Marktgröße, Trends und Wachstum des Marktes für Augenpflege bis 2034

Marktgröße und Prognosen für den Markt für Sehkorrekturprodukte (2021–2034), globaler und regionaler Marktanteil, Trends und Analyse der Wachstumschancen. Berichtsabdeckung: Nach Produkttyp (Brillen, Kontaktlinsen, Intraokularlinsen und Sonstiges) und Vertriebskanal (Einzelhandel, E-Commerce, Kliniken und Krankenhäuser) sowie Geografie (Nordamerika, Europa, Asien-Pazifik sowie Süd- und Mittelamerika).

- Status : Veröffentlichte Daten

- Berichtscode : TIPRE00011953

- Kategorie : Biowissenschaften

- Anzahl der Seiten : 150

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 26, 2026

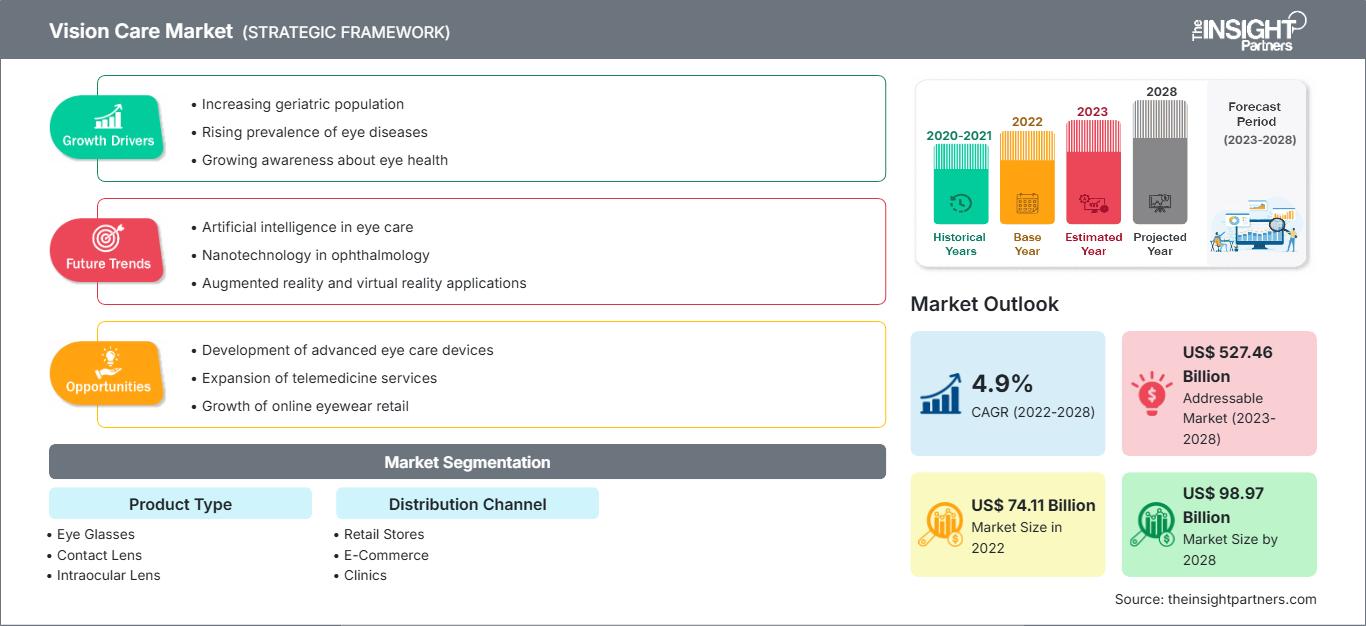

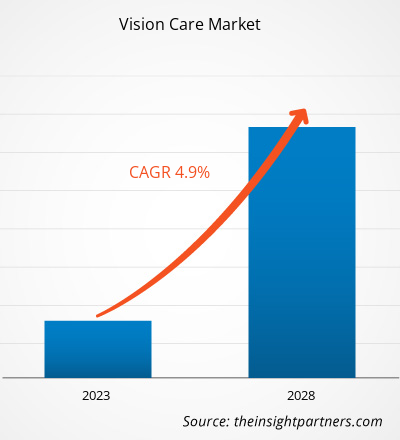

Der globale Markt für Augenpflege wird bis 2034 voraussichtlich ein Volumen von 70,50 Milliarden US-Dollar erreichen, gegenüber 46,10 Milliarden US-Dollar im Jahr 2025. Es wird erwartet, dass der Markt im Prognosezeitraum 2026–2034 eine durchschnittliche jährliche Wachstumsrate (CAGR) von 4,83 % verzeichnen wird.

Zu den wichtigsten Marktdynamiken zählen der weltweit zunehmende Fokus auf Augengesundheit aufgrund der vermehrten Bildschirmzeit, die steigende Verbreitung von Kurzsichtigkeit bei Kindern und Jugendlichen sowie der deutliche Trend hin zu hochwertigen, hochbrechenden Linsenmaterialien. Darüber hinaus dürfte der Markt von der wachsenden Beliebtheit von Tageskontaktlinsen, der Expansion optischer Einzelhandelsketten in Schwellenländern und dem zunehmenden Einsatz fortschrittlicher Beschichtungen wie Blaulichtfilter und Antireflexbeschichtungen in Standard-Korrektionsbrillen profitieren.

Marktanalyse für Augenpflege

Die Marktanalyse im Bereich der Sehkorrektur zeigt einen Trend hin zu personalisierter Augenversorgung, da Verbraucher sowohl Sehschärfe als auch Ästhetik priorisieren. Der Markt diversifiziert sich in volumenstarke und wertorientierte Segmente sowie in wachstumsstarke Premiumsegmente mit digitaler Linsenbearbeitung und intelligenten Brillen. Strategische Chancen eröffnen sich im Bereich der Myopiebehandlung für Kinder, wo spezialisierte Korrektions- und Kontaktlinsen einen klaren Wettbewerbsvorteil gegenüber herkömmlichen Optionen bieten. Das Marktwachstum hängt von der Integration der Teleoptometrie für die Ferndiagnostik und einem effizienten Lieferkettenmanagement für die schnelle Linsenbearbeitung ab. Die Wettbewerbsdifferenzierung erfolgt heute vor allem durch Branding, das die Augengesundheit, den UV-Schutz und nachhaltige Rahmenmaterialien wie Bioacetate hervorhebt. Dieser Ansatz ermöglicht es Premiummarken, in einem Markt mit vielfältigen Einzelhändlern höhere Preise zu erzielen.

Marktübersicht für Augenpflege

Produkte für die Augengesundheit haben sich von einfachen Funktionsgeräten zu unverzichtbaren Gesundheits- und Lifestyle-Accessoires entwickelt. Dazu gehören Spezialkontaktlinsen für Astigmatismus, multifokale Intraokularlinsen und Sportbrillen. Globale Konzerne und D2C-Startups konkurrieren in diesem Markt und verwenden Materialien wie Polycarbonat, Trivex und Silikonhydrogel. Die steigende Nachfrage nach präventiver Augenpflege bei gesundheitsbewussten Verbrauchern in Nordamerika und Europa hat die Beliebtheit von Premium-Linsenbeschichtungen als Standardlösung für mehr Wohlbefinden erhöht. Nordamerika ist aufgrund seiner fortschrittlichen Gesundheitsinfrastruktur umsatzstärkster Markt, während der asiatisch-pazifische Raum bei Fertigungsinnovationen und der Akzeptanz im Einzelhandel aufholt. Der US-Markt ist der am weitesten entwickelte, angetrieben durch eine alternde Bevölkerung und die breite Verfügbarkeit von Sehversicherungen. Der Wettbewerb zwischen den Marken fördert eine größere Vielfalt an Brillenfassungen und die Integration intelligenter Funktionen wie photochromer Technologie und Augmented-Reality-Schnittstellen.

Passen Sie diesen Bericht Ihren Anforderungen an.

Kostenlose AnpassungMarkt für Augenpflege: Strategische Einblicke

-

Ermitteln Sie die wichtigsten Markttrends dieses Berichts.Diese KOSTENLOSE Probe beinhaltet eine Datenanalyse, die von Markttrends bis hin zu Schätzungen und Prognosen reicht.

Markttreiber und Chancen im Bereich der Augenheilkunde

Markttreiber:

- Zunehmende Verbreitung von Sehstörungen: Der weltweite Anstieg von Kurzsichtigkeit, Weitsichtigkeit und Alterssichtigkeit, bedingt durch die alternde Bevölkerung und die Nutzung digitaler Geräte, ist ein Hauptgrund für den Bedarf an verschreibungspflichtigen Brillen und Kontaktlinsen.

- Technologische Fortschritte im Brillenglasdesign: Die zunehmende Verbreitung digitaler Oberflächen- und Wellenfronttechnologie sorgt für eine anhaltend hohe Nachfrage nach hochauflösenden Brillengläsern. Da Verbraucher Wert auf überlegene Sehschärfe legen, verzeichnen Gleitsichtgläser weiterhin stetig steigende Absatzzahlen.

- Rasante Expansion des Omnichannel-Handels: Der Online-Optikhandel hat traditionelle Markteintrittsbarrieren beseitigt. Dies zeigt sich besonders deutlich in der schnellen Verbreitung von D2C-Brillenmarken und abonnementbasierten Kontaktlinsendiensten in Nordamerika und Europa.

Marktchancen:

- Erweiterung des Myopiemanagements: Über die Standardkorrektur hinaus bieten Speziallinsen, die das Fortschreiten der Myopie bei Kindern verlangsamen sollen, optische Herstellern bedeutende Möglichkeiten.

- Wachstum in aufstrebenden APAC-Korridoren: Die Bildung strategischer Partnerschaften zwischen globalen Marktführern im Bereich der Augenversorgung und lokalen Vertriebspartnern kann den Zugang zu margenstarken Marktsegmenten in China und Indien erleichtern, wo das Bewusstsein für Augengesundheit zunimmt.

- Diversifizierung hin zu umweltfreundlicher Brillenmode: Für Marken ergeben sich zunehmend Möglichkeiten, umweltbewusste Zielgruppen durch Zertifizierungen wie Recyclinganteil und biobasierte Materialien anzusprechen.

Marktbericht für Sehpflege: Segmentierungsanalyse

Der Marktanteil im Bereich der Augenheilkunde wird in verschiedenen Segmenten analysiert, um ein besseres Verständnis seiner Struktur, seines Wachstumspotenzials und der sich abzeichnenden Trends zu ermöglichen. Nachfolgend ist der in den meisten Branchenberichten verwendete Standardansatz zur Segmentierung dargestellt:

Nach Produkttyp:

- Brillen: Das mengenmäßig größte Segment, bestehend aus Gestellen und Gläsern. Sie bleiben weltweit die erste Wahl zur Sehkorrektur, angetrieben von Modetrends und technologischen Glasbeschichtungen.

- Kontaktlinsen: Ein schnell wachsendes Segment für Konsumenten, die Wert auf Komfort und ästhetische Freiheit legen. Innovationen bei Silikon-Hydrogel-Materialien haben Tragekomfort und Haltbarkeit verbessert.

- Intraokularlinse: Hauptsächlich bedingt durch die steigende Anzahl von Kataraktoperationen und Fortschritte bei ophthalmologischen Operationsverfahren für eine alternde Weltbevölkerung.

- Sonstiges: Dazu gehören Reinigungslösungen, Linsenbehälter und spezielles Augenzubehör, das die Pflege von primären Augenpflegeprodukten unterstützt.

Nach Vertriebskanal:

- Einzelhandelsgeschäfte: Der dominierende Vertriebskanal für den Kauf von Brillen und Sonnenbrillen, der den Kunden professionelle Anpassungsdienste und persönliche Beratungen bietet.

- E-Commerce: Der am schnellsten wachsende Vertriebskanal, der eine große Auswahl an Brillenfassungen und Kontaktlinsen mit dem Komfort der Lieferung nach Hause und der Möglichkeit zur virtuellen Anprobe bietet.

- Kliniken: Ein wichtiger Kanal für spezialisierte diagnostische Sehversorgung und die Verschreibung von medizinischen Kontaktlinsen oder therapeutischen Produkten.

- Krankenhäuser: Schwerpunkt auf chirurgischer Augenversorgung und der Verteilung von Intraokularlinsen bei Katarakt- oder refraktiven Operationen.

Nach Geographie:

- Nordamerika

- Europa

- Asien-Pazifik

- Süd- und Mittelamerika

- Naher Osten und Afrika

Berichtsumfang zum Markt für Augenpflege

| Berichtattribute | Details |

|---|---|

| Marktgröße im Jahr 2025 | 46,10 Milliarden US-Dollar |

| Marktgröße bis 2034 | 70,50 Milliarden US-Dollar |

| Globale durchschnittliche jährliche Wachstumsrate (2026 - 2034) | 4,83 % |

| Historische Daten | 2021-2024 |

| Prognosezeitraum | 2026–2034 |

| Abgedeckte Segmente |

Nach Produkttyp

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Marktdichte im Bereich der Augenheilkunde: Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Augenpflegeprodukte wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher. Gründe hierfür sind unter anderem sich wandelnde Verbraucherpräferenzen, technologische Fortschritte und ein wachsendes Bewusstsein für die Vorteile der Produkte. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln innovative Lösungen, um den Bedürfnissen der Verbraucher gerecht zu werden, und nutzen neue Trends, was das Marktwachstum zusätzlich beflügelt.

Marktanteilsanalyse für Sehpflegeprodukte nach Regionen

Der asiatisch-pazifische Raum wird in den kommenden Jahren voraussichtlich das schnellste Wachstum verzeichnen. Auch die aufstrebenden Märkte in Süd- und Mittelamerika, dem Nahen Osten und Afrika bieten Brillenherstellern und Anbietern von Korrektionsgläsern zahlreiche ungenutzte Expansionsmöglichkeiten. Der Markt für Sehkorrekturen befindet sich in einem tiefgreifenden Wandel: Er entwickelt sich von einer auf Grundbedürfnissen basierenden medizinischen Versorgung zu einer globalen, technologiegetriebenen Gesundheits- und Lifestyle-Branche. Wachstumstreiber sind die zunehmende digitale Augenbelastung, der Anstieg von Kurzsichtigkeit bei Kindern und die Expansion des Segments für luxuriöse Designerbrillen. Nachfolgend finden Sie eine Zusammenfassung der Marktanteile und Trends nach Regionen:

Nordamerika

- Marktanteil: Ein ausgereiftes, aber stetig wachsendes Segment, das durch eine fortschrittliche Diagnoseinfrastruktur und eine hohe Versicherungsdurchdringung angetrieben wird.

-

Wichtigste Einflussfaktoren:

- Hohe Prävalenz von Presbyopie in der alternden Babyboomer-Bevölkerung, die Gleitsichtbrillenlösungen erfordert

- Etablierung der Blaulichtfiltertechnologie im betrieblichen Gesundheitsmanagement und in Remote-Arbeitsumgebungen

- Zunehmende Nutzung von Tageslinsen gegenüber herkömmlichen wiederverwendbaren Linsen

- Trends: Rasante Ausweitung der Tele-Optometrie-Dienstleistungen und die erfolgreiche Integration von virtuellen Anprobe-Technologien zur Verbesserung des Einkaufserlebnisses im E-Commerce.

Europa

- Marktanteil: Besitzt einen bedeutenden globalen Marktanteil, der auf einer tief verwurzelten Tradition im Premium-Rahmendesign und der Präzisions-Linsenentwicklung in Italien, Deutschland und Frankreich basiert.

-

Wichtigste Einflussfaktoren:

- Hohe Verbrauchernachfrage nach ikonischen Luxusmarken und hochwertiger Handwerkskunst bei Brillen

- Etablierte regulatorische Rahmenbedingungen für ophthalmologische Medizinprodukte und Berufsstandards

- Robuste öffentliche und private Unterstützung des Gesundheitswesens für Sehscreening und Korrekturverfahren

- Trends: Ein strategischer Wandel hin zu nachhaltiger Produktion zeichnet sich ab, wobei Marken Bioacetate und Recyclingmaterialien priorisieren. Zudem rücken hochbrechende Linsenmaterialien immer stärker in den Fokus, um den Ansprüchen stilbewusster europäischer Konsumenten gerecht zu werden.

Asien-Pazifik

- Marktanteil: Die am schnellsten wachsende Region, wobei China und Indien die Hauptmärkte für den gesamten Kontinent darstellen, insbesondere für Produkte zur Myopiekontrolle.

-

Wichtigste Einflussfaktoren:

- Eine große Anzahl von Studenten und jungen Erwachsenen sucht nach Spezialbrillen zur Behandlung von Kurzsichtigkeit.

- Staatlich geförderte Initiativen im Bereich der öffentlichen Gesundheit konzentrierten sich auf groß angelegte Sehtests in Schulen.

- Die rasante Urbanisierung und steigende verfügbare Einkommen führen zu einer Vorliebe für westliche Luxus-Optikmarken.

- Trends: Starke Abhängigkeit von Omnichannel-Handelsplattformen und eine steigende Nachfrage nach erschwinglichen, aber dennoch stilvollen Eigenmarken-Brillenfassungen in aufstrebenden urbanen Zentren.

Süd- und Mittelamerika

- Marktanteil: Aufstrebender Markt mit einer wachsenden professionellen Optikindustrie in Ländern wie Brasilien und Chile.

-

Wichtigste Einflussfaktoren:

- Zunehmendes Bewusstsein für die Bedeutung des UV-Schutzes für die Augengesundheit in sonnenreichen Regionen

- Modernisierung unabhängiger Optikergeschäfte zu formalisierten Einzelhandelsketten zur Versorgung urbaner Zentren

- Steigendes Interesse an elektiven refraktiven Eingriffen in mittleren bis hohen Einkommensschichten

- Trends: Wachstum preisorientierter Boutique-Marken und Einführung regionaler Produktionszentren zur Verringerung der Abhängigkeit von teuren importierten Brillen.

Naher Osten und Afrika

- Marktanteil: Entwicklungsmarkt mit erheblichem Wachstumspotenzial, der sich in Richtung formalisierter kommerzieller Augenpflegedienstleistungen entwickelt.

-

Wichtigste Einflussfaktoren:

- Traditionelle Nachfrage nach hochwertigen modischen Brillen in den Ländern des Golf-Kooperationsrats (GCC)

- Hohe Nachfrage nach Spezialobjektiven, die rauen, staubigen und stark blendenden Umgebungen standhalten können.

- Strategische Investitionen in Zentren für Medizintourismus zur Bereitstellung fortschrittlicher Augenoperationen

- Trends: Einsatz mobiler Augenkliniken zur Versorgung der ländlichen Bevölkerung, verbunden mit einem Fokus auf kosteneffektive Korrekturlösungen für Kinder.

Hohe Marktdichte und starker Wettbewerb

Der Wettbewerb verschärft sich aufgrund der Präsenz etablierter Marktführer wie EssilorLuxottica, Johnson & Johnson Vision Care und Alcon. Regionale Experten und Nischenanbieter wie Hoya Corporation und Carl Zeiss Meditec tragen neben Innovatoren wie Warby Parker und Zenni Optical ebenfalls zu einer vielfältigen Marktlandschaft bei.

Dieses wettbewerbsintensive Umfeld zwingt die Anbieter dazu, sich durch Folgendes zu differenzieren:

- Technologische Integration: Positionierung von Smart Glasses und digital beschichteten Linsen als überlegene Alternativen zur Standardoptik.

- Produktdiversifizierung: Wir bieten eine komplette Produktpalette an, von Augentropfen gegen trockene Augen über chirurgische Intraokularlinsen bis hin zu modischen Brillenfassungen.

- Vertikale Integration: Management der gesamten Wertschöpfungskette von der Linsenherstellung und dem Rahmendesign bis hin zu Einzelhandelsversicherungen und Augenkliniken.

Chancen und strategische Schritte

- Kooperieren Sie mit Telemedizinplattformen, um die stark steigende Nachfrage nach Online-Sehrezepten und virtuellen Anproben zu nutzen.

- Durch die Integration nachhaltiger Fertigungsprozesse soll die Generation Z angesprochen werden, die ethisch vertretbare Brillen mit geringem CO2-Fußabdruck sucht.

Die wichtigsten Unternehmen auf dem Markt für Augenpflege sind:

- Alcon Inc

- Bausch Health Companies Inc

- Carl Zeiss AG

- Cooper Companies Inc

- Essilorluxottica SA

- Johnson & Johnson Services Inc.

- Hoya Corporation

- Rodenstock GmbH

- Menicon Co. Ltd

- Rayner Intraokularlinsen Limited

Hinweis: Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge geordnet.

Neuigkeiten und aktuelle Entwicklungen im Markt für Augenheilkunde

- Im März 2026 gab ZEISS Vision Care eine strategische Partnerschaft mit Medical Eyeglass Center (MEC) bekannt, einem landesweit anerkannten Full-Service-Anbieter für die Verwaltung von Optikfachgeschäften. Durch diese Zusammenarbeit wird ZEISS exklusiver Labor- und Servicepartner innerhalb der MEC-Organisation für die Verwaltung von Optikfachgeschäften. MEC wird in den teilnehmenden Praxen als exklusiver Partner von ZEISS für die Verwaltung von Optikfachgeschäften fungieren.

- Im Januar 2026 kündigte HOYA® Vision Care, ein weltweit führender Anbieter von ophthalmischen Linsentechnologien, die Markteinführung von HOYA LensPreview™ an, einer fortschrittlichen virtuellen Anprobelösung, die in das HOYA Hub™-Ökosystem integriert ist.

Marktbericht zur Augenheilkunde: Abdeckung und Ergebnisse

Der Bericht „Marktgröße und Prognose für den Markt für Augenpflege (2021–2034)“ bietet eine detaillierte Analyse des Marktes und deckt folgende Bereiche ab:

- Marktgröße und Prognose für den Markt für Augenheilkunde auf globaler, regionaler und Länderebene für alle wichtigen Marktsegmente, die im Rahmen des Berichts abgedeckt werden

- Trends im Markt für Augenheilkunde sowie Marktdynamiken wie Treiber, Hemmnisse und wichtige Chancen

- Detaillierte PEST- und SWOT-Analyse

- Marktanalyse für Augenpflege mit Fokus auf wichtige Markttrends, globale und regionale Rahmenbedingungen, Hauptakteure, regulatorische Rahmenbedingungen und aktuelle Marktentwicklungen

- Branchenlandschafts- und Wettbewerbsanalyse mit Fokus auf Marktkonzentration, Heatmap-Analyse, prominente Akteure und aktuelle Entwicklungen im Markt für Augenpflege.

- Detaillierte Unternehmensprofile

Mrinal ist eine erfahrene Research-Analystin mit über 8 Jahren Erfahrung in der Marktanalyse und Beratung im Bereich Life Sciences. Mit ihrer strategischen Denkweise und ihrem unerschütterlichen Streben nach Exzellenz hat sie sich umfassende Expertise in den Bereichen Pharmaprognosen, Marktchancenbewertung und Entwicklung von Branchen-Benchmarks angeeignet. Ihre Arbeit konzentriert sich darauf, umsetzbare Erkenntnisse zu liefern, die Kunden fundierte strategische Entscheidungen ermöglichen. Mrinals Kernkompetenz liegt in der Übersetzung komplexer quantitativer Datensätze in aussagekräftige Geschäftsinformationen. Ihr analytischer Scharfsinn ist entscheidend für die Entwicklung von Go-to-Market-Strategien (GTM) und die Erschließung von Wachstumschancen in der Pharma- und Medizinproduktebranche. Als vertrauenswürdige Beraterin konzentriert sie sich konsequent auf die Optimierung von Arbeitsabläufen und die Etablierung von Best Practices, um so Innovation und Betriebseffizienz für ihre Kunden zu fördern.

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends