Marktübersicht, Wachstum, Trends, Analyse, Forschungsbericht für Arbeitskleidung im Gesundheitswesen (2020-2027)

Marktprognose für Arbeitskleidung im Gesundheitswesen bis 2027 – Auswirkungen von COVID-19 und globale Analyse nach Produkt (Overalls, Kittel und andere) und Endverbrauch (Krankenhäuser, häusliche Krankenpflege, ambulante/primäre Pflegeeinrichtungen und andere)

- Status : Veröffentlicht

- Berichtscode : TIPRE00014590

- Kategorie : Konsumgüter

- Anzahl der Seiten : 149

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 20, 2024

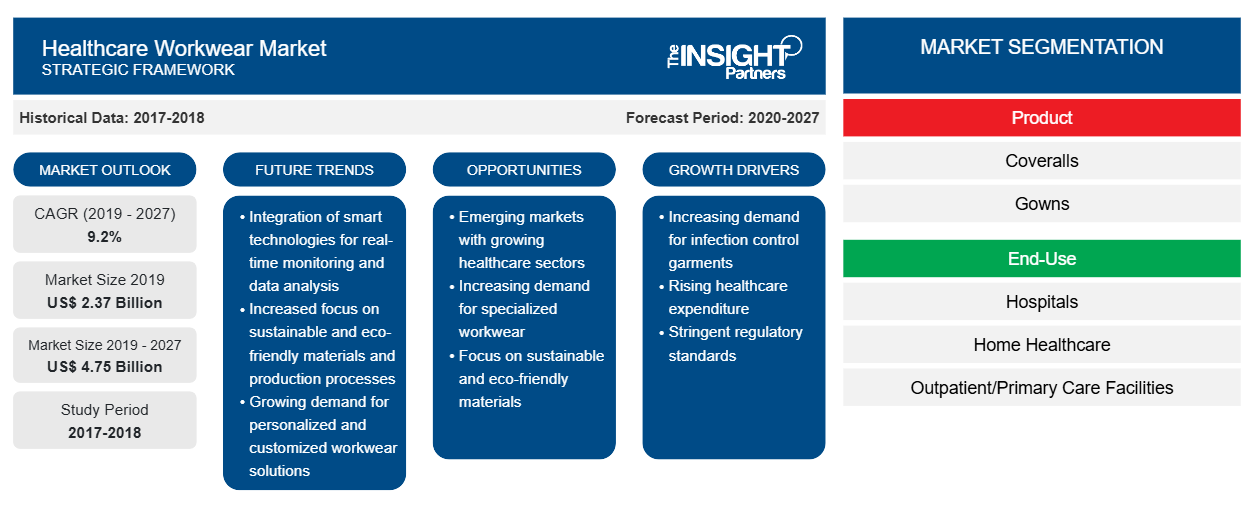

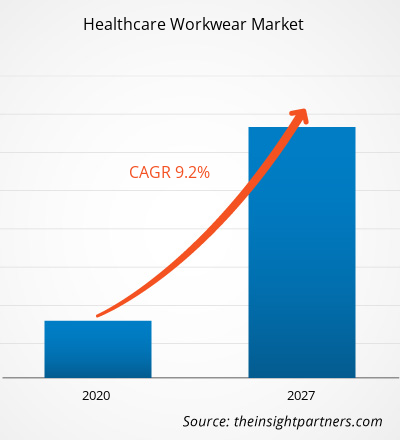

Der Markt für Arbeitskleidung im Gesundheitswesen wurde im Jahr 2019 auf 2.365,96 Millionen US-Dollar geschätzt und soll bis 2027 einen Wert von 4.747,36 Millionen US-Dollar erreichen; von 2020 bis 2027 dürfte er mit einer durchschnittlichen jährlichen Wachstumsrate von 9,2 % wachsen.

Arbeitskleidung im Gesundheitswesen schützt medizinisches Personal vor Krankheitserregern. Overalls, Kittel, Schutzbrillen oder Gesichtsschutz, Masken, Handschuhe, Laborkittel, OP-Kleidung, Schuhe und Stiefelüberzüge gehören zu den auf dem Markt erhältlichen Arten von Arbeitskleidung im Gesundheitswesen, die fast jeden Teil des Körpers bedecken. Medizinisches Personal wählt Arbeitskleidung im Gesundheitswesen entsprechend den Anforderungen ihrer Arbeit aus. Schutzbrillen oder Gesichtsschutz sind Plastikbrillen, die Schutz vor plötzlichen Spritzern von Flüssigkeiten wie Blut, Erbrochenem und Exkrementen bieten. Das Bedecken von Mund und Nase mit Masken verhindert das Ausatmen von Mikroorganismen in einer sterilen Umgebung. Arbeitskleidung im Gesundheitswesen wie Masken, Kittel und Gesichtsschutz hilft, die Ausbreitung von Viren zu verhindern und bietet Schutz für das medizinische Personal, darunter Ärzte, Pflegepersonal und anderes Krankenhauspersonal.

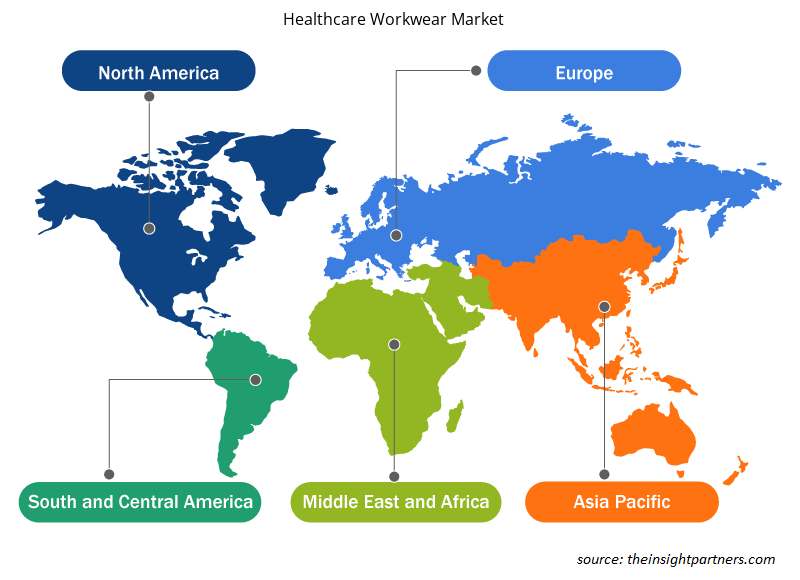

Im Jahr 2019 hatte Europa den größten Anteil am globalen Markt für Arbeitskleidung im Gesundheitswesen. Die steigende Zahl chirurgischer Eingriffe trägt zur Dominanz der Region auf dem Weltmarkt bei. Laut Eurostat wurden 2017 in der EU etwa 1,4 Millionen Kaiserschnitte durchgeführt. Darüber hinaus wird erwartet, dass die geriatrische Bevölkerung in Europa in den nächsten Jahren zunimmt. Laut einem Bericht der Europäischen Kommission wird der Altenquotient voraussichtlich von 29,6 % im Jahr 2016 auf über 50,0 % im Jahr 2070 ansteigen. Auch die steigende Zahl chronischer Krankheiten treibt die Gesamtzahl der in der Region durchgeführten Operationen in die Höhe. Laut der European Chronic Disease Alliance sind chronische Krankheiten wie Krebs, Diabetes, Herzkrankheiten und Schlaganfälle sowie chronische Atemwegserkrankungen die häufigsten Todesursachen in Europa und machen 77 % der gesamten Krankheitslast und 86 % aller Todesfälle aus. Die European Society of Gynecological Oncology (ESGO), die European Society for Radiotherapy and Oncology (ESTRO) und die European Society of Pathology (ESP) entwickeln evidenzbasierte und klinisch relevante Richtlinien zur Verbesserung der medizinischen Versorgung von Frauen mit Gebärmutterhalskrebs in Europa. Solche Initiativen werden in Verbindung mit der steigenden Zahl von Operationen bei Erkrankungen der weiblichen Geschlechtsorgane in den kommenden Jahren wahrscheinlich zum Wachstum des Marktes für Arbeitskleidung im Gesundheitswesen beitragen .

Der COVID-19-Ausbruch wurde erstmals im Dezember 2019 in Wuhan, China, gemeldet und hat sich seitdem weltweit rasant ausgebreitet. Im September 2020 waren die USA, Brasilien, Indien, Russland, Spanien und Großbritannien einige der am schlimmsten betroffenen Länder in Bezug auf bestätigte Fälle und gemeldete Todesfälle. Da das neuartige Coronavirus durch Atemtröpfchen auf gesunde Personen übertragen wird, wenn eine infizierte Person hustet oder niest, müssen Angehörige der Gesundheitsberufe hochwertige Arbeitskleidung tragen, um sich vor der Infektion zu schützen. Dies hat zu einer weiteren hohen Nachfrage nach Arbeitskleidung im Gesundheitswesen wie persönlicher Schutzausrüstung (PSA), Handschuhen und Masken geführt.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für Berufskleidung im Gesundheitswesen: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Markteinblicke

Entwicklung wiederverwendbarer persönlicher Schutzausrüstung soll Marktwachstum ankurbeln

Die auf dem Markt für Arbeitskleidung im Gesundheitswesen tätigen Unternehmen entwickeln neue und innovative wiederverwendbare persönliche Schutzausrüstung, um medizinische Abfälle und die Gesamtkosten für PSA zu reduzieren. Im Juli 2020 führte Loyal Textile Mills Limited den Viral Sheild ein, eine neue Linie wiederverwendbarer PSA und Masken sowie eine Schutzkleidungsserie mit antimikrobieller Wirkung, insbesondere gegen SARS-CoV-2. Die Produktreihe wurde in Zusammenarbeit mit HeiQ aus der Schweiz und Reliance Industries India auf den Markt gebracht. Die Produkte bestehen aus einem dreilagigen antimikrobiellen Gewebe, das mit „HeiQViroblock“ behandelt wurde. HeiQViroblock ist eine in der Schweiz erfundene Technologie. Die neue PSA hat den synthetischen Blutpenetrationstest, den Flüssigkeitsbarrieretest und den Virenpenetrationstest bestanden. Die wiederverwendbaren PSA-Produkte können zur Wiederverwendung 10 Mal gewaschen und sterilisiert werden. Dieses Produkt ist die weltweit erste wiederverwendbare PSA, die den Virenpenetrationstest bestanden hat. HeiQViroblock NPJ03 kombiniert registrierte Silbertechnologie für antibakterielle und antivirale Wirkung und Vesikeltechnologie als Booster. Die Silbertechnologie zieht die entgegengesetzt geladenen Viren an und bindet sich dauerhaft an ihre Schwefelgruppen. Darüber hinaus hilft die Technologie der kugelförmigen Fettbläschen (Liposomen), den Cholesteringehalt der Virusmembran in kurzer Zeit abzubauen, wodurch Silber die Viren schnell zerstören kann.

Produktinformationen

Basierend auf dem Produkttyp ist der Markt für Arbeitskleidung im Gesundheitswesen in Overalls, Kittel und Sonstiges unterteilt. Das Segment Kittel führte den Markt für Arbeitskleidung im Gesundheitswesen mit dem größten Anteil im Jahr 2019 an. Die Kittel, die von Angehörigen der Gesundheitsberufe verwendet werden, werden hauptsächlich in Operationskittel, Operationsisolationskittel und nicht-chirurgische Kittel eingeteilt. Operationskittel werden von medizinischem Personal während chirurgischer Eingriffe getragen, um den Austausch von Körperflüssigkeiten, Mikroorganismen und Partikeln zwischen ihnen und den Patienten zu vermeiden. Die weltweit steigende Zahl chirurgischer Eingriffe unterstützt das Wachstum des Marktes für das Kittelsegment.

Einblicke in die Endverbraucherbranche

Basierend auf der Endnutzung ist der Markt für Arbeitskleidung im Gesundheitswesen in Krankenhäuser, häusliche Pflege, ambulante/primäre Pflegeeinrichtungen und andere unterteilt. Das Krankenhaussegment führte den Markt für Arbeitskleidung im Gesundheitswesen mit dem größten Anteil im Jahr 2019 an. Der Markt für Arbeitskleidung im Gesundheitswesen hat aufgrund der enormen Zunahme der Zahl von Krankenhäusern und Gesundheitseinrichtungen ein erhebliches Wachstum erlebt. Demografische Verschiebungen und gesellschaftliche Veränderungen führen zu einem Anstieg des Drucks auf die Gesundheitssysteme und erzeugen die Nachfrage nach neuen Wegen in der Gesundheitsversorgung. Die weltweit steigende Zahl geriatrischer Bevölkerungen trägt ebenfalls zum Wachstum des Gesundheitssektors bei.

Zu den wichtigsten Akteuren auf dem Markt für Arbeitskleidung im Gesundheitswesen zählen 3M, Alpha Pro Tech, Ansell Limited, Cardinal Health, Derekduck Industry Corp., O&M Halyard, International Enviroguard, Tronex International, Inc., KIMBERLY-CLARK CORPORATION und Surgeine Healthcare (India) Pvt. Ltd. Die Unternehmen verfolgen verschiedene Strategien, um ihren Marktanteil zu erhöhen. Die Unternehmen verfolgen Expansionsstrategien, um ihre Präsenz in Industrie- und Entwicklungsländern zu erweitern oder ihre Servicekapazität und ihr Portfolio zu erweitern. Strategien und Geschäftsplanungen bei der Expansion helfen ihnen, die wachsende Marktnachfrage zu befriedigen.

Regionale Einblicke in den Markt für Arbeitskleidung im Gesundheitswesen

Die regionalen Trends und Faktoren, die den Markt für Arbeitskleidung im Gesundheitswesen während des Prognosezeitraums beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie von Arbeitskleidung im Gesundheitswesen in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Markt für Arbeitskleidung im Gesundheitswesen

Umfang des Marktberichts über Arbeitskleidung im Gesundheitswesen

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2019 | 2,37 Milliarden US-Dollar |

| Marktgröße bis 2027 | 4,75 Milliarden US-Dollar |

| Globale CAGR (2019 - 2027) | 9,2 % |

| Historische Daten | 2017-2018 |

| Prognosezeitraum | 2020–2027 |

| Abgedeckte Segmente |

Nach Produkt

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer für Arbeitskleidung im Gesundheitswesen: Die Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Arbeitskleidung im Gesundheitswesen wächst rasant. Dies wird durch die steigende Nachfrage der Endnutzer aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts vorangetrieben. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung der Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten Unternehmen auf dem Markt für Arbeitskleidung im Gesundheitswesen sind:

- 3M

- Alpha Pro Tech

- ANSELL LTD

- Kardinal Gesundheit

- Derekduck Industry Corp

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für Arbeitskleidung im Gesundheitswesen

Bericht-Spotlights

- Fortschrittliche Branchentrends auf dem globalen Markt für Arbeitskleidung im Gesundheitswesen helfen den Akteuren bei der Entwicklung wirksamer langfristiger Strategien

- In Industrie- und Entwicklungsländern angewandte Strategien für Unternehmenswachstum

- Quantitative Analyse des globalen Marktes für Arbeitskleidung im Gesundheitswesen von 2017 bis 2027

- Schätzung der Nachfrage nach Arbeitskleidung im Gesundheitswesen in verschiedenen Branchen

- PEST-Analyse zur Veranschaulichung der Wirksamkeit der in der Branche tätigen Käufer und Lieferanten bei der Vorhersage des Marktwachstums

- Aktuelle Entwicklungen zum Verständnis der Wettbewerbssituation auf dem Markt und der Nachfrage nach Arbeitskleidung im Gesundheitswesen

- Markttrends und -aussichten in Verbindung mit Faktoren, die das Wachstum des Marktes für Arbeitskleidung im Gesundheitswesen vorantreiben und bremsen

- Entscheidungsprozess durch das Verständnis von Strategien, die das kommerzielle Interesse im Hinblick auf das Wachstum des globalen Marktes für Arbeitskleidung im Gesundheitswesen untermauern

- Größe des Marktes für Arbeitskleidung im Gesundheitswesen an verschiedenen Marktknoten

- Detaillierte Übersicht und Segmentierung des globalen Marktes für Arbeitskleidung im Gesundheitswesen sowie seine Dynamik in der Branche

- Marktgröße für Berufskleidung im Gesundheitswesen in verschiedenen Regionen mit vielversprechenden Wachstumschancen

Markt für Arbeitskleidung im Gesundheitswesen, nach Produkt

- Overalls

- Kleider

- Sonstiges

Markt für Arbeitskleidung im Gesundheitswesen nach Endverbrauch

- Krankenhäuser

- Häusliche Gesundheitspflege

- Ambulante/primäre Versorgungseinrichtungen

- Sonstiges

Firmenprofile

- 3M

- Alpha Pro Tech

- ANSELL LTD

- Kardinal Gesundheit

- Derekduck Industry Corp

- O&M-Fall

- Internationaler Umweltschutz

- Tronex International, Inc

- KIMBERLY-CLARK CORPORATION

- Surgeine Healthcare (Indien) Pvt. Ltd.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends