Tamaño del mercado de atención oftalmológica, tendencias y crecimiento hasta 2034

Tamaño y pronósticos del mercado de cuidado de la visión (2021-2034), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por tipo de producto (gafas, lentes de contacto, lentes intraoculares y otros), canal de distribución (tiendas minoristas, comercio electrónico, clínicas y hospitales) y geografía (América del Norte, Europa, Asia Pacífico y América del Sur y Central).

- Estado : Datos publicados

- Código de informe : TIPRE00011953

- Categoría : Ciencias de la vida

- Número de páginas : 150

- Formatos de informe disponibles :

- Fecha de última actualización : June 26, 2026

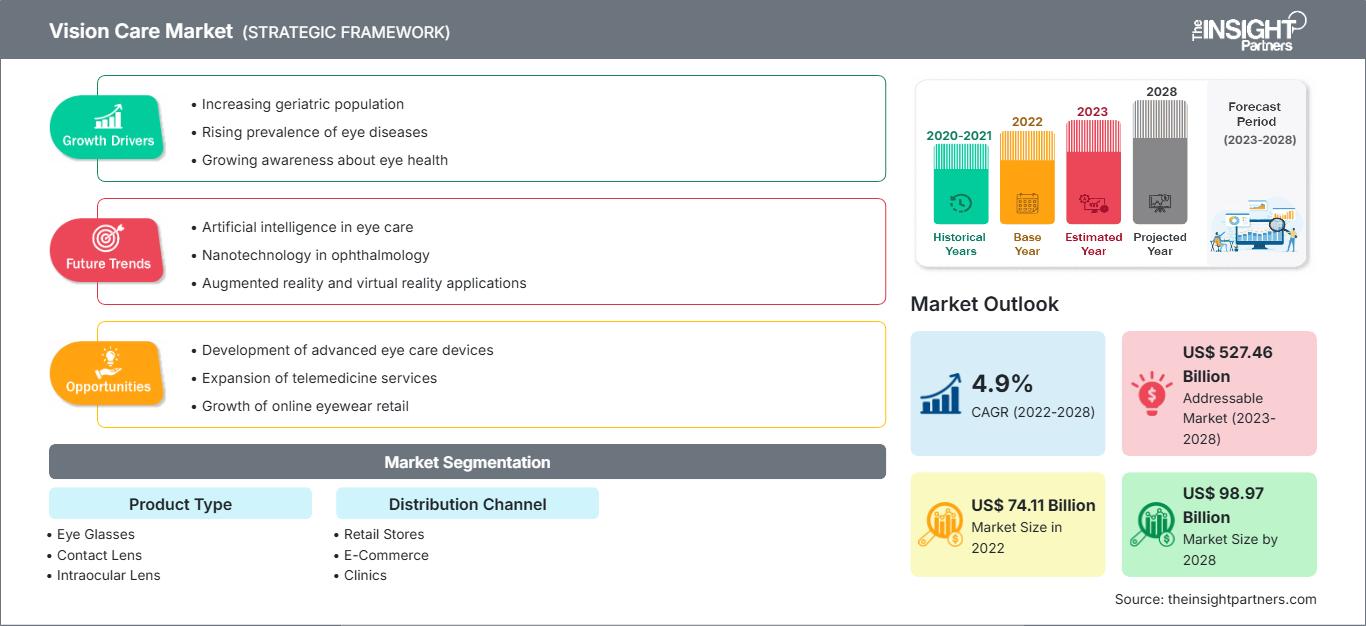

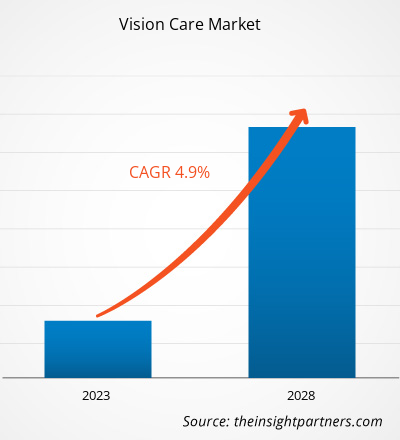

Se prevé que el mercado mundial del cuidado de la visión alcance los 70.500 millones de dólares estadounidenses en 2034, frente a los 46.100 millones de dólares estadounidenses en 2025. Se espera que el mercado registre una tasa de crecimiento anual compuesta (CAGR) del 4,83% durante el período de previsión 2026-2034.

Entre las principales dinámicas del mercado se incluyen una mayor atención mundial a la salud ocular debido al aumento del tiempo frente a las pantallas, la creciente prevalencia de la miopía en la población pediátrica y un cambio significativo hacia materiales de lentes de alta gama y alto índice de refracción. Además, se espera que el mercado se beneficie de la creciente popularidad de las lentes de contacto desechables diarias, la expansión de las cadenas de ópticas en las economías emergentes y la creciente incorporación de recubrimientos avanzados, como los filtros de luz azul y las tecnologías antirreflectantes, en las gafas graduadas estándar.

Análisis del mercado de atención oftalmológica

El análisis del mercado de la atención oftalmológica muestra una tendencia hacia la atención personalizada, ya que los consumidores priorizan tanto la agudeza visual como la estética. El mercado se está diversificando en segmentos de alto volumen y valor, así como en segmentos premium de alto crecimiento que incluyen el tallado digital de lentes y las gafas inteligentes. Surgen oportunidades estratégicas en el tratamiento de la miopía infantil, donde las lentes correctivas y de contacto especializadas ofrecen una clara ventaja competitiva sobre las opciones tradicionales. El crecimiento del mercado depende de la integración de la teleoptometría para el diagnóstico remoto y de una gestión eficiente de la cadena de suministro para el rápido acabado de las lentes. La diferenciación competitiva ahora se basa en una estrategia de marca que destaca el bienestar ocular, la protección UV y los materiales sostenibles para las monturas, como los bioacetatos. Este enfoque permite a las marcas premium fijar precios más altos en un mercado con diversos actores minoristas.

Descripción general del mercado de atención oftalmológica

Los productos para el cuidado de la visión han evolucionado desde herramientas funcionales básicas hasta convertirse en accesorios esenciales para la salud y el estilo de vida. El cuidado de la visión incluye lentes de contacto especializadas para el astigmatismo, lentes intraoculares multifocales y gafas deportivas de alto rendimiento. Tanto grandes corporaciones como startups de venta directa al consumidor compiten en este mercado, utilizando materiales como policarbonato, Trivex e hidrogel de silicona. La creciente demanda de cuidado ocular preventivo entre los consumidores preocupados por su salud en Norteamérica y Europa ha impulsado la popularidad de los recubrimientos de lentes premium como una solución estándar para el bienestar. Norteamérica lidera en ingresos gracias a su avanzada infraestructura sanitaria, mientras que Asia-Pacífico avanza en innovación manufacturera y adopción minorista. El mercado estadounidense es el más desarrollado, impulsado por el envejecimiento de la población y la amplia disponibilidad de seguros de visión. La competencia entre marcas fomenta una mayor variedad de monturas y la inclusión de funciones inteligentes como la tecnología fotocromática y las interfaces de realidad aumentada.

Personaliza este informe para adaptarlo a tus necesidades.

Obtén PERSONALIZACIÓN GRATUITAMercado del cuidado de la visión: Perspectivas estratégicas

-

Descubra las principales tendencias del mercado que se recogen en este informe.Esta muestra GRATUITA incluirá análisis de datos, que abarcan desde tendencias de mercado hasta estimaciones y pronósticos.

Factores impulsores y oportunidades del mercado de cuidado de la visión

Factores que impulsan el mercado:

- Aumento de la prevalencia de los trastornos de la visión: El incremento mundial de la miopía, la hipermetropía y la presbicia, impulsado por el envejecimiento de la población y el uso de dispositivos digitales, es un factor determinante en la demanda de gafas graduadas y lentes de contacto.

- Avances tecnológicos en el diseño de lentes: La expansión de la tecnología de tallado digital y de frente de onda ha mantenido una alta demanda de lentes de alta definición. A medida que los consumidores optan por una mayor claridad visual, las lentes progresivas siguen experimentando un crecimiento constante en su volumen de ventas.

- Expansión acelerada del comercio minorista omnicanal: El comercio electrónico de productos ópticos ha eliminado las barreras de entrada tradicionales. Esto se evidencia especialmente en la rápida adopción de marcas de gafas de venta directa al consumidor (D2C) y servicios de lentes de contacto por suscripción en Norteamérica y Europa.

Oportunidades de mercado:

- Expansión hacia el control de la miopía: Más allá de la corrección estándar, las lentes especializadas diseñadas para ralentizar la progresión de la miopía en niños ofrecen importantes oportunidades para los fabricantes de productos ópticos.

- Crecimiento en los corredores emergentes de la región Asia-Pacífico: La formación de alianzas estratégicas entre los líderes mundiales en el cuidado de la visión y los distribuidores locales puede facilitar el acceso a segmentos de mercado de alto margen en China e India, donde la concienciación sobre la salud ocular está aumentando.

- Diversificación hacia las gafas ecológicas: Existe una creciente oportunidad para que las marcas se dirijan a segmentos demográficos con conciencia ambiental a través de certificaciones como Contenido Reciclado y Materiales de Base Biológica.

Análisis de segmentación del informe de mercado de atención oftalmológica

La cuota de mercado del sector de la salud visual se analiza en diversos segmentos para comprender mejor su estructura, potencial de crecimiento y tendencias emergentes. A continuación, se muestra el enfoque de segmentación estándar utilizado en la mayoría de los informes del sector:

Por tipo de producto:

- Gafas: El segmento más grande por volumen, que abarca monturas y lentes. Sigue siendo la opción principal para la corrección de la visión a nivel mundial, impulsada por las tendencias de la moda y los recubrimientos tecnológicos de las lentes.

- Lentes de contacto: Un segmento en rápido crecimiento que satisface las necesidades de los consumidores que buscan comodidad y libertad estética. Las innovaciones en materiales de hidrogel de silicona han mejorado la comodidad y la facilidad de uso.

- Lentes intraoculares: Su uso se debe principalmente al creciente número de cirugías de cataratas y a los avances en los procedimientos quirúrgicos oftalmológicos para una población mundial que envejece.

- Otros: Incluye soluciones de limpieza, estuches para lentes y accesorios oculares especializados que facilitan el mantenimiento de los productos básicos para el cuidado de la visión.

Por canal de distribución:

- Tiendas minoristas: El canal dominante para la compra de gafas graduadas y de sol, que ofrece a los clientes servicios profesionales de ajuste y consultas presenciales.

- Comercio electrónico: El canal de distribución de más rápido crecimiento, que ofrece una amplia variedad de monturas y lentes de contacto con la comodidad de la entrega a domicilio y la posibilidad de probarse las gafas virtualmente.

- Clínicas: Un canal vital para la atención oftalmológica especializada y la prescripción de lentes de contacto de grado médico o productos terapéuticos.

- Hospitales: Se centra en la atención quirúrgica de la visión y la distribución de lentes intraoculares durante cirugías de cataratas o refractivas.

Por geografía:

- América del norte

- Europa

- Asia Pacífico

- América del Sur y Central

- Oriente Medio y África

Alcance del informe de mercado sobre el cuidado de la visión

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2025 | 46.100 millones de dólares estadounidenses |

| Tamaño del mercado para 2034 | 70.500 millones de dólares estadounidenses |

| Tasa de crecimiento anual compuesta global (2026 - 2034) | 4,83% |

| Datos históricos | 2021-2024 |

| Período de pronóstico | 2026-2034 |

| Segmentos cubiertos |

Por tipo de producto

|

| Regiones y países incluidos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de los actores del mercado de cuidado de la visión: comprender su impacto en la dinámica empresarial.

El mercado del cuidado de la visión está experimentando un rápido crecimiento, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y una mayor concienciación sobre los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

Análisis de la cuota de mercado de los servicios de atención oftalmológica por región geográfica

Se prevé que la región de Asia-Pacífico experimente el mayor crecimiento en los próximos años. Los mercados emergentes de América del Sur y Central, Oriente Medio y África también ofrecen numerosas oportunidades sin explotar para la expansión de fabricantes de gafas y proveedores de lentes correctivas. El mercado del cuidado de la visión está experimentando una transformación significativa, pasando de ser un sector médico basado en necesidades a una industria global de la salud y el estilo de vida impulsada por la tecnología. El crecimiento se debe a la creciente prevalencia de la fatiga visual digital, el aumento de la miopía pediátrica y la expansión del sector de gafas de diseño de lujo. A continuación, se presenta un resumen de la cuota de mercado y las tendencias por región:

América del norte

- Cuota de mercado: Un segmento maduro pero en constante crecimiento, impulsado por una infraestructura de diagnóstico avanzada y una alta penetración de los seguros.

-

Factores clave:

- Alta prevalencia de presbicia en la población de la generación del baby boom que envejece y requiere soluciones multifocales.

- Generalización de la tecnología de filtrado de luz azul en el bienestar corporativo y en entornos de trabajo remoto.

- Mayor adopción de lentes de contacto desechables diarias en lugar de las variantes reutilizables tradicionales.

- Tendencias: Rápida expansión de los servicios de teleoptometría y la exitosa integración de tecnologías de prueba virtual para mejorar la experiencia del consumidor en el comercio electrónico.

Europa

- Cuota de mercado: Posee una importante cuota de mercado global, respaldada por una larga tradición en el diseño de monturas de alta gama y la ingeniería de precisión de lentes en Italia, Alemania y Francia.

-

Factores clave:

- Alta demanda por parte de los consumidores de marcas de lujo icónicas y artesanía de alta calidad en gafas.

- Marcos regulatorios establecidos para dispositivos médicos oftálmicos y estándares profesionales

- Sólido apoyo público y privado de la atención médica para exámenes de la vista y procedimientos correctivos.

- Tendencias: Se observa un cambio estratégico hacia la fabricación sostenible, con marcas que priorizan los bioacetatos y los materiales reciclados. Asimismo, se aprecia un creciente interés en materiales para lentes de alto índice para satisfacer las demandas de los consumidores europeos preocupados por el estilo.

Asia-Pacífico

- Cuota de mercado: La región de mayor crecimiento, con China e India como principales mercados para todo el continente, especialmente en lo que respecta a productos para el control de la miopía.

-

Factores clave:

- Gran población estudiantil y de adultos jóvenes busca lentes especializados para controlar la progresión de la miopía.

- Las iniciativas de salud pública apoyadas por el gobierno se centraron en la detección temprana de problemas de visión en las escuelas.

- La rápida urbanización y el aumento de los ingresos disponibles están generando una preferencia por las marcas ópticas de lujo occidentalizadas.

- Tendencias: Gran dependencia de las plataformas de venta minorista omnicanal y un aumento en la demanda de monturas de marca propia asequibles pero elegantes en los centros urbanos emergentes.

América del Sur y Central

- Cuota de mercado: Mercado emergente con una creciente industria óptica profesional en países como Brasil y Chile.

-

Factores clave:

- Aumentar la concienciación sobre la importancia de la protección UV para la salud ocular en regiones con alta exposición solar.

- Modernización de ópticas independientes para convertirlas en cadenas minoristas formalizadas que abastezcan los centros urbanos.

- Aumento del interés por las cirugías refractivas electivas entre los segmentos de ingresos medios y altos.

- Tendencias: Crecimiento de marcas boutique basadas en la relación calidad-precio y la introducción de centros de fabricación regionales para reducir la dependencia de costosas importaciones de gafas.

Oriente Medio y África

- Cuota de mercado: Mercado en desarrollo con un importante potencial de crecimiento, en transición hacia servicios comerciales formalizados de atención oftalmológica.

-

Factores clave:

- Demanda tradicional de gafas de moda de alta gama en los países del Consejo de Cooperación del Golfo (CCG).

- Alta demanda de lentes especializadas capaces de soportar entornos hostiles, polvorientos y con mucho deslumbramiento.

- Inversiones estratégicas en centros de turismo médico para ofrecer cirugías oftalmológicas avanzadas.

- Tendencias: Implementación de clínicas oftalmológicas móviles para atender a las poblaciones rurales, junto con un enfoque en soluciones correctivas rentables para el segmento pediátrico.

Alta densidad de mercado y competencia

La competencia se intensifica debido a la presencia de líderes consolidados como EssilorLuxottica, Johnson & Johnson Vision Care y Alcon. Expertos regionales y empresas especializadas como Hoya Corporation y Carl Zeiss Meditec, junto con innovadores como Warby Parker y Zenni Optical, también contribuyen a un panorama de mercado diverso.

Este entorno competitivo impulsa a los proveedores a diferenciarse a través de:

- Integración tecnológica: Posicionar las gafas inteligentes y las lentes con superficie digital como alternativas superiores a la óptica estándar.

- Diversificación de productos: Ofrecemos una gama completa de productos, desde gotas para ojos secos hasta lentes intraoculares quirúrgicas y monturas de última moda.

- Integración vertical: Gestionar toda la cadena de valor, desde la fabricación de lentes y el diseño de monturas hasta los seguros minoristas y las clínicas oftalmológicas.

Oportunidades y movimientos estratégicos

- Colabora con plataformas de telesalud para aprovechar la creciente demanda de recetas oftalmológicas en línea y funciones de prueba virtual.

- Incorporar procesos de fabricación sostenibles para atraer a los consumidores de la Generación Z que buscan gafas éticas y con baja huella de carbono.

Las principales empresas que operan en el mercado del cuidado de la visión son:

- Alcon Inc

- Empresas de salud Bausch Inc.

- Carl Zeiss AG

- Cooper Companies Inc

- Essilorluxottica SA

- Johnson & Johnson Services Inc.

- Corporación Hoya

- Rodenstock GmbH

- Compañía Menicon Ltd.

- Lentes intraoculares Rayner limitada

Descargo de responsabilidad: Las empresas mencionadas anteriormente no están clasificadas en ningún orden en particular.

Noticias y novedades del mercado de cuidado de la visión

- En marzo de 2026, ZEISS Vision Care anunció una alianza estratégica con Medical Eyeglass Center (MEC), una organización de gestión de ópticas integral y reconocida a nivel nacional. Esta colaboración convierte a ZEISS en el laboratorio y proveedor de servicios exclusivo de MEC. MEC será la organización de gestión de ópticas exclusiva asociada con ZEISS en las ópticas participantes.

- En enero de 2026, HOYA® Vision Care, líder mundial en tecnología de lentes oftálmicas, anunció el lanzamiento de HOYA LensPreview™, una solución avanzada de prueba virtual integrada en el ecosistema HOYA Hub™.

Cobertura y entregables del informe de mercado sobre el cuidado de la visión

El informe "Tamaño y pronóstico del mercado de cuidado de la visión (2021-2034)" proporciona un análisis detallado del mercado que abarca las siguientes áreas:

- Tamaño y pronóstico del mercado de cuidado de la visión a nivel mundial, regional y nacional para todos los segmentos clave del mercado cubiertos en el alcance.

- Tendencias del mercado de cuidado de la visión, así como dinámicas del mercado como factores impulsores, limitaciones y oportunidades clave.

- Análisis detallado PEST y FODA

- Análisis del mercado de cuidado de la visión que abarca las principales tendencias del mercado, el marco global y regional, los principales actores, las regulaciones y los desarrollos recientes del mercado.

- Análisis del panorama de la industria y de la competencia, que abarca la concentración del mercado, el análisis de mapas de calor, los principales actores y los desarrollos recientes en el mercado del cuidado de la visión.

- Perfiles detallados de las empresas

Mrinal es una experimentada analista de investigación con más de 8 años de experiencia en inteligencia de mercado y consultoría en ciencias de la vida. Con una mentalidad estratégica y un firme compromiso con la excelencia, ha desarrollado una amplia experiencia en pronósticos farmacéuticos, evaluación de oportunidades de mercado y desarrollo de indicadores de referencia para la industria. Su trabajo se centra en brindar información práctica que permita a los clientes tomar decisiones estratégicas informadas.

La principal fortaleza de Mrinal reside en convertir conjuntos de datos cuantitativos complejos en inteligencia de negocios significativa. Su perspicacia analítica es fundamental para definir estrategias de salida al mercado (GTM) y descubrir oportunidades de crecimiento en los sectores farmacéutico y de dispositivos médicos. Como consultora de confianza, se centra constantemente en optimizar los procesos de flujo de trabajo y establecer las mejores prácticas, impulsando así la innovación y la eficiencia operativa para sus clientes.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias