Markteinblicke, Wachstum und Prognose für Elektro-Lkw (2025-2031)

Marktgröße und Prognose für Elektro-Lkw (2021–2034), globaler und regionaler Marktanteil, Trend- und Wachstumschancenanalyse. Berichtsabdeckung: Nach Antrieb (BEV, PHEV und FCV), Fahrzeugtyp (LCV und mittelschwere & schwere Nutzfahrzeuge), Reichweite (weniger als 200 Meilen und mehr als 200 Meilen), Automatisierungsgrad (teilautonom und vollautonom).

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00025913

- Kategorie : Automobil- und Transportwesen

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : January 27, 2026

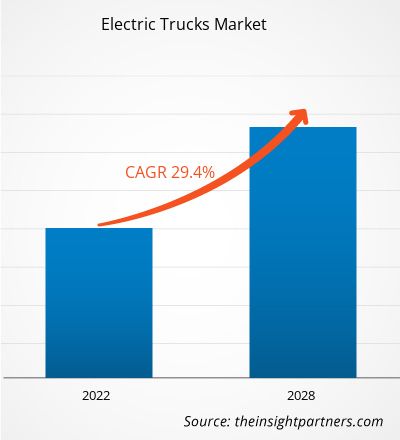

Der Markt für Elektro-Lkw wird bis 2034 voraussichtlich ein Volumen von 119,43 Millionen US-Dollar erreichen, gegenüber 12,51 Millionen US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Prognosezeitraum 2026–2034 eine robuste durchschnittliche jährliche Wachstumsrate (CAGR) von 28,5 % verzeichnen wird.

Marktanalyse für Elektro-Lkw

Die Marktprognose für Elektro-Lkw deutet auf ein robustes Wachstum hin, das durch immer strengere globale Emissionsvorschriften, die rasante Entwicklung von Batterietechnologien und Energiespeicherlösungen sowie den zunehmenden Einsatz emissionsfreier Fahrzeuge in wichtigen Branchen wie Logistik, Transport und E-Commerce gestützt wird. Staatliche Förderprogramme und unternehmerische Nachhaltigkeitsziele beschleunigen die Elektrifizierung von Fahrzeugflotten weltweit und fördern so maßgeblich die Marktexpansion. Fahrzeughersteller (OEMs) reagieren darauf mit hohen Investitionen in Forschung und Entwicklung, um die Reichweite ihrer Fahrzeuge zu verbessern, die Ladeinfrastruktur auszubauen und fortschrittliche autonome Fahr- und Telematikfunktionen zu integrieren. Ziel ist es, Elektro-Lkw als zentrale Komponenten zukünftiger nachhaltiger Logistikketten zu etablieren.

Marktübersicht für Elektro-Lkw

Elektro-Lkw sind Nutzfahrzeuge, die von leichten Transportern bis hin zu schweren Sattelzügen reichen und ganz oder teilweise elektrisch angetrieben werden. Die Energie dafür wird entweder in Bordbatterien gespeichert oder von Brennstoffzellen bereitgestellt. Sie bieten insbesondere erhebliche Vorteile, darunter deutlich reduzierte Treibhausgasemissionen und Lärmbelastung sowie wesentlich niedrigere Betriebskosten im Vergleich zu herkömmlichen Diesel-Lkw. Ihre Einsatzmöglichkeiten wachsen in verschiedensten Bereichen, von der Stadtlogistik über die Zustellung auf der letzten Meile und den regionalen Güterverkehr bis hin zu spezialisierten Baubranchen. Das Wachstum des globalen Marktes basiert im Wesentlichen auf ambitionierten Zielen zur Dekarbonisierung, sinkenden Batteriekosten und – strategisch gesehen – der Entwicklung der Wasserstoff-Brennstoffzellentechnologie als praktikable Lösung für den hohen Bedarf an Schwerlast- und Langstreckentransporten.

Passen Sie diesen Bericht Ihren Anforderungen an.

Sie erhalten eine kostenlose Anpassung aller Berichte – einschließlich Teilen dieses Berichts, Länderanalysen und Excel-Datenpaketen – sowie attraktive Angebote und Rabatte für Start-ups und Universitäten.

Markt für Elektro-Lkw: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen für Elektro-Lkw

Markttreiber:

- Strenge Emissionsnormen und globale Dekarbonisierungsziele: Weltweit werden die Vorgaben für emissionsfreie Nutzfahrzeugflotten von Regierungen immer strenger durchgesetzt, insbesondere in Ballungsräumen und entlang wichtiger Verkehrskorridore. Dieser regulatorische Druck zwingt Logistikdienstleister und Flottenbetreiber gleichermaßen dazu, schnellstmöglich von Fahrzeugen mit Verbrennungsmotor auf nachhaltige Elektrofahrzeuge umzusteigen.

- Steigende Kraftstoffkosten und die Nachfrage nach kosteneffizienter Logistik: Die Volatilität und die hohen Kosten herkömmlicher Kraftstoffe machen die Gesamtbetriebskosten (TCO) von Elektro-Lkw zunehmend attraktiv. Der geringere Wartungsaufwand und der günstigere Energieverbrauch pro Kilometer bieten einen starken finanziellen Anreiz für die Modernisierung großer Fahrzeugflotten und Effizienzsteigerungen.

- Technologische Fortschritte bei Batteriedichte und Ladeinfrastruktur: Kontinuierliche Innovationen in der Lithium-Ionen- und Festkörperbatterietechnologie verbessern die Energiedichte rasant und erhöhen so die Reichweite der Fahrzeuge. Gleichzeitig trägt der Einsatz von MCS und dedizierter Hochleistungsladeinfrastruktur maßgeblich zur Reduzierung der Reichweitenangst bei und macht Elektro-Lkw fit für den Mittel- und Langstreckeneinsatz.

Marktchancen:

- Expansion in Schwellenländern mit förderlicher Elektromobilitätspolitik: Schwellenländer, insbesondere im asiatisch-pazifischen Raum und in Lateinamerika, stellen bedeutende, bisher unerschlossene Märkte dar. Staatliche Subventionen, günstige regulatorische Rahmenbedingungen und der rasante Anstieg des E-Commerce in diesen Regionen eröffnen Herstellern von Elektro-Lkw enorme Chancen, ihre Geschäftstätigkeit und Marktanteile auszubauen.

- Integration von autonomem Fahren und fortschrittlicher Telematik: Die Konvergenz von elektrischer Antriebstechnologie und autonomen Fahrsystemen eröffnet revolutionäre Möglichkeiten. OEMs erproben derzeit teil- und vollautonome Elektro-Lkw, die die Betriebskosten weiter senken, die Fahrersicherheit erhöhen und die Kapazität im Güterverkehr effizienter nutzen könnten.

- Beschleunigte Entwicklung von Wasserstoff-Brennstoffzellen-Lkw: Die Einschränkungen hinsichtlich Batteriegewicht und Ladezeit bei Schwerlast- und Langstreckenanwendungen werden durch Wasserstoff-Brennstoffzellenfahrzeuge (FCV) überwunden. FCVs bieten schnelles Betanken und eine größere Reichweite und stellen somit eine ideale und äußerst lukrative Marktchance für emissionsfreie Fern- und Überlandtransporte dar.

Marktbericht für Elektro-Lkw: Segmentierungsanalyse

Der Marktanteil von Elektro-Lkw wird in verschiedenen Segmenten analysiert, um ein besseres Verständnis seiner Struktur, seines Wachstumspotenzials und der aufkommenden Trends in Technologie und Anwendung zu ermöglichen. Nachfolgend ist der in den meisten Branchenberichten verwendete Standard-Segmentierungsansatz dargestellt:

Durch Antrieb:

- Batterieelektrisches Fahrzeug (BEV)

- Plug-in-Hybrid-Elektrofahrzeug (PHEV)

- Brennstoffzellenfahrzeug (FCV)

Nach Fahrzeugtyp:

- Leichte Nutzfahrzeuge (LCV)

- Mittlere und schwere Nutzfahrzeuge (HCV)

Nach Reichweite:

- Weniger als 200 Meilen

- Mehr als 200 Meilen

Nach Automatisierungsgrad:

- Halbautonom

- Vollständig autonom

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Süd- und Mittelamerika

- Naher Osten und Afrika

Regionale Einblicke in den Markt für Elektro-Lkw

Die regionalen Trends und Einflussfaktoren auf den Markt für Elektro-Lkw im gesamten Prognosezeitraum wurden von den Analysten von The Insight Partners ausführlich erläutert. Dieser Abschnitt behandelt außerdem die Marktsegmente und die geografische Verteilung des Marktes für Elektro-Lkw in Nordamerika, Europa, Asien-Pazifik, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika.

Berichtsumfang zum Markt für Elektro-Lkw

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 12,51 Millionen US-Dollar |

| Marktgröße bis 2034 | 119,43 Millionen US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 28,5 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Durch Antrieb

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte der Akteure im Bereich der Elektro-Lkw: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Elektro-Lkw wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Kundenbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

- Überblick über die wichtigsten Akteure auf dem Markt für Elektro-Lkw

Marktanteilsanalyse für Elektro-Lkw nach Regionen

Der asiatisch-pazifische Raum wird voraussichtlich in den kommenden Jahren das schnellste Wachstum verzeichnen. Auch die aufstrebenden Märkte in Süd- und Mittelamerika sowie im Nahen Osten und Afrika bieten Anbietern von Elektro-Lkw zahlreiche ungenutzte Möglichkeiten zur Expansion. Der Markt für Elektro-Lkw weist in den einzelnen Regionen aufgrund von Faktoren wie regulatorischen Rahmenbedingungen, verfügbarer Infrastruktur und der Produktionsstärke der einheimischen Erstausrüster (OEMs) unterschiedliche Wachstumsraten auf. Nachfolgend finden Sie eine Zusammenfassung der Marktanteile und Trends nach Regionen:

1. Nordamerika

- Marktanteil: Hält gemessen am Umsatz den größten Marktanteil aufgrund starker staatlicher Anreize für Elektrofahrzeuge und der rasanten Entwicklung spezialisierter Ladeinfrastruktur, insbesondere in den USA und Kanada.

- Wichtigste Einflussfaktoren: Die Einführung von IRA-Steuergutschriften für gewerbliche emissionsarme Fahrzeuge, die zu unmittelbaren Kaufentscheidungen führen.

- Trends: Ein bedeutender Trend ist die Einführung der Megawatt-Ladetechnologie (MCS) zur Unterstützung der Elektrifizierung von Schwerlast- und Langstrecken-Güterverkehrskorridoren.

2. Europa

- Marktanteil: Besitzt einen bedeutenden Marktanteil, was vor allem auf die ambitionierten CO₂-Reduktionsziele und die zunehmende Verbreitung von städtischen Umweltzonen (LEZ) zurückzuführen ist.

- Wichtigste Einflussfaktoren: Die verbindlichen Vorgaben des EU Green Deals und die strengen CO₂-Normen für schwere Nutzfahrzeuge.

- Trends: Es gibt konzentrierte Bemühungen, einen Wasserstoffkorridor über den Kontinent zu entwickeln, um den Fern- und grenzüberschreitenden Lkw-Verkehr mit Brennstoffzellenfahrzeugen zu unterstützen.

3. Asien-Pazifik

- Marktanteil: Die am schnellsten wachsende Region, angeführt von China, das den Markt sowohl hinsichtlich des Volumens als auch der lokalen Produktionskapazität dominiert.

- Wichtigste Einflussfaktoren: Aggressive staatliche Subventionen und unterstützende Elektromobilitätspolitik (z. B.

- Trends: Integration von KI-gestützter Telematik zur Flottenoptimierung und massive Investitionen in die lokale, großvolumige Batterieproduktion (einschließlich der Blade-Batterietechnologie von BYD).

4. Süd- und Mittelamerika

- Marktanteil: Ein aufstrebender Markt, der durch eine steigende Nachfrage nach effizienten urbanen Logistik- und Zustellungsdiensten auf der letzten Meile gekennzeichnet ist.

- Wichtigste Einflussfaktoren: Günstige Steuerstrukturen für den Import von gewerblichen Elektrofahrzeugen in bestimmten Ländern (z. B. Chile, Brasilien).

- Trends: Der Markt konzentriert sich überwiegend auf die Einführung kostengünstiger BEV-Lösungen, die speziell für Kurzstrecken- und Stadtzustellanwendungen entwickelt wurden.

5. Naher Osten und Afrika

- Marktanteil: Ein aufstrebender Markt mit starkem Wachstumspotenzial, der vor allem durch massive Infrastruktur- und Diversifizierungsinvestitionen in wichtigen Volkswirtschaften getrieben wird.

- Wichtigste Treiber: Investitionen in Ladelösungen, die mit erneuerbarer Energie betrieben werden.

- Trends: In Logistikzentren werden Pilotprojekte für Wasserstoff-Lkw in der Frühphase durchgeführt, wobei die riesigen Solarenergieressourcen der Region zur Produktion von grünem Wasserstoff genutzt werden.

Marktdichte der Akteure im Bereich der Elektro-Lkw: Auswirkungen auf die Geschäftsdynamik verstehen

Hohe Marktdichte und starker Wettbewerb

Der Markt für Elektro-Lkw ist hart umkämpft und zeichnet sich durch einen dynamischen Mix aus etablierten globalen OEMs (wie Daimler, AB Volvo und PACCAR) und hochinnovativen, aufstrebenden EV-Startups (darunter Rivian, Tesla und Nikola) aus. Der Wettbewerb ist global, wobei asiatische Giganten wie BYD das Segment der leichten Nutzfahrzeuge (LCV) dominieren, insbesondere im asiatisch-pazifischen Raum. Dieses wettbewerbsintensive Umfeld zwingt die Anbieter, sich durch strategische Alleinstellungsmerkmale zu differenzieren.

- Fortschrittliche Batterietechnologie und Reichweitenoptimierung: Entwicklung eigener, hochdichter Akkupacks zur Erzielung wettbewerbsfähiger Reichweiten über große Entfernungen.

- Entwicklung von Wasserstoff-Brennstoffzellen für Schwerlastanwendungen: Investitionen in FCV-Plattformen, um das lukrative Segment der Klasse 8 (Schwerlastfahrzeuge) zu erschließen, das eine größere Reichweite und schnelles Betanken erfordert.

- Integration autonomer Fahrfunktionen und Flottenmanagementlösungen: Wir bieten fortschrittliche, integrierte Telematik- und automatisierte Fahrfunktionen, um die Betriebskosten von Flotten zu senken und die Sicherheit zu erhöhen.

- Skalierbarkeit und Effizienz der globalen Lieferkette: Aufbau robuster Lieferketten für Batterien und Komponenten, um den rasch steigenden Produktionszielen gerecht zu werden.

Wichtige Unternehmen auf dem Markt für Elektro-Lkw:

- AB Volvo – Schweden

- BYD Company Ltd – China

- Daimler AG – Deutschland

- PACCAR Inc. – Vereinigte Staaten

- Navistar, Inc. – Vereinigte Staaten

- FAW Group Co., Ltd. – China

- Schonen – Schweden

- Proterra Inc. – Vereinigte Staaten

- Rivian – Vereinigte Staaten

Hinweis: Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge geordnet.

Neuigkeiten und aktuelle Entwicklungen auf dem Markt für Elektro-Lkw

- AB Volvo hat neue Elektro-Lkw-Modelle für den Stadt- und Regionalverkehr vorgestellt: Der FL 16–18 t BEV mit Vollluftfederung und verschiedenen Fahrgestellkonfigurationen wurde präsentiert, ebenso wie die FM-Niederflur- und die FMX-BEV-Fahrgestelle. Zudem wurde die FH 6×4 BEV-Sattelzugmaschine mit bis zu 540 kWh Akkukapazität für den Fernverkehr vorgestellt.

- BYD lieferte seinen 100. Elektro-Lkw der Klasse 8 in den USA aus und brachte einen globalen Pickup auf den Markt: BYD feierte die Auslieferung seines 100. batterieelektrischen 8TT-Lkw an Anheuser-Busch in Oakland und unterstrich damit seine Strategie für emissionsfreie Logistik. Das Unternehmen brachte außerdem den BYD Shark Pickup in Mexiko auf den Markt und präsentierte seine Super e-Plattform mit Megawatt-Schnellladetechnologie, die ultraschnelles Laden mit 1 MW für Nutzfahrzeuge ermöglicht.

Marktbericht für Elektro-Lkw: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für Elektro-Lkw (2021–2034)“ bietet eine detaillierte Analyse des Marktes und deckt folgende Bereiche ab:

- Marktgröße und Prognose für Elektro-Lkw auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die in den Geltungsbereich fallen.

- Trends im Markt für Elektro-Lkw sowie Marktdynamiken wie Treiber, Hemmnisse und wichtige Chancen.

- Detaillierte PEST- und SWOT-Analyse zur Beurteilung des makroökonomischen und internen Wettbewerbsumfelds.

- Marktanalyse für Elektro-Lkw mit Fokus auf wichtige Markttrends, globale und regionale Rahmenbedingungen, Hauptakteure, Regulierungen und aktuelle Marktentwicklungen.

- Branchenlandschafts- und Wettbewerbsanalyse mit Fokus auf Marktkonzentration, Heatmap-Analyse, prominente Akteure und aktuelle Entwicklungen auf dem Markt für Elektro-Lkw.

- Detaillierte Unternehmensprofile der wichtigsten Branchenteilnehmer.

Naveen ist ein erfahrener Marktforschungs- und Beratungsexperte mit über 9 Jahren Erfahrung in kundenspezifischen, syndizierten und Beratungsprojekten. In seiner aktuellen Funktion als Associate Vice President hat er erfolgreich Stakeholder entlang der gesamten Projektwertschöpfungskette gemanagt und ist Autor von über 100 Forschungsberichten und über 30 Beratungsaufträgen. Seine Arbeit erstreckt sich auf Industrie- und Regierungsprojekte und trägt maßgeblich zum Kundenerfolg und zur datengesteuerten Entscheidungsfindung bei.

Naveen hat einen Ingenieursabschluss in Elektronik und Kommunikation von der VTU, Karnataka, und einen MBA in Marketing und Operations von der Manipal University. Er ist seit 9 Jahren aktives IEEE-Mitglied und nimmt an Konferenzen und technischen Symposien teil und engagiert sich ehrenamtlich auf Sektions- und regionaler Ebene. Vor seiner aktuellen Position arbeitete er als Associate Strategic Consultant bei IndustryARC und als Industrial Server Consultant bei Hewlett Packard (HP Global).

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends