Marktwachstum und Ausblick für Präzisionsdiagnostik bis 2034

Marktgröße und Prognose für Präzisionsdiagnostik (2021–2034): Globaler und regionaler Marktanteil, Trends und Wachstumspotenzialanalyse. Berichtsabdeckung: Nach Typ (Gentests, Spezialtests); Anwendung (Onkologie, Kardiologie, Atemwegserkrankungen, Immunologie); Endnutzer (Klinische Labore, Krankenhäuser, Häusliche Pflege); und Geografie

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00029425

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : January 27, 2026

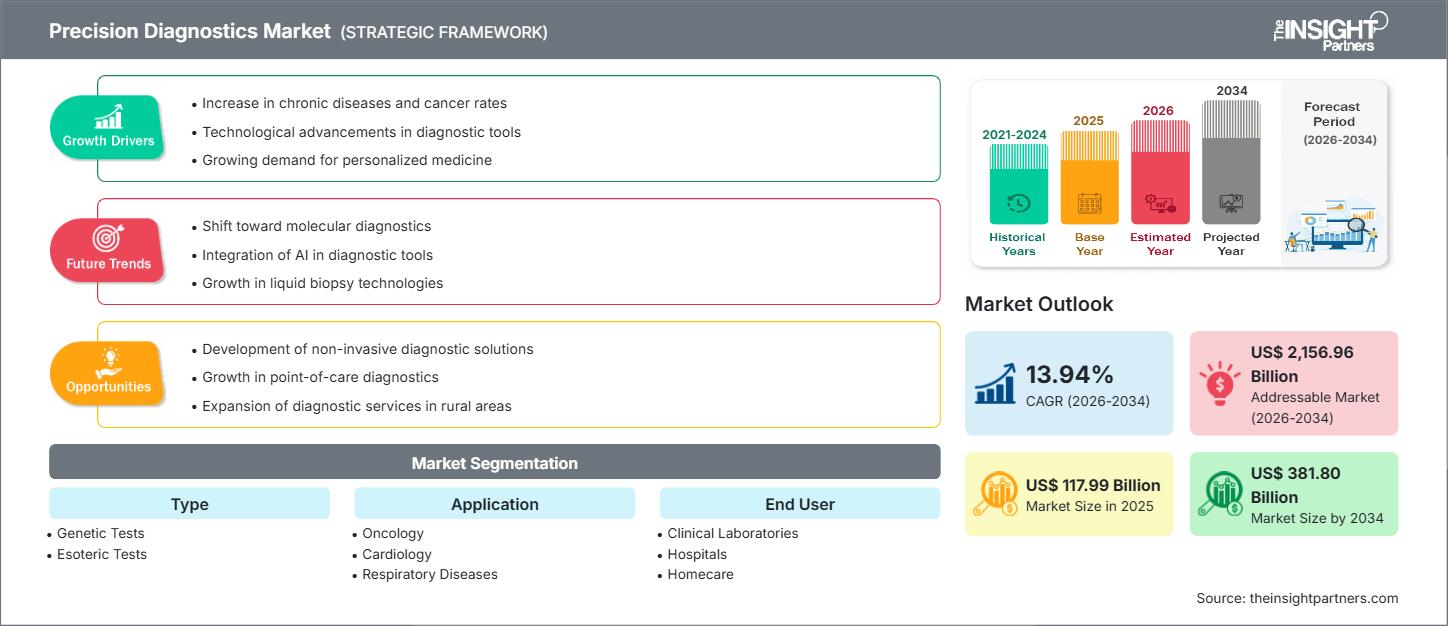

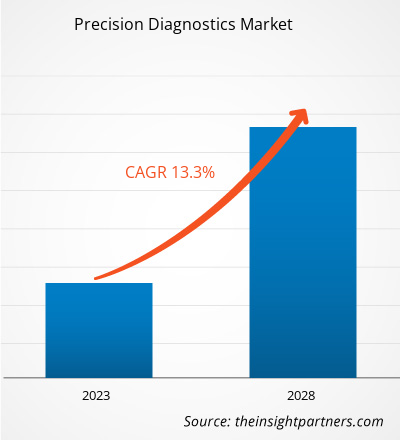

Der Markt für Präzisionsdiagnostik wird bis 2034 voraussichtlich ein Volumen von 381,80 Milliarden US-Dollar erreichen, gegenüber 117,99 Milliarden US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Zeitraum 2026–2034 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 13,94 % verzeichnen wird.

Marktanalyse für Präzisionsdiagnostik

Der Markt für Präzisionsdiagnostik wächst rasant, angetrieben durch den Trend zur personalisierten Medizin, den Fortschritt molekularer Diagnosetechnologien wie der Next-Generation-Sequenzierung (NGS) und die zunehmende Verbreitung chronischer und infektiöser Erkrankungen, insbesondere in der Onkologie. Diese Diagnostikverfahren, darunter Gentests, Flüssigbiopsien und Begleitdiagnostik, sind entscheidend für die Identifizierung spezifischer Biomarker, ermöglichen eine frühere und genauere Krankheitserkennung und unterstützen die Auswahl gezielter Therapien. Technologien wie Genomik, Proteomik und fortschrittliche Datenanalyse/KI werden zunehmend integriert, um komplexe Patientendaten zu interpretieren und Therapieansprechen vorherzusagen.

Marktübersicht Präzisionsdiagnostik

Präzisionsdiagnostik ist ein Teilgebiet der Präzisionsmedizin, das sich darauf konzentriert, durch die Analyse genetischer, umweltbedingter und lebensstilbedingter Faktoren eine präzise und zeitnahe Erklärung für die gesundheitlichen Probleme eines Patienten zu liefern. Dies führt zu maßgeschneiderten Behandlungsplänen und löst den bisherigen Einheitsansatz ab. Diese Instrumente ermöglichen ein tiefes molekulares Verständnis von Krankheiten, die Auswahl der wirksamsten Therapien und die Verbesserung der Behandlungsergebnisse. Zu den wichtigsten Produkten gehören spezialisierte Diagnostik-Kits, Assays und hochentwickelte Geräte für Tests wie NGS und PCR.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für Präzisionsdiagnostik: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen im Bereich Präzisionsdiagnostik

Markttreiber:

- Zunehmende Verbreitung chronischer Krankheiten und Krebs: Die weltweit steigende Inzidenz chronischer Krankheiten, insbesondere von Krebs, erfordert den Einsatz präziser Diagnoseverfahren zur frühzeitigen und genauen Erkennung sowie zur Entwicklung personalisierter Behandlungsstrategien, was die Marktnachfrage ankurbelt.

- Technologische Fortschritte in der Molekulardiagnostik: Kontinuierliche Innovationen bei Technologien wie Next-Generation Sequencing (NGS), Polymerase Chain Reaction (PCR) und Liquid Biopsy haben die Kosten gesenkt, die Genauigkeit erhöht und die Anwendung der Präzisionsdiagnostik erweitert, wodurch deren Akzeptanz beschleunigt wurde.

- Steigende Nachfrage nach personalisierter Medizin: Der zunehmende Fokus auf die Erstellung individualisierter Behandlungspläne auf der Grundlage des einzigartigen genetischen Profils eines Patienten ist ein grundlegender Treiber für die Entwicklung und Anwendung von Begleitdiagnostika und anderen Präzisionstests.

Marktchancen:

- Integration von Künstlicher Intelligenz (KI) und Maschinellem Lernen (ML): KI/ML-Tools bieten erhebliche Möglichkeiten, indem sie die Analyse komplexer genomischer, bildgebender und klinischer Daten verbessern, was die Geschwindigkeit und Genauigkeit der Diagnose sowie die Vorhersage von Patientenergebnissen verbessert.

- Ausbau der Begleitdiagnostik (CDx): Die Entwicklung von CDx, bei der ein spezifischer Diagnosetest mit einem entsprechenden Therapeutikum verknüpft wird, bietet ein hohes Wachstumspotenzial, da Pharmaunternehmen zunehmend zielgerichtete Therapien auf den Markt bringen, die einen Diagnosetest zur Patientenauswahl erfordern.

- Zunehmende Verbreitung nicht-invasiver Tests (Flüssigbiopsie): Die Flüssigbiopsie, die Biomarker in Körperflüssigkeiten wie Blut nachweist, bietet eine weniger invasive Alternative zur Gewebebiopsie. Ihr Einsatz in der Krebsvorsorge, der Rezidivüberwachung und der Therapieauswahl birgt ein erhebliches Marktpotenzial.

Marktbericht für Präzisionsdiagnostik: Segmentierungsanalyse

Der Marktanteil der Präzisionsdiagnostik wird in verschiedenen Segmenten analysiert, um ein besseres Verständnis ihrer Struktur, ihres Wachstumspotenzials und der sich abzeichnenden Trends zu ermöglichen. Nachfolgend ist ein Standard-Segmentierungsansatz dargestellt, der in den meisten Branchenberichten verwendet wird:

Nach Typ:

- Gentests

- Esoterische Tests

Auf Antrag:

- Onkologie

- Kardiologie

- Atemwegserkrankungen

- Immunologie

Vom Endbenutzer:

- Klinische Labore

- Krankenhäuser

- Häusliche Pflege

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Süd- und Mittelamerika

- Naher Osten und Afrika

Markt für Präzisionsdiagnostik – Regionale Einblicke

Die regionalen Trends und Einflussfaktoren auf den Markt für Präzisionsdiagnostik im gesamten Prognosezeitraum wurden von den Analysten von The Insight Partners eingehend erläutert. Dieser Abschnitt behandelt außerdem die Marktsegmente und die geografische Verteilung des Marktes für Präzisionsdiagnostik in Nordamerika, Europa, Asien-Pazifik, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika.

Berichtsumfang zum Markt für Präzisionsdiagnostik

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 117,99 Milliarden US-Dollar |

| Marktgröße bis 2034 | 381,80 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 13,94 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nach Typ

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte der Akteure im Bereich der Präzisionsdiagnostik: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Präzisionsdiagnostik wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile der Produkte. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Kundenbedürfnissen gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

- Verschaffen Sie sich einen Überblick über die wichtigsten Akteure im Markt für Präzisionsdiagnostik.

Marktanteilsanalyse für Präzisionsdiagnostik nach Regionen

Nordamerika wird voraussichtlich den Markt für Präzisionsdiagnostik dominieren, gefolgt von Europa. Die Vormachtstellung dieser Region beruht auf einer robusten und fortschrittlichen Gesundheitsinfrastruktur, signifikanten Investitionen in Forschung und Entwicklung im Bereich Biotechnologie und Genomik sowie der frühen Einführung fortschrittlicher Präzisionstherapien, insbesondere in den USA.

Es wird erwartet, dass die Region Asien-Pazifik im Prognosezeitraum der am schnellsten wachsende regionale Markt sein wird. Treiber dieser Entwicklung sind steigende Gesundheitsausgaben, ein zunehmendes Bewusstsein für personalisierte Medizin, staatlich geförderte Initiativen zur Genomforschung in Ländern wie China und Indien sowie die zunehmende Verbreitung chronischer Krankheiten.

Nachfolgend eine Zusammenfassung der Marktanteile und Trends nach Regionen:

1. Nordamerika

- Marktanteil: Besitzt den größten Marktanteil, was auf eine robuste IT- und Gesundheitsinfrastruktur sowie die Präsenz führender Diagnostik- und Pharmaunternehmen zurückzuführen ist.

-

Wichtigste Einflussfaktoren:

- Hohe staatliche und private Investitionen in Genommedizin und Forschung & Entwicklung.

- Günstige Erstattungspolitik für fortgeschrittene Diagnosetests.

- Frühe und weitverbreitete Einführung von NGS und Begleitdiagnostik.

- Trends: Rasante Integration von KI für die diagnostische Bildanalyse und die Interpretation genetischer Daten; zunehmender Fokus auf die Flüssigbiopsie zur Krebsüberwachung.

2. Europa

- Marktanteil: Besitzt den zweitgrößten Marktanteil, was auf den zunehmenden Fokus des Gesundheitswesens auf personalisierte Medizin und die alternde Bevölkerung zurückzuführen ist.

-

Wichtigste Einflussfaktoren:

- Regierungsinitiativen und Fördermittel zur Integration von Präzisionsdiagnostik in die öffentlichen Gesundheitssysteme.

- Starke Präsenz führender Biotech- und Diagnostikunternehmen (z. B. in Deutschland, Großbritannien).

- Zunehmende Nutzung molekularer Diagnostik zur Behandlung von Infektionskrankheiten.

- Trends: Schwerpunkt auf der Entwicklung standardisierter und validierter Diagnoseplattformen; Fokus auf ethischen und regulatorischen Rahmenbedingungen für die Nutzung genetischer Daten.

3. Asien-Pazifik

- Marktanteil: Der am schnellsten wachsende regionale Markt, angetrieben durch rasche Verbesserungen beim Zugang zur Gesundheitsversorgung und steigende Investitionen.

-

Wichtigste Einflussfaktoren:

- Staatlich geförderte Programme zur Modernisierung des Gesundheitswesens und zur Digitalisierung der Wirtschaft.

- Zunehmende Verbreitung chronischer Krankheiten und genetischer Störungen in dicht besiedelten Ländern (China, Indien).

- Ausbau der inländischen Produktionskapazitäten für Diagnostika.

- Trends: Zunehmender Einsatz kostengünstiger NGS-Technologien; Wachstum der molekularen Diagnostik für lokale Krebs- und Infektionskrankheitsvarianten.

4. Süd- und Mittelamerika

- Marktanteil: Aufstrebende Region mit wachsender Akzeptanz, die durch Gesundheitsreformen und steigendes Bewusstsein vorangetrieben wird.

-

Wichtigste Einflussfaktoren:

- Steigende Gesundheitsausgaben und Modernisierung der klinischen Labore.

- Ausbau erschwinglicher Diagnostikleistungen, einschließlich hauseigener Tests in großen Krankenhäusern.

- Trends: Fokus auf die Implementierung grundlegender molekularer Diagnosetests; Expansion globaler Diagnostikanbieter in lokale Märkte.

5. Naher Osten und Afrika

- Marktanteil: Aufstrebender Markt mit starkem Potenzial, angeführt von Initiativen zur digitalen Transformation in den Ländern des Golf-Kooperationsrats (GCC) und Südafrika.

-

Wichtigste Einflussfaktoren:

- Wichtige nationale Strategien für digitale Gesundheit und KI zur Förderung von Innovationen im Gesundheitswesen.

- Steigende Investitionen in spezialisierte Gesundheitseinrichtungen und Genforschungszentren.

- Trends: Einführung fortschrittlicher Sequenzierungsmethoden für Erbkrankheiten; Nutzung von Telemedizin und patientennaher Diagnostik zur Verbesserung des Zugangs in abgelegenen Gebieten.

Marktdichte der Akteure im Bereich der Präzisionsdiagnostik: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Präzisionsdiagnostik ist durch den zunehmenden Wettbewerb zwischen großen globalen Anbietern von Life-Science- und Diagnostiklösungen sowie aufstrebenden Nischenanbietern und spezialisierten Startups, die sich auf Flüssigbiopsie, Bioinformatik und KI-gestützte Lösungen konzentrieren, stark geprägt. Unternehmen treiben Innovationen voran, um ihre Marktposition zu stärken und die steigende Nachfrage nach zielgerichteten und präzisen Diagnoseverfahren zu decken.

Der Wettbewerb zwingt die Anbieter dazu, sich durch Folgendes zu differenzieren:

- Unternehmen kombinieren diagnostische Angebote mit therapeutischen Entwicklungspipelines, um integrierte Komplettlösungen für eine personalisierte Patientenversorgung anzubieten.

- Intensiver Fokus auf die Entwicklung schnellerer, sensitiverer und kostengünstigerer Next-Generation-Sequenzierungsplattformen (NGS) und spezialisierter Testkits.

- Organisationen integrieren künstliche Intelligenz in Diagnoseplattformen, um die Datenanalyse zu automatisieren, die Interpretation komplexer Genomdaten zu verbessern und die Diagnosegeschwindigkeit zu erhöhen.

Chancen und strategische Schritte

- Große Pharma- und Diagnostikunternehmen kooperieren mit Biotech-Startups und akademischen Einrichtungen, um die Entwicklung neuartiger Biomarker und begleitender Diagnostika zu beschleunigen.

- Die Nutzung von Multi-Omics-Daten (Genomik, Proteomik, Metabolomik) und Big-Data-Analysen eröffnet neue Einnahmequellen, indem sie umfassende diagnostische und prädiktive Gesundheitseinblicke bietet.

- Die Akteure expandieren in wachstumsstarke Regionen wie den asiatisch-pazifischen Raum und entwickeln regionsspezifische Tests, um auf lokale Krankheitsmuster und regulatorische Bedürfnisse einzugehen.

Die wichtigsten Unternehmen auf dem Markt für Präzisionsdiagnostik sind:

- Quest Diagnostics Incorporated

- QIAGEN

- Swiss Precision Diagnostics GmbH

- Koninklijke Philips NV

- Lantheus Medical Imaging, Inc.

- Siemens Healthineers AG

- Abbott

- Novartis AG

- Sanofi

Hinweis: Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge geordnet.

Neuigkeiten und aktuelle Entwicklungen im Markt für Präzisionsdiagnostik

- Am 20. November 2025 gaben Abbott und Exact Sciences beispielsweise eine endgültige Vereinbarung bekannt, wonach Abbott Exact Sciences übernehmen wird. Dies ermöglicht Abbott den Einstieg und die Marktführerschaft in schnell wachsenden Segmenten der Krebsdiagnostik und damit den Zugang zu Millionen weiterer Menschen. Die Übernahme erweitert Abbotts bereits hohes einstelliges Wachstumsprofil um einen neuen Wachstumsbereich und sichert dem Unternehmen die Führungsposition in den schnell wachsenden US-amerikanischen Segmenten für Krebsvorsorge und Präzisionsonkologie mit einem Volumen von 60 Milliarden US-Dollar.

- Am 19. November 2025 gab Royal Philips, ein weltweit führendes Unternehmen im Bereich Gesundheitstechnologie, die Erweiterung seiner Partnerschaft mit Cortechs.ai, einem Pionier im Bereich quantitativer Neuroimaging-Lösungen, bekannt. Die Zusammenarbeit stärkt Philips' führende Position in der präzisen Neurodiagnostik. Durch die Kombination der MR-Technologien der nächsten Generation von Philips mit der KI-gestützten Nachbearbeitungssoftware für quantitative Neuroimaging von Cortechs.ai wird die Erkennung, Überwachung und Behandlung neurologischer Erkrankungen grundlegend verändert.

- Am 18. Juni 2025 gaben QIAGEN und GENCURIX, Inc. eine neue Partnerschaft zur Entwicklung von Onkologie-Assays für die QIAcuityDx-Plattform bekannt, einem leistungsstarken digitalen PCR-System, das für die klinische Diagnostik entwickelt wurde.

- Am 15. Juni 2025 gaben WILMINGTON und Incyte beispielsweise eine Zusammenarbeit im Bereich der Präzisionsmedizin bekannt, um ein neuartiges Diagnosepanel zu entwickeln, das Incytes umfangreiches Portfolio an experimentellen Therapien für Patienten mit myeloproliferativen Neoplasien (MPN), einer Gruppe seltener Blutkrebsarten, unterstützen soll. Dazu gehört auch Incytes monoklonaler Antikörper INCA033989, der auf mutiertes Calreticulin (mutCALR) abzielt und bei Myelofibrose (MF) und essentieller Thrombozythämie (ET) entwickelt wird.

Marktbericht Präzisionsdiagnostik: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für Präzisionsdiagnostik (2021–2034)“ bietet eine detaillierte Analyse des Marktes und deckt folgende Bereiche ab:

- Marktgröße und Prognose für Präzisionsdiagnostik auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Geltungsbereich abgedeckt werden

- Markttrends im Bereich der Präzisionsdiagnostik sowie Marktdynamiken wie Treiber, Hemmnisse und wichtige Chancen

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für Präzisionsdiagnostik: Wichtige Markttrends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Rahmenbedingungen und aktuelle Marktentwicklungen

- Branchenlandschaft und Wettbewerbsanalyse mit Fokus auf Marktkonzentration, Heatmap-Analyse, führende Akteure und aktuelle Entwicklungen im Markt für Präzisionsdiagnostik. Detaillierte Unternehmensprofile.

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends