Taille, part de marché et demande du marché des implants de hanche d'ici 2034

Taille et prévisions du marché des implants de hanche (2021-2034), parts de marché mondiales et régionales, tendances et analyse des opportunités de croissance : ce rapport couvre les segments suivants : par type de produit (prothèse totale de hanche, prothèse partielle de hanche, resurfaçage de la hanche et reprise d’implant de hanche), par type de matériau (métal sur polyéthylène, céramique sur céramique, céramique sur métal, céramique sur polyéthylène et autres), par utilisateur final (hôpitaux, cliniques orthopédiques, centres de chirurgie ambulatoire et autres) et par zone géographique (Amérique du Nord, Europe, Asie-Pacifique, Moyen-Orient et Afrique, Amérique du Sud et centrale).

- Statut : Publié

- Code du rapport : TIPMD00002030

- Catégorie : Sciences de la vie

- Nombre de pages : 252

- Formats de rapport disponibles :

- Date de dernière mise à jour : May 29, 2026

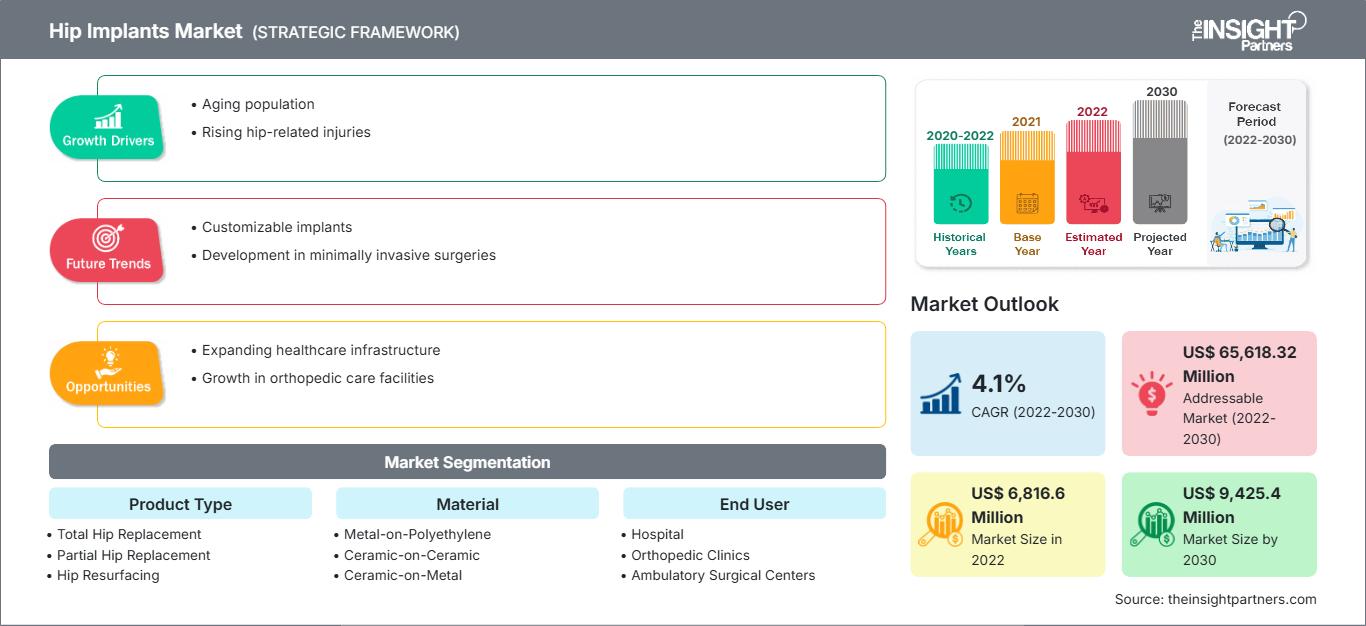

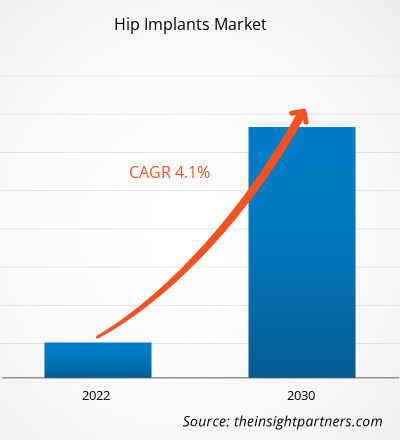

Le marché des implants de hanche devrait atteindre 12,04 milliards de dollars américains d'ici 2034, contre 8,27 milliards de dollars américains en 2025. Ce marché devrait enregistrer un TCAC de 4,3 % entre 2026 et 2034.

Analyse du marché des implants de hanche

Le marché mondial des implants de hanche est stimulé par l'augmentation des cas d'arthrose et de fractures de la hanche, ainsi que par le vieillissement de la population. L'épidémie croissante d'obésité, associée aux troubles articulaires liés au mode de vie, engendre une demande accrue de prothèses de hanche. Le développement de matériaux en céramique et en titane pour les implants offre une meilleure longévité et de meilleurs résultats pour les patients. De plus en plus de personnes optent pour des méthodes chirurgicales mini-invasives, et les techniques chirurgicales s'améliorent. Les pays émergents connaissent une hausse des coûts de santé et un meilleur accès aux services orthopédiques.

Aperçu du marché des implants de hanche

Le marché mondial des implants de hanche connaît une expansion soutenue, portée par la demande croissante de solutions orthopédiques de pointe visant à restaurer la mobilité et à améliorer la qualité de vie. Le vieillissement de la population, conjugué à la prévalence croissante des maladies osseuses dégénératives et des traumatismes, entraîne une augmentation du nombre d'interventions chirurgicales. Le développement de dispositifs médicaux personnalisés et imprimés en 3D pour la conception d'implants permet une meilleure précision et une durée de vie opérationnelle prolongée. Le développement des infrastructures de santé dans les régions émergentes offre de meilleures perspectives d'accès aux soins pour les patients. L'adoption des procédures d'implantation de prothèse de hanche dans les hôpitaux et les centres orthopédiques continue de progresser, grâce à une meilleure information du public sur les avantages du remplacement articulaire et à l'amélioration des systèmes de remboursement dans certains pays.

Personnalisez ce rapport selon vos besoins.

Bénéficiez d'une PERSONNALISATION GRATUITEMarché des implants de hanche : Perspectives stratégiques

-

Découvrez les principales tendances du marché présentées dans ce rapport.Cet échantillon GRATUIT comprendra une analyse de données, allant des tendances du marché aux estimations et prévisions.

Facteurs de croissance et opportunités du marché des implants de hanche

Facteurs de marché :

- Population vieillissante croissante : L’augmentation de la population âgée entraîne une demande accrue de chirurgies de remplacement de la hanche, car les personnes âgées ont plus de risques de développer une dégénérescence articulaire, des fractures et des troubles liés à la mobilité.

- Prévalence croissante de l'arthrose : L'incidence croissante de l'arthrose entraîne une demande accrue d'implants de hanche, car les patients ont besoin de traitements chirurgicaux pour soulager leur douleur et retrouver la fonctionnalité de leurs articulations.

- Augmentation des traumatismes, de l'obésité et des blessures liées au mode de vie : la hausse des accidents de la route, conjuguée à l'augmentation des taux d'obésité et à la prévalence croissante des modes de vie sédentaires, entraîne des lésions plus graves de l'articulation de la hanche, ce qui crée un besoin accru d'opérations chirurgicales avec implants.

Opportunités de marché :

- Expansion sur les marchés émergents : Les économies émergentes présentent un potentiel de croissance prometteur car leurs systèmes de santé se développent et les populations ont un meilleur accès à des solutions d’implants de hanche abordables et de pointe.

- Implants personnalisés et imprimés en 3D : Le développement de la technologie d’impression 3D permet la création d’implants de hanche personnalisés, qui correspondent aux besoins physiques spécifiques de chaque patient, ce qui conduit à de meilleurs résultats chirurgicaux et à une utilisation accrue de solutions orthopédiques précises.

- Évolution vers les soins ambulatoires : La tendance croissante des patients à opter pour des interventions en ambulatoire entraîne une réduction de la durée des hospitalisations, ce qui se traduit par une diminution des dépenses de santé et une utilisation accrue des opérations de pose de prothèses de hanche mini-invasives dans les centres de soins ambulatoires.

Analyse de segmentation du rapport sur le marché des implants de hanche

Le marché des implants de hanche est segmenté en différentes catégories afin de mieux comprendre son fonctionnement, son potentiel de croissance et ses tendances actuelles. Voici l'approche de segmentation standard utilisée dans les rapports sectoriels :

Par type de produit :

- Prothèse totale de hanche : L’arthrose sévère et les fractures nécessitant une arthroplastie complète constituent la principale indication de cette intervention. Le vieillissement de la population, conjugué à une meilleure durée de vie des implants, explique l’adoption croissante de cette procédure.

- Prothèse partielle de hanche : La prothèse partielle de hanche constitue un traitement efficace pour les patients âgés souffrant d’une fracture du col du fémur. Cette intervention présente plusieurs avantages : durée opératoire réduite, récupération rapide et minimisation des risques de complications chirurgicales.

- Relissage de la hanche : Les patients jeunes et actifs optent pour le relissage de la hanche car cette intervention préserve la majeure partie de leur structure osseuse et leur permet de mieux bouger, grâce au développement des systèmes d’implants métal sur métal.

- Révision de prothèse de hanche : La demande de révision de prothèses de hanche continue d’augmenter car les prothèses primaires présentent des taux d’échec plus élevés, et l’allongement de l’espérance de vie entraîne un besoin accru d’interventions chirurgicales pour rétablir la fonction et la stabilité articulaires.

Par type de matériau :

- Métal sur polyéthylène

- Céramique sur céramique

- Céramique sur métal

- Céramique sur polyéthylène

- Autres

Par les utilisateurs finaux :

- Hôpital

- Cliniques orthopédiques

- Centres de chirurgie ambulatoire

- Autres

Par géographie :

- Amérique du Nord

- Europe

- Asie-Pacifique

- Amérique du Sud et centrale

- Moyen-Orient et Afrique

Portée du rapport sur le marché des implants de hanche

| Attribut du rapport | Détails |

|---|---|

| Taille du marché en 2025 | 8,27 milliards de dollars américains |

| Taille du marché d'ici 2034 | 12,04 milliards de dollars américains |

| TCAC mondial (2026 - 2034) | 4,3% |

| Données historiques | 2021-2024 |

| Période de prévision | 2026-2034 |

| Segments couverts |

Par type de produit

|

| Régions et pays couverts |

Amérique du Nord

|

| Leaders du marché et profils d'entreprises clés |

|

Densité des acteurs du marché des implants de hanche : comprendre son impact sur la dynamique commerciale

Le marché des implants de hanche connaît une croissance rapide, portée par une demande croissante des utilisateurs finaux, elle-même alimentée par l'évolution des préférences des consommateurs, les progrès technologiques et une meilleure connaissance des avantages du produit. Face à cette demande grandissante, les entreprises diversifient leur offre, innovent pour répondre aux besoins des consommateurs et tirent parti des tendances émergentes, contribuant ainsi à la croissance du marché.

Analyse des parts de marché des implants de hanche par zone géographique

Le marché connaît la croissance la plus rapide en Asie-Pacifique. Les marchés émergents d'Amérique du Sud, du Moyen-Orient et d'Afrique offrent des opportunités inexploitées aux fournisseurs d'implants de hanche pour se développer.

La croissance du marché des implants de hanche varie selon les régions en raison du vieillissement de la population, de l'amélioration des infrastructures de santé, de l'augmentation du nombre d'interventions chirurgicales et de l'essor du tourisme médical. Voici un résumé des parts de marché et des tendances par région :

1. Amérique du Nord

- Part de marché : Détient une part importante du marché mondial

- Principaux facteurs de croissance : L’Amérique du Nord est le principal moteur de croissance grâce à son infrastructure de santé avancée, à des taux de chirurgie élevés et à une forte adoption des technologies innovantes en matière d’implants de hanche.

- Tendances : Adoption croissante de la prothèse de hanche assistée par robot, évolution de plus en plus vers les centres de chirurgie ambulatoire et utilisation accrue d'implants intelligents dotés de capacités de surveillance en temps réel.

2. Europe

- Part de marché : Part de marché substantielle

- Principaux facteurs : vieillissement croissant de la population, systèmes de santé publique performants et forte sensibilisation aux traitements orthopédiques.

- Tendances : Développement de matériaux implantaires biocompatibles et durables, innovation réglementaire plus stricte (règlement européen relatif aux dispositifs médicaux) et utilisation croissante de registres orthopédiques basés sur les données pour l'optimisation des traitements.

3. Asie-Pacifique

- Part de marché : Région à la croissance la plus rapide, avec une part de marché en augmentation annuelle.

- Principaux facteurs : Augmentation de la population gériatrique, amélioration de l'accès aux soins de santé, croissance du tourisme médical et augmentation des interventions orthopédiques.

- Tendances : Adoption rapide d'implants économiques, expansion de la production locale, augmentation des interventions chirurgicales mini-invasives et pénétration croissante des solutions orthopédiques numériques dans les économies émergentes.

4. Amérique du Sud et centrale

- Part de marché : Part de marché en croissance constante

- Principaux facteurs : Amélioration des infrastructures de santé, augmentation des cas de traumatismes et accessibilité financière croissante des interventions de remplacement de la hanche dans les régions urbaines.

- Tendances : Croissance des investissements dans les hôpitaux privés, disponibilité accrue d'implants abordables, expansion des procédures de soins traumatologiques et adoption progressive des techniques chirurgicales avancées.

5. Moyen-Orient et Afrique

- Part de marché : Faible part de marché, en forte croissance

- Principaux facteurs : Développement des infrastructures de santé, augmentation des investissements médicaux et demande croissante de solutions chirurgicales orthopédiques de pointe.

- Tendances : essor du tourisme médical, développement de centres orthopédiques de pointe dans les pays du CCG, augmentation des dépenses publiques de santé et meilleur accès aux chirurgies implantaires dans les régions urbaines.

Forte densité de marché et concurrence

La concurrence est forte en raison de la présence d'acteurs établis tels que Zimmer Biomet Holdings Inc et Stryker Corp. Les fournisseurs régionaux et de niche contribuent également à la compétitivité du paysage concurrentiel dans toutes les régions.

Le niveau élevé de concurrence incite les entreprises à se démarquer en proposant :

- Produits et services avancés

- Respect des directives réglementaires

Opportunités et initiatives stratégiques

- Le marché des implants de hanche offre des perspectives de croissance grâce aux économies émergentes, aux technologies d'implants avancées, aux solutions personnalisées et à la demande croissante de chirurgies mini-invasives.

- Les entreprises privilégient l'innovation produit, les partenariats avec les hôpitaux, l'expansion géographique et l'adoption de la robotique et de l'impression 3D pour obtenir un avantage concurrentiel.

Autres entreprises analysées au cours de la recherche :

- Medtronic plc

- Conformis Inc.

- Globus Medical Inc.

- NuVasive Inc.

- Arthrex Inc.

- Société scientifique MicroPort

- Waldemar Link GmbH & Co. KG

- Orthofix Medical Inc.

- Medacta International SA

- Systèmes d'implants Aesculap

- Integra LifeSciences Holdings Corporation

- LimaCorporate SpA

Actualités et développements récents du marché des implants de hanche

- En octobre 2025, Zimmer Biomet Holdings, Inc., leader mondial des technologies médicales, a annoncé que la FDA (Food and Drug Administration) américaine avait accordé la désignation de dispositif révolutionnaire à son premier système de prothèse totale de hanche traité à l'iode. Il s'agit du premier produit de l'histoire de Zimmer Biomet à recevoir cette désignation.

- En décembre 2025, OrthAlign, Inc., leader mondial des technologies de navigation chirurgicale, a annoncé l'extension de sa plateforme Lantern Hip afin de proposer une approche postérieure pour les arthroplasties totales de hanche (ATH). Cette plateforme offre une utilité clinique accrue, permettant aux chirurgiens d'utiliser Lantern Hip pour toute ATH, quelle que soit leur préférence clinique concernant la position du patient (décubitus latéral ou dorsal).

Rapport sur le marché des implants de hanche : contenu et livrables

Le rapport « Taille et prévisions du marché des implants de hanche (2026-2034) » fournit une analyse détaillée du marché couvrant les domaines suivants :

- Taille et prévisions du marché des implants de hanche aux niveaux mondial, régional et national pour tous les segments de marché clés couverts par le présent document.

- Tendances du marché des implants de hanche, ainsi que dynamique du marché (facteurs moteurs, contraintes et opportunités)

- Analyse PEST et SWOT détaillée

- Analyse du marché des implants de hanche : tendances clés, cadre mondial et régional, principaux acteurs, réglementations et évolutions récentes du marché

- Analyse du paysage industriel et de la concurrence, incluant la concentration du marché, l'analyse par carte thermique, les principaux acteurs et les développements récents du marché des implants de hanche

- Profils d'entreprise détaillés

Analyste de recherche chevronnée, Mme Mrinal cumule plus de 8 ans d'expérience en veille stratégique et conseil dans le secteur des sciences de la vie. Dotée d'un esprit stratégique et d'un engagement indéfectible envers l'excellence, elle a acquis une expertise approfondie en prévision pharmaceutique, en évaluation des opportunités de marché et en élaboration de benchmarks sectoriels. Son travail consiste à fournir des informations exploitables permettant à ses clients de prendre des décisions stratégiques éclairées.

La principale force de Mme Mrinal réside dans sa capacité à traduire des données quantitatives complexes en données décisionnelles pertinentes. Son sens de l'analyse est essentiel à l'élaboration de stratégies de mise sur le marché (GTM) et à la découverte d'opportunités de croissance dans les secteurs pharmaceutique et des dispositifs médicaux. Consultante de confiance, elle s'attache constamment à rationaliser les processus et à établir les meilleures pratiques, favorisant ainsi l'innovation et l'efficacité opérationnelle de ses clients.

- Analyse complète de la taille du marché et prévisions

- Analyse détaillée de la segmentation

- Évaluation approfondie de la dynamique du marché

- Aperçus par région et par pays

- Paysage concurrentiel et analyse comparative des entreprises

- Intelligence économique stratégique

Témoignages

Le rapport sur le marché des systèmes SCADA d'Insight Partners est complet et fournit des informations précieuses sur les tendances actuelles et les prévisions. L'équipe a fait preuve d'un grand professionnalisme, d'une grande réactivité et d'un grand soutien tout au long du projet. Nous sommes très satisfaits et recommandons vivement leurs services.

RAN KEDEM Partenaire, Reali Technologies LTDJ'ai demandé un rapport sur un marché logiciel très spécifique et l'équipe l'a produit en quelques jours. Les informations étaient très pertinentes et bien présentées. J'ai ensuite demandé des modifications et des ajouts au rapport. L'équipe a de nouveau été très réactive et j'ai reçu le rapport final en moins d'une semaine.

JEAN-HERVÉ JENN Président, Future AnalyticaNous avons collaboré avec The Insight Partners pour une importante étude de marché et des prévisions. Ils nous ont fourni une vision claire des opportunités et des risques, ce qui nous a aidés à élaborer nos plans. Leurs recherches étaient faciles à utiliser et basées sur des données solides. Elles nous ont permis de prendre des décisions éclairées et en toute confiance. Nous les recommandons vivement.

PIYUSH NAGPAL Vice-président principal, Feux de route mondiauxInsight Partners a réalisé une étude de marché pertinente et bien structurée, avec une solide expertise du domaine. Son équipe a fait preuve de professionnalisme et de réactivité tout au long du projet. Son site web convivial a facilité l'accès aux rapports sectoriels. Nous recommandons vivement ses services d'études fiables et de haute qualité.

YUKIHIKO ADACHI PDG, Bleu profond, LLC.C'est la première fois que j'achète une étude de marché auprès de The Insight Partners. J'étais un peu hésitant au début, mais j'ai consulté leur site web et me suis senti plus à l'aise pour prendre le risque d'acheter une étude de marché. Je suis entièrement satisfait de la qualité du rapport et du service client. J'avais plusieurs questions et commentaires concernant le rapport initial, mais après quelques échanges par e-mail avec leur analyste, je pense avoir obtenu un rapport qui pourra alimenter notre processus de planification stratégique. Merci beaucoup pour votre temps et pour avoir rendu cette expérience positive. Je recommanderai sans hésiter vos services et vous serez mon premier contact lorsque nous aurons besoin de données de marché supplémentaires.

JOHN SUZUKI Président-directeur général, administrateur du conseil d'administration, BK TechnologiesJe tiens à vous remercier pour votre soutien et le professionnalisme dont vous avez fait preuve lors du traitement de ma demande d'informations concernant le marché des dispositifs de diagnostic in vitro (DIV) pour les maladies infectieuses au Nigéria. J'apprécie votre patience, vos conseils et votre volonté d'offrir une réduction, ce qui nous a finalement permis de conclure un accord. Je me réjouis de collaborer à nouveau avec The Insight Partners, grâce à l'impression que vous m'avez laissée suite à cette première rencontre.

DR CHIJIOKE DIRECTEUR GÉNÉRAL D'ONYIA, PineCrest Healthcare Ltd.Raison d'acheter

- Prise de décision éclairée

- Compréhension de la dynamique du marché

- Analyse concurrentielle

- Connaissances clients

- Prévisions de marché

- Atténuation des risques

- Planification stratégique

- Justification des investissements

- Identification des marchés émergents

- Amélioration des stratégies marketing

- Amélioration de l'efficacité opérationnelle

- Alignement sur les tendances réglementaires