Strategie di mercato degli impianti spinali, principali attori, opportunità di crescita, analisi e previsioni entro il 2031

Dimensioni e previsioni del mercato degli impianti spinali (2021-2031), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per prodotto (impianti spinali con fusione e impianti spinali senza fusione), procedura (foraminotomia, laminectomia, sostituzione del disco spinale, fusione spinale e discectomia), materiale (titanio, fibra di carbonio e acciaio inossidabile), utente finale (ospedali, cliniche specializzate e unità chirurgiche ambulatoriali) e area geografica (Nord America, Europa, Asia Pacifico, Sud e Centro America, Medio Oriente e Africa).

- Stato : Dati rilasciati

- Codice del report : TIPHE100000993

- Categoria : Scienze della vita

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : May 30, 2024

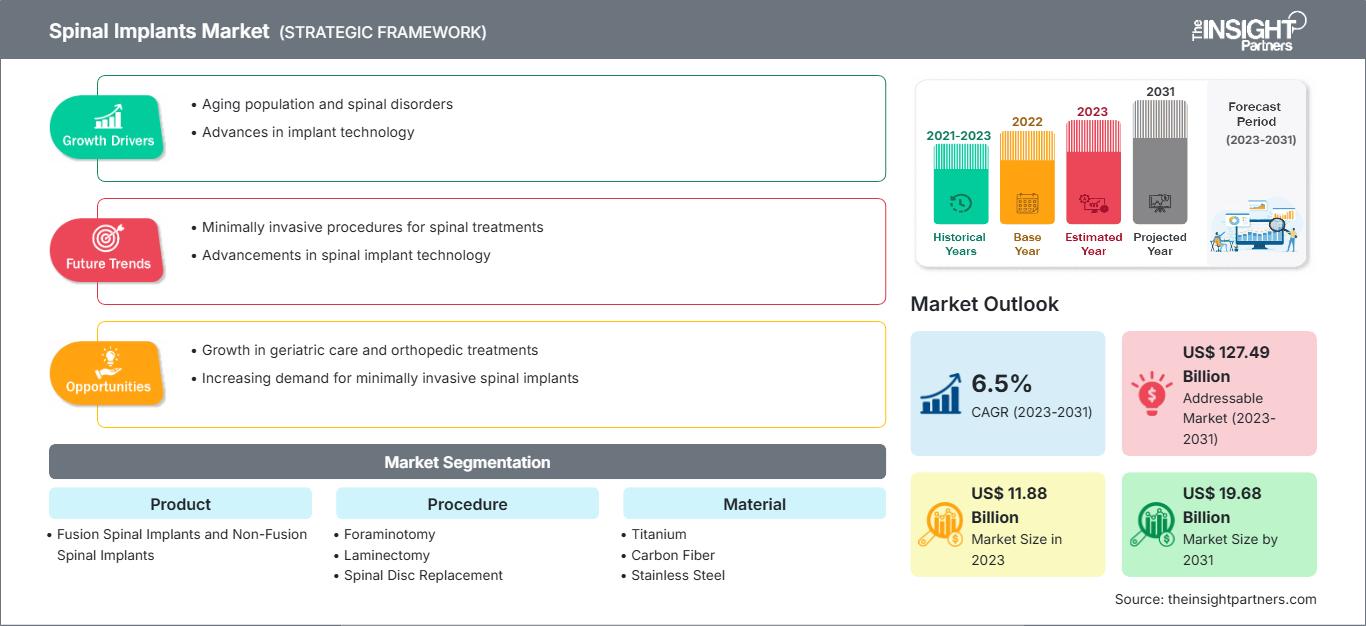

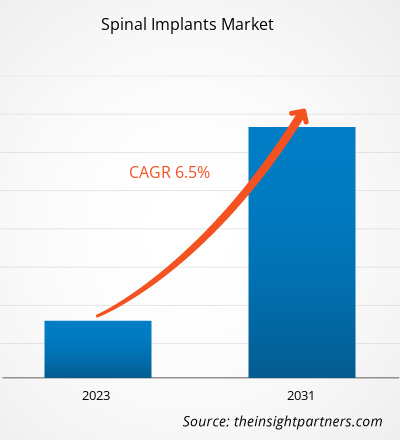

Si prevede che il mercato degli impianti spinali raggiungerà i 19,34 miliardi di dollari entro il 2031. Si prevede che il mercato registrerà un CAGR del 105,5% nel periodo 2025-2031.

Approfondimenti di mercato e opinioni degli analisti:

Gli impianti spinali sono dispositivi medici utilizzati nelle procedure di stabilizzazione della colonna vertebrale per rafforzarla, trattare le deformità e facilitarne la fusione. Le lesioni spinali sono generalmente causate da traumi o da scivolamenti delle vertebre dovuti a degenerazione dei dischi intervertebrali. Fattori come il crescente numero di procedure di impianto spinale e la crescente incidenza di traumi e infortuni sportivi stimolano la crescita del mercato degli impianti spinali. Tuttavia, normative severe ne ostacolano la crescita. Si prevede che la stampa 3D di impianti per interventi chirurgici porterà nuove tendenze nel mercato degli impianti spinali nei prossimi anni.

Fattori di crescita:

Aumento dell'incidenza di traumi e infortuni sportivi

Le lesioni traumatiche, comprese quelle derivanti da incidenti e attività sportive, richiedono spesso interventi spinali, incluso l'uso di impianti per la stabilizzazione e la ricostruzione. La crescente incidenza di lesioni spinali traumatiche contribuisce alla domanda di impianti spinali. Secondo l'Organizzazione Mondiale della Sanità (OMS), a livello globale, circa 1,19 milioni di persone muoiono ogni anno in incidenti stradali e 20-50 milioni di persone subiscono lesioni non mortali, molte delle quali con disabilità. Analogamente, secondo le stime della Mayo Clinic, sport e attività atletiche come immersioni in acque basse, basket e football americano causano circa il 10% delle lesioni del midollo spinale. I dati dell'OMS suggeriscono inoltre che ogni anno in tutto il mondo si registrano tra 250.000 e 500.000 lesioni del midollo spinale (SCI). Tuttavia, la maggior parte delle lesioni del midollo spinale, comprese quelle causate da incidenti stradali, cadute o aggressioni, sono prevenibili. Le persone affette da lesione spinale hanno una probabilità di morire prematuramente da 2 a 5 volte maggiore rispetto a chi non ne è affetto, con tassi di sopravvivenza notevolmente inferiori nei paesi a basso e medio reddito. Pertanto, la crescente incidenza di traumi e infortuni sportivi si traduce in un'elevata domanda di interventi chirurgici, con conseguente incremento della crescita del mercato degli impianti spinali.

Personalizza questo report in base alle tue esigenze

Ottieni la PERSONALIZZAZIONE GRATUITAMercato degli impianti spinali: approfondimenti strategici

-

Scopri le principali tendenze di mercato di questo rapporto.Questo campione GRATUITO includerà analisi dei dati, che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Segmentazione e ambito del report:

L'analisi del mercato degli impianti spinali è stata condotta prendendo in considerazione i seguenti segmenti: prodotto, procedura, materiale e utente finale.

Per prodotto, il mercato è suddiviso in impianti spinali a fusione e impianti spinali senza fusione. Il segmento degli impianti spinali a fusione ha detenuto una quota di mercato maggiore nel 2023. Si prevede che registrerà un CAGR più elevato durante il periodo di previsione. Il mercato degli impianti spinali a fusione è suddiviso in dispositivi toracolombari, dispositivi di fissaggio cervicale e dispositivi di fusione intersomatica.

Il mercato, in base alla procedura, è suddiviso in foraminotomia, laminectomia, sostituzione del disco spinale, fusione spinale e discectomia. Il segmento della laminectomia ha detenuto la quota di mercato più ampia degli impianti spinali nel 2023 e si stima inoltre che la fusione spinale registrerà il CAGR più elevato durante il periodo di previsione.

Il mercato degli impianti spinali, in base al materiale, è segmentato in titanio, fibra di carbonio e acciaio inossidabile. Il segmento dell'acciaio inossidabile ha detenuto la quota di mercato maggiore nel 2023; si prevede che registrerà il CAGR più elevato durante il periodo di previsione.

Il mercato degli impianti spinali, per utente finale, è suddiviso in ospedali, centri di diagnostica per immagini e altri settori. Il segmento ospedaliero ha detenuto la quota di mercato maggiore nel 2023. Si prevede inoltre che registrerà il CAGR più elevato durante il periodo di previsione.

Analisi regionale:

L'ambito geografico del rapporto sul mercato degli impianti spinali include Nord America, Europa, Asia-Pacifico, Sud e Centro America, Medio Oriente e Africa. Nel 2023, il Nord America deteneva la quota di mercato maggiore. La crescente adozione dei dispositivi medici più recenti, l'elevata prevalenza di lesioni spinali e le innovazioni di prodotto da parte dei principali attori contribuiscono all'espansione del mercato degli impianti spinali in Nord America. Secondo la Cleaveland Clinic, gli Stati Uniti segnalano circa 18.000 nuovi casi di lesioni traumatiche del midollo spinale ogni anno, equivalenti a circa 54 casi ogni milione di abitanti. Inoltre, l'usura legata all'età innesca la prevalenza del dolore lombare (LBP) tra la popolazione geriatrica negli Stati Uniti, alimentando a sua volta la domanda di interventi chirurgici spinali e dispositivi impiantabili. Secondo il Servizio Sanitario Nazionale, nel 2022, l'incidenza della LBP nel corso della vita negli Stati Uniti dovrebbe essere del 60-90%, con un'incidenza annua del 5%. La fonte afferma inoltre che il 14,3% dei nuovi pazienti si rivolge al medico ogni anno a causa della lombalgia, e circa 13 milioni di persone si rivolgono al medico a causa della lombalgia cronica. Pertanto, l'elevata prevalenza di lesioni del midollo spinale e lombalgia favorisce il progresso del mercato degli impianti spinali.

Approfondimenti regionali sul mercato degli impianti spinali

Le tendenze e i fattori regionali che hanno influenzato il mercato degli impianti spinali durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione illustra anche i segmenti e la distribuzione geografica del mercato degli impianti spinali in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America Meridionale e Centrale.

Ambito del rapporto di mercato sugli impianti spinali

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2024 | XX miliardi di dollari USA |

| Dimensioni del mercato entro il 2031 | 19,34 miliardi di dollari USA |

| CAGR globale (2025 - 2031) | 105,5% |

| Dati storici | 2021-2023 |

| Periodo di previsione | 2025-2031 |

| Segmenti coperti |

Per prodotto

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato degli impianti spinali: comprendere il suo impatto sulle dinamiche aziendali

Il mercato degli impianti spinali è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni una panoramica dei principali attori del mercato degli impianti spinali

Sviluppi del settore e opportunità future:

Di seguito sono elencati alcuni sviluppi strategici dei principali attori operanti nel mercato degli impianti spinali, come riportato nei comunicati stampa aziendali:

- Nell'ottobre 2023, Silony Medical International AG ha completato l'acquisizione della divisione Global Fusion di Centinel Spine. Grazie a questa acquisizione, Silony entra in modo significativo nel mercato statunitense e rafforza significativamente la sua offerta di gabbie anteriori autonome.

- Nel settembre 2023, Globus Medical Inc ha completato la fusione con NuVasive Inc. La nuova società offre a chirurghi e pazienti una delle soluzioni procedurali muscoloscheletriche più complete, consentendo progressi tecnologici lungo tutto il continuum di cura.

- Nel novembre 2022, NuVasive Inc. ha annunciato il lancio commerciale del NuVasive Tube System (NTS) e di Excavation Micro, una rivoluzionaria tecnologia di chirurgia mininvasiva (MIS) che offre soluzioni complete per la fusione intersomatica lombare transforaminale (TLIF) e la decompressione. Con l'aggiunta del portfolio NuVasive P360, l'azienda ha potenziato le sue competenze in ambito di tecnologie di accesso e strumentazione.

- Nell'agosto 2022, Nexus Spine ha annunciato il lancio commerciale completo del suo sistema di fissazione lombare posteriore PressON. Le barre PressON sono progettate per premere sulle viti peduncolari anziché sulle viti di fissaggio. Questo esclusivo design biomeccanicamente più resistente misura circa un quarto delle dimensioni dei sistemi standard. Le barre vengono impiantate più rapidamente, evitano il rischio di allentamento delle viti di fissaggio e consentono l'assemblaggio intraoperatorio delle barre per i pazienti. Il lancio completo sul mercato ha permesso all'azienda di ampliare il suo portafoglio basato su meccanismi conformi, che include una gamma di dispositivi flessibili per fusione intersomatica in titanio Tranquil, offerti dopo un esauriente periodo di validazione di perfezionamenti e miglioramenti del sistema.

- Nell'ottobre 2021, NuVasive Inc. ha lanciato l'impianto Cohere TLIF-O. Con l'aggiunta dell'impianto Cohere TLIF-O al suo portafoglio Advanced Materials Science (AMS), NuVasive è diventata l'unica azienda a fornire sia impianti in PEEK poroso che in titanio poroso per la chirurgia spinale posteriore.

Panorama competitivo e aziende chiave:

Stryker Corporation, Johnson & Johnson, Globus Medical Inc, ZimVie Inc, Camber Spine Technologies LLC, Spineart SA, Medtronic plc, Orthofix US LLC, ATEC Spine Inc e B. Braun SE sono tra le aziende di spicco descritte nel rapporto di mercato degli impianti spinali. Queste aziende si concentrano sullo sviluppo di nuove tecnologie, sull'aggiornamento dei prodotti esistenti e sull'espansione della loro presenza geografica per soddisfare la crescente domanda dei consumatori in tutto il mondo.

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative