Offshore-Pipeline-Markt – Erkenntnisse durch globale und regionale Analyse – Prognose bis 2031

Marktgröße und Prognose für Offshore-Pipelines (2021 – 2031), Bericht über globale und regionale Anteile, Trends und Wachstumschancenanalyse: Nach Durchmesser (weniger als 24 Zoll und mehr als 24 Zoll), Leitungstyp (Exportleitung, Transportleitung und andere), Produkt (Öl, Erdgas und raffinierte Produkte) und Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00006141

- Kategorie : Energie und Leistung

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : May 16, 2024

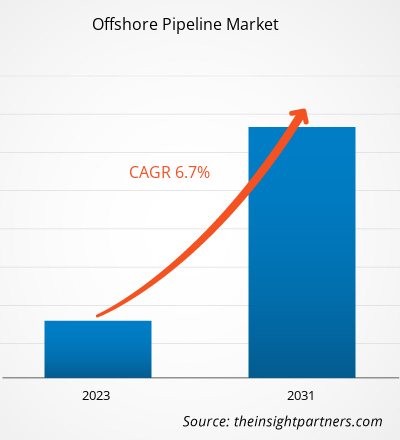

Der Markt für Offshore-Pipelines soll von 15.277,3 Millionen US-Dollar im Jahr 2022 auf 21.044,7 Millionen US-Dollar im Jahr 2031 anwachsen. Der Markt soll zwischen 2023 und 2031 eine durchschnittliche jährliche Wachstumsrate von 6,7 % verzeichnen. Zu den wichtigsten Faktoren, die den Markt für Offshore-Pipelines antreiben, zählen die zunehmende Offshore-Öl- und Gasproduktion, die steigende Produktion neuer Ölbohranlagen und der Umbau bestehender und alter Offshore-Öl- und Gasbohranlagen.CAGR of 6.7% during 2023–2031. Increasing offshore oil and gas production, rising production of new oil rigs, and reconstruction of existing and old offshore oil and gas rigs are among the key factors driving the offshore pipeline market.

Offshore-Pipeline-Marktanalyse

Aufgrund der steigenden Zahl von Erdgasprojekten sowie der Entdeckung neuer Ölfelder, insbesondere an abgelegenen Standorten, wird für den Offshore-Pipeline-Markt ein beträchtliches Wachstum erwartet. Darüber hinaus hat die Erschöpfung der vorhandenen Öl- und Gasreserven in verschiedenen Ländern eine Nachfrage nach grenzüberschreitenden Pipelines für die Versorgung mit Öl- und Gasprodukten geschaffen, was das Wachstum des Offshore-Pipeline-Marktes ankurbelt. Die steigende Nachfrage nach kostengünstigen Transportmethoden für Öl und Gas ist ebenfalls einer der Hauptfaktoren, die voraussichtlich die Nachfrage nach Offshore-Pipelines im Öl- und Gassektor weltweit ankurbeln werden.

Offshore-Pipeline-Marktübersicht

Bevölkerungsexplosion und entsprechende Industrialisierung haben den Energiebedarf auf globaler Ebene angekurbelt. Der Anstieg des Energieverbrauchs hat den Bedarf an Öl und Gas in Entwicklungs- und Industrieländern erhöht. Dies hat zu einer steigenden Nachfrage nach Offshore-Pipeline-Infrastruktur auf der ganzen Welt geführt. Der asiatisch-pazifische Raum ist der größte Verbraucher von Rohöl und Gas. Darüber hinaus melden hochindustrialisierte Länder im asiatisch-pazifischen Raum, darunter China, Indien, Japan und Südkorea, einen steigenden Gesamtenergieverbrauch. Ihr Fokus auf die Steigerung der heimischen Ölproduktion durch verschiedene verbesserte Ölgewinnungstechniken fördert den Markt für Offshore-Pipelines im asiatisch-pazifischen Raum, um den wachsenden Ölbedarf zu decken.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Offshore-Pipeline-Markt: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Treiber und Chancen auf dem Offshore-Pipeline-Markt

Steigende Nachfrage nach Erdgas und Rohöl

Die Nachfrage nach Öl und Erdgas steigt weltweit stetig an. Die USA und China verzeichnen das stärkste Wachstum. Der Anstieg der Industrieproduktion sowie die hohe Nachfrage nach Transportdienstleistungen kurbeln die Nachfrage nach Petrochemikalien an und befeuern damit das Wachstum des Offshore-Pipeline-Marktes. Darüber hinaus ist das weltweite Wachstum des Luftverkehrs, insbesondere in Asien, ein weiterer wichtiger Faktor, der zu einem erhöhten Ölverbrauch führt.fuelling the growth of the offshore pipeline market. Moreover, the growth in air traffic volumes worldwide, particularly in Asia, is another significant factor resulting in increased oil consumption.

Die Organisation erdölexportierender Länder (OPEC) veröffentlichte im Oktober 2020 den „OPEC World Oil Outlook 2020“. Demnach führte die COVID-19-Pandemie zu einem Rückgang der Ölnachfrage; es wurde jedoch erwartet, dass die globale Energienachfrage in Zukunft konstant wachsen und bis 2045 um beachtliche 25 % steigen würde. Der Ausblick geht außerdem davon aus, dass Öl der größte Beitragszahler im Energiemix sein wird und bis 2045 27 % des gesamten Energieanteils ausmachen wird. Die Nachfrage nach Ölprodukten wird in den OECD-Ländern im Zeitraum 2022–2025 voraussichtlich um mehr als 47 Mb/Tag steigen. Andererseits wird die Nachfrage in Nicht-OECD-Ländern im Prognosezeitraum voraussichtlich um 22,5 MB/Tag steigen.OECD countries. On the other hand, the demand in non-OECD countries is projected to rise by 22.5 MB/day during the forecast period.

Ständige Bemühungen zur Verbesserung der Ölförderung

Verschiedene Länder investieren in die Wiederbelebung ihrer bestehenden Ölressourcen, um die heimische Ölproduktion anzukurbeln und ihre Abhängigkeit von Ölimporten zu verringern. In den letzten Jahrzehnten wurde die Dampfinjektion kommerziell genutzt, um die Förderung aus konventionellen Schweröllagerstätten in ihren späteren Entwicklungsstadien zu verbessern. Der eingespritzte Dampf erhöht den Gesamtdruck einer Offshore-Öllagerstätte, was dazu beiträgt, die Mobilitätsrate des Rohöls zu verbessern und ein effizientes Fließen zu ermöglichen. Infolgedessen tragen die verbesserten Ölgewinnungsmethoden dazu bei, die Förderprozesse in bestehenden Offshore-Ölquellen zu revitalisieren. Daher wird erwartet, dass die Ausweitung der Öl- und Gasförderung den Akteuren auf dem Offshore-Pipeline-Markt in den kommenden Jahren vielversprechende Wachstumschancen bietet.

Segmentierungsanalyse des Offshore-Pipeline-Marktberichts

Schlüsselsegmente, die zur Ableitung der Offshore-Pipeline-Marktanalyse beigetragen haben, sind Typ und Endbenutzer.

- Basierend auf dem Durchmesser wurde der Offshore-Pipeline-Markt in weniger als 24 Zoll und mehr als 24 Zoll unterteilt. Das Segment weniger als 24 Zoll hatte im Jahr 2023 einen größeren Marktanteil.

- Nach Leitungstyp ist der Offshore-Pipeline-Markt in Transportleitungen, Exportleitungen und andere unterteilt. Das Segment der Transportleitungen hatte im Jahr 2023 den größten Marktanteil.

- Produktseitig ist der Markt in Öl, Gas und raffinierte Produkte segmentiert. Das Segment der raffinierten Produkte dominierte den Markt im Jahr 2023.

Offshore-Pipeline-Marktanteilsanalyse nach Geografie

Der geografische Umfang des Offshore-Pipeline-Marktberichts ist hauptsächlich in fünf Regionen unterteilt: Nordamerika, Europa, Asien-Pazifik, Naher Osten und Afrika sowie Süd- und Mittelamerika.

Europa dominierte den Offshore-Pipeline-Markt im Jahr 2023. Der Markt in Europa ist in Deutschland, Norwegen, Italien, Russland, Großbritannien und den Rest Europas unterteilt. Europa ist der zweitgrößte Produzent von Erdölprodukten weltweit und verfügt über eine Ölraffineriekapazität von mehr als 15 %. Die Gasindustrie in Europa hat aufgrund der steigenden LNG-Nachfrage verschiedene Verschiebungen erlebt. Darüber hinaus behaupten Norwegen und Russland weiterhin ihre Position als Erdgaslieferanten, während Deutschland, Frankreich und Italien die Hauptimporteure von Erdgas sind. Daher werden die steigende Zahl von Erdgasprojekten sowie die Entdeckung neuer Ölfelder, insbesondere in abgelegenen Gebieten, höchstwahrscheinlich die Nachfrage nach Offshore-Pipelinesystemen und -diensten beschleunigen.

Regionale Einblicke in den Offshore-Pipeline-Markt

Die regionalen Trends und Faktoren, die den Offshore-Pipeline-Markt im Prognosezeitraum beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie des Offshore-Pipeline-Marktes in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Offshore-Pipeline-Markt

Umfang des Offshore-Pipeline-Marktberichts

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2022 | 15.277,3 Millionen US-Dollar |

| Marktgröße bis 2031 | 21.044,7 Millionen US-Dollar |

| Globale CAGR (2023 - 2031) | 6,7 % |

| Historische Daten | 2021-2022 |

| Prognosezeitraum | 2023–2031 |

| Abgedeckte Segmente |

Nach Durchmesser

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Akteure auf dem Offshore-Pipeline-Markt: Auswirkungen auf die Geschäftsdynamik verstehen

Der Offshore-Pipeline-Markt wächst rasant, angetrieben durch die steigende Endverbrauchernachfrage aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung der Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten auf dem Offshore-Pipeline-Markt tätigen Unternehmen sind:

- Enbridge Inc

- Saipem SpA

- McDermott International Ltd.

- Allseas Group SA

- China Petroleum Pipeline Engineering Ltd

- Kinder Morgan

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Offshore-Pipeline-Markt

Neuigkeiten und aktuelle Entwicklungen zum Offshore-Pipeline-Markt

Der Offshore-Pipeline-Markt wird durch die Erhebung qualitativer und quantitativer Daten nach Primär- und Sekundärforschung bewertet, die wichtige Unternehmensveröffentlichungen, Verbandsdaten und Datenbanken umfasst. Nachfolgend sind einige der Entwicklungen auf dem Offshore-Pipeline-Markt aufgeführt:

- Im Juli 2023 erweiterten Kinder Morgan und Howard Energy Partners ihre Erdgastransportsysteme in Eagle Ford. Tejas baut eine 67 Meilen lange Pipeline und Dos Caminos eine 62 Meilen lange Pipeline. Die Projekte sollen im vierten Quartal 2023 abgeschlossen sein und bis zu 2 Milliarden Kubikfuß Erdgas pro Tag an die Märkte an der US-Golfküste liefern. Das 251 Millionen US-Dollar teure Erweiterungsprojekt ist ein wichtiges Versorgungsglied für Stromerzeuger , Industriekunden und LNG-Exporteure entlang des innerstaatlichen Pipelinenetzes von Texas.

- Im Februar 2023 unterzeichnete Enagas eine Vereinbarung mit Reganosa, in deren Rahmen Enagas 54 Millionen Euro an Reganosa für den Kauf eines 130 km langen Netzes von Erdgaspipelines zahlte. Der effiziente Betrieb und die Versorgungssicherheit des iberischen Gasmarktes hängen von diesem Netz ab.

Bericht zum Offshore-Pipeline-Markt – Umfang und Ergebnisse

Der Bericht „Marktgröße und Prognose für Offshore-Pipelines (2021–2031)“ bietet eine detaillierte Analyse des Marktes, die die folgenden Bereiche abdeckt:

- Offshore-Pipeline-Marktgröße und -prognose auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt sind

- Offshore-Pipeline-Markttrends sowie Marktdynamik wie Treiber, Einschränkungen und wichtige Chancen

- Detaillierte PEST/Porters Five Forces- und SWOT-Analyse

- Analyse des Offshore-Pipeline-Marktes mit wichtigen Markttrends, globalen und regionalen Rahmenbedingungen, wichtigen Akteuren, Vorschriften und aktuellen Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse, einschließlich Marktkonzentration, Heatmap-Analyse, prominenten Akteuren und aktuellen Entwicklungen für den Offshore-Pipeline-Markt

- Detaillierte Firmenprofile

Nivedita ist eine versierte Forschungsexpertin mit über 9 Jahren Erfahrung in Marktforschung und Unternehmensberatung. Sie ist derzeit als Projektmanagerin im IKT-Bereich bei The Insight Partners tätig und verfügt über umfassende Fachkenntnisse in der Leitung und Durchführung von syndizierten, kundenspezifischen, abonnementbasierten und beratenden Forschungsaufträgen in unterschiedlichen Technologiesektoren.

Mit einer nachgewiesenen Erfolgsbilanz bei der Bereitstellung datengestützter Analysen und umsetzbarer Erkenntnisse war Nivedita maßgeblich an mehreren kritischen Projekten beteiligt. Ihre Arbeit umfasst die vollständige Projektabwicklung – vom Verständnis der Kundenziele über die Analyse von Markttrends bis hin zur Ableitung strategischer Empfehlungen. Sie hat umfassend mit führenden IKT-Unternehmen zusammengearbeitet und ihnen geholfen, Marktchancen zu erkennen und Branchenveränderungen zu meistern.

Nivedita hat einen MBA in Management vom IMS, Dehradun. Vor ihrem Eintritt bei The Insight Partners sammelte sie wertvolle Erfahrungen bei MarketsandMarkets und Future Market Insights in Pune, wo sie verschiedene Forschungspositionen innehatte und sich ein solides Fundament in Branchenanalyse und Kundenbindung erarbeitete.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends