Dimensioni, quota e previsioni del mercato della sicurezza cloud entro il 2034

Dimensioni e previsioni del mercato della sicurezza cloud (2021-2034), quota globale e regionale, trend e analisi delle opportunità di crescita. Copertura del report: per modello di servizio [Software-as-a-Service (SaaS), Platform-as-a-Service (PaaS) e Infrastructure-as-a-Service (IaaS)], modello di implementazione (cloud pubblico, cloud privato e cloud ibrido), dimensione aziendale (grandi imprese e piccole e medie imprese), tipo di soluzione (sicurezza e-mail e web, gestione delle identità e degli accessi cloud, prevenzione della perdita di dati, sistema di rilevamento/prevenzione delle intrusioni, gestione delle informazioni e degli eventi di sicurezza e altro) e settori verticali [settore bancario, finanziario e assicurativo (BFSI); IT e telecomunicazioni; energia e servizi di pubblica utilità; settore pubblico e governativo; sanità; industria manifatturiera; e altro].

- Stato : Dati rilasciati

- Codice del report : TIPTE100000306

- Categoria : Tecnologia, media e telecomunicazioni

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : March 17, 2026

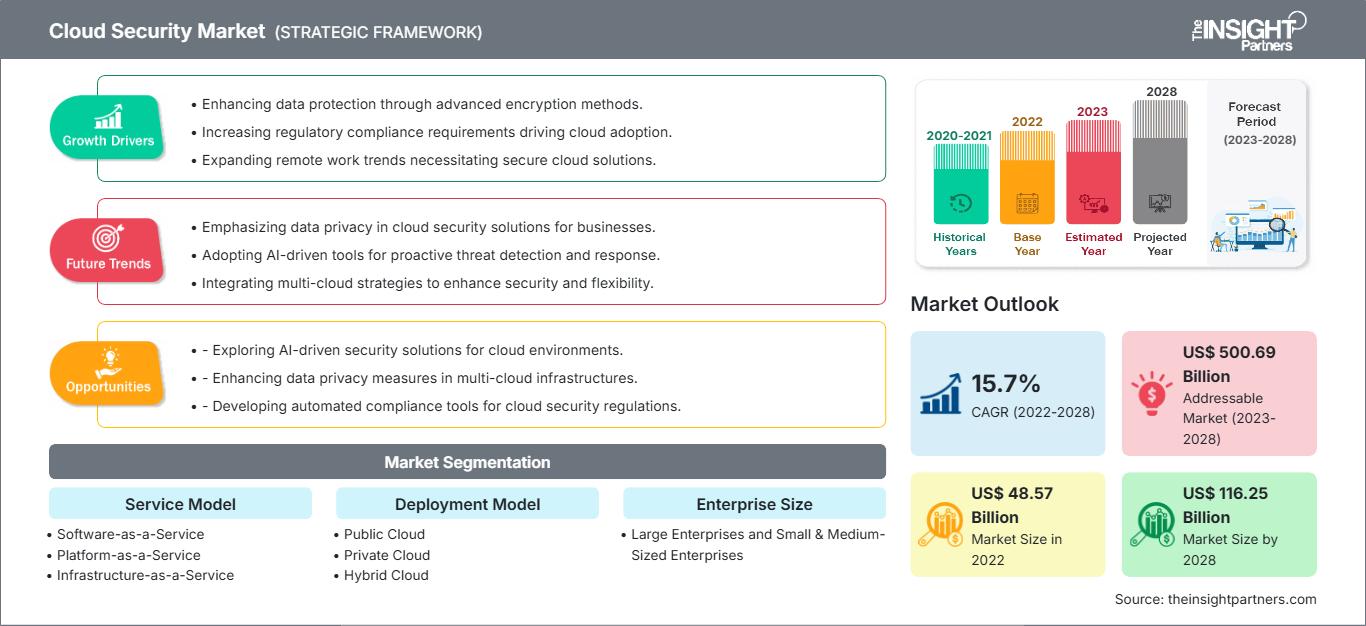

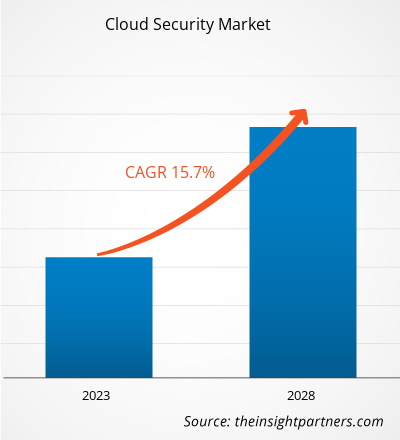

Si prevede che il mercato globale della sicurezza cloud raggiungerà un valore di 156,18 miliardi di dollari entro il 2034, rispetto ai 40,7 miliardi di dollari del 2025. Si prevede inoltre che il mercato registrerà un tasso di crescita annuo composto (CAGR) del 15,34% nel periodo di previsione 2026-2034.

Tra le principali dinamiche di mercato si annoverano l'aumento esponenziale dei sofisticati attacchi informatici, la rapida migrazione dei carichi di lavoro critici verso ambienti multi-cloud e la crescente severità delle normative globali sulla privacy dei dati, come il GDPR e il CCPA. Inoltre, si prevede che il mercato trarrà vantaggio dall'integrazione dell'Intelligenza Artificiale (IA) e dell'Apprendimento Automatico (ML) nel rilevamento delle minacce, dalla proliferazione di culture di lavoro a distanza che richiedono un accesso sicuro e dalla crescente adozione dell'architettura Zero Trust in diversi settori industriali.

Analisi del mercato della sicurezza cloud

L'analisi del mercato della sicurezza cloud indica un cambiamento fondamentale, che passa da una difesa reattiva basata sul perimetro a modelli di sicurezza proattivi e incentrati sui dati. Con la transizione delle organizzazioni verso infrastrutture cloud-native, le tendenze di approvvigionamento mostrano un significativo spostamento verso piattaforme integrate che offrono una visibilità unificata su ambienti frammentati. Stanno emergendo opportunità strategiche in ambito Security-as-Code e DevSecOps, dove l'integrazione della sicurezza direttamente nel ciclo di vita dello sviluppo del software offre un chiaro vantaggio competitivo in termini di velocità e resilienza. L'analisi evidenzia inoltre che il successo sul mercato dipende sempre più dalla capacità di gestire i rischi di errata configurazione, la principale causa di violazioni nel cloud, e dall'implementazione di strumenti di correzione automatizzati. La differenziazione competitiva si basa ora sulla fornitura di una protezione continua e a bassa latenza che non comprometta l'agilità e i vantaggi prestazionali per i quali i servizi cloud sono stati originariamente adottati.

Panoramica del mercato della sicurezza cloud

La sicurezza del cloud si sta evolvendo da requisito IT supplementare a pilastro fondamentale della moderna strategia aziendale digitale. Storicamente incentrato su firewall e crittografia di base, il mercato ora comprende un vasto ecosistema di Cloud Access Security Broker (CASB), Cloud Workload Protection Platform (CWPP) e Posture Management (CSPM). Sebbene le grandi imprese siano state le prime ad adottare queste tecnologie a causa dell'elevato valore dei loro dati, il mercato sta assistendo a una rapida espansione nel segmento delle PMI, alimentata dalla disponibilità di modelli di sicurezza scalabili basati su abbonamento. Sia i colossi affermati della cybersecurity che le agili startup cloud-native si contendono il primato affrontando la complessità degli ecosistemi ibridi e multi-cloud. Ad esempio, il mercato statunitense rappresenta il mercato della sicurezza cloud più grande e maturo a livello globale. Guidato da un'elevata concentrazione di innovatori tecnologici e da rigorosi standard di conformità federali, il panorama statunitense privilegia l'intelligence avanzata sulle minacce e i framework Zero Trust. I massicci investimenti nella trasformazione digitale nei settori pubblico e privato continuano a sostenere la domanda di infrastrutture di sicurezza nazionali.

Personalizza questo report in base alle tue esigenze

Ottieni la PERSONALIZZAZIONE GRATUITAMercato della sicurezza cloud: approfondimenti strategici

-

Scopri le principali tendenze di mercato di questo report.Questo campione GRATUITO includerà un'analisi dei dati, che spazierà dalle tendenze di mercato alle stime e alle previsioni.

Fattori trainanti e opportunità del mercato della sicurezza cloud

Fattori trainanti del mercato:

- La crescente sofisticazione delle minacce informatiche: la frequenza sempre maggiore di ransomware, violazioni di dati e minacce persistenti avanzate (APT) che prendono di mira i dati archiviati nel cloud è uno dei fattori principali. Poiché gli aggressori sfruttano l'intelligenza artificiale per individuare le vulnerabilità, le organizzazioni sono costrette a investire in soluzioni di sicurezza cloud avanzate per proteggere le informazioni aziendali e dei clienti sensibili.

- Rapida adozione di strategie multi-cloud e ibride: le aziende utilizzano sempre più spesso diversi fornitori di servizi cloud per evitare la dipendenza da un singolo fornitore e migliorare l'affidabilità. Questa complessità crea la necessità di piattaforme di sicurezza unificate in grado di garantire l'applicazione coerente delle policy e la visibilità su ambienti cloud eterogenei.

- Requisiti normativi e di conformità più rigorosi: i governi di tutto il mondo stanno introducendo leggi più severe in materia di protezione dei dati. La conformità a normative come l'HIPAA nel settore sanitario o il PCI DSS in quello finanziario richiede solide misure di sicurezza per il cloud, il che comporta investimenti continui in strumenti di audit, crittografia e controllo degli accessi.

Opportunità di mercato:

- Integrazione di IA e automazione nella ricerca delle minacce: per i fornitori di sicurezza si apre un'importante opportunità di sviluppare strumenti basati sull'IA in grado di prevedere e neutralizzare le minacce in tempo reale, senza intervento umano. La risposta automatizzata agli incidenti riduce i tempi di permanenza delle minacce e minimizza i potenziali danni derivanti da una violazione.

- Espansione nei servizi di sicurezza cloud per le PMI: le piccole e medie imprese stanno migrando sempre più verso il cloud, ma spesso non dispongono delle competenze interne necessarie per garantirne la sicurezza. Offrire pacchetti di sicurezza cloud semplificati e gestiti, adattati ai vincoli di budget e tecnici delle PMI, rappresenta un'enorme opportunità di crescita ancora inesplorata.

- Focus sulla sicurezza dell'edge computing: con la crescente diffusione dell'elaborazione decentralizzata e dell'Internet delle cose (IoT), la protezione dei confini del cloud diventa fondamentale. Lo sviluppo di soluzioni di sicurezza specializzate per i data center edge e i dispositivi connessi rappresenta una frontiera strategica per gli operatori del mercato.

Analisi di segmentazione del mercato della sicurezza cloud

La quota di mercato della sicurezza cloud viene analizzata in diversi segmenti per fornire una comprensione più chiara della sua struttura, del potenziale di crescita e delle tendenze emergenti. Di seguito è riportato l'approccio di segmentazione standard utilizzato nella maggior parte dei report di settore:

In base al modello di servizio:

- Software-as-a-Service (SaaS): un segmento dominante e altamente accessibile in cui la sicurezza viene fornita tramite il cloud, rivolgendosi alle organizzazioni che cercano una protezione scalabile e a bassa manutenzione per le proprie applicazioni web.

- Platform-as-a-Service (PaaS): si concentra sulla sicurezza dell'ambiente di sviluppo e distribuzione, garantendo che il middleware e gli strumenti utilizzati dagli sviluppatori siano protetti da vulnerabilità esterne e interne.

- Infrastructure-as-a-Service (IaaS): si concentra sulla protezione dei componenti fondamentali del cloud, come server virtuali, storage e rete, offrendo alle organizzazioni un controllo granulare sulle proprie configurazioni di sicurezza.

In base al modello di implementazione:

- Cloud pubblico: il modello più diffuso grazie alla sua economicità, che richiede solide misure di sicurezza basate sulla responsabilità condivisa per proteggere i dati in ambienti multi-tenant.

- Cloud privato: preferito da settori altamente regolamentati come quello bancario e governativo, questo segmento si concentra su configurazioni personalizzate e ad alta sicurezza dedicate a una singola organizzazione.

- Cloud ibrido: il modello di implementazione in più rapida crescita, che richiede una perfetta integrazione della sicurezza tra l'hardware locale e le risorse del cloud pubblico.

In base alle dimensioni dell'impresa:

- Grandi imprese: attualmente, rappresentano la principale fonte di ricavi, utilizzando suite di sicurezza complete e multilivello per proteggere enormi quantità di dati a livello globale.

- Piccole e medie imprese: un segmento in forte crescita che adotta sempre più la sicurezza cloud-native come alternativa economicamente vantaggiosa alla creazione di costosi centri operativi di sicurezza in loco.

Per tipologia di soluzione:

- Sicurezza di posta elettronica e web: fondamentale per prevenire il phishing e l'ingresso di malware nel punto di attacco più comune, ovvero l'interfaccia utente.

- Gestione delle identità e degli accessi nel cloud (IAM): un elemento fondamentale che garantisce che solo gli utenti autorizzati abbiano accesso a specifiche risorse cloud, spesso tramite autenticazione a più fattori.

- Prevenzione della perdita di dati (DLP): strumenti specializzati progettati per monitorare e bloccare il trasferimento non autorizzato di informazioni sensibili al di fuori del cloud aziendale.

- Sistema di rilevamento/prevenzione delle intrusioni (IDS/IPS): soluzioni di monitoraggio attivo che identificano e neutralizzano il traffico dannoso in tempo reale.

- Sistema di gestione delle informazioni e degli eventi di sicurezza (SIEM): fornisce la registrazione e l'analisi centralizzate degli avvisi di sicurezza per identificare schemi di compromissione.

- Altri: include Cloud Security Posture Management (CSPM) e Cloud Workload Protection Platforms (CWPP).

Per settori verticali:

- Settore bancario, dei servizi finanziari e assicurativi (BFSI): leader di mercato per la spesa in sicurezza a causa dell'estrema delicatezza dei dati finanziari e della rigorosa supervisione normativa.

- IT e telecomunicazioni: aziende pioniere che integrano la sicurezza cloud per proteggere la propria infrastruttura e fornire servizi sicuri ai propri clienti.

- Energia e servizi di pubblica utilità: si concentra sulla protezione delle infrastrutture critiche e delle reti intelligenti dal sabotaggio informatico.

- Settore pubblico e governativo: dà priorità alla sovranità dei dati e alla sicurezza nazionale attraverso implementazioni cloud altamente sicure, spesso private.

- Settore sanitario: spinto dalla necessità di proteggere le cartelle cliniche dei pazienti e di rispettare le leggi sulla privacy durante la transizione verso la telemedicina.

- Produzione: adozione sempre maggiore della sicurezza cloud per proteggere la proprietà intellettuale e i sistemi IoT industriali (IIoT).

- Altri settori: includono vendita al dettaglio, istruzione e media.

Per area geografica:

- America del Nord

- Europa

- Asia Pacifico

- Sud e Centro America

- Medio Oriente e Africa

Ambito del rapporto sul mercato della sicurezza cloud

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2025 | 40,7 miliardi di dollari |

| Dimensioni del mercato entro il 2034 | 156,18 miliardi di dollari |

| Tasso di crescita annuo composto (CAGR) globale (2026-2034) | 15,34% |

| Dati storici | 2021-2024 |

| periodo di previsione | 2026-2034 |

| Segmenti trattati |

Per modello di servizio

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli attori nel mercato della sicurezza cloud: comprenderne l'impatto sulle dinamiche aziendali

Il mercato della sicurezza cloud è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi offerti dal prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

Analisi della quota di mercato della sicurezza cloud per area geografica

Si prevede che la regione Asia-Pacifico registrerà la crescita più rapida nei prossimi anni. Anche i mercati emergenti in Sud e Centro America, Medio Oriente e Africa offrono numerose opportunità di espansione per i fornitori di servizi di sicurezza di alta qualità e le aziende di servizi gestiti.

Il mercato della sicurezza cloud sta attraversando una profonda trasformazione, passando da spesa IT secondaria a fattore abilitante primario per il business. L'ondata globale di trasformazione digitale, la professionalizzazione della criminalità informatica e l'adozione di modelli di lavoro ibridi ne guidano la crescita. Di seguito una sintesi delle quote di mercato e delle tendenze per regione:

America del Nord

- Quota di mercato: detiene la quota maggiore a livello globale, grazie alla presenza di importanti hyperscaler come AWS, Microsoft e Google.

-

Fattori chiave:

- Ampia adozione di strategie "cloud-first" tra le aziende Fortune 500.

- L'elevata frequenza di attacchi informatici sofisticati rende necessaria una difesa all'avanguardia.

- Applicazione rigorosa delle normative federali e statali in materia di protezione dei dati personali.

- Tendenze: Rapida diffusione delle architetture Zero Trust e consolidamento degli strumenti di sicurezza in piattaforme unificate e accessibili alle PMI.

Europa

- Quota di mercato: Un mercato significativo caratterizzato da una forte attenzione alla sovranità dei dati e alla privacy, guidato da Regno Unito, Germania e Francia.

-

Fattori chiave:

- Il rispetto del Regolamento generale sulla protezione dei dati (GDPR) sta incentivando gli investimenti in crittografia e gestione delle identità e degli accessi (IAM).

- Forte sostegno governativo alla modernizzazione delle infrastrutture digitali e alle iniziative di cloud sovrano.

- Adozione crescente di modelli di cloud ibrido nei settori industriale e manifatturiero.

- Tendenze: Un cambiamento strategico verso l'elaborazione localizzata dei dati e la crescente domanda di soluzioni di sicurezza cloud ecocompatibili che ottimizzano l'efficienza energetica nei data center.

Asia-Pacifico

- Quota di mercato: la regione in più rapida crescita, con Cina, India e Giappone che fungono da principali motori per la spesa in infrastrutture e sicurezza cloud.

-

Fattori chiave:

- Crescita esplosiva nei mercati regionali dell'e-commerce e del fintech.

- I progetti governativi relativi alle città intelligenti e all'identità digitale richiedono una solida protezione.

- Rapida urbanizzazione e proliferazione di imprese che privilegiano i dispositivi mobili.

- Tendenze: Forte dipendenza dai Managed Security Service Providers (MSSP) a causa di una carenza locale di talenti nel settore della sicurezza informatica e di un'impennata nell'attività delle startup cloud-native.

America meridionale e centrale

- Quota di mercato: un mercato emergente con servizi finanziari in crescita in paesi come Brasile e Argentina.

-

Fattori chiave:

- Modernizzazione dei sistemi bancari e ascesa delle banche esclusivamente digitali.

- La crescente diffusione di Internet e il passaggio dai sistemi IT tradizionali on-premise al cloud.

- Cresce la consapevolezza dei rischi legati alla sicurezza informatica a seguito di diverse violazioni di dati di alto profilo a livello regionale.

- Tendenze: crescita delle società di consulenza specializzate in sicurezza informatica e introduzione di nodi cloud localizzati da parte di fornitori globali per ridurre la latenza e migliorare la sicurezza.

Medio Oriente e Africa

- Quota di mercato: Mercati in via di sviluppo in transizione verso economie digitali formalizzate, in particolare nella regione del GCC.

-

Fattori chiave:

- I programmi di visione nazionale (ad esempio, Saudi Vision 2030) stanno promuovendo ingenti investimenti nelle infrastrutture digitali.

- L'attenzione strategica si concentra sulla protezione delle risorse critiche del settore petrolifero e del gas dalla guerra cibernetica.

- Elevata domanda di servizi cloud sicuri e scalabili per supportare una popolazione giovane e tecnologicamente avanzata.

- Tendenze: Implementazione di quadri normativi nazionali in materia di cybersicurezza e attenzione allo sviluppo di capacità cloud interne per ridurre la dipendenza da fornitori esterni.

Elevata densità di mercato e concorrenza

La concorrenza si sta intensificando a causa della presenza di leader affermati come Microsoft Corporation, Amazon Web Services (AWS), Palo Alto Networks, Check Point Software Technologies e Cisco Systems. Anche esperti regionali e operatori specializzati nel cloud nativo come Zscaler, CrowdStrike e Cloudflare contribuiscono a un panorama di mercato diversificato e in rapida espansione.

Questo contesto competitivo spinge i fornitori a differenziarsi attraverso:

- Consolidamento delle piattaforme: passaggio da soluzioni puntuali a piattaforme integrate (ad esempio, SASE e CNAPP) che gestiscono l'intero ciclo di vita della sicurezza da un'unica dashboard.

- Integrazione con l'IA: utilizzo dell'IA generativa per automatizzare attività di sicurezza complesse, come la scrittura di regole firewall o l'analisi di grandi quantità di log alla ricerca di segnali, anche minimi, di una violazione.

- Framework Zero Trust: Andare oltre le VPN tradizionali per verificare ogni utente e dispositivo, indipendentemente dal fatto che si trovino all'interno o all'esterno del perimetro di rete.

- Visibilità end-to-end: fornire un'ispezione approfondita dei pacchetti e analisi comportamentali attraverso i livelli IaaS, PaaS e SaaS per eliminare i punti ciechi nel cloud.

Opportunità e mosse strategiche

- Collaborazione con i fornitori di servizi cloud su larga scala: le aziende di cybersecurity stanno stringendo sempre più alleanze strategiche con AWS e Azure per integrare i propri strumenti di sicurezza in modo nativo all'interno delle console cloud.

- Specializzazione in sicurezza per settori verticali: sviluppo di modelli di conformità specifici per i settori sanitario, finanziario e governativo, al fine di semplificare gli oneri normativi per i clienti.

Le principali aziende operanti nel mercato della sicurezza cloud sono:

- Amazon Web Services, Inc.

- Microsoft

- Google LLC

- Oracolo

- IBM Corporation

- Cisco Systems, Inc.

- Trend Micro Incorporated

- Palo Alto Networks, Inc.

- Checkpoint Software Technologies

- VMware, Inc.

Nota: le aziende elencate sopra non sono classificate in un ordine particolare.

Notizie e ultimi sviluppi sul mercato della sicurezza cloud.

- Nel settembre 2024, Check Point Software Technologies Ltd. ha annunciato di aver raggiunto un accordo per l'acquisizione di Lakera, azienda leader nella protezione nativa dell'IA per applicazioni di IA agentica. Attraverso questa acquisizione, Check Point ha stabilito un nuovo punto di riferimento nella sicurezza cloud, offrendo una suite completa di soluzioni di sicurezza end-to-end per l'IA, progettata per proteggere le aziende che stanno accelerando l'adozione di tecnologie di IA basate sul cloud.

- Nel marzo 2025, Google Cloud ha annunciato la firma di un accordo definitivo per l'acquisizione di Wiz, al fine di offrire ad aziende e governi una maggiore scelta in materia di protezione dei dati. Integrando le funzionalità di Wiz, l'azienda puntava a fornire una piattaforma completa per la sicurezza cloud, progettata per proteggere i moderni ambienti IT su infrastrutture multi-cloud.

Copertura e risultati del rapporto sul mercato della sicurezza cloud.

Il report "Dimensioni e previsioni del mercato della sicurezza cloud (2021-2034)" fornisce un'analisi dettagliata del mercato, coprendo le seguenti aree:

- Dimensioni e previsioni del mercato della sicurezza cloud a livello globale, regionale e nazionale per tutti i principali segmenti di mercato coperti dall'ambito

- Tendenze del mercato della sicurezza cloud, nonché dinamiche di mercato quali fattori trainanti, vincoli e opportunità chiave.

- Analisi PEST e SWOT dettagliata

- Analisi del mercato della sicurezza cloud, con particolare attenzione alle principali tendenze di mercato, al quadro globale e regionale, ai principali attori, alle normative e ai recenti sviluppi del mercato.

- Analisi del panorama di settore e della concorrenza, con particolare attenzione alla concentrazione del mercato, all'analisi tramite mappa di calore, ai principali operatori e agli ultimi sviluppi nel mercato della sicurezza cloud.

- Profili aziendali dettagliati

Ankita è una dinamica professionista della ricerca di mercato e della consulenza con oltre 8 anni di esperienza nei settori della tecnologia, dei media, dell'ICT, dell'elettronica e dei semiconduttori. Ha guidato e portato a termine con successo oltre 100 incarichi di consulenza e ricerca per clienti globali come Microsoft, Oracle, NEC Corporation, SAP, KPMG ed Expeditors International. Le sue competenze principali includono la valutazione del mercato, l'analisi dei dati, le previsioni, la formulazione di strategie, l'intelligence competitiva e la redazione di report.

Ankita è esperta nella gestione di cicli di progetto completi, dalla progettazione di proposte pre-vendita e discussioni con i clienti fino alla fornitura di insight fruibili post-vendita. È esperta nella gestione di team interfunzionali, nella strutturazione di moduli di ricerca complessi e nell'allineamento delle soluzioni agli obiettivi aziendali specifici del cliente. Le sue eccellenti capacità di comunicazione, leadership e presentazione le hanno permesso di fornire costantemente risultati orientati al valore in contesti di mercato in rapida evoluzione.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative