Tendenze del mercato degli ancoraggi per tessuti molli e prospettive di crescita nel 2034

Rapporto di analisi sulle dimensioni e le previsioni del mercato degli ancoraggi per tessuti molli (2021-2034), quota globale e regionale, tendenze e opportunità di crescita. Copertura: per tipo (assorbibile e non assorbibile), tipo di legatura (annodata e senza nodo), materiale (ancora di sutura metallica, ancora di sutura bioassorbibile, ancora di sutura PEEK, ancora di sutura biocomposita e altro) e utente finale (ospedale, clinica, servizio medico di emergenza e altro).

- Stato : Dati rilasciati

- Codice del report : TIPRE00024412

- Categoria : Scienze della vita

- Numero di pagine : 150

- Formati di report disponibili :

- Data dell'ultimo aggiornamento : February 09, 2026

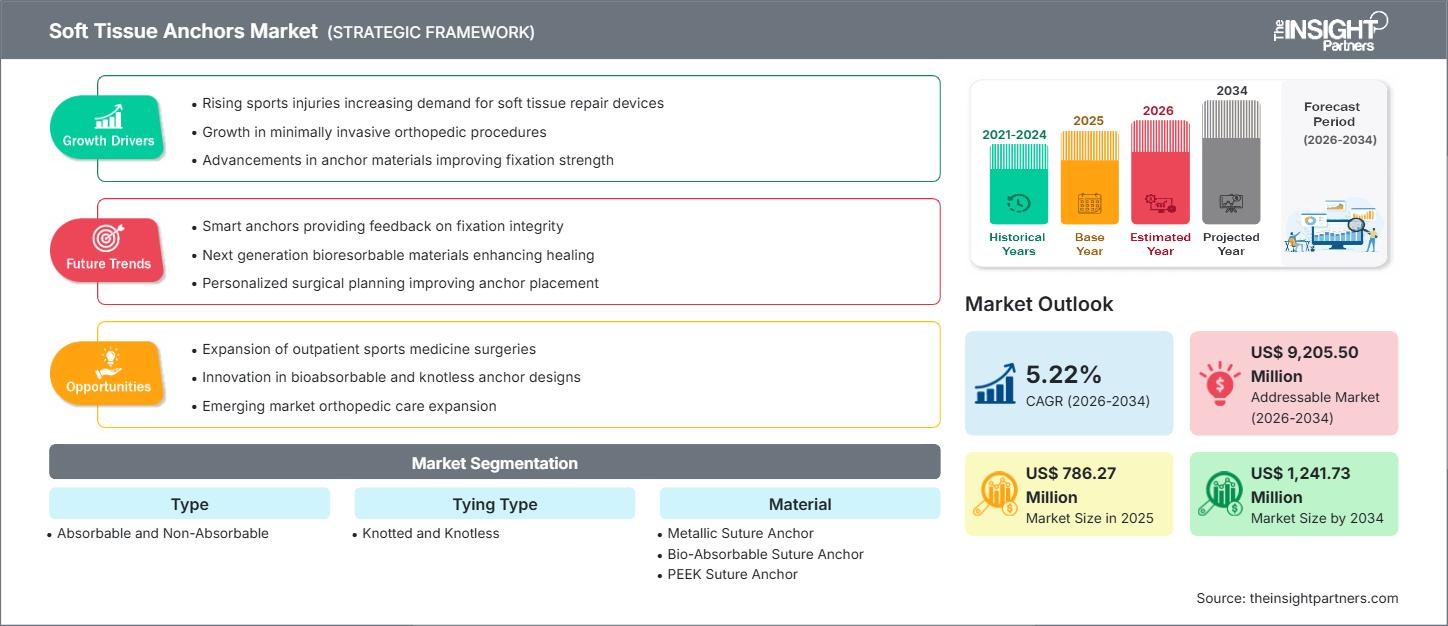

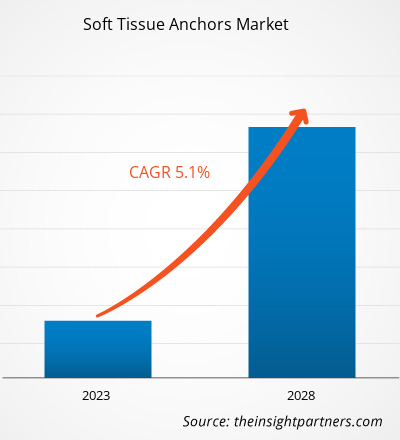

Si prevede che il mercato degli ancoraggi per tessuti molli raggiungerà i 1.241,73 milioni di dollari entro il 2034, rispetto ai 786,27 milioni di dollari del 2025. Si prevede che il mercato registrerà un tasso di crescita annuo composto (CAGR) del 5,22% nel periodo di previsione 2026-2034.

Analisi di mercato degli ancoraggi per tessuti molli

Le previsioni del mercato globale delle ancore per tessuti molli indicano una crescita costante, trainata principalmente dall'aumento dell'incidenza di infortuni sportivi e patologie legamentose e tendinee in tutto il mondo, come le lesioni della cuffia dei rotatori e le ricostruzioni del legamento crociato anteriore. I costanti progressi tecnologici nella progettazione delle ancore, inclusi quelli verso strutture senza nodo e suture a doppio carico che consentono una maggiore resistenza di fissaggio biomeccanico e risultati riproducibili, supportano fortemente l'espansione del mercato. Inoltre, la crescente adozione di procedure artroscopiche mini-invasive nei centri ortopedici specializzati stimola la domanda di soluzioni innovative basate su materiali come biocompositi, PEEK e polimeri riassorbibili, che portano a un recupero più rapido del paziente e a una migliore integrazione biologica.

Panoramica del mercato degli ancoraggi per tessuti molli

Le ancore per tessuti molli sono sofisticati dispositivi ortopedici impiantabili impiegati per il fissaggio sicuro di tessuti molli, come legamenti, tendini e capsule articolari, direttamente alla struttura ossea sottostante. Questi dispositivi sono diventati componenti importanti in vari interventi chirurgici su articolazioni importanti, tra cui, a titolo esemplificativo ma non esaustivo, spalla, ginocchio, anca, gomito, piede e caviglia. Il mercato offre diverse configurazioni per soddisfare specifiche esigenze chirurgiche e garantire un fissaggio migliore, come materiali riassorbibili e non riassorbibili e design con e senza nodi. Grazie alla forte dinamica competitiva e alla continua attenzione alla ricerca e sviluppo delle principali aziende ortopediche, le ancore per tessuti molli sono fondamentali per la moderna medicina sportiva, garantendo una guarigione ottimale tra tessuto e osso e il ripristino funzionale del paziente.

Personalizza questo report in base alle tue esigenze

Ottieni la PERSONALIZZAZIONE GRATUITAMercato degli ancoraggi per tessuti molli: approfondimenti strategici

-

Scopri le principali tendenze di mercato di questo rapporto.Questo campione GRATUITO includerà analisi dei dati, che spaziano dalle tendenze di mercato alle stime e alle previsioni.

Fattori trainanti e opportunità del mercato

Fattori trainanti del mercato

- Aumento dell'incidenza globale degli infortuni muscoloscheletrici: la crescita della partecipazione sportiva e l'invecchiamento della popolazione che mantiene uno stile di vita attivo stanno incrementando il volume degli infortuni ai tessuti molli, determinando una maggiore richiesta di soluzioni di fissaggio affidabili.

- Preferenza per la chirurgia artroscopica mininvasiva: poiché i sistemi sanitari privilegiano trattamenti che riducono al minimo la morbilità e i tempi di degenza ospedaliera, le ancore continueranno a essere adottate nelle procedure mininvasive.

- Tecnologia nei materiali e nella meccanica di fissaggio: materiali biocompositi, PEEK e polimeri riassorbibili migliorano la longevità e la biocompatibilità del fissaggio. Le tecniche senza nodi e le strutture con nastro di sutura migliorano il flusso di lavoro e i risultati chirurgici.

Opportunità di mercato

- Espansione nelle economie emergenti: la crescente capacità degli ospedali ortopedici e l'aumento degli investimenti nella sanità pubblica offrono notevoli opportunità di penetrazione del mercato e di adozione di tecnologie avanzate per gli ancoraggi di sutura.

- Programmi di formazione per chirurghi: iniziative di formazione mirate su strutture avanzate senza nodi e tecniche di fissazione di revisione possono favorire l'utilizzo del prodotto e migliorare i risultati clinici.

- Integrazione strategica dei prodotti: la combinazione di ancore di sutura con offerte complementari quali nastri di sutura, prodotti di aumento biologico e sistemi di navigazione chirurgica migliora le proposte di valore e supporta soluzioni chirurgiche integrate.

Analisi della segmentazione del rapporto di mercato degli ancoraggi per tessuti molli

La quota di mercato delle ancore per tessuti molli viene analizzata in diversi segmenti per fornire informazioni dettagliate sulle preferenze di prodotto, l'adozione tecnologica e i modelli di consumo degli utenti finali. La segmentazione standard è la seguente:

Per tipo

- Ancore assorbibili: polimeri biocompatibili che si degradano nel tempo, riducendo al minimo l'interferenza dell'impianto.

- Ancore non assorbibili: fissaggio permanente mediante materiali come PEEK o metallo, preferibile per interventi chirurgici ad alta tensione o di revisione.

Per tipo di legatura

- Annodato

- Senza nodi

Per materiale

- Ancoraggio di sutura metallico

- Ancora di sutura bioassorbibile

- Ancoraggio di sutura PEEK

- Ancora di sutura biocomposita

Per utente finale

- Ospedali

- Cliniche

- Servizi medici di emergenza

Per geografia

- America del Nord

- Europa

- Asia Pacifico

- America meridionale e centrale

- Medio Oriente e Africa

Approfondimenti regionali sul mercato degli ancoraggi per tessuti molli

Le tendenze regionali e i fattori che influenzano il mercato delle ancore per tessuti molli durante il periodo di previsione sono stati ampiamente spiegati dagli analisti di The Insight Partners. Questa sezione illustra anche i segmenti e la distribuzione geografica del mercato delle ancore per tessuti molli in Nord America, Europa, Asia-Pacifico, Medio Oriente e Africa, America Meridionale e Centrale.

Ambito del rapporto di mercato sulle ancore per tessuti molli

| Attributo del report | Dettagli |

|---|---|

| Dimensioni del mercato nel 2025 | 786,27 milioni di dollari USA |

| Dimensioni del mercato entro il 2034 | 1.241,73 milioni di dollari USA |

| CAGR globale (2026 - 2034) | 5,22% |

| Dati storici | 2021-2024 |

| Periodo di previsione | 2026-2034 |

| Segmenti coperti |

Per tipo

|

| Regioni e paesi coperti |

America del Nord

|

| Leader di mercato e profili aziendali chiave |

|

Densità degli operatori del mercato degli ancoraggi per tessuti molli: comprendere il suo impatto sulle dinamiche aziendali

Il mercato delle ancore per tessuti molli è in rapida crescita, trainato dalla crescente domanda da parte degli utenti finali, dovuta a fattori quali l'evoluzione delle preferenze dei consumatori, i progressi tecnologici e una maggiore consapevolezza dei benefici del prodotto. Con l'aumento della domanda, le aziende stanno ampliando la propria offerta, innovando per soddisfare le esigenze dei consumatori e sfruttando le tendenze emergenti, alimentando ulteriormente la crescita del mercato.

- Ottieni una panoramica dei principali attori del mercato delle ancore per tessuti molli

Analisi della quota di mercato degli ancoraggi per tessuti molli per area geografica

Il mercato degli ancoraggi per tessuti molli mostra traiettorie di crescita diverse nelle diverse regioni, influenzate dalla spesa sanitaria, dalla prevalenza dei centri di medicina sportiva e dalle politiche di rimborso ortopedico.

America del Nord

- Quota di mercato: la più grande a livello mondiale, trainata da infrastrutture avanzate di medicina sportiva e dalla forte presenza dei principali produttori.

- Fattori chiave: rimborso favorevole, studi ortopedici specializzati, elevata consapevolezza da parte dei consumatori.

- Tendenze: rapida adozione di ancoraggi senza nodi e biocompositi.

Europa

- Quota di mercato: quota significativa grazie alla solida assistenza sanitaria pubblica e all'adozione dell'artroscopia.

- Fattori chiave: iniziative di formazione medica, domanda di fissazione a lungo termine, efficienza dei costi.

- Tendenze: integrazione di sistemi di fissaggio avanzati nelle procedure della cuffia dei rotatori e dei legamenti.

Asia-Pacifico

- Quota di mercato: regione in più rapida crescita grazie agli investimenti nel settore sanitario.

- Fattori chiave: espansione degli ospedali, aumento del reddito disponibile, sostegno governativo.

- Tendenze: forte crescita dei dispositivi assorbibili e senza nodi in Cina e India.

America meridionale e centrale

- Quota di mercato: mercato emergente con adozione della salute digitale.

- Fattori chiave: accesso alle attrezzature artroscopiche, partenariati pubblico-privati.

- Tendenze: adozione di soluzioni di ancoraggio convenienti da parte dei fornitori di piccole e medie dimensioni.

Medio Oriente e Africa

- Quota di mercato: mercato in via di sviluppo con forte potenziale di crescita.

- Fattori chiave: espansione delle infrastrutture, crescente partecipazione sportiva.

- Tendenze: standardizzazione dei centri ortopedici per le riparazioni complesse dei tessuti molli.

Densità degli operatori del mercato degli ancoraggi per tessuti molli: comprendere il suo impatto sulle dinamiche aziendali

Elevata densità di mercato e concorrenza

Il mercato delle ancore per tessuti molli è caratterizzato da una forte concorrenza, trainata da ingenti investimenti in ricerca e sviluppo da parte di leader del settore ortopedico riconosciuti a livello mondiale. Le principali aziende, tra cui Arthrex, Stryker e Johnson & Johnson (DePuy Synthes), si impegnano costantemente a differenziare la propria offerta in questo panorama affollato.

Questo ambiente competitivo spinge i fornitori a innovare strategicamente attraverso:

- Sviluppo di modelli di ancoraggio senza nodi e interamente suturati di nuova generazione per un'efficienza chirurgica ottimizzata e una guarigione più rapida.

- Concentrandosi sulla scienza dei materiali innovativi, in particolare sui biocompositi e sui materiali PEEK migliorati, per migliorare l'integrazione e ridurre al minimo le reazioni biologiche.

- Offriamo set di prodotti completi che includono ancore, nastri di sutura e kit monouso per supportare procedure artroscopiche semplificate.

- Investire ingenti risorse nella formazione dei chirurghi e in iniziative di educazione medica per promuovere l'adozione dei loro specifici sistemi di fissaggio.

Opportunità e mosse strategiche

- Acquisire o collaborare con aziende innovative più piccole specializzate in rivestimenti biologici o aumento dei tessuti per creare soluzioni di riparazione integrate.

- Sfruttare la tecnologia proprietaria dei materiali per garantire prezzi elevati ed esclusività di mercato nelle procedure di ricostruzione ad alto volume.

Le principali aziende che operano nel mercato degli ancoraggi per tessuti molli sono:

- Smith & Nephew Plc.

- CONMED Corporation

- Johnson & Johnson Services, Inc. (DePuy Synthes)

- Camera Biomet

- Arthrex, Inc.

- Stryker Corporation

- Medtronic

- Cook Medical LLC

- Aju Pharm Co., Ltd.

Disclaimer: le aziende elencate sopra non sono classificate in un ordine particolare.

Notizie di mercato e sviluppi recenti sulle ancore per tessuti molli

- Il 7 luglio 2025, Smith & Nephew Plc ha lanciato l'ancora Q-FIX Knotless All-Suture, che offre una forza di fissaggio superiore e uno spostamento estremamente ridotto per interventi chirurgici su spalla, anca, piede e caviglia. L'ancora è disponibile con nastro di sutura e opzioni ULTRABRAID.

- CONMED Corporation ha presentato l'AlternatiV+ Max Knotless Anchor, un'ancora biodegradabile twist-in con punta in PEEK compatibile con l'impalcatura BioBrace, progettata per la riparazione dei tessuti molli di spalla, gomito, piede, caviglia e ginocchio.

Copertura e risultati del rapporto di mercato sulle ancore per tessuti molli

Il rapporto "Dimensioni e previsioni del mercato degli ancoraggi per tessuti molli (2021-2034)" fornisce un'analisi dettagliata del mercato che copre le seguenti aree:

- Dimensioni e previsioni del mercato degli ancoraggi per tessuti molli a livello globale, regionale e nazionale per tutti i principali segmenti di mercato coperti dall'ambito

- Tendenze del mercato degli ancoraggi per tessuti molli, nonché dinamiche di mercato quali fattori trainanti, vincoli e opportunità chiave

- Analisi PEST e SWOT dettagliate

- Analisi di mercato degli ancoraggi per tessuti molli che copre le principali tendenze del mercato, il quadro globale e regionale, i principali attori, le normative e i recenti sviluppi del mercato

- Analisi del panorama industriale e della concorrenza che copre la concentrazione del mercato, l'analisi della mappa termica, i principali attori e gli sviluppi recenti nel mercato degli ancoraggi per tessuti molli

- Profili aziendali dettagliati

Mrinal è un'analista di ricerca esperta con oltre 8 anni di esperienza nella consulenza e nell'intelligence di mercato nel settore delle scienze biologiche. Grazie a una mentalità strategica e a un costante impegno verso l'eccellenza, ha maturato una profonda competenza nelle previsioni farmaceutiche, nella valutazione delle opportunità di mercato e nello sviluppo di benchmark di settore. Il suo lavoro è incentrato sulla fornitura di insight fruibili che consentono ai clienti di prendere decisioni strategiche consapevoli.

Il punto di forza di Mrinal risiede nella capacità di tradurre complessi set di dati quantitativi in business intelligence significative. Il suo acume analitico è fondamentale per definire strategie di go-to-market (GTM) e individuare opportunità di crescita nei settori farmaceutico e dei dispositivi medici. In qualità di consulente di fiducia, si concentra costantemente sulla semplificazione dei processi di flusso di lavoro e sulla definizione di best practice, promuovendo così l'innovazione e l'efficienza operativa per i suoi clienti.

- Analisi completa delle dimensioni e delle previsioni di mercato

- Analisi dettagliata della segmentazione

- Valutazione approfondita delle dinamiche di mercato

- Approfondimenti a livello regionale e nazionale

- Analisi del panorama competitivo e benchmarking aziendale

- Business intelligence strategica

Testimonianze

Il report di mercato sui sistemi SCADA di Insight Partners è completo, con preziosi spunti sulle tendenze attuali e sulle previsioni future. Il team si è dimostrato altamente professionale, reattivo e disponibile in ogni fase del progetto. Siamo molto soddisfatti e consigliamo vivamente i loro servizi.

RAN KEDEM Partner, Reali Technologies LTDsHo richiesto un report su un mercato software molto specifico e il team lo ha prodotto in pochi giorni. Le informazioni erano molto pertinenti e ben presentate. Ho quindi richiesto alcune modifiche e aggiunte al report. Il team è stato ancora una volta molto reattivo e ho ricevuto il report finale in meno di una settimana.

JEAN-HERVE JENN Presidente, Future AnalyticaAbbiamo collaborato con The Insight Partners per un importante studio di mercato e una previsione. Ci hanno fornito informazioni chiare su opportunità e rischi, che ci hanno aiutato a definire i nostri piani. La loro ricerca è stata facile da usare e basata su dati solidi. Ci ha aiutato a prendere decisioni intelligenti e consapevoli. Li consigliamo vivamente.

PIYUSH NAGPAL Vicepresidente senior, Abbaglianti globaliInsight Partners ha fornito ricerche di mercato approfondite e ben strutturate, con una solida competenza nel settore. Il loro team si è dimostrato professionale e reattivo in ogni fase. Il sito web intuitivo ha reso l'accesso ai report di settore semplice e immediato. Li consigliamo vivamente per servizi di ricerca affidabili e di alta qualità.

YUKIHIKO ADACHI Amministratore delegato, Deep Blue, LLC.Questa è la prima volta che acquisto un report di mercato da The Insight Partners. Sebbene inizialmente fossi indeciso, ho visitato il loro sito web e mi sono sentito più a mio agio nell'acquistare un report di mercato. Sono completamente soddisfatto della qualità del report e del servizio clienti. Avevo diverse domande e commenti sul report iniziale, ma dopo un paio di conversazioni via email con il loro analista credo di avere un report che posso utilizzare come input per il nostro processo di pianificazione strategica. Grazie mille per aver dedicato del tempo extra e aver reso questa esperienza positiva. Consiglierò sicuramente il vostro servizio ad altri e sarete la mia prima persona a cui rivolgermi quando avremo bisogno di ulteriori dati di mercato.

GIOVANNI SUZUKI Presidente e Amministratore Delegato, Consigliere di Amministrazione, Tecnologie BKDesidero esprimere la mia gratitudine per il supporto e la professionalità dimostrati nel rispondere alla mia richiesta di informazioni sul mercato dei dispositivi medici in vitro per malattie infettive in Nigeria. Apprezzo la vostra pazienza, la vostra guida e la vostra disponibilità a offrirmi uno sconto, che alla fine ci ha permesso di concludere l'affare. Non vedo l'ora di collaborare con The Insight Partners in futuro, grazie anche all'impressione che mi avete lasciato dopo questo primo incontro.

Dott. Chijioke AMMINISTRATORE DELEGATO DI ONYIA, PineCrest Healthcare Ltd.Motivo dell'acquisto

- Processo decisionale informato

- Comprensione delle dinamiche di mercato

- Analisi competitiva

- Analisi dei clienti

- Previsioni di mercato

- Mitigazione del rischio

- Pianificazione strategica

- Giustificazione degli investimenti

- Identificazione dei mercati emergenti

- Miglioramento delle strategie di marketing

- Aumento dell'efficienza operativa

- Allineamento alle tendenze normative