Tendenze del mercato della terapia genica e approfondimenti sulla crescita 2025-2031

Dimensioni e previsioni del mercato della terapia genica (2021-2031), quota globale e regionale, trend e opportunità di crescita. Copertura del rapporto di analisi: per vettori (vettori non virali e vettori virali), indicazione (malattie neurologiche, cancro, distrofia muscolare di Duchenne, malattie epatologiche e altre indicazioni), modalità di somministrazione (in vivo ed ex vivo).

- Stato : Edito

- Codice del report : TIPHE100001165

- Categoria : Scienze della vita

- Numero di pagine : 300

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : April 23, 2026

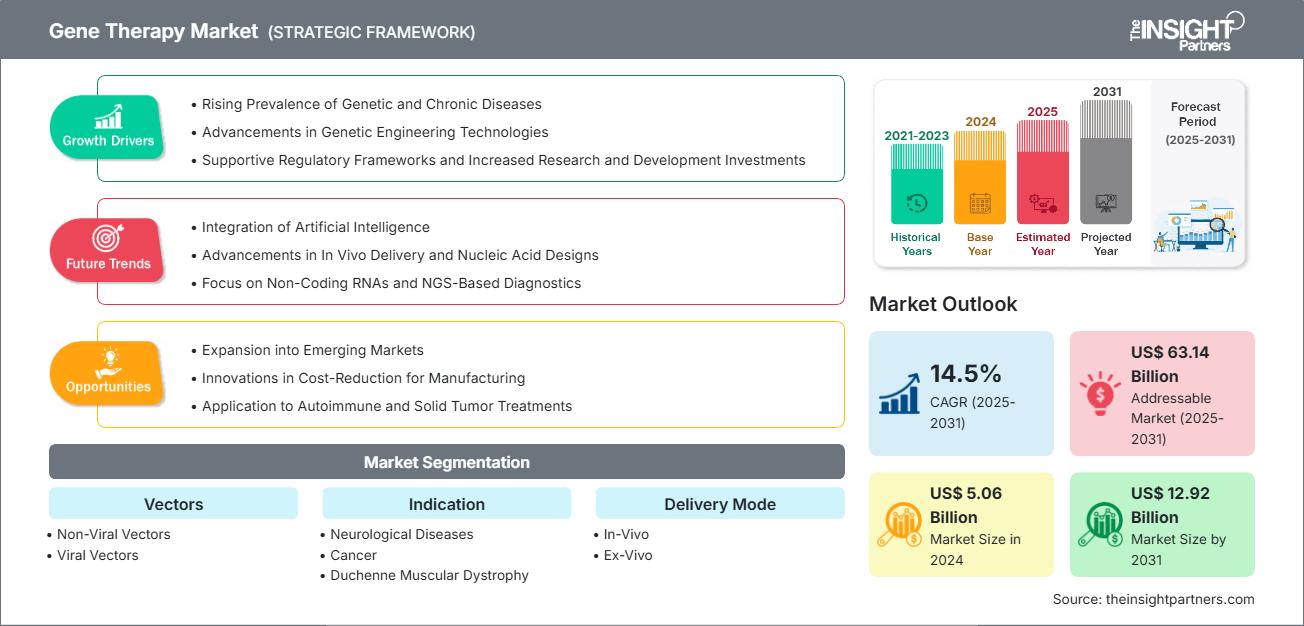

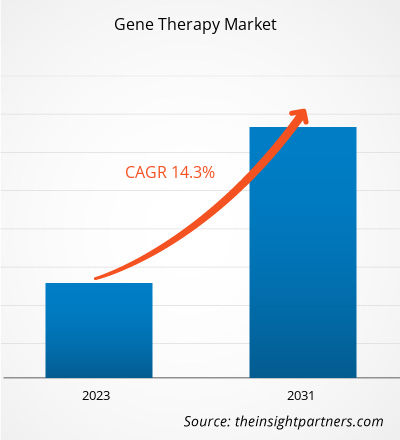

Si prevede che il mercato della terapia genica raggiungerà i 34.100 milioni di dollari entro il 2031. Si stima che il mercato registrerà un CAGR del 19,2% nel periodo 2025-2031.

Approfondimenti di mercato e opinioni degli analisti:

La terapia genica è un processo per il trattamento di malattie che consiste nell'inattivazione di un gene patogeno, nella sostituzione di un gene patogeno con una copia sana del gene o nell'introduzione di un gene nuovo o modificato nell'organismo per contribuire a trattare e prevenire la malattia. La terapia genica può essere classificata in terapia genica in vivo ed ex vivo. La terapia genica mira a sostituire o correggere i geni difettosi con quelli normali, consentendo all'organismo di produrre le proteine o gli enzimi corretti necessari per il normale funzionamento, che possono potenzialmente curare la causa sottostante delle malattie. La crescente prevalenza di malattie genetiche e tumori in tutto il mondo e il crescente numero di approvazioni FDA per le terapie geniche favoriscono la crescita del mercato della terapia genica. Inoltre, le tendenze del mercato della terapia genica includono progressi nelle tecnologie di terapia genica che favoriranno la crescita del mercato in futuro.

Fattori di crescita:

I progressi della biotecnologia hanno portato allo sviluppo di trattamenti per un'ampia gamma di indicazioni. Le terapie geniche vengono utilizzate per trattare diverse patologie, come il cancro, i disturbi neurologici e le malattie genetiche. A livello globale, le terapie geniche sono ampiamente adottate grazie alla disponibilità di prodotti approvati dalla Food and Drug Administration (FDA) statunitense. Di seguito sono riportati alcuni esempi di prodotti di terapia genica approvati dalla FDA negli ultimi anni:

- Nel dicembre 2023, la FDA ha approvato due terapie geniche cellulari per l'anemia falciforme. Lyfgenia (lovotibeglogene autotemcel) di Bluebird Bio è stato autorizzato per i pazienti affetti da anemia falciforme di età pari o superiore a 12 anni con una storia di eventi vaso-occlusivi. È stato approvato insieme a Casgevy (exagamglogene autotemcel), di Vertex Pharmaceuticals e CRISPR Therapeutics.

- Nel giugno 2023, la FDA ha approvato Roctavian, una terapia genica basata su un vettore virale adeno-associato per il trattamento di adulti affetti da emofilia A grave senza anticorpi preesistenti contro il sierotipo 5 del virus adeno-associato. L'emofilia A ereditaria è una grave malattia emorragica dovuta a una mutazione genetica responsabile della produzione del fattore VIII (FVIII), una proteina che consente la coagulazione del sangue. Roctavian è un prodotto di terapia genica monouso che contiene un vettore virale che trasporta un gene per il fattore VIII della coagulazione.

- Nel giugno 2023, la FDA ha approvato Elevidys, la prima terapia genica per il trattamento della distrofia muscolare di Duchenne nei pazienti pediatrici di età compresa tra 4 e 5 anni con una mutazione confermata nel gene della distrofia muscolare di Duchenne e che non presentano una condizione medica preesistente che impedisca il trattamento con questa terapia.

- Nel novembre 2022, la FDA ha approvato HEMGENIX, prodotto da CSL Behring LLC, una terapia genica ricombinante basata sul virus adeno-associato di tipo 5 per il trattamento di pazienti adulti affetti da alcuni tipi di emofilia B.

Pertanto, la crescente approvazione di queste terapie geniche sta alimentando la crescita del mercato della terapia genica.

Personalizza questo report in base alle tue esigenze

Ottieni la PERSONALIZZAZIONE GRATUITAMercato della terapia genica: approfondimenti strategici

-

Scopri le principali tendenze di mercato di questo rapporto.Questo campione GRATUITO includerà analisi dei dati, che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Segmentazione e ambito del report:

L'analisi del mercato della terapia genica è stata condotta considerando i seguenti segmenti: vettori, indicazione, modalità di somministrazione e area geografica. In base ai vettori, il mercato è suddiviso in vettori non virali e vettori virali. In termini di indicazione, il mercato è classificato in malattie neurologiche, cancro, distrofia muscolare di Duchenne, malattie epatologiche e altre indicazioni. In termini di modalità di somministrazione, il mercato è suddiviso in in vivo ed ex vivo. L'ambito del rapporto sul mercato della terapia genica copre Nord America (Stati Uniti, Canada e Messico), Europa (Francia, Germania, Regno Unito, Spagna, Italia e resto d'Europa), Asia-Pacifico (Cina, Giappone, India, Australia, Corea del Sud e resto dell'Asia-Pacifico), Medio Oriente e Africa (Arabia Saudita, Sudafrica, Emirati Arabi Uniti e resto del Medio Oriente e Africa) e Sud e Centro America (Brasile, Argentina e resto del Sud e Centro America).

Analisi segmentale:

Il mercato della terapia genica, in base ai vettori, è suddiviso in vettori non virali e vettori virali. Il segmento dei vettori virali ha detenuto una quota di mercato significativa nel 2023. Si prevede che registrerà un CAGR più elevato nel periodo 2023-2030.

In base alle indicazioni, il mercato è classificato in malattie neurologiche, cancro, distrofia muscolare di Duchenne, malattie epatologiche e altre indicazioni. Il segmento oncologico ha detenuto una quota di mercato significativa nel 2023 e si stima che registrerà il CAGR più elevato nel periodo 2023-2030.

In base alla modalità di somministrazione, il mercato è segmentato in in vivo ed ex vivo. Il segmento in vivo ha detenuto una quota di mercato significativa della terapia genica nel 2023 e si prevede che registrerà un CAGR più elevato nel periodo 2023-2030. La terapia genica in vivo consente un trattamento sistematico, il che implica che può raggiungere più siti e organi in tutto il corpo. Ciò è particolarmente utile per le malattie che colpiscono più aree o presentano segni sistemici, consentendo un approccio terapeutico completo. Inoltre, lo sviluppo di tecnologie di somministrazione avanzate, come vettori virali, nanoparticelle e vettori lipidici, ha migliorato l'efficacia e la specificità della terapia in vivo. Questi progressi potenziano la somministrazione mirata di materiale genetico e migliorano la sicurezza e l'efficacia della terapia.

Analisi regionale:

Geograficamente, il mercato della terapia genica è segmentato in Nord America, Europa, Asia-Pacifico, Sud e Centro America, Medio Oriente e Africa. Nel 2023, il Nord America ha conquistato una quota significativa del mercato. Nel 2023, gli Stati Uniti hanno dominato il mercato della terapia genica in questa regione. La crescita del mercato in Nord America è attribuita alla crescente prevalenza di malattie genetiche, all'aumento del numero di pazienti oncologici, all'aumento dei finanziamenti governativi, alla crescente adozione di terapie geniche avanzate per il trattamento delle malattie e alla crescente approvazione dei prodotti.

Secondo i Centers for Disease Control and Prevention (CDC), nel 2020 sono stati diagnosticati circa 1.603.844 nuovi casi di cancro, con 602.347 decessi per cancro negli Stati Uniti. Per ogni 100.000 individui, sono stati segnalati 403 nuovi casi di cancro. Inoltre, secondo l'Agenzia Internazionale per la Ricerca sul Cancro, si prevede che i nuovi casi di cancro raggiungeranno i 30,2 milioni entro il 2040. Secondo le stime del Government Accountability Office degli Stati Uniti pubblicate nell'ottobre 2021, circa 25-30 milioni di persone soffrono di malattie rare nel paese; quasi il 50% dei pazienti affetti da malattie rare sono bambini. Le malattie rare sono spesso il risultato di una mutazione genetica; si stima che l'80% delle malattie rare sia genetico.

Secondo un aggiornamento dell'ottobre 2021 dei National Institutes of Health, 10 aziende farmaceutiche e 5 organizzazioni no-profit hanno collaborato per accelerare lo sviluppo di terapie geniche per i 30 milioni di americani affetti da malattie rare. La FDA statunitense ha approvato 7 farmaci per la terapia cellulare e genica, con una pipeline di nuovi prodotti che raggiunge circa 1.200 terapie sperimentali. Metà di queste sono in fase di sperimentazione clinica di Fase 2, con stime di crescita annua delle vendite pari al 15% per le terapie cellulari e al 30% circa per le terapie geniche, secondo le stime del rapporto 2023 di Chemical & Engineering News. Tutti questi fattori sopra menzionati contribuiscono alla crescita del mercato della terapia genica nella regione.

Approfondimenti regionali sul mercato della terapia genica

Le tendenze regionali e i fattori che influenzano il mercato della terapia genica durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione illustra anche i segmenti e la distribuzione geografica del mercato della terapia genica in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America Meridionale e Centrale.

Ambito del rapporto di mercato sulla terapia genica

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2024 | XX milioni di dollari USA |

| Dimensioni del mercato entro il 2031 | 34.100,00 milioni di dollari USA |

| CAGR globale (2025 - 2031) | 19,2% |

| Dati storici | 2021-2023 |

| Periodo di previsione | 2025-2031 |

| Segmenti coperti |

Per vettori

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato della terapia genica: comprendere il suo impatto sulle dinamiche aziendali

Il mercato della terapia genica è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni una panoramica dei principali attori del mercato della terapia genica

Sviluppi del settore e opportunità future:

Di seguito sono elencate alcune iniziative intraprese dagli operatori del mercato globale della terapia genica:

- Nel gennaio 2022, Ori Biotech Ltd si è assicurata oltre 100 milioni di dollari in un round di finanziamento di serie B, sottoscritto in eccesso, per introdurre sul mercato un'innovativa piattaforma di produzione di terapie cellulari e geniche.

- Nel gennaio 2020, Astellas Pharma Inc. ha acquisito Audentes Therapeutics, Inc. L'acquisizione consente alla società risultante dalla fusione di diventare leader mondiale nella medicina genetica basata su AAV.

Panorama competitivo e aziende chiave:

Le previsioni di mercato della terapia genica possono aiutare gli stakeholder a pianificare le proprie strategie di crescita. Novartis AG, Astellas Pharma Inc., Bristol-Myers Squibb Company, Bluebird Bio Inc., CSL Behring, Sanofi, F. Hoffmann-La Roche Ltd, Daiichi Sankyo, Biogen e Oxford Biomedica sono tra i principali attori descritti nel rapporto di mercato sulla terapia genica. Queste aziende si concentrano sull'introduzione di nuovi prodotti ad alta tecnologia, sul miglioramento di prodotti esistenti e sull'espansione geografica per soddisfare la crescente domanda dei consumatori in tutto il mondo.

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative