Crescita, dimensione, quota, tendenze, analisi dei principali attori del mercato Chip di apprendimento profondo e previsioni fino al 2027

Mercato dei chip per deep learning fino al 2027 - Analisi e previsioni globali per tipo di chip (GPU, ASIC, FPGA, CPU, altri); tecnologia (System-on-Chip, System-in-Package, modulo multi-chip, altri); settore verticale (media e pubblicità, BFSI, IT e telecomunicazioni, vendita al dettaglio, sanità, automotive e trasporti e altri)

- Stato : Edito

- Codice del report : TIPRE00003229

- Categoria : Elettronica e semiconduttori

- Numero di pagine : 185

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : June 13, 2024

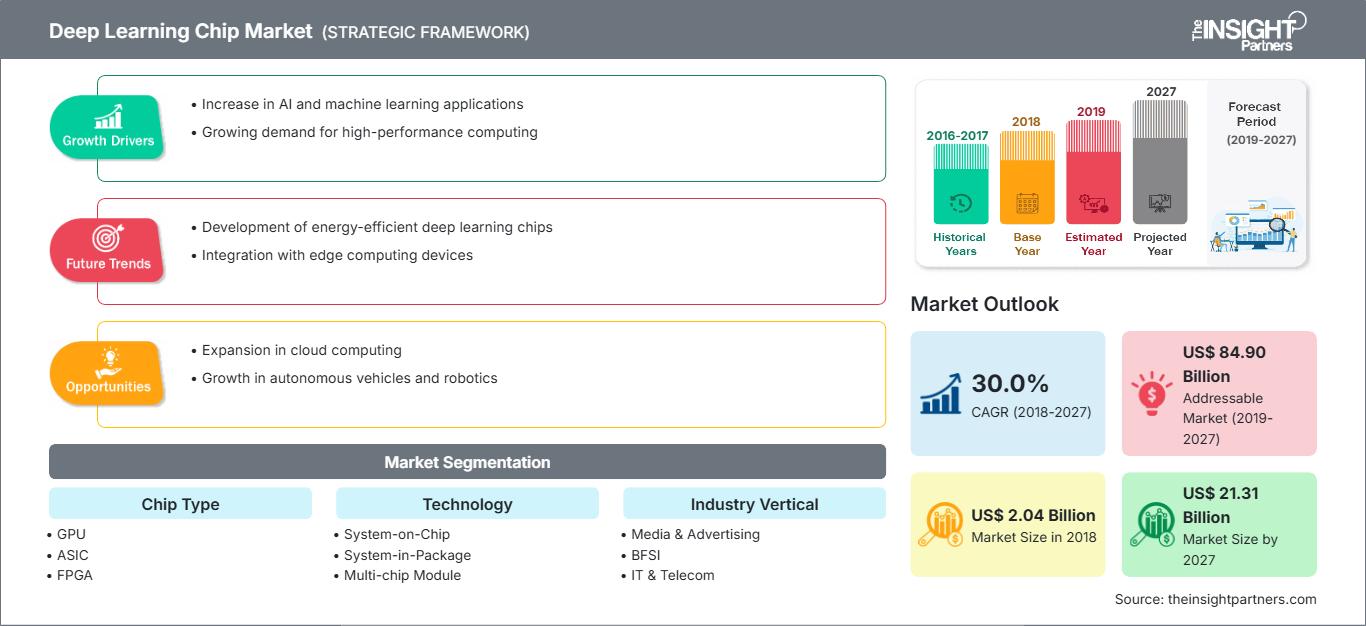

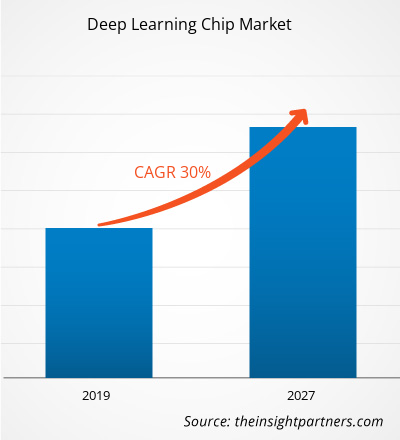

Il mercato globale dei chip per il deep learning ha raggiunto i 2,04 miliardi di dollari nel 2018 e si prevede che crescerà a un CAGR del 30,0% nel periodo di previsione 2019-2027, fino a raggiungere i 21,31 miliardi di dollari entro il 2027.

Il Nord America è leader nel mercato globale dei chip per il deep learning e si prevede che sarà il maggiore contributore di fatturato durante il periodo di previsione. Lo sviluppo di chip per il deep learning è sostenuto da investimenti su larga scala da parte dei giganti della tecnologia per sviluppare modelli a partire da un'enorme quantità di dati generati. L'ascesa del calcolo quantistico e l'implementazione di chip per il deep learning nella robotica stanno guidando la crescita del mercato dei chip per il deep learning nei paesi nordamericani.

Approfondimenti di mercato: l'importanza del calcolo quantistico contribuisce alla crescita del mercato dei chip per il deep learning

Il calcolo quantistico impiega pochi secondi per completare un calcolo che altrimenti richiederebbe più tempo. I computer quantistici rappresentano una trasformazione innovativa dell'intelligenza artificiale, dell'apprendimento automatico e dei big data. Pertanto, si prevede che l'importanza del calcolo quantistico guiderà la crescita del mercato dei chip per il deep learning. Inoltre, il calcolo quantistico è vantaggioso per diversi fattori, tra cui l'ottimizzazione del portafoglio, il rilevamento delle frodi e la gestione del rischio, nonché per le aree in cui è richiesto un feedback immediato sui dati. Pertanto, è più facile per un singolo processore eseguire calcoli complessi in pochi secondi. Inoltre, grazie alla scala e alle dimensioni di Internet, il deep learning aiuta a gestire grandi set di dati a costi molto bassi. Pertanto, si prevede che questi fattori stimoleranno la crescita del mercato globale dei chip per il deep learning.

Personalizza questo rapporto in base alle tue esigenze

Potrai personalizzare gratuitamente qualsiasi rapporto, comprese parti di questo rapporto, o analisi a livello di paese, pacchetto dati Excel, oltre a usufruire di grandi offerte e sconti per start-up e università

Mercato dei chip per l'apprendimento profondo: Approfondimenti strategici

-

Ottieni le principali tendenze chiave del mercato di questo rapporto.Questo campione GRATUITO includerà l'analisi dei dati, che vanno dalle tendenze di mercato alle stime e alle previsioni.

La natura del business sta diventando molto competitiva e, per competere in modo efficiente, le aziende oggigiorno si affidano a informazioni utili e analisi aziendali. Tradizionalmente, gli strumenti di analisi aziendale venivano utilizzati per proiettare le vendite sulla base di dati relativi a eventi risalenti a una settimana o un mese prima. Con l'avvento della tecnologia di intelligenza artificiale, che apprende in tempo reale e fornisce raccomandazioni basate su modelli, le aziende hanno un'enorme opportunità di applicare il deep learning a vari processi per comprendere meglio l'ambiente aziendale e i clienti.

Considerando questi fattori, l'intelligenza artificiale consente alle aziende di migliorare l'efficienza operativa, ridurre i costi operativi, migliorare la qualità del servizio e l'esperienza del cliente.

Informazioni sul tipo di chip

Le unità di elaborazione grafica (GPU) hanno detenuto la quota di mercato principale dei chip per deep learning nel 2018, mentre si prevede che i circuiti integrati specifici per applicazione (ASIC) saranno il segmento in più rapida crescita durante il periodo di previsione. A causa del fatto che gli ASIC sono molto specifici e meno flessibili, rappresentano una delle opzioni hardware più performanti disponibili per le applicazioni di intelligenza artificiale.

Approfondimenti tecnologici

I chipset per deep learning includono sistemi su chip, sistemi in package, moduli multi-chip e altri ancora. Il segmento dei sistemi su chip ha detenuto la quota di mercato maggiore dei chip per deep learning nel 2018, poiché contribuisce a ridurre gli sprechi energetici, lo spazio occupato dai sistemi di grandi dimensioni e i costi.

Approfondimenti verticali di settore

Il mercato globale dei chip per deep learning è suddiviso in BFSI, Retail, IT e telecomunicazioni, Automotive e trasporti, Sanità, Media e intrattenimento e altri. Il BFSI ha detenuto la quota di mercato maggiore nel mercato dei chip per deep learning, mentre si prevede che il settore sanitario sarà il segmento in più rapida crescita. Fattori quali la riduzione dei costi operativi, l'adattamento a conformità e normative in continua evoluzione, la focalizzazione sul core business e l'integrazione dell'automazione nei processi aziendali sono altri fattori importanti che stanno alimentando la crescita del segmento BFSI nel mercato dei chip per deep learning.

Gli operatori presenti nel mercato dei chip per deep learning si concentrano principalmente sul miglioramento dei prodotti implementando tecnologie avanzate. La stipula di partnership, contratti, joint venture, finanziamenti e l'inaugurazione di nuove sedi in tutto il mondo consentono all'azienda di mantenere il proprio marchio a livello globale. Di seguito sono elencati alcuni degli sviluppi recenti;

2019: NVIDIA ha stretto una partnership con Hackster.io per lanciare l'AI at the Edge Challenge, una competizione in cui gli sviluppatori utilizzano il kit per sviluppatori NVIDIA Jetson Nano per realizzare progetti creativi e unici e avere la possibilità di vincere premi fino a 100.000 dollari.

2019: Intel ha annunciato i suoi piani di ampliamento dello stabilimento in Oregon per produrre un chip a 7 nm. Il nuovo stabilimento Intel rappresenterà la terza fase di D1X, un'enorme fabbrica avviata da Intel nel 2010. Ciascuna delle prime due fasi occupava una superficie di 1,1 milioni di piedi quadrati, creando una struttura complessiva equivalente a 15 magazzini Costco. La terza fase aumenterà apparentemente lo spazio produttivo di D1X di circa il 50%. Inoltre, Intel afferma che l'espansione dello stabilimento le consentirà di rispondere con una rapidità del 60% alla carenza di chip.

2019: Huawei ha lanciato HiSecEngine USG12000, il primo AIFW di livello T del settore. HiSecEngine USG12000 è dotato di chip Ascend AI, che offrono capacità di rilevamento intelligente e protezione intelligente dei confini per le reti aziendali.

Approfondimenti regionali sul mercato dei chip per l'apprendimento profondo

Le tendenze e i fattori regionali che influenzano il mercato dei chip per il Deep Learning durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione illustra anche i segmenti e la geografia del mercato dei chip per il Deep Learning in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America Meridionale e Centrale.

Ambito del rapporto sul mercato dei chip per l'apprendimento profondo

| Attributo del rapporto | Dettagli |

|---|---|

| Dimensioni del mercato in 2018 | US$ 2.04 Billion |

| Dimensioni del mercato per 2027 | US$ 21.31 Billion |

| CAGR globale (2018 - 2027) | 30.0% |

| Dati storici | 2016-2017 |

| Periodo di previsione | 2019-2027 |

| Segmenti coperti |

By Tipo di chip

|

| Regioni e paesi coperti |

Nord America

|

| Leader di mercato e profili aziendali chiave |

|

Densità dei player del mercato dei chip di apprendimento profondo: comprendere il suo impatto sulle dinamiche aziendali

Il mercato dei chip per il deep learning è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni il Mercato dei chip per l'apprendimento profondo Panoramica dei principali attori chiave

- GPU

- ASIC

- FPGA

- CPU

- Altri

Per tecnologia

- System-on-Chip

- System-in-Package

- Modulo multi-chip

- Altri

Per settore verticale

- Media e pubblicità

- BFSI, IT e telecomunicazioni

- Vendita al dettaglio

- Sanità

- Automotive e Trasporti

- Altri

Per area geografica

-

Nord America

- Stati Uniti

- Canada

- Messico

-

Europa

- Francia

- Germania

- Regno Unito

- Russia

- Italia

- Resto d'Europa

-

Asia Pacifico (APAC)

- Australia

- Cina

- India

- Giappone

- Corea del Sud

- Resto dell'APAC

-

Medio Oriente e Africa (MEA)

- Arabia Saudita

- Sudafrica

- Emirati Arabi Uniti

- Resto del MEA

-

Sud America (SAM)

- Brasile

- Argentina

- Resto del SAM

Profili aziendali

- Advanced Micro Devices, Inc.

- Alphabet Inc. (Google)

- Amazon.com, Inc.

- Baidu, Inc.

- Huawei Technologies Co., Ltd

- Intel Corporation

- NVIDIA Corporation

- Qualcomm Incorporated

- Samsung Electronics Co., Ltd.

- Xilinx, Inc.

Naveen è un professionista esperto in ricerche di mercato e consulenza con oltre 9 anni di esperienza in progetti personalizzati, sindacati e di consulenza. Attualmente Vicepresidente Associato, ha gestito con successo gli stakeholder lungo l'intera catena del valore del progetto e ha redatto oltre 100 report di ricerca e oltre 30 incarichi di consulenza. Il suo lavoro spazia tra progetti industriali e governativi, contribuendo in modo significativo al successo dei clienti e al processo decisionale basato sui dati.

Naveen ha conseguito una laurea in Ingegneria Elettronica e delle Comunicazioni presso la VTU, Karnataka, e un MBA in Marketing e Operations presso la Manipal University. È membro attivo dell'IEEE da 9 anni, partecipando a conferenze, simposi tecnici e svolgendo attività di volontariato sia a livello di sezione che regionale. Prima del suo attuale ruolo, ha lavorato come Consulente Strategico Associato presso IndustryARC e come Consulente Server Industriali presso Hewlett Packard (HP Global).

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative