Perspectives et opportunités du marché des laboratoires de diagnostic à l'horizon 2034

Taille et prévisions du marché des laboratoires de diagnostic (2021-2034), parts de marché mondiales et régionales, tendances et analyse des opportunités de croissance : par type de laboratoire (laboratoires indépendants, laboratoires hospitaliers, laboratoires de cabinets médicaux) ; services de test (tests de la fonction physiologique, tests généraux et cliniques, tests spécialisés, tests prénataux non invasifs, tests COVID-19) ; source de revenus (organismes de régimes d’assurance maladie, paiements directs, système public) ; et zone géographique.

- Statut : Données publiées

- Code du rapport : TIPRE00029512

- Catégorie : Sciences de la vie

- Nombre de pages : 150

- Formats de rapport disponibles :

- Date de dernière mise à jour : January 27, 2026

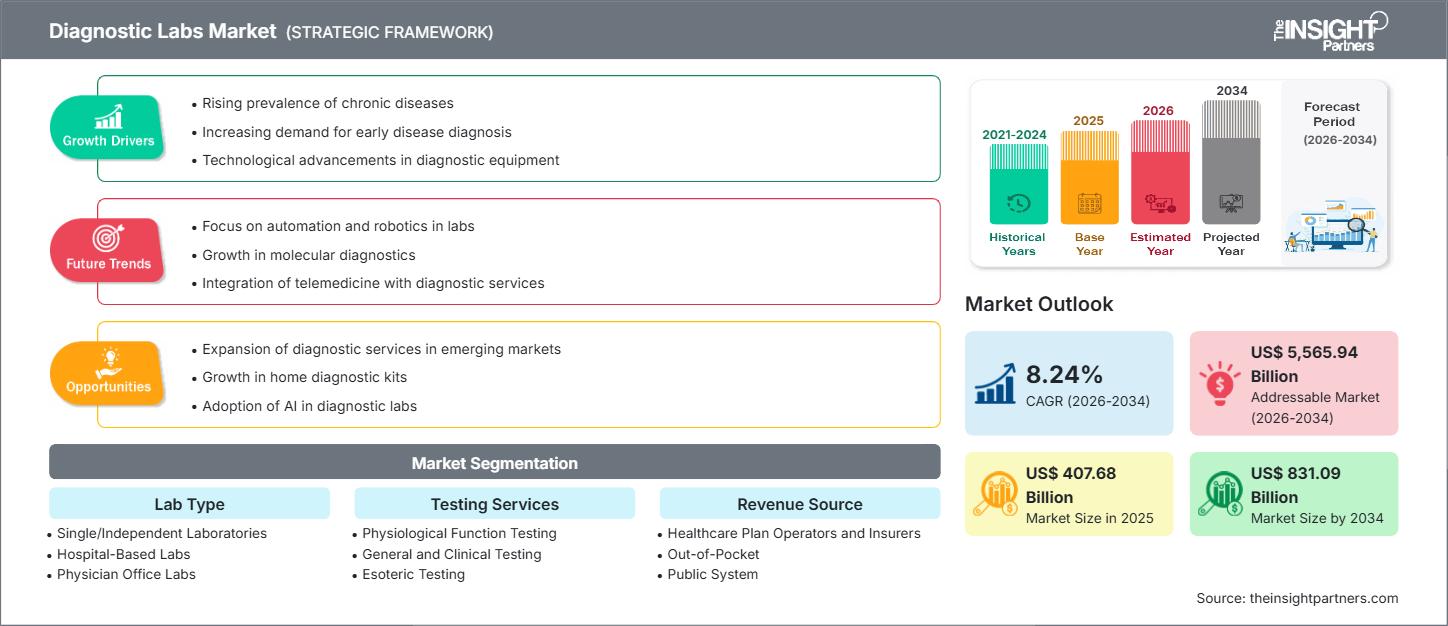

Le marché des laboratoires de diagnostic devrait atteindre 831,09 milliards de dollars américains d'ici 2034, contre 407,68 milliards de dollars américains en 2025. Ce marché devrait enregistrer un TCAC de 8,24 % entre 2026 et 2034.

Analyse du marché des laboratoires de diagnostic

Le marché des laboratoires de diagnostic est en pleine expansion, porté par la prévalence croissante des maladies chroniques et infectieuses à l'échelle mondiale, qui exige des tests fréquents et précis pour un dépistage précoce, un suivi adapté et une planification du traitement. Ce marché connaît une évolution majeure vers des technologies de diagnostic avancées, telles que le diagnostic moléculaire, les tests génétiques et les tests au point de soins (POC), qui offrent des résultats plus rapides et plus précis. L'importance croissante accordée à la médecine préventive et personnalisée stimule également fortement la demande de services de diagnostic. Les laboratoires de diagnostic jouent un rôle essentiel dans l'écosystème de la santé, en fournissant aux professionnels de santé des informations cruciales pour la prise de décisions éclairées concernant les soins aux patients.

Aperçu du marché des laboratoires de diagnostic

Un laboratoire de diagnostic est un établissement spécialisé, doté d'instruments, de réactifs et d'une équipe de professionnels qualifiés, qui réalise un large éventail d'examens et d'analyses médicales sur des échantillons de patients afin de contribuer au diagnostic, à la prise en charge et à la prévention de diverses pathologies. La mise en œuvre de technologies de pointe, notamment l'automatisation et l'intégration de l'intelligence artificielle (IA) et de l'apprentissage automatique (AA), révolutionne les processus de diagnostic en améliorant la précision, l'efficacité et l'interprétation des données. Parmi les principales tendances, on note le développement des tests décentralisés, l'expansion du prélèvement à domicile et l'intégration croissante des services de diagnostic aux plateformes de télémédecine, autant d'éléments visant à améliorer l'accessibilité et le confort des patients. Le respect des réglementations et la garantie de normes de qualité élevées sont des facteurs essentiels qui structurent le fonctionnement de ce marché.

Personnalisez ce rapport selon vos besoins.

Bénéficiez d'une PERSONNALISATION GRATUITEMarché des laboratoires de diagnostic : Perspectives stratégiques

-

Découvrez les principales tendances du marché présentées dans ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Facteurs et opportunités du marché des laboratoires de diagnostic

Facteurs de marché :

- Prévalence croissante des maladies chroniques et infectieuses : La charge mondiale croissante de maladies chroniques comme le diabète, les troubles cardiovasculaires et le cancer, ainsi que le besoin constant de surveillance des maladies infectieuses, alimentent la demande de tests diagnostiques fréquents et spécialisés.

- Progrès technologiques dans les équipements de diagnostic : des innovations telles que le séquençage de nouvelle génération (NGS), les techniques d’imagerie avancées et les analyseurs de chimie clinique/immunoessais hautement automatisés contribuent à des diagnostics plus rapides et plus précis, stimulant ainsi l’adoption par le marché.

- Importance croissante accordée aux soins de santé préventifs : la sensibilisation accrue de la population à l’importance des examens de santé réguliers et du dépistage précoce des maladies augmente le nombre de tests effectués, déplaçant l’attention des « soins aux malades » vers les « soins de bien-être ».

Opportunités de marché :

- Intégration des diagnostics numériques et améliorés par l'IA : L'utilisation de l'IA et de l'apprentissage automatique pour l'analyse de données complexes (par exemple, en radiologie et en pathologie) peut améliorer l'efficacité et faciliter l'interprétation des résultats, offrant ainsi d'importantes opportunités d'innovation et de croissance.

- Croissance des tests au point de service (POC) et des soins de santé décentralisés : le passage à des modèles décentralisés, facilité par des dispositifs POC rapides et faciles à utiliser (comme les glucomètres et les tests de maladies infectieuses), permet une prise de décision clinique plus rapide et étend les tests aux soins à domicile et aux cabinets médicaux.

- Médecine personnalisée et tests génétiques : La demande croissante de médecine personnalisée et de précision accélère le besoin de diagnostics moléculaires avancés et de tests génétiques (comme les tests développés en laboratoire – LDT) pour adapter les traitements aux profils individuels des patients.

Analyse de segmentation du rapport sur le marché des laboratoires de diagnostic

Le marché des laboratoires de diagnostic est analysé selon différents segments afin de mieux comprendre sa structure, son potentiel de croissance et les tendances émergentes.

Par type de laboratoire :

- Laboratoires uniques/indépendants

- Laboratoires hospitaliers

- Laboratoires en cabinet médical

Par les services de test :

- Tests de fonction physiologique

- Tests généraux et cliniques

- Tests ésotériques

- Tests spécialisés

- Tests prénataux non invasifs

- Tests de dépistage de la COVID-19

Par source de revenus :

- Gestionnaires de régimes de soins de santé et assureurs

- Frais à votre charge

- Système public

Par géographie :

- Amérique du Nord

- Europe

- Asie-Pacifique

- Amérique du Sud et centrale

- Moyen-Orient et Afrique

Aperçu régional du marché des laboratoires de diagnostic

Les tendances régionales et les facteurs influençant le marché des laboratoires de diagnostic tout au long de la période prévisionnelle ont été analysés en détail par les analystes de The Insight Partners. Cette section aborde également les segments de marché et la répartition géographique des laboratoires de diagnostic en Amérique du Nord, en Europe, en Asie-Pacifique, au Moyen-Orient et en Afrique, ainsi qu'en Amérique du Sud et centrale.

Portée du rapport sur le marché des laboratoires de diagnostic

| Attribut du rapport | Détails |

|---|---|

| Taille du marché en 2025 | 407,68 milliards de dollars américains |

| Taille du marché d'ici 2034 | 831,09 milliards de dollars américains |

| TCAC mondial (2026 - 2034) | 8,24% |

| Données historiques | 2021-2024 |

| Période de prévision | 2026-2034 |

| Segments couverts |

Par type de laboratoire

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché des laboratoires de diagnostic : comprendre son impact sur la dynamique commerciale

Le marché des laboratoires de diagnostic connaît une croissance rapide, portée par une demande croissante des utilisateurs finaux. Cette demande est alimentée par l'évolution des préférences des consommateurs, les progrès technologiques et une meilleure connaissance des avantages des produits. Face à cette demande grandissante, les entreprises diversifient leur offre, innovent pour répondre aux besoins des consommateurs et tirent parti des tendances émergentes, ce qui contribue à stimuler la croissance du marché.

- Obtenez un aperçu des principaux acteurs du marché des laboratoires de diagnostic

Analyse des parts de marché des laboratoires de diagnostic par zone géographique

L'Amérique du Nord détient une part de marché importante, grâce à son infrastructure de santé bien établie, à ses dépenses de santé élevées et à l'adoption précoce des technologies de diagnostic avancées et de la médecine personnalisée.

Le marché affiche une trajectoire de croissance variable selon les régions en raison de facteurs tels que les cadres réglementaires, la maturité technologique et la prévalence des maladies.

-

Amérique du Nord

- Part de marché : Détient la plus grande part de marché, grâce à une infrastructure de R&D solide et à la présence d'entreprises leaders dans le domaine du diagnostic et des technologies médicales.

- Facteurs clés : forte adoption des technologies de pointe, accent mis sur la santé préventive et la médecine personnalisée, et environnement réglementaire favorable (par exemple, les approbations de la FDA).

- Tendances : Utilisation accrue de l'automatisation, intégration de l'IA dans l'imagerie et la pathologie, et croissance des tests génétiques directs aux consommateurs (DTC).

-

Europe

- Part de marché : Détient une part de marché substantielle, grâce à un système de santé bien développé et aux initiatives gouvernementales en matière de santé publique.

- Facteurs clés : forte prévalence des maladies chroniques et liées à l’âge, et normes réglementaires strictes garantissant la qualité et la fiabilité des tests.

- Tendances : Investissements croissants dans les diagnostics moléculaires avancés et adoption de solutions de tests POC décentralisées pour la prise en charge des maladies chroniques.

-

Asie-Pacifique

- Part de marché : Le marché régional à la croissance la plus rapide, stimulée par une urbanisation rapide, un meilleur accès aux soins de santé et une population importante.

- Principaux facteurs : développement des infrastructures de santé soutenu par les gouvernements, sensibilisation accrue à la santé et investissements croissants des sociétés mondiales de diagnostic dans les économies émergentes comme la Chine et l'Inde.

- Tendances : Expansion des réseaux de chaînes de diagnostic dans les villes de deuxième et troisième rang, adoption de solutions de diagnostic abordables et localisées, et croissance rapide des services de prélèvement d'échantillons à domicile.

-

Amérique du Sud et centrale

- Part de marché : Région émergente à la demande croissante, mais souvent confrontée à des défis liés aux infrastructures et aux dépenses de santé publique.

- Facteurs clés : sensibilisation accrue aux maladies infectieuses et non transmissibles, et modernisation progressive des installations de laboratoires cliniques.

- Tendances : Expansion des systèmes de gestion de l'information de laboratoire (LIMS) abordables et basés sur le cloud, et adoption des services de diagnostic de base.

-

Moyen-Orient et Afrique

- Part de marché : Marché émergent à fort potentiel de croissance, tiré par la transformation numérique et les dépenses de santé dans les pays du Conseil de coopération du Golfe (CCG) et en Afrique du Sud.

- Principaux facteurs : grandes stratégies nationales en matière de santé numérique et d'IA, augmentation des investissements du secteur privé dans les établissements de santé et besoin croissant de diagnostics des maladies infectieuses.

- Tendances : Intégration rapide des chatbots IA et des systèmes de gestion communautaire pour l'engagement des patients et la logistique, et accent mis sur la création de centres de diagnostic accrédités et de haute qualité.

Densité des acteurs du marché des laboratoires de diagnostic : comprendre son impact sur la dynamique commerciale

Le marché des laboratoires de diagnostic se caractérise par un mélange de grandes multinationales intégrées, de fabricants de dispositifs médicaux, d'entreprises spécialisées dans les tests moléculaires et génétiques, et de puissants réseaux de laboratoires régionaux et nationaux. La forte concurrence est alimentée par la nécessité d'être rapide, précis et rentable.

Le contexte concurrentiel pousse les fournisseurs à se différencier par :

- Les entreprises investissent massivement dans de nouvelles plateformes, de nouveaux réactifs et de nouveaux instruments pour les tests à haut débit et les diagnostics spécialisés.

- Les fournisseurs proposent des solutions complètes, allant de la logistique de prélèvement d'échantillons et des services à domicile aux plateformes d'analyse de données avancées et de consultation médicale.

- Face à des réglementations strictes, les laboratoires rivalisent pour maintenir des normes élevées (par exemple, l'accréditation CAP, NABL) afin de garantir des résultats fiables et dignes de confiance.

Opportunités et initiatives stratégiques

- Priorité aux plateformes sociales et numériques : les laboratoires tirent parti des plateformes numériques pour offrir des services pratiques tels que la réservation de tests en ligne, la planification des prélèvements à domicile et la livraison électronique des rapports, améliorant ainsi l’expérience globale du patient.

- Partenariats stratégiques : Les grands acteurs collaborent avec des start-ups spécialisées dans le diagnostic moléculaire et l’IA, ou les acquièrent, afin d’intégrer des capacités de pointe en matière de tests génétiques et d’interprétation des données dans leurs portefeuilles de services.

- Expansion sur les marchés émergents : les chaînes de diagnostic développent activement leur présence physique et numérique dans des régions à forte croissance comme l’Asie-Pacifique et le Moyen-Orient afin de tirer profit de la demande croissante de soins de santé de qualité.

Les principales entreprises opérant sur le marché des laboratoires de diagnostic sont :

- Quest Diagnostics Incorporated

- Eurofins Scientifique

- Société de portefeuille de Laboratory Corporation of America

- Laboratoires Exact Sciences LLC

- SYNLAB International GmbH

- Sonic Healthcare Limited

- Laboratoires DASA

- Diagnostics Kingmed

- Healius Limited

Avertissement : Les entreprises mentionnées ci-dessus ne sont classées dans aucun ordre particulier.

Actualités et développements récents du marché des laboratoires de diagnostic

- Par exemple, le 20 novembre 2025, Abbott et Exact Sciences ont annoncé la signature d'un accord définitif portant sur l'acquisition d'Exact Sciences par Abbott. Cette acquisition permettra à Abbott de pénétrer et de devenir un acteur majeur du secteur en forte croissance du diagnostic du cancer, et ainsi de bénéficier à des millions de personnes supplémentaires. Aux termes de cet accord, les actionnaires d'Exact Sciences recevront 105 dollars par action ordinaire, ce qui représente une valeur totale des capitaux propres d'environ 21 milliards de dollars.

- Le 23 septembre 2025, Quest Diagnostics et Epic ont annoncé une collaboration inédite visant à simplifier et à améliorer l'expérience des prestataires de soins de santé et des patients qui font appel à Quest pour des analyses de laboratoire aux États-Unis.

Rapport sur le marché des laboratoires de diagnostic : contenu et livrables

Le rapport « Taille et prévisions du marché des laboratoires de diagnostic (2021-2034) » fournit une analyse détaillée du marché couvrant les domaines suivants :

- Taille et prévisions du marché des laboratoires de diagnostic aux niveaux mondial, régional et national pour tous les segments de marché clés couverts par le périmètre de l'étude

- Tendances du marché des laboratoires de diagnostic, ainsi que dynamique du marché, notamment les facteurs moteurs, les contraintes et les principales opportunités

- Analyse PEST et SWOT détaillée

- Analyse du marché des laboratoires de diagnostic couvrant les principales tendances du marché, le cadre mondial et régional, les principaux acteurs, les réglementations et les développements récents du marché

- Analyse du paysage sectoriel et de la concurrence, incluant la concentration du marché, une analyse par carte thermique, les principaux acteurs et les développements récents du marché des laboratoires de diagnostic. Profils d'entreprises détaillés.

Analyste de recherche chevronnée, Mme Mrinal cumule plus de 8 ans d'expérience en veille stratégique et conseil dans le secteur des sciences de la vie. Dotée d'un esprit stratégique et d'un engagement indéfectible envers l'excellence, elle a acquis une expertise approfondie en prévision pharmaceutique, en évaluation des opportunités de marché et en élaboration de benchmarks sectoriels. Son travail consiste à fournir des informations exploitables permettant à ses clients de prendre des décisions stratégiques éclairées.

La principale force de Mme Mrinal réside dans sa capacité à traduire des données quantitatives complexes en données décisionnelles pertinentes. Son sens de l'analyse est essentiel à l'élaboration de stratégies de mise sur le marché (GTM) et à la découverte d'opportunités de croissance dans les secteurs pharmaceutique et des dispositifs médicaux. Consultante de confiance, elle s'attache constamment à rationaliser les processus et à établir les meilleures pratiques, favorisant ainsi l'innovation et l'efficacité opérationnelle de ses clients.

- Analyse complète de la taille du marché et prévisions

- Analyse détaillée de la segmentation

- Évaluation approfondie de la dynamique du marché

- Aperçus par région et par pays

- Paysage concurrentiel et analyse comparative des entreprises

- Intelligence économique stratégique

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires