Marktbericht für Absturzsicherungsausrüstung 2028 nach Segmenten, Geografie, Dynamik, jüngsten Entwicklungen und strategischen Erkenntnissen

Marktprognose für Absturzsicherungsausrüstung bis 2028 – Auswirkungen von COVID-19 und globale Analyse nach Typ (Weichwaren, Hartwaren, Rettungssets, Körpergurte, Ganzkörpergurte und andere) und Anwendung (Bau, Transport, Öl und Gas, Bergbau, Energie und Versorgung, Telekommunikation und andere)

- Status : Veröffentlicht

- Berichtscode : TIPRE00006987

- Kategorie : Fertigung und Bau

- Anzahl der Seiten : 147

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 17, 2024

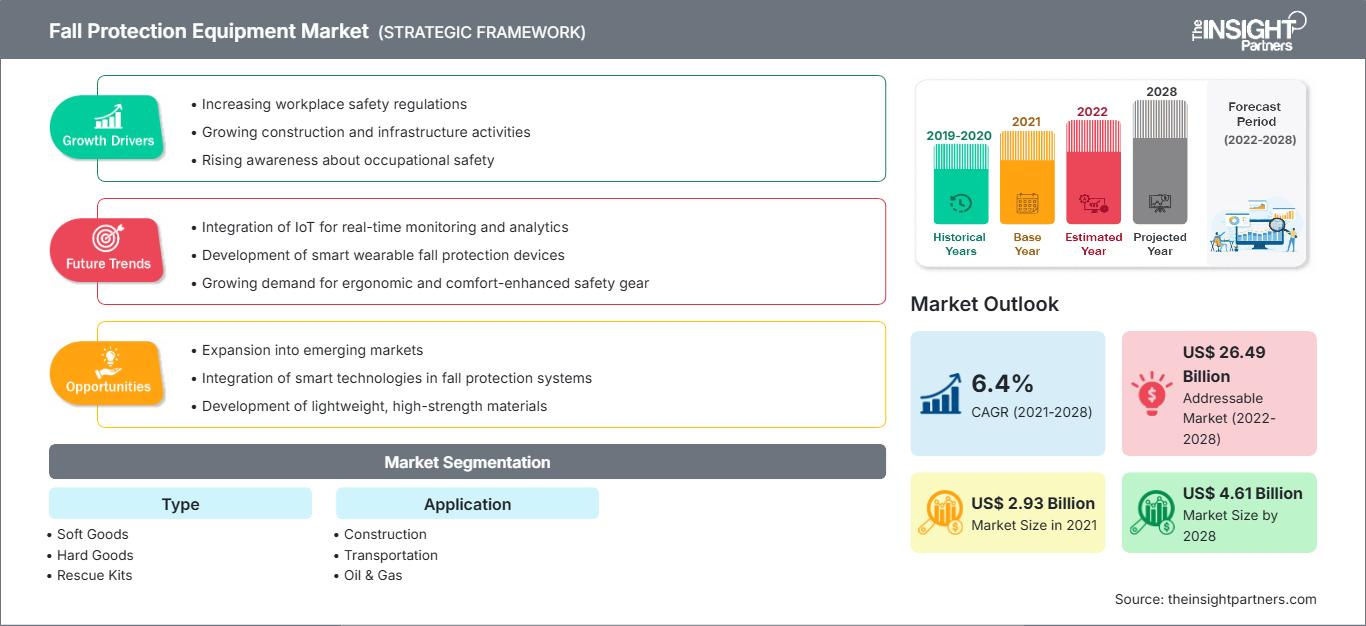

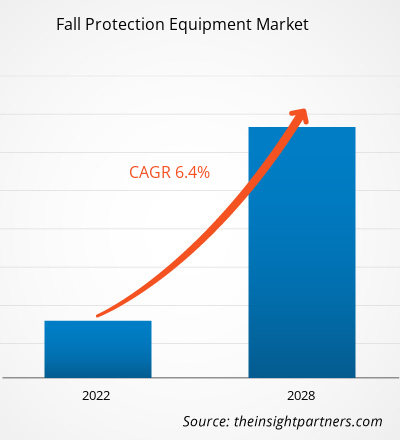

Der Markt für Absturzsicherungsausrüstung soll von 2.934,86 Millionen US-Dollar im Jahr 2021 auf 4.606,61 Millionen US-Dollar im Jahr 2028 wachsen; für den Zeitraum 2021–2028 wird eine durchschnittliche jährliche Wachstumsrate (CAGR) von 6,4 % erwartet.

Die schnelle Industrialisierung in den Industrie- und Entwicklungsländern ist einer der Hauptfaktoren für das Marktwachstum. Aufgrund fehlender angemessener Sicherheitsverfahren in verschiedenen Fertigungs-, Bergbau- und anderen Industrieanlagen treten zunehmend Berufsrisiken auf. Im Vergleich zu anderen Ländern legen die USA mehr Wert auf die Sicherheit und Gesundheit ihrer Arbeitnehmer, was die Einführung von Absturzsicherungsausrüstung im Land vorantreibt. Zur Überwachung der Sicherheitsnormen und -verfahren hat das Land bestimmte Behörden wie die Occupational Safety and Health Administration (OSHA) und das American National Standards Institute (ANSI) eingerichtet. Die OSHA ist eine Organisation für Gesundheits- und Sicherheitsvorschriften und deren Einhaltung, die Arbeitnehmern 10- und 30-stündige Schulungen zu den für verschiedene Berufe relevanten OSHA-Vorschriften und -Standards am Arbeitsplatz anbietet. Der zunehmende Fokus auf Sicherheitspraktiken am Arbeitsplatz und die Verbesserung der staatlichen Vorschriften zur Arbeitssicherheit in Europa und Asien haben den Markt jedoch angetrieben. Steigende Bautätigkeiten und der aufgrund der steigenden Bevölkerung wachsende Öl- und Gassektor in asiatischen Ländern wie Indien und China dürften das Marktwachstum im Prognosezeitraum ankurbeln. Die zunehmende Urbanisierung und das Wachstum der Öl- und Gasindustrie gehören zu den Hauptfaktoren, die das Marktwachstum für Absturzsicherungsausrüstung in den Regionen MEA (Naher Osten und Afrika) und SAM (Südamerika) unterstützen.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Absturzsicherungsausrüstung: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst Datenanalysen, die von Markttrends bis hin zu Schätzungen und Prognosen reichen.

Der COVID-19-Ausbruch hatte auch 2021 in mehreren Ländern negative Auswirkungen. Produktionsschließungen oder eingeschränkte Geschäftsabläufe sowie Lockdowns und Reisebeschränkungen behinderten die Produktion und Lieferkette von Absturzsicherungsausrüstung. Die konstante Nachfrage nach Absturzsicherungsausrüstung verzeichnete 2020 aufgrund des von der Regierung verhängten Lockdowns und einer geringen Anzahl von Bauprojekten einen leichten Rückgang. Im Jahr 2021 besteht jedoch aufgrund einer Zunahme der Bautätigkeiten, der Öl- und Gasexploration sowie von Telekommunikationsprojekten eine Nachfrage nach Absturzsicherungsausrüstung, um die Sicherheit der Mitarbeiter zu gewährleisten. Auch der E-Commerce hat dazu beigetragen, den Bedarf an Absturzsicherungsausrüstung im Bausektor zu steigern.

Markteinblicke in Absturzsicherungsausrüstung: Anstieg der Bautätigkeit

Der Anstieg der Bautätigkeit weltweit ist ein Hauptfaktor, der den Markt für Absturzsicherungsausrüstung antreibt. Da asiatische Länder wie Indien und China ein starkes Bevölkerungswachstum verzeichnen, steigt die Nachfrage nach Gewerbe- und Wohnflächen in diesen Ländern stetig. Die Weltwirtschaft erlebt derzeit einen starken Abschwung aufgrund der sich entwickelnden Kreditknappheit, die dazu führt, dass Volkswirtschaften weltweit ihre Entwicklungsziele verfehlen. Infrastruktur hat im aktuellen Szenario weiterhin höchste Priorität, um Entwicklungslücken zu schließen, da sie als allmächtig und in der Lage gilt, Volkswirtschaften aus finanziellen Turbulenzen zu führen. Regierungen auf der ganzen Welt pumpen Geld in die physische und soziale Infrastruktur, um die Nachfrage nach Produkten und Dienstleistungen durch die Schaffung von Arbeitsplätzen zu steigern.

Typbasierte Markteinblicke

Basierend auf dem Typ ist der Markt für Absturzsicherungsausrüstung in weiche Güter, harte Güter, Rettungssets, Körpergurte, Ganzkörpergurte und Sonstiges unterteilt. Das Segment der harten Güter ist das führende Segment, da es erhöhte Sicherheit bietet. Darüber hinaus soll die zunehmende Innovation in diesem Segment das Marktwachstum ankurbeln. Die steigende Nachfrage nach Ganzkörpergurtsystemen seitens aller industriellen Anwender trägt jedoch dazu bei, dass das Segment mit der höchsten durchschnittlichen jährlichen Wachstumsrate (CAGR) wächst.

Anwendungsbasierte Markteinblicke

In Bezug auf die Anwendung ist der Markt für Absturzsicherungsausrüstung in die Branchen Bauwesen, Öl und Gas, Transport, Energie und Versorgung sowie Telekommunikation unterteilt. Um einen reibungslosen Ablauf der Aktivitäten zu gewährleisten und die Sicherheit der Arbeiter aufrechtzuerhalten, benötigt jede Branche Absturzsicherungsausrüstung in ihren Einrichtungen. Im Jahr 2020 hatte das Bauwesen den größten Marktanteil.

Die Akteure auf dem Markt für Absturzsicherungsausrüstung verfolgen Strategien wie Fusionen, Übernahmen und Marktinitiativen, um ihre Position auf dem Markt zu behaupten. Im Folgenden sind einige Entwicklungen der wichtigsten Akteure aufgeführt:

- Im Mai 2021 brachte die Pure Safety Group ihre Familie von Höhensicherheitsmarken – Stronghold by PSG, Ty-Flt, Checkmate und HART – unter das Banner des Guardian. Durch diese Expansion ist Guardian nun die weltweit größte unabhängige Marke für Absturzsicherung und -prävention.

- 3M Fall Protection hat bis Ende März 2021 Suspension Trauma Safety Straps erfunden und in alle ANSI- und CSA-zertifizierten 3M DBI SALA-Gurte integriert.

Markt für Absturzsicherungsausrüstung

Die Analysten von The Insight Partners haben die regionalen Trends und Faktoren, die den Markt für Absturzsicherungen im Prognosezeitraum beeinflussen, ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die geografische Lage in Nordamerika, Europa, dem asiatisch-pazifischen Raum, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika erörtert.Umfang des Marktberichts zu Absturzsicherungsausrüstung

| Berichtsattribut | Einzelheiten |

|---|---|

| Marktgröße in 2021 | US$ 2.93 Billion |

| Marktgröße nach 2028 | US$ 4.61 Billion |

| Globale CAGR (2021 - 2028) | 6.4% |

| Historische Daten | 2019-2020 |

| Prognosezeitraum | 2022-2028 |

| Abgedeckte Segmente |

By Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer für Absturzsicherungsausrüstung: Verständnis ihrer Auswirkungen auf die Geschäftsdynamik

Der Markt für Absturzsicherungsausrüstung wächst rasant. Dies wird durch die steigende Nachfrage der Endverbraucher aufgrund veränderter Verbraucherpräferenzen, technologischer Fortschritte und eines stärkeren Bewusstseins für die Produktvorteile vorangetrieben. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

- Holen Sie sich die Markt für Absturzsicherungsausrüstung Übersicht der wichtigsten Akteure

- Weichwaren

- Hartwaren

- Rettungssets

- Körpergurte

- Auffanggurte

- Sonstige

Nach Anwendung

- Bau

- Transport

- Öl und Gas

- Bergbau

- Energie und Versorgung

- Telekommunikation

- Sonstige

Nach Geografie

-

Nord Amerika

- USA

- Kanada

- Mexiko

-

Europa

- Frankreich

- Deutschland

- Italien

- Großbritannien

- Russland

- Restliches Europa

-

Asien-Pazifik (APAC)

- China

- Indien

- Südkorea

- Japan

- Australien

- Restliches APAC

-

Naher Osten & Afrika (MEA)

- Südafrika

- Saudi-Arabien

- VAE

- Rest von MEA

-

Südamerika (SAM)

- Brasilien

- Argentinien

- Rest von SAM

Firmenprofile

- 3M

- Falltech

- French Creek Production

- Frontline

- Guardian Fall Protection

- Kee Safety

- KwikSafety

- MSA Safety Incorporated

- Honeywell International Inc.

- Tritech Fall Protection

Nivedita ist eine versierte Forschungsexpertin mit über 9 Jahren Erfahrung in Marktforschung und Unternehmensberatung. Sie ist derzeit als Projektmanagerin im IKT-Bereich bei The Insight Partners tätig und verfügt über umfassende Fachkenntnisse in der Leitung und Durchführung von syndizierten, kundenspezifischen, abonnementbasierten und beratenden Forschungsaufträgen in unterschiedlichen Technologiesektoren.

Mit einer nachgewiesenen Erfolgsbilanz bei der Bereitstellung datengestützter Analysen und umsetzbarer Erkenntnisse war Nivedita maßgeblich an mehreren kritischen Projekten beteiligt. Ihre Arbeit umfasst die vollständige Projektabwicklung – vom Verständnis der Kundenziele über die Analyse von Markttrends bis hin zur Ableitung strategischer Empfehlungen. Sie hat umfassend mit führenden IKT-Unternehmen zusammengearbeitet und ihnen geholfen, Marktchancen zu erkennen und Branchenveränderungen zu meistern.

Nivedita hat einen MBA in Management vom IMS, Dehradun. Vor ihrem Eintritt bei The Insight Partners sammelte sie wertvolle Erfahrungen bei MarketsandMarkets und Future Market Insights in Pune, wo sie verschiedene Forschungspositionen innehatte und sich ein solides Fundament in Branchenanalyse und Kundenbindung erarbeitete.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends