Marktstrategien für Wirbelsäulenimplantate, Top-Player, Wachstumschancen, Analyse und Prognose bis 2031

Marktgröße und Prognose für Wirbelsäulenimplantate (2021–2031), globaler und regionaler Marktanteil, Trend- und Wachstumschancenanalyse. Berichtsabdeckung: Nach Produkt (Fusions-Wirbelsäulenimplantate und Nicht-Fusions-Wirbelsäulenimplantate), Verfahren (Foraminotomie, Laminektomie, Bandscheibenersatz, Wirbelsäulenversteifung und Diskektomie), Material (Titan, Kohlenstofffaser und Edelstahl), Endnutzer (Krankenhäuser, Fachkliniken und ambulante Operationszentren) und Geografie (Nordamerika, Europa, Asien-Pazifik, Süd- und Mittelamerika sowie Naher Osten und Afrika).

- Status : Veröffentlichte Daten

- Berichtscode : TIPHE100000993

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : May 30, 2024

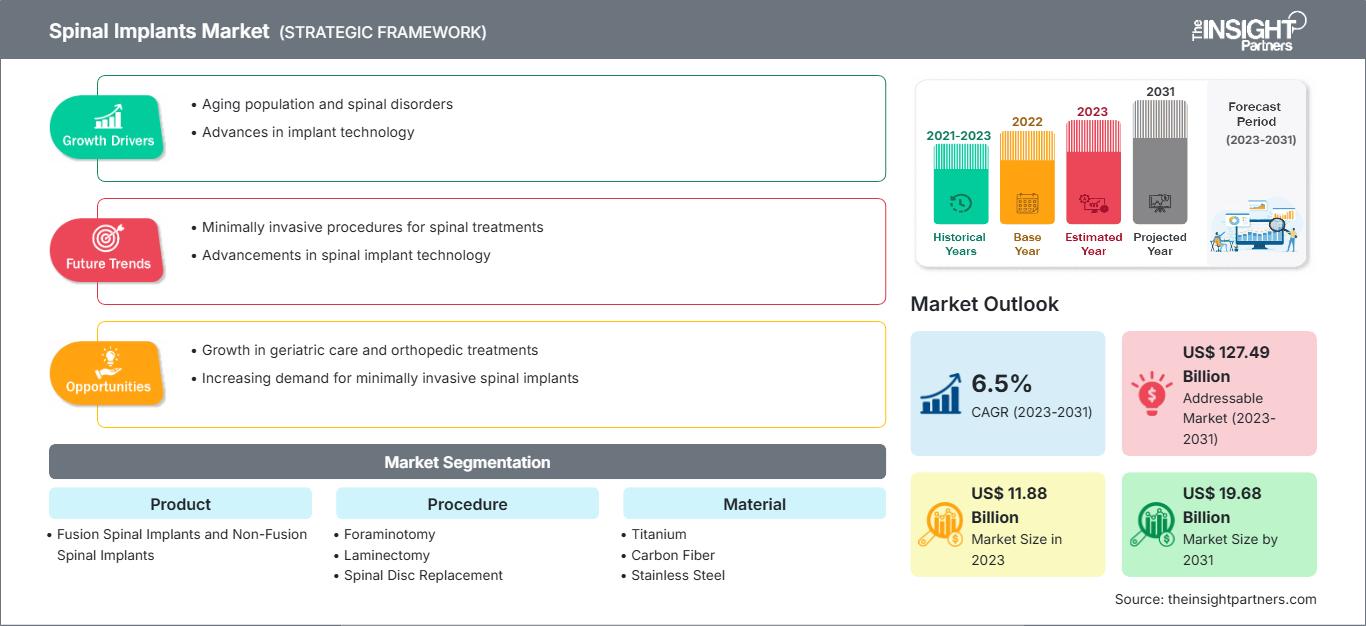

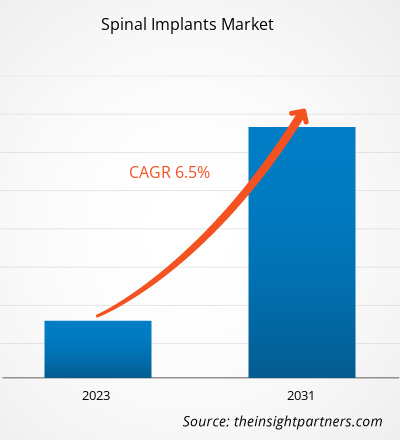

Es wird erwartet, dass der Markt für Wirbelsäulenimplantate bis 2031 ein Volumen von 19,34 Milliarden US-Dollar erreichen wird. Für den Zeitraum 2025–2031 wird ein durchschnittliches jährliches Wachstum von 105,5 % prognostiziert.

Markteinblicke und Analystenmeinung:

Wirbelsäulenimplantate sind medizinische Geräte, die bei Wirbelsäulenstabilisierungsverfahren eingesetzt werden, um die Wirbelsäule zu stärken, Fehlstellungen zu korrigieren und die Versteifung zu fördern. Wirbelsäulenverletzungen entstehen in der Regel durch Traumata oder Wirbelgleiten aufgrund degenerativer Bandscheibenerkrankungen. Faktoren wie die steigende Anzahl von Wirbelsäulenimplantationen und die zunehmende Häufigkeit von Traumata und Sportverletzungen treiben das Wachstum des Marktes für Wirbelsäulenimplantate an. Strenge regulatorische Vorgaben hemmen dieses Wachstum jedoch. Der 3D-Druck von Implantaten für chirurgische Eingriffe dürfte in den kommenden Jahren neue Trends auf dem Markt für Wirbelsäulenimplantate mit sich bringen.

Wachstumstreiber:

Zunehmende Häufigkeit von Traumata und Sportverletzungen

Traumatische Verletzungen, beispielsweise durch Unfälle und Sport, erfordern häufig Eingriffe an der Wirbelsäule, darunter den Einsatz von Implantaten zur Stabilisierung und Rekonstruktion. Die steigende Zahl traumatischer Wirbelsäulenverletzungen trägt zur Nachfrage nach Wirbelsäulenimplantaten bei. Laut Weltgesundheitsorganisation (WHO) sterben weltweit jährlich etwa 1,19 Millionen Menschen bei Verkehrsunfällen, und 20 bis 50 Millionen erleiden nicht-tödliche Verletzungen, von denen viele eine Behinderung davontragen. Schätzungen der Mayo Clinic zufolge verursachen Sportarten wie Flachwassertauchen, Basketball und Fußball etwa 10 % aller Rückenmarksverletzungen. Die WHO-Daten legen zudem nahe, dass jährlich weltweit 250.000 bis 500.000 Rückenmarksverletzungen registriert werden. Die meisten Rückenmarksverletzungen, darunter solche, die durch Autounfälle, Stürze oder Angriffe verursacht werden, sind jedoch vermeidbar. Menschen mit Rückenmarksverletzungen haben ein 2- bis 5-fach höheres Risiko, vorzeitig zu sterben, als Menschen ohne Rückenmarksverletzungen. In Ländern mit niedrigem und mittlerem Einkommen sind die Überlebensraten deutlich niedriger. Die steigende Zahl von Traumata und Sportverletzungen führt daher zu einer hohen Nachfrage nach chirurgischen Eingriffen und kurbelt somit das Wachstum des Marktes für Wirbelsäulenimplantate an.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für Wirbelsäulenimplantate: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Berichtssegmentierung und -umfang:

Die Marktanalyse für Wirbelsäulenimplantate wurde unter Berücksichtigung der folgenden Segmente durchgeführt: Produkt, Verfahren, Material und Endnutzer.

Nach Produktart ist der Markt in Wirbelsäulenimplantate mit und ohne Fusion unterteilt. Das Segment der Wirbelsäulenimplantate mit Fusion hielt 2023 den größten Marktanteil am gesamten Wirbelsäulenimplantatmarkt. Es wird erwartet, dass es im Prognosezeitraum eine höhere durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnen wird. Der Markt für Wirbelsäulenimplantate mit Fusion ist weiter unterteilt in thorakolumbale Implantate, zervikale Fixationssysteme und interkorporelle Fusionssysteme.

Der Markt ist nach Eingriffen in Foraminotomie, Laminektomie, Bandscheibenersatz, Wirbelsäulenversteifung und Diskektomie unterteilt. Das Segment der Laminektomie hielt 2023 den größten Marktanteil bei Wirbelsäulenimplantaten, und für die Wirbelsäulenversteifung wird im Prognosezeitraum das höchste durchschnittliche jährliche Wachstum erwartet.

Der Markt für Wirbelsäulenimplantate ist nach Material in Titan, Kohlenstofffaser und Edelstahl unterteilt. Das Segment Edelstahl hielt 2023 den größten Marktanteil und wird voraussichtlich im Prognosezeitraum die höchste durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnen.

Der Markt für Wirbelsäulenimplantate ist nach Endnutzer in Krankenhäuser, Diagnose- und Bildgebungszentren sowie Sonstige unterteilt. Das Segment der Krankenhäuser hielt 2023 den größten Marktanteil und wird voraussichtlich auch im Prognosezeitraum die höchste durchschnittliche jährliche Wachstumsrate (CAGR) verzeichnen.

Regionalanalyse:

Der geografische Geltungsbereich des Marktberichts für Wirbelsäulenimplantate umfasst Nordamerika, Europa, den asiatisch-pazifischen Raum, Süd- und Mittelamerika sowie den Nahen Osten und Afrika. Nordamerika hielt 2023 den größten Marktanteil. Die zunehmende Nutzung neuester Medizinprodukte, die hohe Prävalenz von Wirbelsäulenverletzungen und Produktinnovationen führender Akteure tragen zum Wachstum des Marktes für Wirbelsäulenimplantate in Nordamerika bei. Laut der Cleveland Clinic werden in den USA jährlich rund 18.000 neue Fälle von traumatischen Rückenmarksverletzungen gemeldet, was etwa 54 Fällen pro 1 Million Einwohner entspricht. Darüber hinaus führt altersbedingter Verschleiß zu einer Zunahme von Rückenschmerzen bei älteren Menschen in den USA und treibt somit die Nachfrage nach Wirbelsäulenoperationen und implantierbaren Geräten an. Laut dem National Health Service (NHS) lag die Lebenszeitprävalenz von Rückenschmerzen in den USA im Jahr 2022 bei 60–90 %, mit einer jährlichen Inzidenz von 5 %. Die Quelle gibt außerdem an, dass jährlich 14,3 % der neuen Patienten aufgrund von Rückenschmerzen einen Arzt aufsuchen und dass etwa 13 Millionen Menschen wegen chronischer Rückenschmerzen einen Arzt konsultieren. Die hohe Prävalenz von Rückenmarksverletzungen und Rückenschmerzen begünstigt somit das Wachstum des Marktes für Wirbelsäulenimplantate.

Markt für Wirbelsäulenimplantate: Regionale Einblicke

Die regionalen Trends und Einflussfaktoren auf den Markt für Wirbelsäulenimplantate im gesamten Prognosezeitraum wurden von den Analysten von The Insight Partners eingehend erläutert. Dieser Abschnitt behandelt außerdem die Marktsegmente und die geografische Verteilung des Marktes für Wirbelsäulenimplantate in Nordamerika, Europa, Asien-Pazifik, dem Nahen Osten und Afrika sowie Süd- und Mittelamerika.

Umfang des Marktberichts zu Wirbelsäulenimplantaten

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2024 | US$ XX Milliarden |

| Marktgröße bis 2031 | 19,34 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2025 - 2031) | 105,5 % |

| Historische Daten | 2021-2023 |

| Prognosezeitraum | 2025–2031 |

| Abgedeckte Segmente |

Nebenprodukt

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte der Akteure im Bereich Wirbelsäulenimplantate: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Wirbelsäulenimplantate wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

- Verschaffen Sie sich einen Überblick über die wichtigsten Akteure auf dem Markt für Wirbelsäulenimplantate.

Branchenentwicklungen und Zukunftschancen:

Nachfolgend sind einige strategische Entwicklungen führender Akteure auf dem Markt für Wirbelsäulenimplantate aufgeführt, die aus Unternehmens-Pressemitteilungen hervorgehen:

- Im Oktober 2023 schloss die Silony Medical International AG die Übernahme des globalen Fusionsgeschäfts von Centinel Spine ab. Mit dieser Akquisition gelingt Silony ein bedeutender Markteintritt in den USA und eine signifikante Stärkung ihres Angebots an eigenständigen Cage-Implantaten für den vorderen Bereich.

- Im September 2023 schloss Globus Medical Inc. die Fusion mit NuVasive Inc. ab. Das fusionierte Unternehmen bietet Chirurgen und Patienten eine der umfassendsten Lösungen für muskuloskelettale Eingriffe und ermöglicht technologische Fortschritte entlang der gesamten Behandlungskette.

- Im November 2022 gab NuVasive Inc. die Markteinführung des NuVasive Tube System (NTS) und von Excavation Micro bekannt, einer revolutionären Technologie für minimalinvasive Chirurgie (MIS), die Komplettlösungen für die transforaminale lumbale interkorporelle Fusion (TLIF) und Dekompression bietet. Mit den Erweiterungen des NuVasive P360-Portfolios verbesserte das Unternehmen seine Kompetenzen im Bereich Zugangs- und Instrumentierungstechnologie.

- Im August 2022 gab Nexus Spine die vollständige Markteinführung seines PressON-Systems zur posterioren lumbalen Fixierung bekannt. Die PressON-Stäbe werden auf Pedikelschrauben anstatt auf Stellschrauben aufgepresst. Diese einzigartige, biomechanisch stabilere Konstruktion ist etwa ein Viertel so groß wie herkömmliche Systeme. Die Stäbe lassen sich schneller implantieren, verhindern das Lockern der Stellschrauben und ermöglichen die intraoperative Montage für den Patienten. Mit der vollständigen Markteinführung konnte das Unternehmen sein Portfolio an flexiblen, mechanismusbasierten Implantaten erweitern. Dieses umfasst unter anderem eine Reihe von Tranquil-Titan-Interbody-Fusionsimplantaten, die nach einer umfassenden Validierungsphase mit Optimierungen und Systemverbesserungen angeboten werden.

- Im Oktober 2021 brachte NuVasive Inc. das Cohere TLIF-O-Implantat auf den Markt. Mit der Aufnahme des Cohere TLIF-O-Implantats in sein Portfolio im Bereich der fortgeschrittenen Materialwissenschaften (AMS) ist NuVasive nun das einzige Unternehmen, das sowohl poröse PEEK- als auch poröse Titanimplantate für die dorsale Wirbelsäulenchirurgie anbietet.

Wettbewerbsumfeld und Schlüsselunternehmen:

Zu den führenden Unternehmen, die im Marktbericht für Wirbelsäulenimplantate vorgestellt werden, gehören Stryker Corporation, Johnson & Johnson, Globus Medical Inc., ZimVie Inc., Camber Spine Technologies LLC, Spineart SA, Medtronic plc, Orthofix US LLC, ATEC Spine Inc. und B. Braun SE. Diese Unternehmen konzentrieren sich auf die Entwicklung neuer Technologien, die Verbesserung bestehender Produkte und den Ausbau ihrer geografischen Präsenz, um der weltweit steigenden Kundennachfrage gerecht zu werden.

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends