Marktgröße, Marktanteil und Prognose für Bildverarbeitungssysteme bis 2034

Marktgröße und Prognose für Bildverarbeitungssysteme (2021–2034), globaler und regionaler Marktanteil, Trend- und Wachstumspotenzialanalyse. Berichtsabdeckung: Nach Typ (intelligente Bildverarbeitungssysteme, PC-basierte Bildverarbeitungssysteme und 3D-Bildverarbeitungssysteme); Komponenten (Kameras, Framegrabber, Prozessoren, Beleuchtung und Optik, Bildverarbeitungssoftware, Bildsensoren und Sonstiges); Schnittstelle (USB 2.0/USB 3.0, Camera Links, GigE, CoaXPress, Sonstiges); und Endnutzer (Automobilindustrie, Elektronik und Halbleiter, Lebensmittel und Getränke, Pharmazeutika, Logistik und Sonstiges).

- Status : Veröffentlichte Daten

- Berichtscode : TIPTE100000156

- Kategorie : Elektronik und Halbleiter

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : December 23, 2025

Der Markt für Bildverarbeitungssysteme wurde im Jahr 2025 auf 20,37 Milliarden US-Dollar geschätzt und soll bis 2034 auf 53,40 Milliarden US-Dollar anwachsen, was einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 12,80 % im Zeitraum 2026–2034 entspricht.

Marktanalyse für Bildverarbeitungssysteme

Der Markt für Bildverarbeitungssysteme steht vor einem starken Wachstum, angetrieben durch die zunehmende Automatisierung in der Industrie, die steigende Nachfrage nach visueller Inspektion und Messung sowie den Bedarf an verbesserter betrieblicher Effizienz. Diese Systeme, bestehend aus Kameras, Software, Optiken und Sensoren, ermöglichen die Erkennung, Identifizierung, Messung und Inspektion von Objekten in der Fertigung und verwandten Branchen. Der verstärkte Fokus auf Robotik, die Integration von Industrie 4.0 und bildverarbeitungsgestützte Systeme beflügelt das Marktwachstum zusätzlich.

Marktübersicht für Bildverarbeitungssysteme

Maschinelle Bildverarbeitungssysteme (MVS) sind intelligente Automatisierungslösungen, die Kameras, Beleuchtung, Optik und Verarbeitungsalgorithmen nutzen, um menschliche Sehaufgaben in industriellen Prozessen nachzubilden. Diese Systeme optimieren Abläufe durch die Automatisierung von Inspektionen, die Steuerung von Robotern, die Durchführung von Mess- und Prüfaufgaben sowie die Reduzierung manueller Arbeitskraft. MVS-Lösungen werden in der Fertigungsindustrie, der Automobilindustrie, der Elektronikbranche und anderen Sektoren immer wichtiger, um Durchsatz, Genauigkeit und die Einhaltung von Qualitätsstandards zu steigern.

Passen Sie diesen Bericht Ihren Anforderungen an.

Sie erhalten eine kostenlose Anpassung aller Berichte – einschließlich Teilen dieses Berichts, Länderanalysen und Excel-Datenpaketen – sowie attraktive Angebote und Rabatte für Start-ups und Universitäten.

Markt für Bildverarbeitungssysteme: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen für Bildverarbeitungssysteme

Markttreiber:

- Zunehmender Bedarf an qualitativ hochwertiger Produktprüfung und schnelleren Produktionszyklen in der Fertigung.

- Zunehmende Verbreitung von Robotik und bildgestützter Automatisierung in Branchen wie der Automobil- und Elektronikindustrie.

- Regierungsinitiativen und Investitionen zur Förderung intelligenter Fabriken, Automatisierung und der Digitalisierung der Industrie.

Marktchancen:

- Expansion in aufstrebende Märkte, in denen die industrielle Automatisierung an Bedeutung gewinnt, z. B. in die Region Asien-Pazifik.

- Integration von Echtzeitanalysen, maschinellem Lernen und 3D-Vision-Systemen zur Ermöglichung komplexerer Inspektionen und Robotikanwendungen.

Marktsegmentierungsanalyse für Bildverarbeitungssysteme

Nach Typ:

- Intelligente Bildverarbeitungssysteme

- PC-basierte Bildverarbeitungssysteme

- 3D-Maschinensichtsysteme

Nach Komponente:

- Kameras

- Frame Grabbers

- Prozessoren

- Beleuchtung & Optik

- Bildverarbeitungssoftware

- Bildsensoren und andere

Über die Schnittstelle:

- USB 2.0 / USB 3.0

- Camera Link

- GigE

- CoaXPress

Nach Endverbrauchsbranche:

- Automobil

- Elektronik & Halbleiter

- Speisen und Getränke

- Pharmazeutika

- Logistik

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Süd- und Mittelamerika

- Naher Osten und Afrika

Markt für Bildverarbeitungssysteme – Regionale Einblicke

Die regionalen Trends und Einflussfaktoren auf den Markt für Bildverarbeitungssysteme im gesamten Prognosezeitraum wurden von den Analysten von The Insight Partners ausführlich erläutert. Dieser Abschnitt behandelt außerdem die Marktsegmente und die geografische Verteilung des Marktes für Bildverarbeitungssysteme in Nordamerika, Europa, Asien-Pazifik, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika.

Marktbericht zu Bildverarbeitungssystemen – Umfang

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 20,37 Milliarden US-Dollar |

| Marktgröße bis 2034 | 53,40 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 12,80 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nach Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte der Akteure im Bereich maschineller Bildverarbeitungssysteme: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Bildverarbeitungssysteme wächst rasant, angetrieben durch die steigende Nachfrage der Endnutzer. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile der Produkte. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Kundenbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

- Verschaffen Sie sich einen Überblick über die wichtigsten Akteure im Markt für Bildverarbeitungssysteme.

Marktanteilsanalyse für Bildverarbeitungssysteme nach Regionen

Nordamerika

- Besitzt einen bedeutenden Marktanteil, der auf eine fortschrittliche Fertigungsinfrastruktur, die frühzeitige Einführung von Automatisierung und Bildverarbeitungssystemen zurückzuführen ist.

- Trends: Verstärkter Einsatz von bildgesteuerter Robotik und intelligenten Kameras in der Automobil- und Elektronikbranche.

Europa

- Starke öffentliche und private Initiativen treiben die Fabrikautomatisierung und die Einhaltung von Normen in der Automobil- und Elektronikindustrie voran.

- Trends: Einführung interoperabler Bildverarbeitungssysteme und grenzüberschreitende Fertigungsoptimierung.

Asien-Pazifik

- Die am schnellsten wachsende Region ist auf den Ausbau der Produktionsstätten, die zunehmende industrielle Automatisierung und die verstärkten Investitionen in Bildverarbeitungssysteme zurückzuführen.

- Trends: Rasche Akzeptanz in China, Indien und Südostasien für Inspektion, Elektronikfertigung, Verpackung und Automobilindustrie.

Süd- und Mittelamerika

- Aufstrebender Markt mit wachsender Nachfrage nach kostengünstigen Bildverarbeitungssystemen und Fabrikautomation.

- Trend: Kleinere und mittelständische Hersteller setzen vermehrt auf modulare Bildverarbeitungssysteme zur Qualitätskontrolle.

Naher Osten und Afrika

- Entwicklungsregion mit Infrastrukturinvestitionen und zunehmender Automatisierung in der Fertigung, der Öl- und Gasindustrie sowie der Logistik.

- Trends: Zunehmende Nutzung von bildgestützter Inspektion und Robotik in neuen Produktionszentren.

Marktdichte der Akteure im Bereich maschineller Bildverarbeitungssysteme: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Bildverarbeitungssysteme umfasst sowohl globale Marktführer als auch zahlreiche regionale Spezialisten, was ihn mäßig wettbewerbsintensiv und technologieintensiv macht. Führende Anbieter differenzieren sich durch:

- Fortschrittliche Integration von 3D-Vision, KI und intelligenten Kameramodulen.

- Skalierbare Lösungen, die sowohl kleinen als auch großen Herstellern gerecht werden.

- Partnerschaften mit Anbietern von Robotik, Automatisierung und Software, um durchgängige, bildgesteuerte Lösungen anzubieten.

Zu den wichtigsten Unternehmen auf dem Markt für Bildverarbeitungssysteme gehören:

- Basler AG

- Cognex Corporation

- DataLogic SpA

- FLIR Systems, Inc.

- IDS Imaging Development Systems GmbH

- ISRA VISION AG

- Keyence Corporation

- OmniVision Technologies, Inc.

- Omron Microscan Systems, Inc.

- Toshiba Teli Corporation

Weitere im Rahmen der Studie analysierte Unternehmen:

- Microscan Systems, Inc.

- National Instruments Corporation

- Sony Corporation

- Teledyne Technologies Incorporated

- Allied Vision Technologies GmbH

- JAI A/S

- KRANKER ANG

- Baumer Holding AG

- Vision Components GmbH

- Tordivel AS

Marktneuigkeiten und aktuelle Entwicklungen im Bereich Bildverarbeitungssysteme

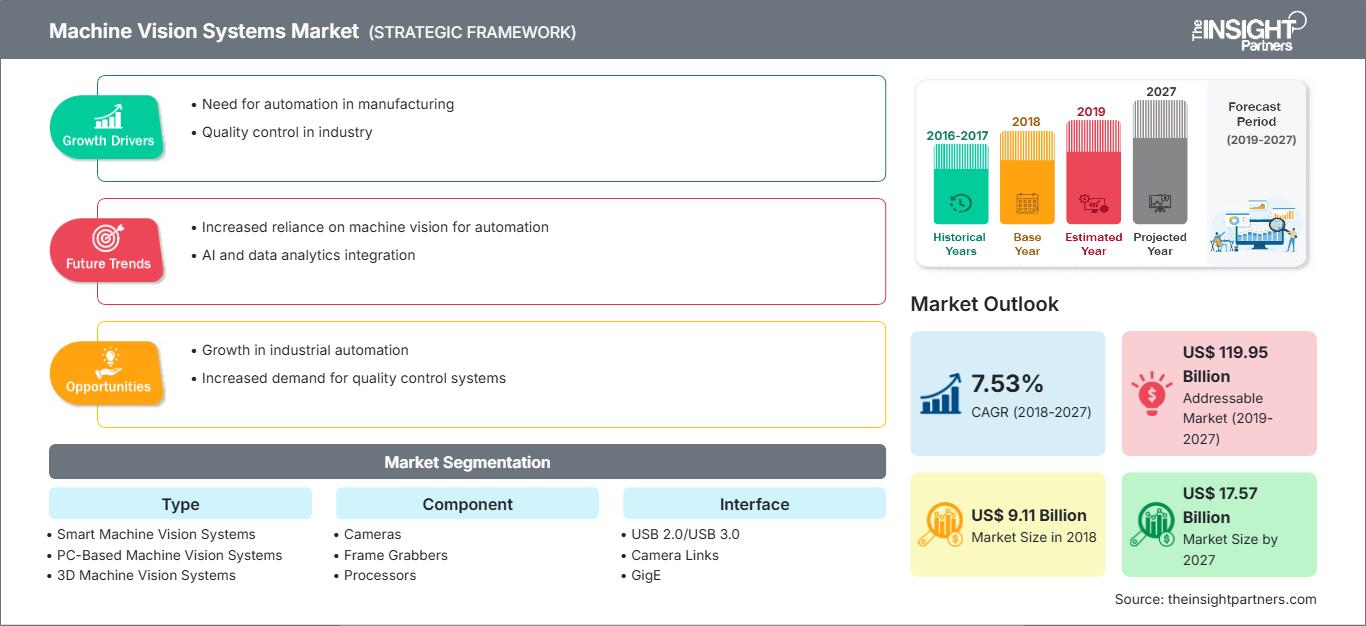

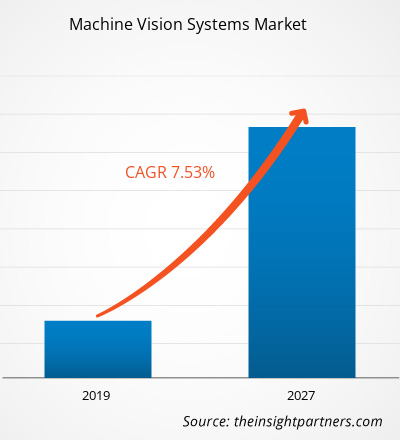

- Laut einer Pressemitteilung wird der Markt für Bildverarbeitungssysteme bis 2027 (Basisjahr 2018) voraussichtlich ein Volumen von 17,57 Milliarden US-Dollar erreichen.

- Der Markt sah starke Wachstumsaussichten für intelligente Bildverarbeitungssysteme und 3D-Bildverarbeitungssysteme, die zunehmend in den Bereichen Automobil, Elektronik & Halbleiter und Logistik eingesetzt werden.

- Die wichtigsten Akteure erweitern ihre Fähigkeiten durch KI, 3D-Bildgebung und Partnerschaften mit Roboterherstellern, um Inspektions- und Automatisierungsaufgaben zu verbessern.

Marktbericht zu Bildverarbeitungssystemen: Abdeckung und Ergebnisse

Der Bericht „Markt für maschinelle Bildverarbeitungssysteme – Globale Analyse und Prognosen (2021–2034)“ von The Insight Partners bietet folgende Informationen:

- Marktgröße und Prognose auf globaler, regionaler und Länderebene für alle wichtigen Segmente, die unter den Geltungsbereich fallen.

- Markttrends und -dynamiken wie Treiber, Hemmnisse und Chancen.

- Detaillierte PEST- und SWOT-Analyse.

- Die Analyse umfasst wichtige Markttrends, den regulatorischen Rahmen, die wichtigsten Akteure und aktuelle Entwicklungen.

- Branchenlandschaft und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominente Akteure und aktuelle Entwicklungen.

- Detaillierte Unternehmensprofile der wichtigsten Akteure.

Naveen ist ein erfahrener Marktforschungs- und Beratungsexperte mit über 9 Jahren Erfahrung in kundenspezifischen, syndizierten und Beratungsprojekten. In seiner aktuellen Funktion als Associate Vice President hat er erfolgreich Stakeholder entlang der gesamten Projektwertschöpfungskette gemanagt und ist Autor von über 100 Forschungsberichten und über 30 Beratungsaufträgen. Seine Arbeit erstreckt sich auf Industrie- und Regierungsprojekte und trägt maßgeblich zum Kundenerfolg und zur datengesteuerten Entscheidungsfindung bei.

Naveen hat einen Ingenieursabschluss in Elektronik und Kommunikation von der VTU, Karnataka, und einen MBA in Marketing und Operations von der Manipal University. Er ist seit 9 Jahren aktives IEEE-Mitglied und nimmt an Konferenzen und technischen Symposien teil und engagiert sich ehrenamtlich auf Sektions- und regionaler Ebene. Vor seiner aktuellen Position arbeitete er als Associate Strategic Consultant bei IndustryARC und als Industrial Server Consultant bei Hewlett Packard (HP Global).

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends