision: Die Kombination aus navigierter Chirurgie, digitaler Bildgebung und ähnlichen Technologien hat es erleichtert, das Transplantat präzise zu platzieren, was zu besseren klinischen Ergebnissen, kürzeren Erholungszeiten und einem vermehrten Einsatz von hochentwickelten Knochentransplantatersatzstoffen in der Zahnchirurgie führt.

Marktchancen:

- Neue Zentren für Zahntourismus: Der Aufstieg des Medizin- und Zahntourismus in Regionen, die eine kostengünstige und qualitativ hochwertige Gesundheitsversorgung bieten, führt zu einem erhöhten Bedarf an Knochentransplantationen.

- Zunehmender Einsatz von Biologika: Die Integration von Wachstumsfaktoren, Stammzellen und bioaktiven Molekülen in Knochentransplantate verbessert die Ergebnisse des Regenerationsverfahrens signifikant. Daher bietet die Anwendung von Biologika in der Zahnchirurgie dem Dentalsektor ein erhebliches Wachstumspotenzial.

- Wachstum bei zahnärztlichen Unterstützungsorganisationen (DSOs): Die kontinuierliche Weiterentwicklung der DSOs führt zum Zusammenschluss von Zahnarztpraxen, zur Vereinheitlichung der Abläufe und zu einer Zunahme der Anzahl von Implantat- und Knochenaufbauoperationen.

Marktbericht zu Knochenersatzmaterialien für die Zahnheilkunde: Segmentierungsanalyse

Der Markt für Knochenersatzmaterialien in der Zahnmedizin ist in verschiedene Segmente unterteilt, um einen besseren Überblick über seine Funktionsweise, sein Wachstumspotenzial und die neuesten Trends zu geben. Nachfolgend ist der in Branchenberichten übliche Segmentierungsansatz dargestellt:

Nach Typ:

- Allotransplantate: Allotransplantate sind in der Zahnmedizin und Chirurgie ein gängiges Verfahren, bei dem menschliches Knochengewebe von Spendern verwendet wird. Ihre Biokompatibilität und klinische Zuverlässigkeit sind ihre Stärken, weshalb sie dank verbesserter Verarbeitung und erhöhter Sicherheit bei der Kieferkammaugmentation, der Alveolenpräservation und der Parodontalregeneration eingesetzt werden.

- Autotransplantat: Bei Autotransplantaten handelt es sich um Knochenmaterial des Patienten selbst, das die höchste biologische Aktivität bietet, aber auch die stärksten Schmerzen und Beschwerden an der Entnahmestelle verursacht, weshalb Kliniker aus Gründen des Komforts und der Bequemlichkeit nach Alternativen suchen.

- Xenotransplantate: Xenotransplantate, die typischerweise von Rindern oder Schweinen stammen, haben aufgrund ihrer strukturellen Ähnlichkeit mit menschlichen Knochen weltweite Akzeptanz erlangt, da sie sich bei der Erhaltung der Alveole und der Entwicklung des Implantatbetts als robust erwiesen haben.

- Synthetisches Knochentransplantat: Synthetische Transplantate werden aus künstlich hergestellten Biomaterialien wie Hydroxylapatit und bioaktivem Glas gefertigt und bieten eine leicht verfügbare, nicht infektionsgefährdende Lösung mit anpassbaren Eigenschaften.

- Sonstige: Die Kategorie „Sonstige“ umfasst sowohl Komposit- als auch innovative biologische oder künstliche Transplantate, die sowohl Materialien als auch Wachstumsfaktoren nutzen, um eine komplexe Regeneration zu unterstützen und dadurch bessere klinische Ergebnisse zu erzielen.

Auf Antrag:

- Sockelerhaltung

- Kammverstärkung

- Regeneration von Parodontaldefekten

- Implantat-Knochenregeneration

- Andere

Vom Endbenutzer:

- Krankenhaus

- Kliniken

- Andere Endnutzer

Jeder Endnutzer hat unterschiedliche Bedürfnisse hinsichtlich Handhabung, Sicherheit und Vorschriften, was wiederum Einfluss auf die Produktauswahl, die klinischen Arbeitsabläufe und die Verfahrensprotokolle hat.

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Lateinamerika

- Naher Osten und Afrika

Umfang des Marktberichts über Knochenersatzmaterialien für die Zahnheilkunde

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 669,10 Millionen US-Dollar |

| Marktgröße bis 2034 | 1.400,46 Millionen US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2025 - 2034) | 8,6 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nach Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmer im Bereich der Knochenersatzmaterialien für die Zahnheilkunde: Dichte und ihre Auswirkungen auf die Geschäftsdynamik

Der Markt für Knochenersatzmaterialien in der Zahnmedizin wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Kundenbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

Marktanteilsanalyse für dentale Knochentransplantat-Ersatzstoffe nach Regionen

Der Markt für Knochenersatzmaterialien in der Zahnmedizin im asiatisch-pazifischen Raum dürfte aufgrund der weltweit zunehmenden Zahnerkrankungen das schnellste Wachstum verzeichnen. Schwellenländer in Lateinamerika, dem Nahen Osten und Afrika bieten Anbietern von zahnmedizinischen Geräten zahlreiche ungenutzte Expansionsmöglichkeiten.

Der Markt für Knochenersatzmaterialien in der Zahnmedizin entwickelt sich regional unterschiedlich, da Wirtschaftswachstum und steigende Gesundheitsausgaben die Bezahlbarkeit zahnärztlicher Eingriffe verbessert haben. Nachfolgend finden Sie eine Zusammenfassung der Marktanteile und Trends nach Region:

1. Nordamerika

- Marktanteil: Besitzt einen bedeutenden Anteil am Weltmarkt

-

Wichtigste Einflussfaktoren:

- Eine starke klinische Akzeptanz, eine fortschrittliche Infrastruktur für die zahnärztliche Versorgung und eine hohe Nachfrage nach Implantaten sind die Haupttreiber des Wachstums, während Innovation, Unterstützung durch die Kostenerstattung und die Präferenz der Zahnärzte für fortschrittliche Transplantate die Hauptfaktoren für eine robuste Marktexpansion darstellen.

- Trends: Die Präferenz für hochwertige Knochentransplantatersatzstoffe wird durch die hohe Akzeptanz von Implantaten und den Einsatz fortschrittlicher regenerativer Technologien vorangetrieben.

2. Europa

- Marktanteil: Bedeutender Anteil aufgrund der frühen Einführung von Knochentransplantatersatzstoffen im Zahnbereich

-

Wichtigste Einflussfaktoren:

- Gute zahnärztliche Leistungen, eine alternde Bevölkerung und strenge regulatorische Standards sind die Hauptfaktoren für die Akzeptanz; zunehmende Implantatverfahren und die Präferenz für minimalinvasive Knochentransplantationslösungen sind die Hauptfaktoren für die stetige Marktentwicklung.

- Trends: Die Akzeptanz des Produkts wird durch die steigende Nachfrage nach minimalinvasiven Transplantationen und die Einhaltung hoher Qualitätsstandards beeinflusst.

3. Asien-Pazifik

- Marktanteil: Am schnellsten wachsende Region mit jährlich steigenden Marktanteilen.

-

Wichtigste Einflussfaktoren:

- Das rasante Wachstum des Zahntourismus, das steigende Bewusstsein für Mundgesundheit, eine wachsende Mittelschicht und die zunehmende Anzahl von Implantaten sind einige der Faktoren, die die Marktnachfrage begünstigen; China, Indien und Südostasien sind starke Märkte in Bezug auf die Akzeptanz.

- Trends: Die Verwendung von Transplantatersatz wird durch den rasanten Anstieg des Zahntourismus und den breiteren Zugang zur zahnärztlichen Versorgung begünstigt.

4. Süd- und Mittelamerika

- Marktanteil: Stetig wachsender Marktanteil

-

Wichtigste Einflussfaktoren:

- Die Verbesserung der zahnärztlichen Leistungen, die steigende Nachfrage nach Implantaten und die Gründung weiterer Privatkliniken tragen zum Wachstum des Marktes bei.

- Trends: Zunehmende Anzahl von Zahnimplantaten und die Expansion privater Kliniken.

5. Naher Osten und Afrika

- Marktanteil: Geringer Marktanteil, der jedoch rasant wächst

-

Wichtigste Einflussfaktoren:

- Eine bessere zahnärztliche Infrastruktur, höhere Investitionen in spezialisierte Behandlungen und ein größeres Bewusstsein für moderne Transplantatmaterialien sind die Hauptgründe für das langsame Marktwachstum, insbesondere in den Ländern des Golf-Kooperationsrats (GCC) und in städtischen Gebieten.

- Trends: Investitionen in eine moderne zahnärztliche Infrastruktur erleichtern den Einsatz fortschrittlicher Knochentransplantationslösungen.

Marktteilnehmer im Bereich der Knochenersatzmaterialien für die Zahnheilkunde: Dichte und ihre Auswirkungen auf die Geschäftsdynamik

Hohe Marktdichte und starker Wettbewerb

Der Wettbewerb ist aufgrund der Präsenz etablierter Unternehmen wie Dentsply Sirona Inc., Geistlich Pharma AG, ZimVie Inc. und Straumann Holding AG stark. Auch regionale und spezialisierte Anbieter tragen zur Wettbewerbslandschaft bei.

Dieser hohe Wettbewerbsdruck zwingt Unternehmen dazu, sich durch folgende Angebote von der Konkurrenz abzuheben:

- Erweiterte Sicherheitsfunktionen

- Mehrwertdienste wie Analytik und vorausschauende Wartung, operative Echtzeitanalysen und Installation

- Wettbewerbsfähige Preismodelle

- Starker Kundensupport und einfache Integration

Chancen und strategische Schritte

- Unternehmen investieren verstärkt in Forschung und Entwicklung, was Innovationen bei Detektionstechnologien vorantreibt. Dies verbessert auch Sensitivität und Spezifität und ermöglicht die Behandlung spezifischer zahnmedizinischer Probleme in verschiedenen Regionen.

- Die Hersteller werden sich voraussichtlich auf die lokale Produktion konzentrieren, um Kosten zu senken und die Lieferketten zu stärken, insbesondere in Märkten mit hohem Absatzvolumen wie Indien.

Weitere im Rahmen der Studie analysierte Unternehmen:

- Botiss Biomaterials GmbH

- NovaBone Products LLC

- Collagen Matrix Inc.

- RTI Chirurgie

- Graftys SA

- Dentium Co. Ltd.

- Maxigen Biotech Inc.

- REGEDENT AG

- Unicare Biomedical, Inc.

- Neoss Ltd.

Marktneuigkeiten und aktuelle Entwicklungen im Bereich zahnärztlicher Knochenersatzmaterialien

- Orthofix gibt die 510(k)-Zulassung und die vollständige Markteinführung von OsteoCove bekannt, einem fortschrittlichen bioaktiven synthetischen Implantat für Wirbelsäulen- und orthopädische Eingriffe: Im Oktober 2023 brachte Orthofix Medical Inc. OsteoCove, ein fortschrittliches bioaktives synthetisches Implantat, auf den Markt. Dieses Implantat ist als Kitt und in Streifenform erhältlich.

- ZimVie kündigt die Markteinführung von RegenerOss CC Allograft Particulate und RegenerOss Bone Graft Plug an: Im April 2023 brachte ZimVie Inc. RegenerOss CC Allograft und RegenerOss Bone Graft Plug in Nordamerika auf den Markt, die in verschiedenen zahnärztlichen Anwendungen eingesetzt werden sollen.

Marktbericht zu Knochenersatzmaterialien für die Zahnheilkunde: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für Knochentransplantat-Ersatzstoffe in der Zahnmedizin (2021–2034)“ bietet eine detaillierte Analyse des Marktes, die folgende Bereiche abdeckt:

- Marktgröße und Prognose für Knochenersatzmaterialien in der Zahnmedizin auf globaler, regionaler und Länderebene für alle abgedeckten Segmente

- Markttrends und Dynamiken im Bereich der Knochentransplantat-Ersatzstoffe für die Zahnheilkunde, einschließlich treibender Faktoren, Hemmnisse und wichtiger Chancen.

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für Knochenersatzmaterialien in der Zahnmedizin: Wichtige Trends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Bestimmungen und aktuelle Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse mit Fokus auf Marktkonzentration, Heatmap-Analyse, führende Akteure und aktuelle Entwicklungen im Markt für dentale Knochentransplantatersatzstoffe

- Detaillierte Unternehmensprofile

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends