Informe de mercado de artículos para el hogar 2030 por segmentos, geografía, dinámica, desarrollos recientes e ideas estratégicas

Tamaño y pronósticos del mercado de artículos para el hogar (2020-2030), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por tipo de producto (utensilios de cocina y repostería, vajilla, electrodomésticos, artículos de baño y otros) y canal de distribución (supermercados e hipermercados, tiendas especializadas, comercio minorista en línea y otros).

- Estado : Publicada

- Código de informe : TIPRE00030119

- Categoría : Bienes de consumo

- Número de páginas : 150

- Formatos de informe disponibles :

- Fecha de última actualización : June 12, 2024

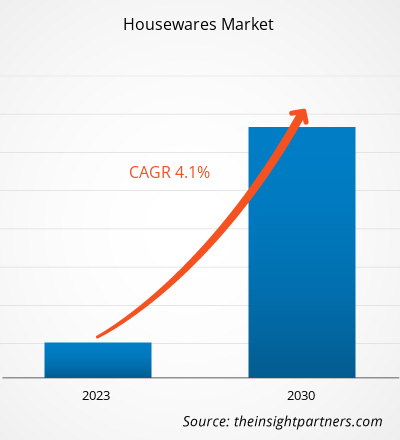

[Informe de investigación] El tamaño del mercado de artículos para el hogar se valoró en US$ 321,40 mil millones en 2022 y se espera que alcance los US$ 442,51 mil millones para 2030; se estima que registrará una CAGR del 4,1% de 2022 a 2030.

Perspectivas del mercado y opinión de analistas:

Los artículos para el hogar son productos y artículos que se utilizan en el hogar para cocinar, hornear y organizar el hogar, entre otros fines. El mercado de artículos para el hogar ha estado creciendo de manera constante debido a factores como los cambios en los estilos de vida y el mayor tiempo que se pasa en casa, que han desencadenado la demanda de artículos para el hogar funcionales y estéticamente agradables. Durante la pandemia de COVID-19, las personas pasaron más tiempo en casa e invirtieron en mejorar sus espacios de vida. Además, el auge del comercio electrónico y las plataformas de compras en línea ha facilitado que los consumidores accedan y compren una amplia gama de productos para el hogar desde sus hogares. Estos factores, junto con los diseños innovadores y las opciones sostenibles que ofrecen las empresas de artículos para el hogar, favorecen la expansión del mercado de artículos para el hogar.

Factores impulsores del crecimiento y desafíos:

Los cambios dinámicos en el estilo de vida y el aumento de las familias con dos ingresos llevaron a un aumento de los ingresos disponibles y a una mejora en el nivel de vida de los hogares. Con el aumento de los ingresos disponibles, los consumidores gastan cantidades significativas en artículos para el hogar y otros electrodomésticos que contribuyen a una vida más cómoda. A menudo están dispuestos a comprar productos nuevos debido a sus estilos únicos, que apelan a su individualidad, lo que resulta en una mayor frecuencia de compra. Además, un número creciente de hogares unipersonales desencadena la necesidad de modificaciones en el hogar, lo que impulsa la demanda de artículos para el hogar, como electrodomésticos de cocina, utensilios de cocina, vajilla y artículos básicos para el baño.

Además, el aumento de la urbanización ha impulsado la demanda de unidades residenciales y, en última instancia, de productos para el hogar. Según la Oficina del Censo de EE. UU. y el Departamento de Vivienda y Desarrollo Urbano de EE. UU., EE. UU. completó la construcción de ~1,3 millones de unidades de vivienda en 2021, mientras que la construcción de ~1,7 millones de unidades de vivienda estaba en curso. De manera similar, la creciente urbanización en los países europeos ha creado una enorme demanda de viviendas residenciales. Según la Comisión Europea, los permisos de construcción residencial aumentaron un 42,3% de 2015 a 2021 en la Unión Europea. En 2021, Francia, Alemania y Polonia representaron la mayor parte del inicio de la construcción residencial en Europa. Por lo tanto, la creciente construcción de unidades de vivienda en varios países impulsa aún más la demanda de artículos para el hogar. Por lo tanto, la creciente compra de artículos para el hogar junto con el creciente número de hogares impulsa el crecimiento del mercado de artículos para el hogar.

Sin embargo, el mercado de artículos para el hogar está muy fragmentado y desorganizado debido a que en los países en desarrollo operan muchas pequeñas empresas privadas y vendedores ambulantes que no han sido explotados. Según un artículo publicado en Business Standards, en 2020, el 80% del mercado de artículos de cocina no estaba organizado en la India. Las pequeñas empresas locales utilizan materias primas de baja calidad para fabricar artículos para el hogar, como utensilios de cocina, utensilios para hornear, accesorios de baño y vajillas. El uso de materias primas de baja calidad da como resultado productos finales de mala calidad que son propensos a dañarse. Además, los fabricantes ofrecen estos productos a bajo costo; por lo tanto, la mayoría de los consumidores compran estos productos debido a su asequibilidad y fácil disponibilidad. Este factor da como resultado la reducción de la base de clientes de los principales fabricantes de artículos para el hogar.

Además, con mayor frecuencia, los fabricantes locales en el mercado de artículos para el hogar no organizado no cumplen con las normas regulatorias, lo que puede generar problemas de calidad y obstaculizar la percepción de los consumidores hacia los artículos para el hogar. Además, la disponibilidad de productos falsificados puede obstaculizar la imagen de marca de los actores clave. Por lo tanto, la falta de uniformidad en las operaciones y regulaciones obstaculiza el crecimiento del mercado de artículos para el hogar.

Personalice este informe según sus necesidades

Obtendrá personalización en cualquier informe, sin cargo, incluidas partes de este informe o análisis a nivel de país, paquete de datos de Excel, así como también grandes ofertas y descuentos para empresas emergentes y universidades.

Mercado de artículos para el hogar: perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Segmentación y alcance del informe:

El mercado mundial de artículos para el hogar está segmentado en función del tipo de producto, el canal de distribución y la geografía. Según el tipo de producto, el mercado se clasifica en utensilios de cocina y para hornear, vajillas, electrodomésticos de cocina, artículos básicos para el baño y otros. Por canal de distribución, el mercado se clasifica en supermercados e hipermercados, tiendas especializadas, venta minorista en línea y otros. Por geografía, el mercado mundial de artículos para el hogar está ampliamente segmentado en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

Análisis segmental:

Según el tipo de producto, el mercado de artículos para el hogar se clasifica en utensilios de cocina y para hornear, vajilla, electrodomésticos de cocina, artículos básicos de baño y otros. Se espera que el segmento de vajilla registre la CAGR más alta durante 2022-2030. El segmento de vajilla incluye productos como vajilla, cubertería, cristalería y vajilla. El aumento de la demanda de vajilla en el mercado de artículos para el hogar se puede atribuir a los hábitos gastronómicos transformados durante la pandemia de COVID-19. Con más gente cenando en casa, la gente ha empezado a centrarse en la vajilla estética y funcional, ya que mejora las experiencias gastronómicas en el hogar. Desde las comidas diarias hasta las reuniones especiales, los consumidores buscan juegos de vajilla que mejoren su experiencia gastronómica. Además, la creciente apreciación por los diseños únicos y artesanales juega un papel importante a la hora de impulsar la demanda de vajilla. Los consumidores se sienten cada vez más atraídos por las piezas de vajilla hechas a mano y de inspiración artística que aportan un toque de individualidad y personalidad a sus entornos de comedor. Por tanto, un cambio hacia opciones de vajilla más personalizadas y visualmente llamativas ha contribuido al progreso del mercado de artículos para el hogar para el segmento de vajilla. Vivo - Villeroy & Boch Group, Corelle, Pyrex, Luminarc y Schott Zwiesel son algunos de los actores destacados que operan en el mercado de vajillas.

Análisis regional:

El mercado de artículos para el hogar está segmentado en cinco regiones clave: América del Norte, Europa, Asia Pacífico, América del Sur y Central, y Oriente Medio y África. Asia Pacífico dominó el mercado mundial de artículos para el hogar en 2022, ya que el mercado en esta región se valoró en 120.630 millones de dólares en ese año. Europa es el segundo contribuyente más importante, con más del 23% de la participación del mercado mundial. Se espera que Asia Pacífico registre una CAGR considerable de más del 5% durante 2022-2030. La creciente urbanización y los ingresos disponibles de la población de clase media son un factor primordial que impulsa la demanda de artículos para el hogar modernos y prácticos, incluidos electrodomésticos de cocina avanzados y vajillas elegantes.

Perspectivas regionales del mercado de artículos para el hogar

Los analistas de Insight Partners explicaron en detalle las tendencias y los factores regionales que influyen en el mercado de artículos para el hogar durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de artículos para el hogar en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

- Obtenga datos regionales específicos para el mercado de artículos para el hogar

Alcance del informe del mercado de artículos para el hogar

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2022 | US$ 321.4 mil millones |

| Tamaño del mercado en 2030 | US$ 442,51 mil millones |

| CAGR global (2022-2030) | 4,1% |

| Datos históricos | 2020-2021 |

| Período de pronóstico | 2023-2030 |

| Segmentos cubiertos |

Por tipo de producto

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado: comprensión de su impacto en la dinámica empresarial

El mercado de artículos para el hogar está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor conciencia de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían sus ofertas, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

La densidad de actores del mercado se refiere a la distribución de las empresas o firmas que operan dentro de un mercado o industria en particular. Indica cuántos competidores (actores del mercado) están presentes en un espacio de mercado determinado en relación con su tamaño o valor total de mercado.

Las principales empresas que operan en el mercado de artículos para el hogar son:

- Bradshaw Home Inc

- La empresa Denby Pottery Co. Ltd.

- Compañía HF Coors Inc.

- Inter Ikea Holding BV

- Compañía manufacturera Hutzler Inc.

Descargo de responsabilidad : Las empresas enumeradas anteriormente no están clasificadas en ningún orden particular.

- Obtenga una descripción general de los principales actores clave del mercado de artículos para el hogar

Impacto de la pandemia de COVID-19:

La pandemia de COVID-19 inicialmente obstaculizó el mercado mundial de artículos para el hogar debido al cierre de unidades de fabricación, la escasez de mano de obra, la interrupción de las cadenas de suministro y la inestabilidad financiera. La interrupción de las operaciones en varias industrias debido a la desaceleración económica causada por el brote de COVID-19 restringió el suministro de artículos para el hogar. Además, varias tiendas cerraron, lo que limitó las ventas de artículos para el hogar. Sin embargo, las empresas comenzaron a ganar terreno a medida que se revocaron las limitaciones impuestas anteriormente en varios países en 2021. Además, la implementación de campañas de vacunación contra COVID-19 por parte de los gobiernos de diferentes países alivió la situación, lo que provocó un aumento de las actividades comerciales en todo el mundo. Varios mercados, incluido el mercado de artículos para el hogar, informaron un crecimiento después de la flexibilización de los cierres y las restricciones de movimiento.

Panorama competitivo y empresas clave:

Bradshaw Home Inc, Denby Pottery, HF Coors Co Inc, Inter Ikea Holding Bv, Hutzler Manufacturing Co Inc, TTK Prestige Ltd, Newell Brands Inc, BSH Hausgerate GmbH, Kohler Co y Haier US Appliance Solutions Inc se encuentran entre los actores destacados que operan en el mercado global de artículos para el hogar.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias