Marktbericht zu erblichen Krebstests 2031 nach Segmenten, Geografie, Dynamik, jüngsten Entwicklungen und strategischen Erkenntnissen

Marktgröße und Prognose für Tests auf erblichen Krebs (2021 – 2031), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalysen: Nach Diagnosetyp (Biopsie und Bildgebung), Technologie (Sequenzierung, PCR und Microarray) und Endbenutzer (Krankenhaus, Kliniken und Diagnosezentren); und Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00006578

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : February 15, 2025

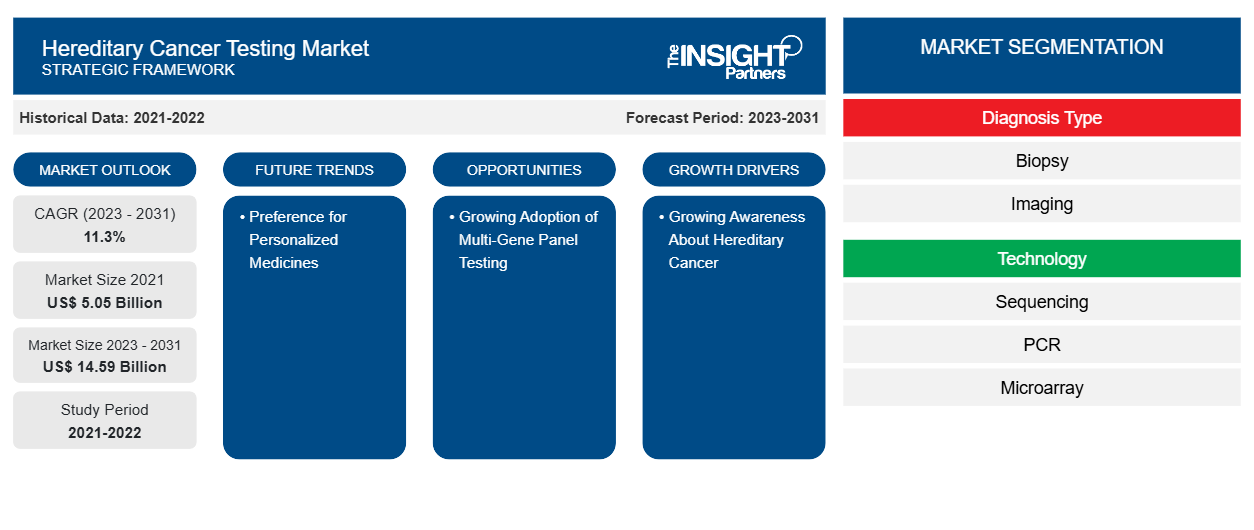

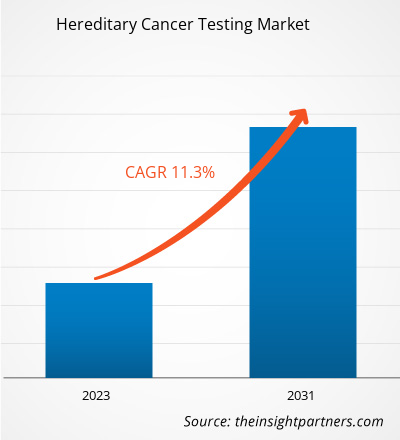

Das Marktvolumen für Erbkrebstests wurde auf 5,05 Milliarden US-Dollar im Jahr 2021 und XX Milliarden US-Dollar im Jahr 2023 geschätzt und soll bis 2031 14,59 Milliarden US-Dollar erreichen; für den Zeitraum 2023–2031 wird eine durchschnittliche jährliche Wachstumsrate von 11,3 % erwartet. Die zunehmende Verbreitung von Erbkrebs und das wachsende Bewusstsein für Erbkrebs sind treibende Faktoren. Die Präferenz für personalisierte Medikamente wird wahrscheinlich weiterhin der Schlüssel zu den Markttrends für Erbkrebstests sein.

Marktanalyse für Tests auf erblichen Krebs

Krebs ist eine genetische Störung, die durch bestimmte Variationen in Genen verursacht wird, die die Zellfunktion steuern und insbesondere deren Wachstum und Replikation beeinflussen. Erbliche genetische Mutationen verursachen 5–10 % aller Krebserkrankungen. Die Forscher haben Mutationen in bestimmten Genen mit mehr als 50 erblichen Krebssyndromen in Verbindung gebracht, die Personen betreffen, die bestimmte Krebsarten entwickeln. Darüber hinaus hängen etwa 5–10 % der Brustkrebserkrankungen mit den von den Eltern geerbten mutierten Genen zusammen. Variationen in den Genen BRCA1 und BRCA2 sind weit verbreitet. Frauen mit einer BRCA1-Mutation haben ein Lebenszeitrisiko von etwa 72 %, an Brustkrebs zu erkranken, während bei Frauen mit der BRCA2-Mutation ein Risiko von etwa 69 % besteht.

Marktübersicht für Tests auf erblichen Krebs

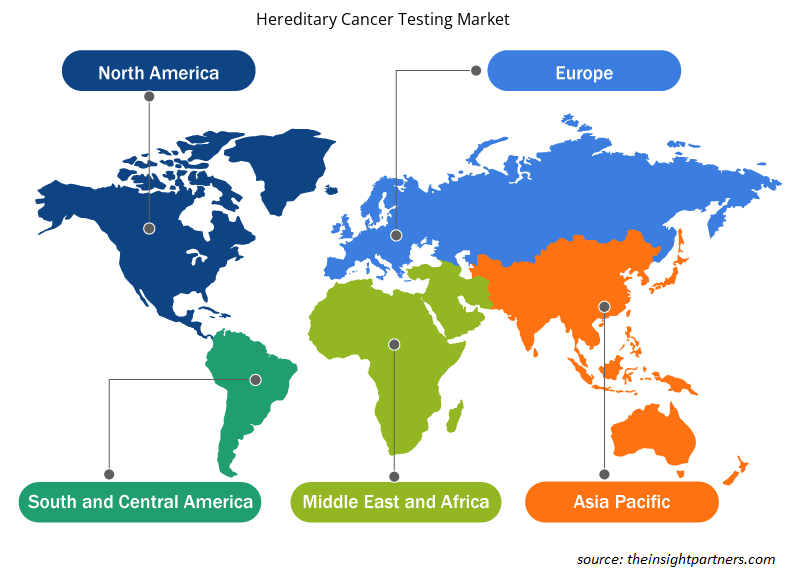

Der asiatisch-pazifische Raum ist der am schnellsten wachsende Markt für Tests auf Erbkrebs. Die Region bietet ein enormes Potenzial für Akteure auf dem Markt für Tests auf Erbkrebs, da Länder wie Südkorea staatliche Unterstützung für die Aufklärung über Krebs und andere Initiativen bieten. Die Nachfrage nach genetischer Sequenzierung in China wächst, vor allem aufgrund der wachsenden Mittelschicht, der älteren Bevölkerung und des wachsenden Gesundheitssystems des Landes. Laut WHO-Daten hat die chinesische Regierung den Plan „Healthy China 2030“ umgesetzt, der für die Bevölkerung des Landes von Nutzen ist.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlose Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für erbliche Krebstests: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Treiber und Chancen des Marktes für Tests auf erblichen Krebs

Wachsendes Bewusstsein für erblichen Krebs

Das Bewusstsein für erbliche Krebserkrankungen wächst dank verschiedener staatlicher Bemühungen. Im letzten Jahrzehnt haben die öffentliche medizinische, gesundheitliche und wissenschaftliche Gemeinschaft in die Sensibilisierung für erbliche Krebserkrankungen investiert, wobei der Schwerpunkt auf dem erblichen Krebsrisiko, der Familiengeschichte und genetischen Tests auf erbliche Krebsanfälligkeit lag. Darüber hinaus konzentrieren sich die Hersteller auf die Einführung von Strategien wie Produkteinführungen und -zulassungen, F&E-Investitionen, staatliche Finanzierung und Partnerschaften, um Patienten weltweit einen einfachen Zugang zu ermöglichen. So startete Ambry im April 2024 die Zusammenarbeit Inter-Organization Cancer Genetics Clinical Evidence Coalition (INTERACT), um Tests auf erbliche Krebserkrankungen voranzutreiben und den Zugang zu spezialisierten genetischen Tests zu verbessern.

Zunehmende Nutzung von Multi-Gen-Panel-Tests – eine Chance

Ein Multigen-Panel macht die Durchführung mehrerer Tests für verschiedene Krebsarten oder Variantentypen überflüssig. Kopienzahlvariationen (CNV) sind eine häufige Quelle genetischer Variationen und an vielen genetischen Erkrankungen beteiligt. Sie sind auch ein wichtiger Bestandteil der Diagnose erblicher Krebserkrankungen.

Die britische Regierung und Genomic England haben erklärt, dass alle CNV-Analysen nun per NGS und nicht mehr per Multiplex-Ligation-Dependent Probe Amplification (MLPA) durchgeführt werden. Dank dieser Vorteile werden alle Laborprozesse rationalisiert und die Erkennung aller SNV-, INDEL- und CNV-Varianten mithilfe eines einzigen Workflows und Analyse-Pipelines ermöglicht.

In zahlreichen nordamerikanischen, europäischen und asiatischen Ländern wird die Einführung von Multigen-Paneltests zunehmen.

Segmentierungsanalyse des Marktberichts zu Tests auf erblichem Krebs

Wichtige Segmente, die zur Ableitung der Marktanalyse für Tests auf erblichen Krebs beigetragen haben, sind Produktdiagnosetyp, Technologie und Endbenutzer.

- Basierend auf der Diagnoseart ist der Markt für Erbkrebstests in Biopsie und Bildgebung unterteilt. Das Biopsiesegment hatte im Jahr 2023 den größten Marktanteil. Es wird jedoch erwartet, dass das Bildgebungssegment im Prognosezeitraum die höchste durchschnittliche jährliche Wachstumsrate verzeichnet.

- Basierend auf der Technologie ist der Markt für Erbkrebstests in Sequenzierung, PCR und Microarray segmentiert. Das Sequenzierungssegment hielt im Jahr 2023 den größten Marktanteil und wird im Prognosezeitraum voraussichtlich die höchste durchschnittliche jährliche Wachstumsrate verzeichnen.

- Basierend auf dem Endverbraucher ist der Markt für Erbkrebstests in Diagnosezentren, Krankenhäuser und Kliniken unterteilt. Das Krankenhaussegment hielt im Jahr 2023 den größten Marktanteil. Darüber hinaus wird geschätzt, dass dasselbe Segment im Prognosezeitraum die höchste durchschnittliche jährliche Wachstumsrate (CAGR) auf dem Markt verzeichnet.

Marktanteilsanalyse für Tests auf erblichen Krebs nach geografischer Lage

Der geografische Umfang des Marktberichts zu Erbkrebstests ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Asien-Pazifik, Europa, Naher Osten und Afrika sowie Südamerika/Süd- und Mittelamerika.

Der nordamerikanische Markt für Tests auf erblichen Krebs ist in die USA, Kanada und Mexiko unterteilt. Die USA hielten 2023 den größten Anteil am nordamerikanischen Markt für Tests auf erblichen Krebs. Das prognostizierte Wachstum des nordamerikanischen Marktes für Tests auf erblichen Krebs wird durch die steigende Zahl von Krebspatienten, zunehmende staatliche Finanzierung und die steigende Inzidenz genetischer Erkrankungen in der Bevölkerung der USA und Kanadas in den letzten Jahren vorangetrieben. Die Regierung hat auch Initiativen ergriffen, um die Bevölkerung für Krebs zu sensibilisieren. Beispielsweise bietet die American Society of Clinical Oncology (ASCO) einen Kurs zur Krebsaufklärung an, um umfassendes und grundlegendes Wissen über diese Erkrankung, einschließlich der Genetik von erblichem Krebs, zu verbreiten.

Regionale Einblicke in den Markt für erbliche Krebstests

Die regionalen Trends und Faktoren, die den Markt für Erbkrebstests im Prognosezeitraum beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie für Erbkrebstests in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Markt für Tests auf erblichen Krebs

Umfang des Marktberichts zu Tests auf erblichen Krebs

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2021 | 5,05 Milliarden US-Dollar |

| Marktgröße bis 2031 | 14,59 Milliarden US-Dollar |

| Globale CAGR (2023 - 2031) | 11,3 % |

| Historische Daten | 2021-2022 |

| Prognosezeitraum | 2023–2031 |

| Abgedeckte Segmente |

Nach Diagnosetyp

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktteilnehmerdichte für Tests auf erblichem Krebs: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Tests auf erblichen Krebs wächst rasant, angetrieben von der steigenden Nachfrage der Endnutzer aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts. Mit der steigenden Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung der Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten auf dem Markt für Tests auf erblichen Krebs tätigen Unternehmen sind:

- Hologic Inc.

- Koninklijke Philips NV

- Quest Diagnostics GmbH

- Myriad Genetics, Inc.

- Krebsgenetik Inc.

- Invitae Corporation

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für Tests auf erblichem Krebs

Neuigkeiten und aktuelle Entwicklungen zum Markt für Erbkrebstests

Der Markt für Tests auf erblichen Krebs wird durch die Erhebung qualitativer und quantitativer Daten aus Primär- und Sekundärforschung bewertet, die wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken umfasst. Im Folgenden finden Sie eine Liste der Entwicklungen auf dem Markt für Tests auf erblichen Krebs:

- Exact Sciences Corp. gab die Einführung des Riskguard-Tests für erblichen Krebs in den USA bekannt. Dieser Test liefert einen individuellen Patientenbericht, der genspezifische und familiäre Risiken anhand einer einfachen Blut- oder Speichelprobe für 10 häufige Krebsarten enthält, darunter Dickdarm- , Gebärmutter-, Magen-, Bauchspeicheldrüsen-, Brust-, Prostata-, Haut-, Eierstock-, Nieren- und Hormonkrebs. (Exact Sciences Corp /Pressemitteilung, Februar 2024)

- Devyser hat die Einführung zweier neuer Produkte angekündigt: Devyser LynchFAP und Devyser BRCA PALB2. Diese Kits bieten eine effiziente, gezielte und zuverlässige Analyse von Genen, die mit einem erhöhten Krebsrisiko verbunden sind. Devyser LynchFAP bietet eine umfassende Lösung zur Analyse von PMS2 und 9 weiteren Genen, die mit erblichen kolorektalen Krebssyndromen verbunden sind (Quelle: Devyser, Pressemitteilung, Juni 2023)

Marktbericht zum Test auf erblichen Krebs: Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für erbliche Krebstests (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Marktgröße und Prognose auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Projekts abgedeckt sind

- Marktdynamik wie Treiber, Beschränkungen und wichtige Chancen

- Wichtige Zukunftstrends

- Detaillierte PEST/Porters Five Forces- und SWOT-Analyse

- Globale und regionale Marktanalyse mit wichtigen Markttrends, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und aktuellen Entwicklungen

- Detaillierte Firmenprofile

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends