Quota di mercato, domanda e crescita della fibra di carbonio verde entro il 2034

Dati storici : 2021-2024 | Anno base : 2025 | Periodo di previsione : 2026-2034Rapporto di analisi sulle dimensioni e le previsioni del mercato della fibra di carbonio verde (2021-2034), quota globale e regionale, tendenze e opportunità di crescita. Copertura: per tipo (fibra di carbonio riciclata Chopper e fibra di carbonio riciclata macinata), fonte (rottami automobilistici, rottami aerospaziali e altri) e applicazione (aerospaziale, automobilistico, energia eolica, articoli sportivi e altri)

- Stato : Prossimo

- Codice del report : TIPRE00029863

- Categoria : Prodotti chimici e materiali

- Numero di pagine : 150

- Formati di report disponibili :

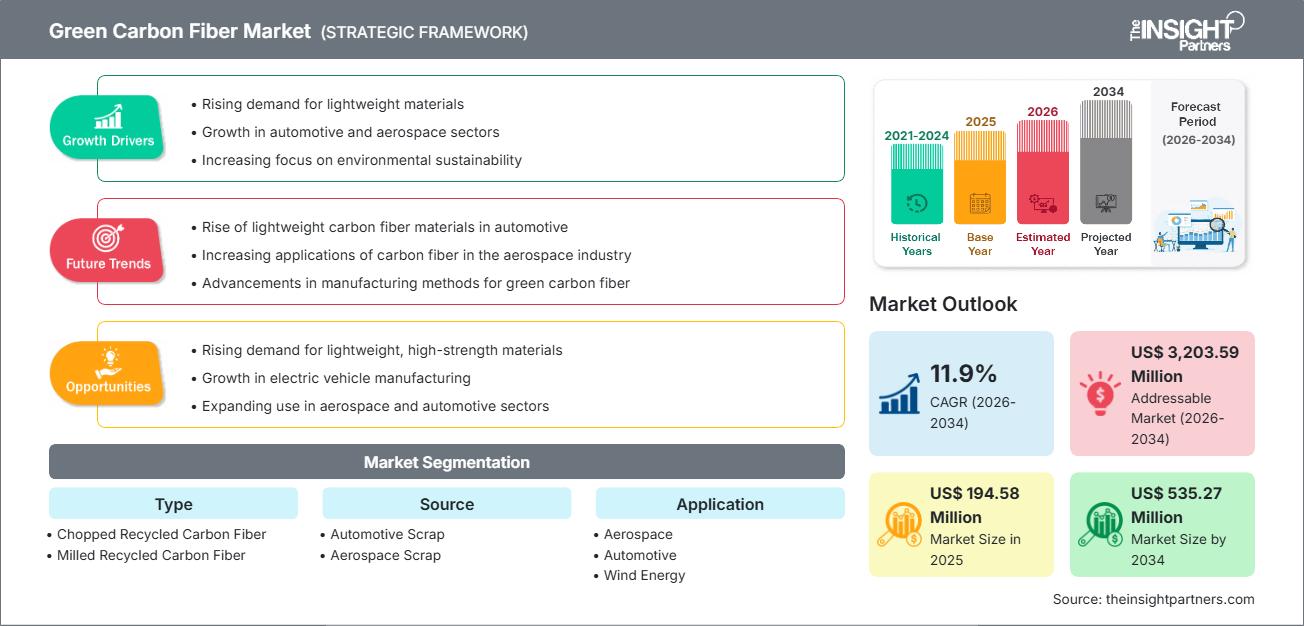

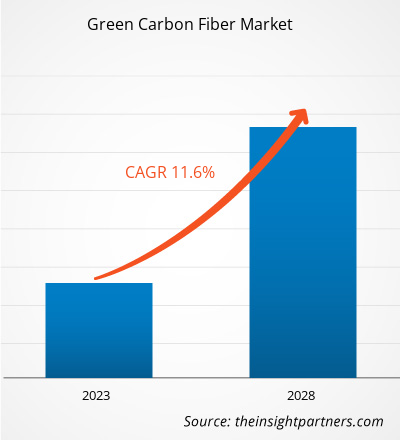

Si prevede che il mercato globale della fibra di carbonio verde raggiungerà i 535,27 milioni di dollari entro il 2034, rispetto ai 194,58 milioni di dollari del 2025. Si prevede che il mercato registrerà un CAGR dell'11,9% nel periodo di previsione 2026-2034.

Le principali dinamiche di mercato includono una crescente attenzione globale alla decarbonizzazione industriale, una crescente pressione normativa per deviare i rifiuti compositi dalle discariche e un significativo passaggio a modelli di economia circolare nella produzione ad alte prestazioni. Inoltre, si prevede che il mercato trarrà beneficio dalla crescente adozione di materiali riciclati nelle applicazioni di massa, dall'espansione di impianti di riciclaggio specializzati in Asia-Pacifico ed Europa e dalla crescente inclusione di fibre sostenibili in progetti su larga scala come parchi eolici offshore e flotte di veicoli elettrici di nuova generazione.

Analisi del mercato della fibra di carbonio verde

L'analisi del mercato della fibra di carbonio verde mostra uno spostamento verso materiali secondari di alto valore, poiché i produttori danno priorità alla sostenibilità del ciclo di vita e all'efficienza dei costi. Le tendenze degli acquisti indicano che il mercato si sta dividendo tra fibre di recupero aerospaziali di alta qualità e lavorazione di rottami ad alto volume per il settore automobilistico. Stanno emergendo opportunità strategiche nella compoundazione termoplastica e nello stampaggio a compressione, dove le proprietà meccaniche della fibra di carbonio riciclata offrono un chiaro vantaggio competitivo rispetto alla fibra di vetro tradizionale o alle resine vergini. L'analisi rileva inoltre che l'espansione del mercato dipende dall'ottimizzazione dei processi di recupero delle fibre, come la pirolisi e la solvolisi, per mantenere un'elevata resistenza alla trazione. La differenziazione competitiva ora si distingue per la capacità di fornire lunghezze di fibra costanti e composizioni chimiche superficiali pulite che consentono un'adesione superiore in nuove matrici composite. Questo approccio aiuta i riciclatori specializzati a praticare prezzi più elevati in un mercato sempre più dominato dai requisiti di conformità ambientale.

Panoramica del mercato della fibra di carbonio verde

I compositi sostenibili si sono evoluti da materiali sperimentali di nicchia a soluzioni industriali tradizionali. La fibra di carbonio verde include fibre fresate ad alta precisione, fibre tagliate con precisione e tappetini non tessuti derivati da fonti di recupero. Sia i leader chimici globali che le startup dell'economia circolare competono in questo mercato, utilizzando fonti di scarto come scarti di produzione e strutture a fine vita. La crescente domanda di alleggerimento per migliorare l'autonomia dei veicoli elettrici e l'efficienza delle turbine eoliche ha aumentato la popolarità della fibra di carbonio verde come soluzione portatile per il benessere del pianeta. Nord America ed Europa sono leader in termini di fatturato grazie a settori aerospaziali e automobilistici consolidati, mentre l'area Asia-Pacifico sta progredendo nelle infrastrutture di riciclaggio su larga scala e nell'adozione al dettaglio di beni di consumo. Il mercato statunitense è altamente sviluppato, trainato dai giganti aerospaziali focalizzati sulla sostenibilità e dall'ampia disponibilità di tecnologie di riciclaggio avanzate. La concorrenza tra i marchi sta alimentando una maggiore varietà di materiali e l'inclusione di resine sostenibili per creare sistemi compositi completamente ecologici.

Personalizza questo report in base alle tue esigenze

Ottieni la PERSONALIZZAZIONE GRATUITAMercato della fibra di carbonio verde: approfondimenti strategici

-

Scopri le principali tendenze di mercato di questo rapporto.Questo campione GRATUITO includerà analisi dei dati, che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Driver e opportunità del mercato della fibra di carbonio verde

Fattori trainanti del mercato:

- Normative ambientali rigorose e divieti di smaltimento in discarica: molte regioni stanno implementando norme severe contro lo smaltimento dei rifiuti compositi. Questa pressione normativa, insieme al crescente interesse per la produzione a rifiuti zero, sta alimentando la popolarità della fibra di carbonio riciclata.

- Efficienza in termini di costi rispetto alla fibra di carbonio vergine: la produzione di fibra riciclata consuma significativamente meno energia e offre un prezzo inferiore rispetto alle fibre vergini a base di PAN. Mentre le industrie cercano di ottimizzare i costi dei materiali, le alternative sostenibili continuano a registrare stabili aumenti di volume.

- Rapida espansione della produzione di veicoli elettrici: la transizione verso l'elettrificazione nel settore automobilistico ha rimosso le tradizionali barriere all'utilizzo di materiali riciclati. Ciò è particolarmente evidente nella rapida adozione di fibre triturate e macinate per componenti non strutturali degli interni e del sottocofano.

Opportunità di mercato:

- Espansione nell'elettronica di consumo e negli articoli sportivi: oltre all'uso industriale, la fibra di carbonio verde offre notevoli opportunità negli involucri ad alta rigidità per computer portatili e nei telai leggeri per biciclette e racchette da tennis.

- Crescita delle infrastrutture per le energie rinnovabili: la creazione di partnership strategiche tra produttori di turbine eoliche e aziende di riciclaggio può facilitare l'accesso a segmenti di mercato ad alto margine in cui la fibra riciclata viene utilizzata per rinforzare le pale delle turbine più grandi.

- Diversificazione nei pellet termoplastici avanzati: i produttori hanno sempre più opportunità di concentrarsi su produzioni specifiche attraverso lo sviluppo di pellet rinforzati con fibra di carbonio per la stampa 3D e lo stampaggio a iniezione.

Analisi della segmentazione del rapporto sul mercato della fibra di carbonio verde

La quota di mercato della fibra di carbonio verde viene analizzata in diversi segmenti per fornire una comprensione più chiara della sua struttura, del potenziale di crescita e delle tendenze emergenti. Di seguito è riportato l'approccio di segmentazione standard utilizzato nei report di settore:

Per tipo:

- Fibra di carbonio riciclata tritata: un segmento dominante ampiamente utilizzato nei tappetini non tessuti e nei rinforzi per lo stampaggio a iniezione di materiali termoplastici grazie alla sua versatilità e facilità di lavorazione.

- Fibra di carbonio riciclata macinata: una nicchia in rapida crescita che prevede la macinazione della fibra in una polvere fine, sempre più preferita per applicazioni che richiedono una maggiore conduttività elettrica o una finitura superficiale in rivestimenti e resine.

Per fonte:

- Rottami automobilistici: rimangono un canale primario per materie prime in grandi volumi, beneficiando dell'espansione dei programmi di alleggerimento dei veicoli e degli scarti di produzione.

- Rottami aerospaziali: la fonte di maggior valore, che fornisce fibre ad alto modulo recuperate da aeromobili a fine vita e rifiuti pre-impregnati di produzione, consentendo applicazioni secondarie ad alte prestazioni.

Per applicazione:

- Aerospaziale: utilizzo di fibre riciclate per pannelli interni, condotti e componenti strutturali non critici per raggiungere gli obiettivi aziendali di emissioni nette pari a zero.

- Settore automobilistico: l'applicazione in più rapida crescita, in particolare per i pannelli del telaio, le strutture del pavimento e gli alloggiamenti delle batterie nei veicoli elettrici.

- Energia eolica: offre una gamma selezionata ma in crescita di opzioni di rinforzo per calotte di longheroni e componenti di pale nel settore delle energie rinnovabili.

- Articoli sportivi: spinti dalla domanda dei consumatori di attrezzature ecologiche ad alte prestazioni, come mazze da golf, bastoni da hockey e telai per biciclette.

Per geografia:

- America del Nord

- Europa

- Asia Pacifico

- America meridionale e centrale

- Medio Oriente e Africa

Ambito del rapporto sul mercato della fibra di carbonio verde

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2025 | 194,58 milioni di dollari USA |

| Dimensioni del mercato entro il 2034 | 535,27 milioni di dollari USA |

| CAGR globale (2026 - 2034) | 11,9% |

| Dati storici | 2021-2024 |

| Periodo di previsione | 2026-2034 |

| Segmenti coperti |

Per tipo

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato della fibra di carbonio verde: comprendere il suo impatto sulle dinamiche aziendali

Il mercato della fibra di carbonio ecologica è in rapida crescita, trainato dalla crescente domanda degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei vantaggi del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

Analisi della quota di mercato della fibra di carbonio verde per area geografica

Si prevede che la regione Asia-Pacifico crescerà più rapidamente nei prossimi anni grazie agli ingenti investimenti nell'energia eolica e nella produzione di veicoli elettrici. Anche Europa e Nord America offrono numerose opportunità inesplorate per le tecnologie di riciclo avanzate e il recupero aerospaziale ad alto valore.

Il mercato della fibra di carbonio verde sta attraversando una profonda trasformazione, passando da una nicchia di ricerca e sviluppo a una materia prima industriale essenziale per l'economia a zero emissioni nette. La crescita è trainata dall'urgente necessità di ridurre il peso degli aeromobili, dall'impennata della produzione di veicoli elettrici (EV) e dall'imponente espansione delle infrastrutture per le energie rinnovabili. Di seguito è riportato un riepilogo delle quote di mercato e delle tendenze per regione:

America del Nord

- Quota di mercato: un segmento importante guidato da un'industria aerospaziale solida e dalla presenza di importanti innovatori nel settore del riciclaggio.

-

Fattori chiave:

- Forte domanda da parte del settore della difesa di materiali leggeri sostenibili

- Incentivi federali per l'energia pulita e la circolarità della produzione nazionale

- Elevata concentrazione di rottami aerospaziali provenienti dai principali produttori di aeromobili

- Tendenze: adozione di successo di fibre riciclate nei filamenti per la stampa 3D e ampliamento degli impianti commerciali di solvolisi.

Europa

- Quota di mercato: detiene la quota maggiore a livello mondiale, ancorata alle rigide direttive UE sul riciclaggio dei veicoli a fine vita e sulla neutralità carbonica.

-

Fattori chiave:

- Enorme base produttiva automobilistica in Germania e Francia, con priorità ai materiali ecologici

- Infrastruttura di elaborazione consolidata per il recupero dei rifiuti compositi

- Solido sostegno governativo alle iniziative di economia circolare

- Tendenze: un cambiamento strategico verso l'utilizzo di fibre riciclate nelle infrastrutture del trasporto pubblico e un'attenzione particolare ai tappetini non tessuti ad alte prestazioni.

Asia-Pacifico

- Quota di mercato: la regione in più rapida crescita, con Cina e Giappone che agiscono come motori principali per il consumo sostenibile di materiali.

-

Fattori chiave:

- Enorme base di consumatori alla ricerca di prodotti elettronici e sportivi ecocompatibili

- Iniziative sostenute dal governo incentrate sulla trasformazione in un polo globale per la produzione di veicoli elettrici

- Rapida espansione degli impianti eolici offshore che richiedono materiali compositi avanzati

- Tendenze: Forte affidamento su tecnologie di smistamento automatizzate e produzione su larga scala di fibre tritate per l'industria elettronica.

America meridionale e centrale

- Quota di mercato: mercato emergente con crescente attenzione alle energie rinnovabili in paesi come Brasile e Cile.

-

Fattori chiave:

- Investimenti crescenti in installazioni di parchi eolici di grandi dimensioni che richiedono pale leggere e ad alta rigidità

- Modernizzazione delle operazioni di assemblaggio aerospaziale regionale per soddisfare gli standard internazionali di sostenibilità

- Tendenze: Crescita di impianti di riciclaggio localizzati per gestire il crescente volume di rifiuti industriali derivanti dalla fiorente produzione regionale di componenti per autoveicoli.

Medio Oriente e Africa

- Quota di mercato: mercato in via di sviluppo con elevato potenziale legato ai cambiamenti strategici nei settori dell'energia e della produzione avanzata.

-

Fattori chiave:

- Investimenti strategici in città intelligenti e progetti infrastrutturali avanzati nella regione del Golfo

- Crescente interesse per le tecnologie delle celle a combustibile a idrogeno e la conseguente necessità di serbatoi di stoccaggio leggeri

- Tendenze: implementazione di impianti di pirolisi su scala pilota e attenzione all'utilizzo di fibre riciclate per infrastrutture di desalinizzazione e stoccaggio di energia su larga scala.

Elevata densità di mercato e concorrenza

La concorrenza si sta intensificando grazie alla presenza di leader affermati come Toray Industries, SGL Carbon e Mitsubishi Chemical Group. Anche esperti regionali nel riciclo e operatori di nicchia come Vartega Inc, Gen 2 Carbon e Carbon Conversions contribuiscono a creare un panorama di mercato diversificato e in rapida espansione.

Questo ambiente competitivo spinge i fornitori a differenziarsi attraverso:

- Convalida delle prestazioni: evidenzia che le fibre riciclate possono mantenere oltre il 90% della rigidità delle fibre vergini, rendendole un'alternativa superiore per le applicazioni sensibili al peso.

- Trasparenza della catena di fornitura: i produttori gestiscono l'intero ciclo di vita, dalla raccolta degli scarti negli impianti aerospaziali alla consegna della fibra lavorata agli OEM del settore automobilistico, garantendo standard etici e tracciabili.

- Lavorazione innovativa: nuove tecnologie come la selezione basata sull'intelligenza artificiale e il riciclaggio chimico a basso consumo energetico contribuiscono a creare polveri e fasci di alta qualità utilizzati in prodotti di consumo di fascia alta in tutto il mondo.

Opportunità e mosse strategiche

- Collaborare con i principali OEM del settore automobilistico e aerospaziale per garantire accordi di fornitura di rottami a lungo termine. Ciò garantisce una materia prima stabile per rottami automobilistici e aerospaziali, offrendo al contempo agli OEM un modo affidabile per raggiungere i loro obiettivi di neutralità carbonica.

- Sviluppare trattamenti chimici proprietari (appretto) per fibre riciclate per migliorarne l'adesione alle resine termoplastiche. Ciò consente alla fibra di carbonio verde di raggiungere proprietà meccaniche più vicine a quelle della fibra vergine, aprendo la strada ad applicazioni strutturali ad alto margine.

- Incorporare la fibra di carbonio verde in settori in forte crescita come la mobilità aerea urbana (UAM/taxi aerei) e lo stoccaggio dell'idrogeno. Queste applicazioni richiedono un peso estremamente ridotto e possono assorbire i costi leggermente più elevati dei materiali riciclati avanzati.

Le principali aziende che operano nel mercato della fibra di carbonio verde sono:

- Procotex Corp SA

- Stems Inc.

- Sigmatex (UK) Ltd

- Shocker Composites LLC

- Conversioni di carbonio Co

- SGL Carbon SE

- Toray Industries Inc

- Gen 2 Carbon Ltd

- Catack-H Co Ltd

- Riciclo innovativo

Disclaimer: le aziende elencate sopra non sono classificate in un ordine particolare.

Notizie e sviluppi recenti sul mercato della fibra di carbonio verde

- Nell'ottobre 2025, Toray Industries, Inc. ha annunciato di aver sviluppato una tecnologia di riciclo in grado di decomporre diverse plastiche rinforzate con fibra di carbonio (CFRP) realizzate con resine termoindurenti, mantenendone la resistenza e la qualità superficiale. L'azienda ha sfruttato questa tecnologia per creare un tessuto non tessuto utilizzando fibre di carbonio riciclate.

- Nel maggio 2025, Syensqo e Vartega hanno annunciato una collaborazione tecnica e commerciale per creare un ecosistema che promuova l'uso di prodotti in fibra di carbonio riciclata post-industriale in applicazioni ad alte prestazioni.

Copertura e risultati del rapporto sul mercato della fibra di carbonio verde

Il rapporto sulle dimensioni e le previsioni del mercato della fibra di carbonio verde (2021-2034) fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato della fibra di carbonio verde a livello globale, regionale e nazionale per tutti i segmenti di mercato chiave coperti dall'ambito

- Tendenze del mercato della fibra di carbonio verde, nonché dinamiche di mercato quali fattori trainanti, vincoli e opportunità chiave

- Analisi PEST e SWOT dettagliate

- Analisi del mercato della fibra di carbonio verde che copre le principali tendenze del mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa termica, i principali attori e gli sviluppi recenti nel mercato della fibra di carbonio verde.

- Profili aziendali dettagliati

- Analisi storica (2 anni), anno base, previsione (7 anni) con CAGR

- Analisi PEST e SWOT

- Valore/volume delle dimensioni del mercato - Globale, Regionale, Nazionale

- Industria e panorama competitivo

- Set di dati Excel

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative

Sblocca sconti esclusivi sui report

Richiedi ora

Ottieni un campione gratuito per - Mercato della fibra di carbonio verde

Ottieni un campione gratuito per - Mercato della fibra di carbonio verde