Dimensioni, domanda e crescita del mercato degli integratori per animali domestici entro il 2034

Dimensioni e previsioni del mercato degli integratori per animali domestici (2021-2034), quota globale e regionale, trend e analisi delle opportunità di crescita. Copertura del rapporto: per forma (masticabile, in polvere e altre), tipo di animale domestico (cani, gatti e altri), canale di distribuzione (online e offline) e area geografica.

- Stato : Dati rilasciati

- Codice del report : TIPRE00019974

- Categoria : Cibo e bevande

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : April 09, 2026

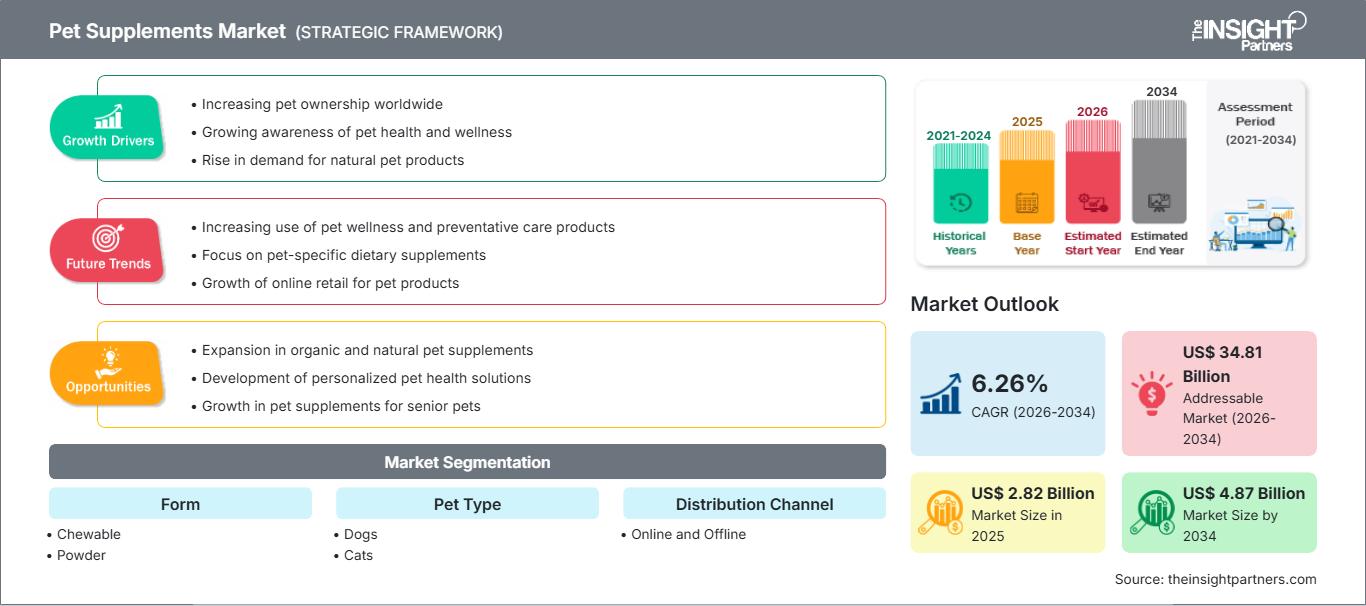

Si prevede che il mercato degli integratori per animali domestici raggiungerà un valore di 4,87 miliardi di dollari entro il 2034, rispetto ai 2,82 miliardi di dollari del 2025. Si prevede inoltre che il mercato registrerà un tasso di crescita annuo composto (CAGR) del 6,26% nel periodo di previsione 2026-2034.

La crescente preferenza dei consumatori per gli ingredienti naturali negli integratori per animali domestici è destinata a diventare una tendenza chiave nel mercato globale di tali prodotti. Oggi, i proprietari di animali domestici verificano i nutrienti e gli additivi contenuti negli integratori per assicurarsi che i loro animali ricevano le cure più appropriate e benefiche. Pertanto, la maggiore consapevolezza tra i proprietari di animali domestici riguardo ai benefici degli ingredienti naturali ha alimentato la domanda di integratori naturali per animali in tutto il mondo.

Analisi del mercato degli integratori per animali domestici

Uno dei principali fattori che guidano la crescita del mercato degli integratori per animali domestici è rappresentato dalle iniziative strategiche dei principali operatori del settore. La crescente domanda di prodotti per animali domestici ricchi di nutrienti, di alta qualità e personalizzati ha stimolato l'innovazione da parte dei produttori di integratori. Questi si stanno concentrando sullo sviluppo di integratori innovativi, sicuri e di qualità superiore. Inoltre, stanno diversificando i loro portafogli prodotti lanciando una varietà di integratori per animali domestici con diverse forme e benefici per la salute. Ad esempio, nel giugno 2024, ADM ha annunciato il lancio in Europa di sette formule complete per prodotti per animali domestici, pensate per un mercato che dà sempre più priorità alla salute olistica degli animali. Disponibili in compresse masticabili e bustine di polvere, queste formule funzionali vantano benefici per il benessere molto ricercati, supportati da evidenze scientifiche e conformi alle normative europee, offrendo ai consumatori opzioni affidabili per supportare il percorso di benessere dei loro animali domestici.

Panoramica del mercato degli integratori per animali domestici

Gli integratori per animali domestici sono prodotti che offrono nutrienti aggiuntivi come vitamine, oligoelementi, minerali o una combinazione di questi in diverse forme. Gli integratori per animali domestici contribuiscono a migliorare il sistema immunitario e a ridurre il rischio di infiammazioni, cancro, malattie cardiache, diabete e altre patologie. Inoltre, aiutano a rafforzare la capacità di combattere problemi come infezioni batteriche, prurito cutaneo e allergie ambientali, migliorando la salute della pelle. Il mercato degli integratori per animali domestici è trainato da fattori quali la crescente diffusione degli animali da compagnia e la crescente attenzione al loro benessere. Il mercato globale degli integratori per animali domestici è segmentato in base alla forma, al tipo di animale e al canale di distribuzione. In base alla forma, il mercato è segmentato in compresse masticabili, polveri e altre. Il segmento delle compresse masticabili deteneva la quota maggiore del mercato degli integratori per animali domestici nel 2023.

Personalizza questo report in base alle tue esigenze

Ottieni la PERSONALIZZAZIONE GRATUITAMercato degli integratori per animali domestici: approfondimenti strategici

-

Scopri le principali tendenze di mercato di questo report.Questo campione GRATUITO includerà un'analisi dei dati, che spazierà dalle tendenze di mercato alle stime e alle previsioni.

Fattori trainanti e opportunità del mercato degli integratori per animali domestici

L'aumento del numero di proprietari di animali domestici favorirà la crescita del mercato.

Negli ultimi anni, l'aumento del reddito disponibile e il crescente interesse per l'adozione di animali domestici hanno favorito la diffusione della cultura degli animali in molti paesi del mondo. La crescente proprietà di animali domestici in diversi paesi sta trainando la crescita del mercato degli integratori per animali. Inoltre, a causa della pandemia di COVID-19, molte persone hanno lavorato da casa e si sono autoisolate; questo cambiamento di stile di vita ha spinto molte famiglie ad adottare un animale domestico. Molte persone si sono sentite più sicure con un animale da compagnia che ha fornito supporto emotivo e mentale durante la pandemia.

Preferenze dei consumatori per le piattaforme di e-commerce: un'opportunità

Negli ultimi anni, l'utilizzo delle piattaforme di e-commerce è aumentato in tutto il mondo. Alcuni dei fattori chiave che guidano le vendite di vari prodotti, inclusi gli integratori per animali domestici, attraverso le piattaforme di e-commerce sono la crescente diffusione di smartphone e internet, l'aumento del potere d'acquisto dei consumatori e la comodità dell'esperienza di acquisto offerta da queste piattaforme di vendita al dettaglio online. Molte persone preferiscono le piattaforme di vendita al dettaglio online per acquistare integratori per animali domestici grazie alla disponibilità di prodotti di diverse marche, descrizioni dettagliate dei prodotti, valutazioni e recensioni dei consumatori, sconti, offerte e servizi di consegna a domicilio. Durante la pandemia di COVID-19, la propensione dei consumatori verso lo shopping online è aumentata. Con la crescente preferenza dei consumatori per le piattaforme di e-commerce, i produttori di integratori per animali domestici stanno rafforzando la loro presenza online vendendo i loro prodotti attraverso piattaforme di e-commerce come Walmart, Amazon e Lidl. Pertanto, la crescente preferenza dei consumatori per le piattaforme di e-commerce offre un'enorme opportunità ai produttori di integratori per animali domestici di distribuire i propri prodotti attraverso queste piattaforme e ampliare la propria base clienti e i margini di profitto.

Analisi di segmentazione del mercato degli integratori per animali domestici

I segmenti chiave che hanno contribuito alla definizione dell'analisi di mercato degli integratori per animali domestici sono la forma, il tipo di animale e il canale di distribuzione.

- In base alla forma, il mercato degli integratori per animali domestici si suddivide in masticabili, in polvere e altri. Il segmento dei masticabili deteneva la quota di mercato maggiore nel 2023.

- In base alla tipologia di animale domestico, il mercato è segmentato in cani, gatti e altri. Il segmento dei cani deteneva la quota di mercato maggiore nel 2023.

- In termini di canale di distribuzione, il mercato si divide in online e offline. Il segmento offline ha dominato il mercato nel 2023.

Analisi della quota di mercato degli integratori per animali domestici per area geografica

L'ambito geografico del rapporto sul mercato degli integratori per animali domestici è suddiviso principalmente in cinque regioni: Nord America, Asia Pacifico, Europa, Medio Oriente e Africa e Sud e Centro America.

Nel 2023, il Nord America ha dominato il mercato degli integratori per animali domestici. La crescita significativa di questo mercato è dovuta alla crescente "umanizzazione" degli animali, che sta incrementando la domanda di snack, alimenti e integratori per animali. Inoltre, la maggiore consapevolezza degli elevati benefici nutrizionali degli integratori per animali sta influenzando le decisioni di acquisto dei consumatori. Infine, la crescente attenzione dei proprietari di animali domestici verso i vantaggi degli ingredienti naturali sta alimentando la domanda di integratori naturali per animali in Nord America.

Ambito del rapporto sul mercato degli integratori per animali domestici

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2025 | 2,82 miliardi di dollari USA |

| Dimensioni del mercato entro il 2034 | 4,87 miliardi di dollari USA |

| Tasso di crescita annuo composto (CAGR) globale (2026-2034) | 6,26% |

| Dati storici | 2021-2024 |

| periodo di previsione | 2026-2034 |

| Segmenti trattati |

Per modulo

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori nel mercato degli integratori per animali domestici: comprenderne l'impatto sulle dinamiche di business

Il mercato degli integratori per animali domestici è in rapida crescita, trainato dalla crescente domanda da parte degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

Notizie e recenti sviluppi del mercato degli integratori per animali domestici

Il mercato degli integratori per animali domestici viene valutato raccogliendo dati qualitativi e quantitativi a seguito di ricerche primarie e secondarie, che includono importanti pubblicazioni aziendali, dati di associazioni e database. Di seguito è riportato un elenco degli sviluppi e delle strategie del mercato degli integratori per animali domestici:

Mars Petcare entra nel settore degli integratori alimentari con il lancio di Pedigree Multivitamins. Questa nuova linea di prodotti è composta da tre tipi di compresse masticabili morbide, specificamente formulate per soddisfare le esigenze nutrizionali essenziali degli animali domestici. Pedigree Multivitamins mira a supportare il sistema immunitario, favorire una sana digestione e prendersi cura delle articolazioni degli animali. (Fonte: Mars Petcare/Comunicato stampa, 2023)

- Native Pet ha lanciato The Daily, un nuovo integratore alimentare completo per cani, sviluppato negli ultimi due anni. (Nutraceuticals World, Sito web aziendale/Notizie/2023)

Copertura e risultati del rapporto sul mercato degli integratori per animali domestici

Il rapporto "Dimensioni e previsioni del mercato degli integratori per animali domestici (2021-2031)" fornisce un'analisi dettagliata del mercato, coprendo le seguenti aree:

- Dimensioni del mercato e previsioni a livello globale, regionale e nazionale per tutti i principali segmenti di mercato inclusi nell'ambito

- Dinamiche di mercato quali fattori trainanti, vincoli e opportunità chiave

- Principali tendenze future

- Analisi dettagliata delle cinque forze di Porter e analisi SWOT

- Analisi del mercato globale e regionale, con particolare attenzione alle principali tendenze, ai principali operatori, alle normative e ai recenti sviluppi del mercato.

- Analisi del panorama industriale e della concorrenza, con particolare attenzione alla concentrazione del mercato, all'analisi tramite mappa termica, ai principali operatori e agli sviluppi recenti.

- Profili aziendali dettagliati

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative