Diagnostic Labs Market Outlook & Opportunities 2034

Coverage: By Lab Type (Single/Independent Laboratories, Hospital-Based Labs, Physician Office Labs); Testing Services (Physiological Function Testing, General and Clinical Testing, Esoteric Testing, Specialized Testing, Non-invasive Prenatal Testing, COVID-19 Testing); Revenue Source (Healthcare Plan Operators and Insurers, Out-of-Pocket, Public System); and Geography

- Status : Data Released

- Report Code : TIPRE00029512

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : January 27, 2026

2025 Market Size

US$ 407.68 Bn

Base year value

2034 Forecast

US$ 831.09 Bn

Projected by 2034

CAGR 2026-2034

8.24 %

Growth rate

Addressable Market

US$ 5,565.94 Bn

(2026-2034)

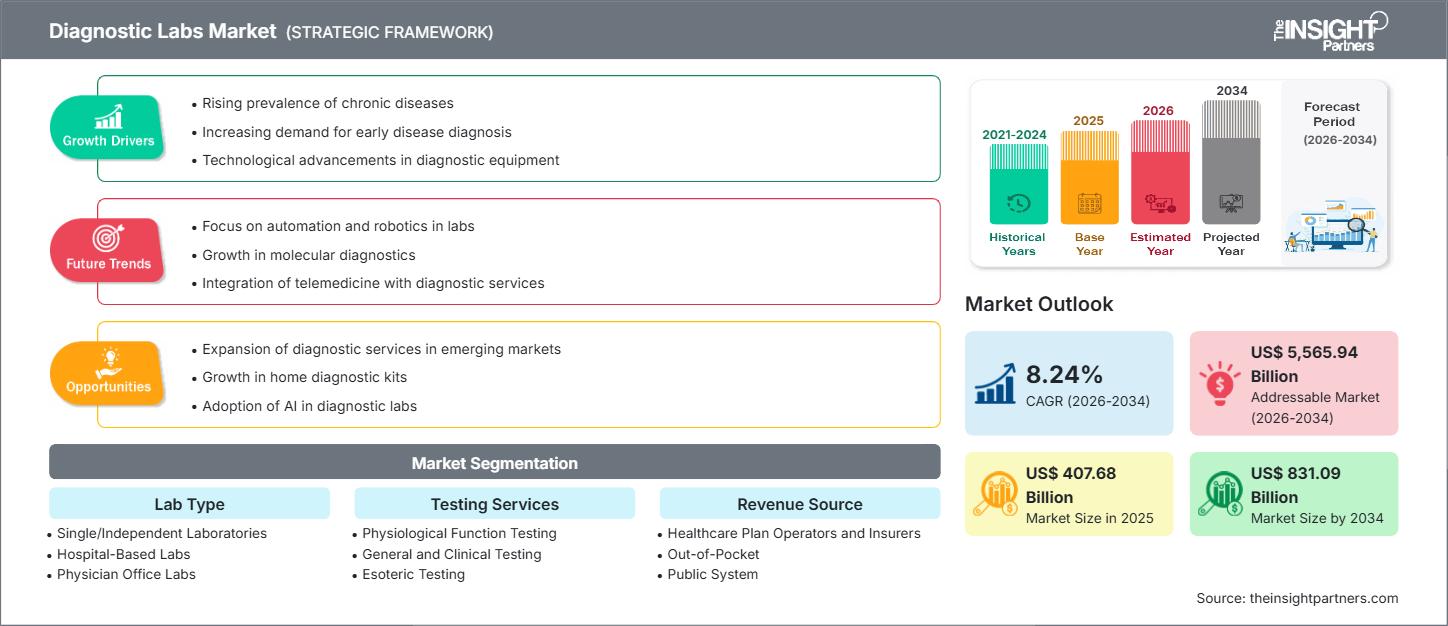

The diagnostic labs market size is expected to reach US$ 831.09 billion by 2034 from US$ 407.68 billion in 2025. The market is anticipated to register a CAGR of 8.24% during 2026–2034.

Diagnostic Labs Market Analysis

The Diagnostic Labs Market is rapidly expanding, driven by the increasing prevalence of chronic and infectious diseases globally, which necessitates frequent and accurate testing for early detection, monitoring, and treatment planning. The market is witnessing a major shift toward advanced diagnostic technologies, including molecular diagnostics, genetic testing, and point-of-care (POC) testing, which offer faster and more precise results. The growing emphasis on preventive healthcare and personalized medicine is also significantly boosting the demand for diagnostic services. Diagnostic labs are pivotal in the healthcare ecosystem, providing critical information to healthcare providers to make informed patient care decisions.

Diagnostic Labs Market Overview

A diagnostic laboratory is a specialized facility equipped with instruments, reagents, and trained professionals to perform a wide array of medical tests and analyses on patient samples to aid in the diagnosis, management, and prevention of various health conditions. The implementation of advanced technologies, including automation and the integration of Artificial Intelligence (AI) and Machine Learning (ML), is revolutionizing diagnostic processes by enhancing accuracy, efficiency, and data interpretation. Key trends include the growth of decentralized testing, the expansion of home sample collection, and the increasing integration of diagnostic services with telehealth platforms, all aimed at improving accessibility and patient convenience. Regulatory compliance and ensuring high-quality standards are crucial factors shaping the market's operations.

Market Research Highlights

- Global market for Diagnostic Labs was valued at US$ 407.68 Billion in 2025

- Annual market size is expected to reach US$ 831.09 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 5,565.94 Billion

- Market is anticipated to register a CAGR of 8.24% during the forecast period

- The United States represents a key market, supported by Rising prevalence of chronic diseases, Increasing demand for early disease diagnosis, Technological advancements in diagnostic equipment, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Expansion of diagnostic services in emerging markets, Growth in home diagnostic kits, Adoption of AI in diagnostic labs are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Quest Diagnostics Incorporated, Eurofins Scientific, Laboratory Corporation of America Holdings, Exact Sciences Laboratories LLC, SYNLAB International GmbH, Sonic Healthcare Limited, DASA Labs, Kingmed Diagnostics, Healius Limited, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Diagnostic Labs Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Diagnostic Labs Market Drivers and Opportunities

Market Drivers:

- Increasing Prevalence of Chronic and Infectious Diseases: The rising global burden of chronic conditions like diabetes, cardiovascular disorders, and cancer, along with the ongoing need for infectious disease monitoring, drives the demand for frequent and specialized diagnostic testing.

- Technological Advancements in Diagnostic Equipment: Innovations such as Next-Generation Sequencing (NGS), advanced imaging techniques, and highly automated clinical chemistry/immunoassay analyzers contribute to faster and more accurate diagnoses, fueling market adoption.

- Growing Focus on Preventive Healthcare: Increasing awareness among the population about the value of routine health check-ups and early disease screening is boosting the volume of tests conducted, shifting the focus from 'sick care' to 'wellness care.

Market Opportunities:

- Integration of Digital and AI-Enhanced Diagnostics: The use of AI and machine learning for analyzing complex data (e.g., in radiology and pathology) can improve efficiency and aid in the interpretation of results, offering significant opportunities for innovation and growth.

- Growth of Point-of-Care (POC) Testing and Decentralized Healthcare: The shift towards decentralized models, facilitated by easy-to-use, rapid POC devices (like glucose monitors and infectious disease tests), allows for faster clinical decision-making and expands testing into home-care settings and physician offices.

- Personalized Medicine and Genetic Testing: The rising demand for personalized and precision medicine is accelerating the need for advanced molecular diagnostics and genetic testing (like Laboratory Developed Tests - LDTs) to tailor treatments to individual patient profiles.

Diagnostic Labs Market Report Segmentation Analysis

The Diagnostic Labs Market is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends.

By Lab Type:

- Single/Independent Laboratories

- Hospital-Based Labs

- Physician Office Labs

By Testing Services:

- Physiological Function Testing

- General and Clinical Testing

- Esoteric Testing

- Specialized Testing

- Non-invasive Prenatal Testing

- COVID-19 Testing

By Revenue Source:

- Healthcare Plan Operators and Insurers

- Out-of-Pocket

- Public System

By Geography:

- North America

- Europe

- Asia-Pacific

- South & Central America

- Middle East & Africa

Diagnostic Labs Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 407.68 Billion |

| Market Size by 2034 | US$ 831.09 Billion |

| Global CAGR (2026 - 2034) | 8.24% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Lab Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Diagnostic Labs Market Players Density: Understanding Its Impact on Business Dynamics

The Diagnostic Labs Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Diagnostic Labs Market Share Analysis by Geography

North America holds a significant market share, driven by its well-established healthcare infrastructure, high healthcare expenditure, and the early adoption of advanced diagnostic technologies and personalized medicine.

The market shows a varied growth trajectory across regions due to factors such as regulatory frameworks, technological maturity, and disease burden.

-

North America

- Market Share: Holds the largest market share, benefiting from a robust R&D infrastructure and the presence of leading diagnostics and medtech companies.

- Key Drivers: High adoption of advanced technologies, strong focus on preventive health and personalized medicine, and supportive regulatory landscape (e.g., FDA approvals).

- Trends: Increased use of automation, AI integration in imaging and pathology, and growth in direct-to-consumer (DTC) genetic testing.

-

Europe

- Market Share: Holds a substantial share, driven by a well-developed healthcare system and government initiatives for public health.

- Key Drivers: High prevalence of chronic and age-related diseases, and strong regulatory standards ensuring test quality and reliability.

- Trends: Growing investment in advanced molecular diagnostics and adoption of decentralized POC testing solutions to manage chronic diseases.

-

Asia Pacific

- Market Share: The fastest-growing regional market, driven by rapid urbanization, improving healthcare access, and a large population size.

- Key Drivers: Government-backed healthcare infrastructure development, rising health awareness, and increasing investment by global diagnostic companies in emerging economies like China and India.

- Trends: Expansion of diagnostic chain networks into Tier 2 and Tier 3 cities, adoption of affordable and localized diagnostic solutions, and rapid growth in home sample collection services.

-

South and Central America

- Market Share: Emerging region with growing demand, but often faces challenges related to infrastructure and public healthcare spending.

- Key Drivers: Increased awareness of infectious and non-communicable diseases, and gradual modernization of clinical laboratory facilities.

- Trends: Expansion of affordable, cloud-based laboratory information management systems (LIMS) and uptake of basic diagnostic services.

-

Middle East and Africa

- Market Share: Emerging market with strong growth potential, led by digital transformation and healthcare spending in the Gulf Cooperation Council (GCC) countries and South Africa.

- Key Drivers: Major national digital health and AI strategies, increasing private sector investment in healthcare facilities, and a rising need for infectious disease diagnostics.

- Trends: Rapid integration of AI chatbots and community management systems for patient engagement and logistics, and focus on establishing accredited, high-quality diagnostic centers.

Diagnostic Labs Market Players Density: Understanding Its Impact on Business Dynamics

The Diagnostic Labs Market features a blend of large, integrated global diagnostic corporations, medical device manufacturers, specialized molecular/genetic testing firms, and powerful regional and national laboratory chains. Intense competition is driven by the need for speed, accuracy, and cost-efficiency.

The competitive landscape is driving vendors to differentiate through:

- Companies are investing heavily in new platforms, reagents, and instruments for high-throughput testing and specialized diagnostics.

- Vendors are offering end-to-end solutions, from sample collection logistics and at-home services to advanced data analytics and physician consultation platforms.

- With stringent regulations, laboratories are competing to maintain high standards (e.g., CAP, NABL accreditation) to ensure reliable and trusted results.

Opportunities and Strategic Moves

- Focus on Social and Digital Platforms: Laboratories are leveraging digital platforms to offer convenient services like online test booking, home collection scheduling, and electronic report delivery, improving the overall patient experience.

- Strategic Partnerships: Large players are collaborating with or acquiring specialized molecular diagnostics and AI-focused startups to integrate cutting-edge genetic testing and data interpretation capabilities into their service portfolios.

- Expansion into Emerging Markets: Diagnostic chains are actively expanding their physical and digital footprints in high-growth regions like Asia-Pacific and the Middle East to capitalize on rising demand for quality healthcare.

Major Companies Operating in the Diagnostic Labs Market Are:

- Quest Diagnostics Incorporated

- Eurofins Scientific

- Laboratory Corporation of America Holdings

- Exact Sciences Laboratories LLC

- SYNLAB International GmbH

- Sonic Healthcare Limited

- DASA Labs

- Kingmed Diagnostics

- Healius Limited

Disclaimer: The companies listed above are not ranked in any particular order.

Diagnostic Labs Market News and Recent Developments

- For instance, on November 20, 2025, Abbott and Exact Sciences announced a definitive agreement for Abbott to acquire Exact Sciences, which will enable it to enter and lead in fast-growing cancer diagnostics segments, serving millions more people. Under the terms of the agreement, Exact Sciences shareholders will receive $105 per common share, representing a total equity value of approximately $21 billion.

- On September 23, 2025, Quest Diagnostics and Epic announced a first-of-its-kind collaboration designed to streamline and improve experiences for healthcare providers and patients who engage Quest for laboratory testing in the United States.

Diagnostic Labs Market Report Coverage and Deliverables

The "Diagnostic Labs Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Diagnostic Labs Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Diagnostic Labs Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Diagnostic Labs Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Diagnostic Labs Market. Detailed company profiles.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends