Estrategias de mercado de Implantes espinales, principales actores, oportunidades de crecimiento, análisis y pronóstico para 2031

Tamaño y pronóstico del mercado de implantes espinales (2021-2031), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por producto (implantes espinales con y sin fusión), procedimiento (foraminotomía, laminectomía, reemplazo de disco espinal, fusión espinal y discectomía), material (titanio, fibra de carbono y acero inoxidable), usuario final (hospitales, clínicas especializadas y unidades de cirugía ambulatoria) y geografía (Norteamérica, Europa, Asia Pacífico, Sudamérica y Centroamérica, Oriente Medio y África).

- Estado : Datos publicados

- Código de informe : TIPHE100000993

- Categoría : Ciencias de la vida

- Número de páginas : 150

- Formatos de informe disponibles :

- Fecha de última actualización : May 30, 2024

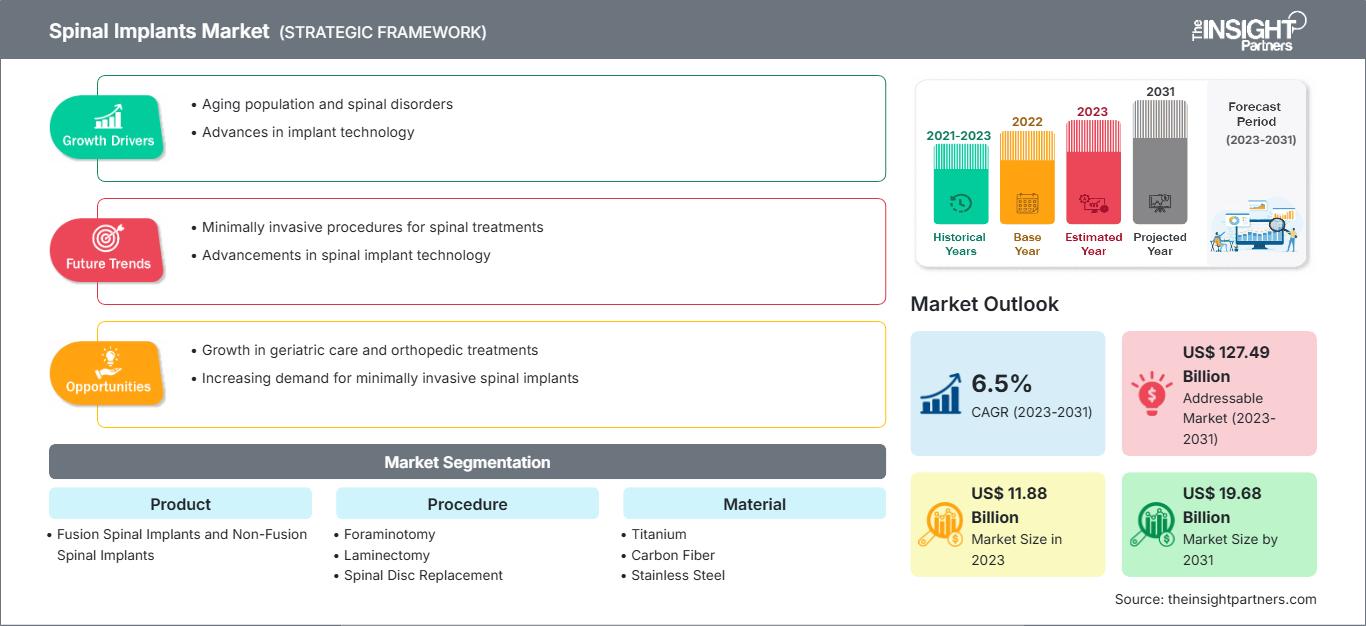

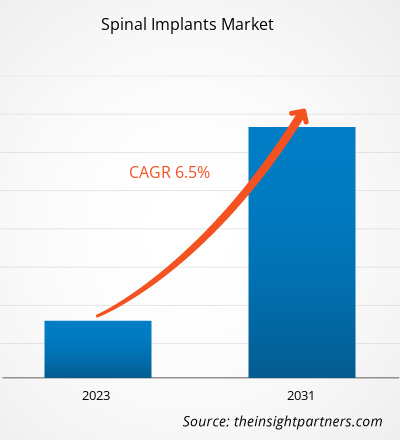

Se espera que el tamaño del mercado de implantes espinales alcance los US$ 19.34 mil millones para 2031. Se anticipa que el mercado registre una CAGR del 105,5% durante 2025-2031.

Perspectivas del mercado y opinión de los analistas:

Los implantes espinales son dispositivos médicos que se utilizan en procedimientos de estabilización de la columna vertebral para fortalecerla, tratar deformidades y facilitar la fusión. Las lesiones de columna generalmente son causadas por traumatismos o deslizamientos vertebrales debido a la degeneración de los discos intervertebrales. Factores como el creciente número de procedimientos de implantes espinales y la creciente incidencia de traumatismos y lesiones deportivas impulsan el crecimiento del mercado de implantes espinales. Sin embargo, las estrictas regulaciones frenan el crecimiento del mercado. Se espera que la impresión 3D de implantes para procedimientos quirúrgicos impulse nuevas tendencias en el mercado de implantes espinales en los próximos años.

Factores impulsores del crecimiento:

Aumento de la incidencia de traumatismos y lesiones relacionadas con el deporte

Las lesiones traumáticas, incluidas las causadas por accidentes y actividades deportivas, a menudo requieren intervenciones de columna vertebral, incluyendo el uso de implantes para estabilización y reconstrucción. La creciente incidencia de lesiones traumáticas de columna vertebral contribuye a la demanda de implantes espinales. Según la Organización Mundial de la Salud (OMS), a nivel mundial, aproximadamente 1,19 millones de personas mueren cada año en accidentes de tránsito, y entre 20 y 50 millones sufren lesiones no mortales, muchas de las cuales sufren discapacidad. De igual manera, según estimaciones de la Clínica Mayo, deportes y actividades atléticas como el buceo en aguas poco profundas, el baloncesto y el fútbol causan aproximadamente el 10 % de las lesiones de médula espinal. Los datos de la OMS también sugieren que anualmente se registran entre 250 000 y 500 000 lesiones de médula espinal (LME) en todo el mundo. Sin embargo, la mayoría de las lesiones de médula espinal, incluidas las causadas por accidentes automovilísticos, caídas o agresiones, son prevenibles. Las personas que sufren LME tienen entre 2 y 5 veces más probabilidades de morir prematuramente que quienes no las padecen, y los países de ingresos bajos y medios registran tasas de supervivencia notablemente más bajas. Por lo tanto, la creciente incidencia de traumatismos y lesiones relacionadas con el deporte genera una gran demanda de intervenciones quirúrgicas, lo que a su vez impulsa el crecimiento del mercado de implantes espinales.

Personalice este informe según sus necesidades

Obtenga PERSONALIZACIÓN GRATUITAMercado de implantes espinales: Perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Segmentación y alcance del informe:

El análisis del mercado de implantes espinales se ha realizado considerando los siguientes segmentos: producto, procedimiento, material y usuario final.

Por producto, el mercado se divide en implantes espinales de fusión e implantes espinales sin fusión. El segmento de implantes espinales de fusión tuvo la mayor participación de mercado en 2023. Se prevé una mayor tasa de crecimiento anual compuesta (TCAC) durante el período de pronóstico. El mercado de implantes espinales de fusión se subdivide en dispositivos toracolumbares, dispositivos de fijación cervical y dispositivos de fusión intersomática.

El mercado, por procedimiento, se clasifica en foraminotomía, laminectomía, reemplazo de disco intervertebral, fusión espinal y discectomía. El segmento de laminectomía tuvo la mayor participación de mercado en implantes espinales en 2023, y se estima que la fusión espinal registrará la mayor tasa de crecimiento anual compuesta (TCAC) durante el período de pronóstico.

El mercado de implantes espinales, por material, se segmenta en titanio, fibra de carbono y acero inoxidable. El segmento de acero inoxidable tuvo la mayor participación de mercado en 2023; se prevé que registre la mayor tasa de crecimiento anual compuesta (TCAC) durante el período de pronóstico.

El mercado de implantes espinales, por usuario final, se clasifica en hospitales, centros de diagnóstico por imagen, entre otros. El segmento hospitalario tuvo la mayor participación de mercado en 2023. Además, se espera que registre la tasa de crecimiento anual compuesta (TCAC) más alta durante el período de pronóstico.

Análisis regional:

El alcance geográfico del informe de mercado de implantes espinales incluye América del Norte, Europa, Asia Pacífico, América del Sur y Central, y Oriente Medio y África. En 2023, América del Norte tenía la mayor cuota de mercado. La creciente adopción de los dispositivos médicos más modernos, la alta prevalencia de lesiones espinales y las innovaciones de productos por parte de actores clave contribuyen a la expansión del tamaño del mercado de implantes espinales en América del Norte. Según la Clínica Cleaveland, EE. UU. reporta aproximadamente 18.000 nuevos casos de lesiones traumáticas de la médula espinal cada año, lo que equivale a aproximadamente 54 casos por millón de habitantes. Además, el desgaste relacionado con la edad desencadena la prevalencia del dolor lumbar (LBP) entre la población geriátrica en EE. UU., lo que a su vez impulsa la demanda de cirugías espinales y dispositivos implantables. Según el Servicio Nacional de Salud, en 2022, la incidencia de LBP a lo largo de la vida en EE. UU. se reportó entre el 60% y el 90%, con una incidencia anual del 5%. La fuente también indica que el 14,3 % de los nuevos pacientes acuden al médico cada año debido al dolor lumbar, y aproximadamente 13 millones de personas acuden al médico debido al dolor lumbar crónico. Por lo tanto, la alta prevalencia de lesiones medulares y dolor lumbar favorece el avance del mercado de implantes espinales.

Perspectivas regionales del mercado de implantes espinales

Los analistas de The Insight Partners han explicado detalladamente las tendencias regionales y los factores que influyen en el mercado de implantes espinales durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de implantes espinales en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

Alcance del informe de mercado sobre implantes espinales

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2024 | XX mil millones de dólares estadounidenses |

| Tamaño del mercado en 2031 | US$ 19.34 mil millones |

| CAGR global (2025-2031) | 105,5% |

| Datos históricos | 2021-2023 |

| Período de pronóstico | 2025-2031 |

| Segmentos cubiertos |

Por producto

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de implantes espinales: comprensión de su impacto en la dinámica empresarial

El mercado de implantes espinales está creciendo rápidamente, impulsado por la creciente demanda del usuario final debido a factores como la evolución de las preferencias del consumidor, los avances tecnológicos y un mayor conocimiento de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades del consumidor y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

- Obtenga una descripción general de los principales actores clave del mercado de implantes espinales

Desarrollos de la industria y oportunidades futuras:

A continuación se enumeran algunos desarrollos estratégicos de los principales actores que operan en el mercado de implantes espinales, según comunicados de prensa de la empresa:

- En octubre de 2023, Silony Medical International AG completó la adquisición del negocio global de fusión de Centinel Spine. Con esta adquisición, Silony logra una importante entrada en el mercado estadounidense y refuerza significativamente su oferta de jaulas independientes anteriores.

- En septiembre de 2023, Globus Medical Inc. completó su fusión con NuVasive Inc. La empresa combinada ofrece a los cirujanos y pacientes una de las soluciones de procedimientos musculoesqueléticos más completas, lo que permite avances tecnológicos en todo el proceso de atención.

- En noviembre de 2022, NuVasive Inc. anunció el lanzamiento comercial del Sistema de Tubos NuVasive (NTS) y Excavation Micro, una revolucionaria tecnología de cirugía mínimamente invasiva (CMI) que ofrece soluciones completas para la fusión intercorporal lumbar transforaminal (TLIF) y la descompresión. Con las nuevas incorporaciones al portafolio NuVasive P360, la compañía mejoró sus capacidades tecnológicas de acceso e instrumentación.

- En agosto de 2022, Nexus Spine anunció el lanzamiento comercial completo de su sistema de fijación lumbar posterior PressON. Las barras PressON están diseñadas para presionar sobre tornillos pediculares en lugar de tornillos de fijación. Este diseño único, biomecánicamente más resistente, mide aproximadamente una cuarta parte del tamaño de los sistemas estándar. Las barras se implantan más rápido, evitan el aflojamiento de los tornillos de fijación y permiten el montaje intraoperatorio de las barras en los pacientes. El lanzamiento completo al mercado permitió a la compañía ampliar su cartera de productos basados en mecanismos compatibles, que incluye una gama de dispositivos flexibles de fusión intersomática de titanio Tranquil, que se ofrecen tras un exhaustivo período de validación de mejoras y mejoras del sistema.

- En octubre de 2021, NuVasive Inc. lanzó el implante Cohere TLIF-O. Con la incorporación del implante Cohere TLIF-O a su portafolio de Ciencia de Materiales Avanzados (AMS), NuVasive se ha convertido en la única empresa que ofrece implantes de PEEK poroso y titanio poroso para cirugía de columna posterior.

Panorama competitivo y empresas clave:

Stryker Corporation, Johnson & Johnson, Globus Medical Inc, ZimVie Inc, Camber Spine Technologies LLC, Spineart SA, Medtronic plc, Orthofix US LLC, ATEC Spine Inc y B. Braun SE se encuentran entre las empresas destacadas que aparecen en el informe del mercado de implantes espinales. Estas empresas se centran en el desarrollo de nuevas tecnologías, la modernización de productos existentes y la expansión de su presencia geográfica para satisfacer la creciente demanda mundial de los consumidores.

Mrinal es una experimentada analista de investigación con más de 8 años de experiencia en inteligencia de mercado y consultoría en ciencias de la vida. Con una mentalidad estratégica y un firme compromiso con la excelencia, ha desarrollado una amplia experiencia en pronósticos farmacéuticos, evaluación de oportunidades de mercado y desarrollo de indicadores de referencia para la industria. Su trabajo se centra en brindar información práctica que permita a los clientes tomar decisiones estratégicas informadas.

La principal fortaleza de Mrinal reside en convertir conjuntos de datos cuantitativos complejos en inteligencia de negocios significativa. Su perspicacia analítica es fundamental para definir estrategias de salida al mercado (GTM) y descubrir oportunidades de crecimiento en los sectores farmacéutico y de dispositivos médicos. Como consultora de confianza, se centra constantemente en optimizar los procesos de flujo de trabajo y establecer las mejores prácticas, impulsando así la innovación y la eficiencia operativa para sus clientes.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias