Digitalisierung im Logistik-Lieferkettenmarkt – Erkenntnisse durch globale und regionale Analyse – Prognose bis 2031

Historische Daten : 2021-2022 | Basisjahr : 2023 | Prognosezeitraum : 2024-2031Digitalisierung in der Logistik-Lieferkette – Marktgröße und Prognose (2021–2031), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalyse: Nach Komponente (Software und Dienstleistungen), Unternehmensgröße (Großunternehmen und KMU), Branche (Einzelhandel und E-Commerce, Gesundheitswesen, Fertigung, Automobilindustrie und andere) und Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00013577

- Kategorie : Technologie, Medien und Telekommunikation

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

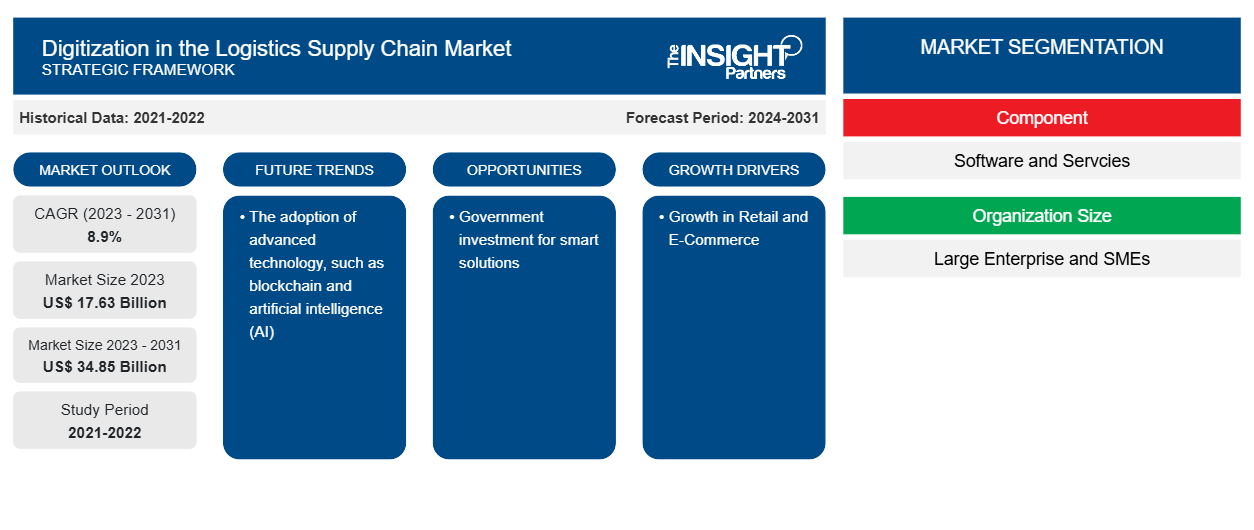

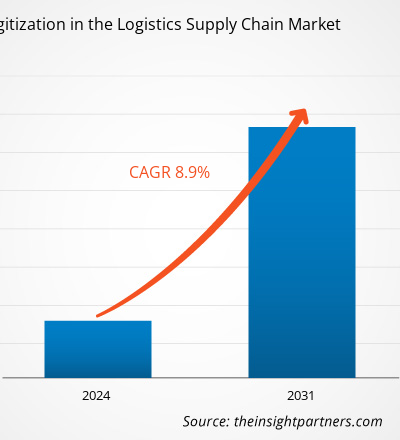

Die Größe der Digitalisierung im Logistik-Lieferkettenmarkt wird voraussichtlich von 17,63 Milliarden US-Dollar im Jahr 2023 auf 34,85 Milliarden US-Dollar im Jahr 2031 anwachsen. Der Markt wird voraussichtlich zwischen 2023 und 2031 eine durchschnittliche jährliche Wachstumsrate von 8,9 % verzeichnen. Die steigende Nachfrage nach Lieferkettenmanagement und der wachsende Einzelhandel und E-Commerce-Sektor werden wahrscheinlich weiterhin die wichtigsten Trends bei der Digitalisierung im Logistik-Lieferkettenmarkt bleiben.

Marktanalyse zur Digitalisierung in der Logistik-Lieferkette

Die Automatisierung in verschiedenen Branchen wie der Automobilindustrie, dem Einzelhandel und E-Commerce, der Fertigung, dem Gesundheitswesen und anderen hat den Betreibern dieser Branchen in großem Umfang Vorteile gebracht, indem sie menschliche Fehler reduziert hat. Beispielsweise wächst der Einzelhandel weltweit kontinuierlich und wird in Zukunft voraussichtlich noch weiter wachsen. Daher konzentriert sich die wachsende Einzelhandelsbranche darauf, die Gesamtbetriebskosten zu senken, indem manuelle Vorgänge zur Lagerhaltung und Verwaltung der Lieferkette und Logistik abgeschafft werden. Die Nachfrage nach Automatisierungslösungen im gesamten Einzelhandel treibt den Markt an. Der Logistiksektor erlebt in mehreren Branchen eine digitale Transformation, da die Beteiligten dazu neigen, Fehler zu minimieren, Abläufe zu verbessern und pünktliche Lieferungen zu gewährleisten, was den Markt antreibt.

Digitalisierung in der Logistik-Lieferkette Marktübersicht

Die fortschreitende digitale Transformation verändert traditionelle Geschäftsmodelle und macht sie effektiver und effizienter. Die Einführung digitaler Technologien hilft Marktteilnehmern in verschiedenen Branchen, durch die Optimierung ihrer Geschäftsmodelle einen Wettbewerbsvorteil gegenüber den anderen Akteuren zu erlangen. Die Digitalisierung der Abläufe in der Logistikversorgungskette hilft ihnen, Personalkosten zu sparen, ihre Prozesse zu beschleunigen und Fehler zu minimieren. Die Einbeziehung fortschrittlicherer Technologien wie künstlicher Intelligenz (KI) hilft ihnen, mithilfe fortschrittlicher Analysen effektive Geschäftsentscheidungen zu treffen.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Digitalisierung im Logistik-Lieferkettenmarkt: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Digitalisierung in der Logistik-Lieferkette – Treiber und Chancen

Wachstum im Einzelhandel und E-Commerce begünstigt den Markt

Der Anstieg des Einkommens und der Kaufkraft der Menschen war ein wichtiger Faktor für das Wachstum im Einzelhandel und im E-Commerce. Die zunehmende Verbreitung von Mobiltelefonen und Internetverbindungen hat dem Einzelhandel Machbarkeit und einfache Zugänglichkeit verliehen, was zu einem Wachstum des E-Commerce geführt hat. Laut der India Brand Equity Foundation (IBEF) verfügen Länder wie die USA, Kanada, Deutschland, Großbritannien, China, Japan, Frankreich, Australien, die Schweiz, Italien und Indien über einen robusten Einzelhandelsmarkt. Die Digitalisierung der Logistiklieferkette hilft den Beteiligten in der Lieferkette, ihre Abläufe zu optimieren. Die Digitalisierung hilft bei der Echtzeitverfolgung und -aufspürung von Bestellungen und Rohstoffen in der Lieferkette. Sie trägt zu einer effizienten Koordination zwischen Herstellern, Lieferanten, Händlern und Einzelhändlern bei, um Kosten zu senken, die Qualität zu verbessern und Kundenanforderungen zu erfüllen. Somit treibt das Wachstum im Einzelhandel und im E-Commerce die Nachfrage nach Lösungen zur Verbesserung der Lieferkette und des Logistik-Workflows an, was die Digitalisierung im Marktwachstum der Logistiklieferkette weiter vorantreibt.

Staatliche Investitionen für intelligente Lösungen – Eine Chance durch die Digitalisierung im Logistik-Lieferkettenmarkt

Um die Digitalisierung weltweit voranzutreiben, investiert die Regierung in intelligente Lösungen. Die Einführung intelligenter Lösungen trägt dazu bei, die Produktion anzukurbeln, den Betrieb zu optimieren und eine höhere Kapitalrendite zu erzielen. Sie trägt dazu bei, komplexe Geschäftsmodelle zu vereinfachen und schnellere Abläufe zu ermöglichen.

- Im September 2023 kündigte die Biden-Harris-Regierung 160 Millionen US-Dollar für intelligente Transporttechnologie an. Diese Investition konzentrierte sich auch auf Systeminnovationen wie Lieferung und Logistik, Verkehrssignale, Smart Grid und Datenintegration.

- Im Februar 2023 kündigte der indische Finanzminister eine Haushaltszuweisung von rund 3363,5 Millionen US-Dollar (27.482 Crore INR) für die Dedicated Freight Corridor Corporation of India (DFCC) an, eine Steigerung von 75 % gegenüber dem Vorjahr. In der Haushaltsrede wurde die Priorisierung von 100 wichtigen Transportinfrastrukturprojekten hervorgehoben, wie etwa die Zustellung auf der letzten und ersten Meile für Häfen, Kohle, Stahl, Düngemittel und Getreide.

Daher können solche Investitionen die Digitalisierung im Logistik- und Lieferkettensektor vorantreiben und als Chance für Marktwachstum dienen.

Digitalisierung in der Logistik-Lieferkette Marktbericht Segmentierungsanalyse

Wichtige Segmente, die zur Ableitung der Digitalisierung in der Marktanalyse der Logistik-Lieferkette beigetragen haben, sind Komponenten, Organisationsgröße und Branche.

- Basierend auf den Komponenten ist der Markt in Software und Dienstleistungen unterteilt. Das Softwaresegment hatte im Jahr 2023 einen größeren Marktanteil.

- Nach Unternehmensgröße ist der Markt in Großunternehmen und KMU segmentiert. Das Segment der Großunternehmen hatte im Jahr 2023 den größten Marktanteil.

- Nach Branchen ist der Markt in Einzelhandel und E-Commerce, Gesundheitswesen, Fertigung, Automobil und andere unterteilt. Das Segment Einzelhandel und E-Commerce hielt im Jahr 2023 den größten Marktanteil.

Digitalisierung in der Logistik-Lieferkette Marktanteilsanalyse nach Geografie

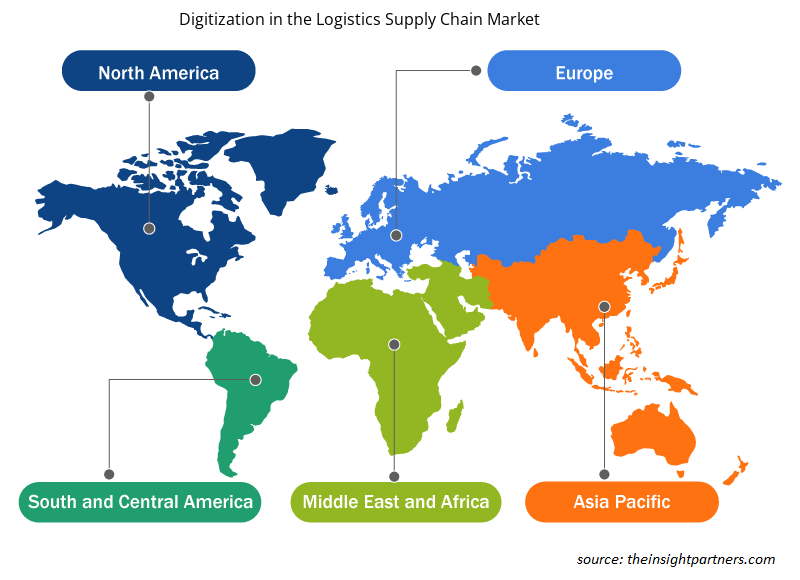

Der geografische Umfang der Digitalisierung im Markt für Logistik-Lieferketten ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Südamerika/Süd- und Mittelamerika.

In Bezug auf den Umsatz hatte Nordamerika den größten Marktanteil bei der Digitalisierung der Logistikversorgungskette. Die USA, Kanada und Mexiko gehören zu den wichtigsten Ländern Nordamerikas. Die Region ist ein früher Anwender technologisch fortschrittlicher Lösungen, was einer der Schlüsselfaktoren für das Marktwachstum ist. Der Aufstieg der Einzelhandels- und E-Commerce-Branche in der Region erzeugt die Nachfrage nach digitalen Lösungen zur Optimierung der Lieferkette und der Logistikaktivitäten, die den Markt fördern. Laut dem US-Handelsministerium stiegen die Umsätze im US-Einzelhandel und in der Lebensmittelbranche im Februar 2024 im Vergleich zum Januar 2024 um 0,6 %. Darüber hinaus hatte Kanada laut der International Trade Administration im Jahr 2022 rund 75 % der E-Commerce-Nutzer der kanadischen Gesamtbevölkerung, und bis 2025 soll dieser Anteil auf 77,6 % steigen. Die Zahl der Menschen in Kanada, die online einkaufen, nimmt zu, was zu den verstärkten E-Commerce-Aktivitäten des Landes wie Produktlieferungen beiträgt.

Digitalisierung im Logistik-Lieferkettenmarkt – Regionale Einblicke

Die regionalen Trends und Faktoren, die die Digitalisierung im Logistik-Lieferkettenmarkt während des gesamten Prognosezeitraums beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie der Digitalisierung im Logistik-Lieferkettenmarkt in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zur Digitalisierung im Logistik-Lieferkettenmarkt

Umfang des Marktberichts zur Digitalisierung in der Logistik-Lieferkette

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2023 | 17,63 Milliarden US-Dollar |

| Marktgröße bis 2031 | 34,85 Milliarden US-Dollar |

| Globale CAGR (2023 - 2031) | 8,9 % |

| Historische Daten | 2021-2022 |

| Prognosezeitraum | 2024–2031 |

| Abgedeckte Segmente |

Nach Komponente

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Digitalisierung in der Logistik-Lieferkette – Marktakteursdichte: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für die Digitalisierung in der Logistikversorgungskette wächst rasant, angetrieben durch die steigende Nachfrage der Endnutzer aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung der Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten Unternehmen, die im Bereich der Digitalisierung im Logistik-Lieferkettenmarkt tätig sind, sind:

- SAP SE

- Oracle Corporation

- IBM

- Intel Corporation

- Infor

- Hexaware Technologies Limited

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Erhalten Sie einen Überblick über die wichtigsten Akteure des Marktes für die Digitalisierung in der Logistikversorgungskette

Digitalisierung in der Logistik-Lieferkette – Marktnachrichten und aktuelle Entwicklungen

Die Digitalisierung im Markt der Logistikversorgungskette wird durch die Erfassung qualitativer und quantitativer Daten nach Primär- und Sekundärforschung bewertet, die wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken umfasst. Im Folgenden finden Sie eine Liste der Entwicklungen auf dem Markt:

- Im Dezember 2023 kündigte Fujitsu die Einführung eines neuen cloudbasierten Standardisierungs- und Visualisierungsdienstes für Logistikdaten für Spediteure, Logistikunternehmen und Lieferanten entlang der gesamten Lieferkette an. Der Dienst bietet Kunden neue Tools, um Nachhaltigkeit in ihren Betrieben zu erreichen und eine Vielzahl von Herausforderungen zu bewältigen, darunter den drohenden Mangel an Lkw-Fahrern, die dringende Notwendigkeit, den CO2-Fußabdruck des Transports zu reduzieren und die Einhaltung strengerer Branchenvorschriften. (Quelle: Fujitsu, Pressemitteilung, 2023)

- Im Januar 2024 gab Blue Yonder, ein führender Anbieter von Supply-Chain-Lösungen, die Veröffentlichung seines größten Produktupdates in der Geschichte des Unternehmens bekannt und brachte die ersten interoperablen Lösungen für die gesamte Lieferkette auf den Markt – von der Planung über Lagerhaltung, Transport und Handel – die auf der Luminate Cognitive Platform des Unternehmens bereitgestellt werden. Durch die Nutzung der Interoperabilität kann Blue Yonder seinen Kunden höhere Produktivität, weniger Abfall und widerstandsfähigere Lieferketten bieten. (Quelle: Blue Yonder, Pressemitteilung, 2024)

Bericht zur Digitalisierung in der Logistik-Lieferkette – Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose zur Digitalisierung in der Logistik-Lieferkette (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Marktgröße und Prognose auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Projekts abgedeckt sind

- Marktdynamik wie Treiber, Beschränkungen und wichtige Chancen

- Wichtige Zukunftstrends

- Detaillierte PEST/Porters Five Forces- und SWOT-Analyse

- Globale und regionale Marktanalyse mit wichtigen Markttrends, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und aktuellen Entwicklungen

- Detaillierte Firmenprofile

Ankita ist eine dynamische Marktforschungs- und Beratungsexpertin mit über 8 Jahren Erfahrung in den Bereichen Technologie, Medien, IKT sowie Elektronik und Halbleiter. Sie hat über 100 Beratungs- und Forschungsaufträge für globale Kunden wie Microsoft, Oracle, NEC Corporation, SAP, KPMG und Expeditors International erfolgreich geleitet und durchgeführt. Zu ihren Kernkompetenzen gehören Marktbewertung, Datenanalyse, Prognose, Strategieformulierung, Wettbewerbsbeobachtung und das Verfassen von Berichten. Ankita ist versiert in der Abwicklung kompletter Projektzyklen – von der Angebotserstellung vor dem Verkauf und Kundengesprächen bis hin zur Bereitstellung umsetzbarer Erkenntnisse nach dem Verkauf. Sie ist versiert in der Leitung funktionsübergreifender Teams, der Strukturierung komplexer Forschungsmodule und der Ausrichtung von Lösungen an kundenspezifischen Geschäftszielen. Ihre ausgezeichneten Kommunikationsfähigkeiten, Führungsqualitäten und Präsentationsfähigkeiten haben es ihr ermöglicht, in einem schnelllebigen und sich entwickelnden Marktumfeld stets wertorientierte Ergebnisse zu liefern.

- Historische Analyse (2 Jahre), Basisjahr, Prognose (7 Jahre) mit CAGR

- PEST- und SWOT-Analyse

- Marktgröße Wert/Volumen – Global, Regional, Land

- Branchen- und Wettbewerbslandschaft

- Excel-Datensatz

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends

Exklusive Berichtsrabatte freischalten

Jetzt anfragen

Kostenlose Probe anfordern für - Digitalisierung im Logistik-Supply-Chain-Markt

Kostenlose Probe anfordern für - Digitalisierung im Logistik-Supply-Chain-Markt