2G および 3G スイッチオフ市場戦略、主要プレーヤー、成長機会、分析、2030 年までの予測

2Gおよび3Gスイッチオフ市場の規模と予測(2020年~2030年)、世界および地域シェア、トレンド、成長機会分析レポートの対象範囲:タイプ(2Gおよび3G)およびアプリケーション(メッセージ、音声、データ、IoT)別

- ステータス : 出版

- レポートコード : TIPTE100000785

- カテゴリー : テクノロジー、メディア、通信

- ページ数 : 151

- 利用可能なレポート形式 :

- 最終更新日 : June 12, 2024

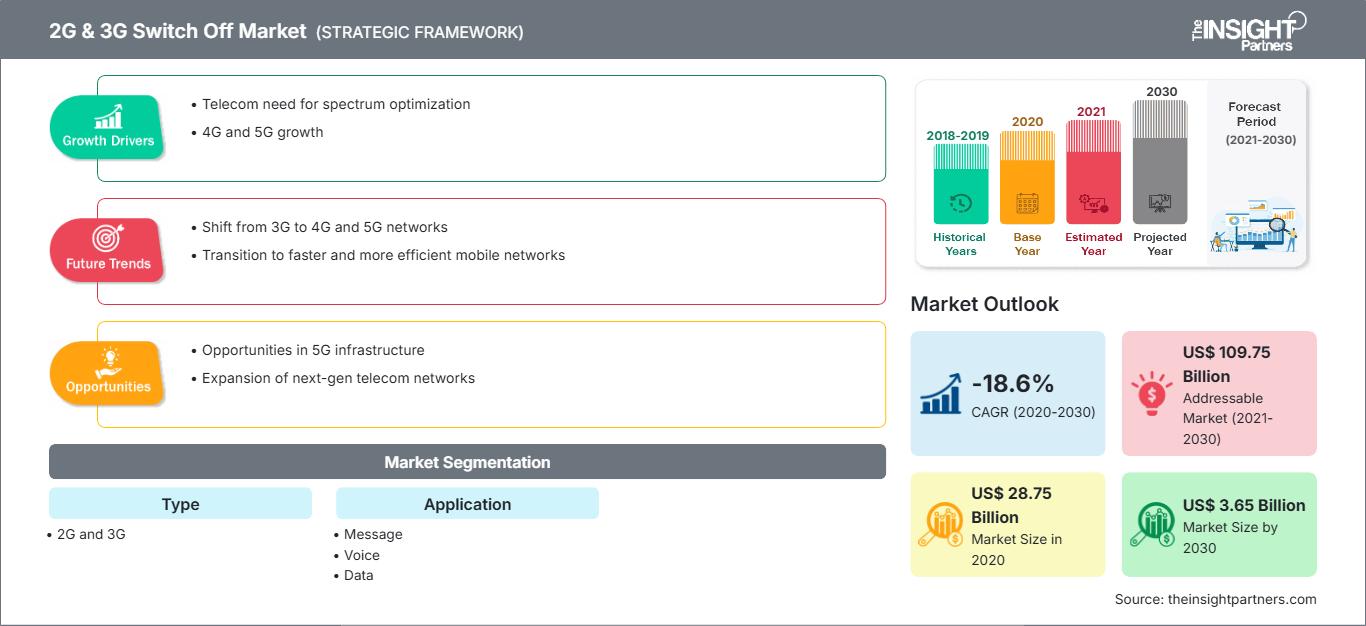

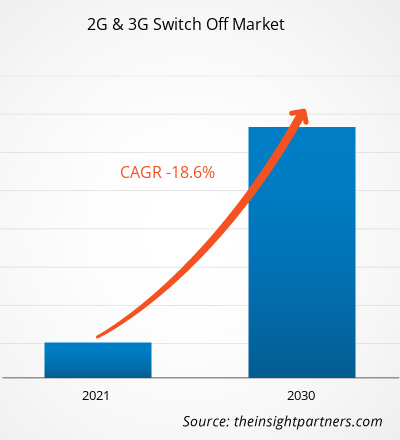

[調査レポート] 2Gおよび3Gスイッチオフ市場規模は、2020年に287億5,000万米ドルと評価され、2030年までに36億5,000万米ドルに減少すると予測されています。また、2020年から2030年にかけて-18.6%のCAGRで成長すると予測されています。

2Gおよび3Gスイッチオフ市場 - アナリストの視点:

5Gの急速な拡大により、モバイルネットワークオペレーター(MNO)は2Gおよび3Gネットワークをシャットダウンし、5G展開用に再利用するようになりました。これが2Gおよび3Gスイッチオフ市場の成長を強力に推進しています。ホームセキュリティやスマートメーターなど、現在のスマートホームデバイスの多くは、2Gおよび3Gネットワークで通信しています。ホームセキュリティシステムは、停電や不正な配線改ざんなどのイベント発生時に監視センターに連絡するために、3Gバックアップコミュニケーターを使用することがよくあります。2Gと3Gは、4Gモジュールよりもコスト効率が高いため、IoTデバイスやマシンツーマシン(M2M)デバイスに適しています。また、データ送信量が少ないIoTデバイスやM2Mデバイスでは、4Gの速度は重要ではありません。セルラーIoTデバイスは常にネットワークに接続されており、モバイル通信によるデータ送信機能は、永続的なローミング状態を維持するM2M加入者識別モジュール(SIM)カードによって実現されています。これにより、異なる通信事業者のモバイルネットワークを利用し、接続を自動的に切り替えて継続的な接続を維持できます。そのため、低速の2Gおよび3G接続でも、今日の基準では十分な速度です。したがって、2Gおよび3Gネットワークの廃止は、2Gまたは3G M2M加入者識別モジュール(SIM)カードに依存するIoTデバイスの接続オプションが制限されることになります。

現在の5Gの展開と将来の6Gの展開が目前に迫っているため、古いテクノロジーの廃止が必要になるため、産業用IoTデバイスは住宅用IoTデバイスよりも影響を受けると予想されます。セルラー接続は、産業用IoT(IIoT)で広範な役割を果たします。組織は、農業、製造、エネルギー、小売、医療、物流などの垂直分野で、さまざまな地理的領域にわたる常時接続を必要とします。デバイスが常に移動している場合、遠隔地に固定されている場合、またはオンデマンドで展開される場合、セルラーが重要になります。対照的に、最新のスマートホームデバイスのほとんどは、家庭用Wi-Fiネットワークを介して接続されています。したがって、2Gおよび3Gの廃止は、スマートホーム/コネクテッドビルディングアプリケーションに最小限の影響しか与えないと予想されます。たとえば、英国におけるスマートメーターの全国展開は、2GベースのM2M接続に大きく依存しています。英国政府の統計によると、2022年には住宅に合計360万台のスマートメーターが設置され、2021年から4%増加しました。英国では、2G(2033年までに完了予定)よりも先に3G(2025年までに完了予定)が廃止されることが、2Gおよび3G廃止市場の成長を後押ししています。しかし、世界的に新しいデバイスを展開するにあたっては、デバイスメーカーは2Gと3Gに続いて4Gも間もなく廃止されることを考慮する必要があります。例えば、SprintのLTEネットワークは2022年6月30日に廃止されました。

要件に合わせてレポートをカスタマイズ

レポートの一部、国レベルの分析、Excelデータパックなどを含め、スタートアップ&大学向けに特別オファーや割引もご利用いただけます(無償)

2Gと3Gのスイッチオフ市場: 戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

2Gおよび3G廃止市場の概要:

旧世代ネットワークに依存し、2G/3G廃止の影響を受けてきたデバイスやサービスは数多くあります。これには、個人の健康レポート、ホームセキュリティ、産業機器の自動化、リアルタイムパフォーマンス、自律操作などが含まれます。これらの分野で使用されているデバイスの多くは、今後数十年にわたって使用されるでしょう。例えば、過去10年間に製造された多くの新車、さらには2021年に製造された新車の中には、3Gで実行されるコネクテッドサービスが搭載されています。これには、位置情報、緊急通報サービス、Wi-Fiホットスポット、リモートロック/ロック解除機能、音声アシスタント、スマートフォンアプリ接続、さらにはコンシェルジュサービスなどが含まれます。さらに、SOSシステムや路側警報もネットワークベースの機能であり、影響を受ける可能性があります。トヨタ、レクサス、日産、ヒュンダイが2019年以前に発売した車両は、この廃止の影響を受けやすいです。

セキュリティシステムは、多くの場合、セルラーネットワーク上で実行されます。 2016 年の初めには、3G ネットワークがセキュリティ パネルで使用される標準通信技術になりました。従来の銅線の固定電話が廃止されるにつれ、メッセージを送信するためにセルラー テクノロジーを使用するワイヤレス セキュリティ システムへの移行が進みました。設置済みの警報システムが 3G 対応の通信機をベースにしている場合、通信事業者が 3G ネットワークを終了し始めると、セキュリティ プロバイダーに関係なく、正常に動作しなくなります。このような場合、セルラー通信機を新しいネットワークで動作するように交換する必要があります。

世界中の複数のネットワーク オペレータが、2023 年までに 2G と 3G を段階的に廃止することを発表しており、2G および 3G スイッチオフ市場の成長を後押ししています。たとえば、この移行が最も顕著なヨーロッパでは、このトレンドを採用した最新のオペレータの 1 つである Orange が、2022 年 8 月の時点で、従来の 2G および 3G を 2025 年から 2030 年にかけて段階的に廃止すると発表しました。

2G および3Gスイッチオフ市場の推進力:

5Gテクノロジーの登場が2Gおよび3Gスイッチオフ市場の成長を促進

台頭中の5Gネットワークは、4Gよりも大容量、低遅延、広帯域を特徴としています。これらのネットワーク強化は、世界中の人々の仕事、生活、遊びに影響を与えると予想されています。Intel Corporationによると、5Gは4Gの最大1,000倍の容量を提供し、IoT開発への道を開きます。5GとIoTは素晴らしい組み合わせで、ワイヤレスネットワークとインターネットの利用方法を再構築する可能性を秘めています。数百または数千のデバイスと簡単に通信できるため、都市、工場、農場、学校、家庭向けの新しいアプリケーションとユースケースが繁栄するでしょう。5Gへの移行は、今後数年間のスマートフォン業界にとって最も重要な成長エンジンとなる可能性があります。 5Gベースのモバイルネットワークの進歩により、低遅延が実現され、仮想現実体験、マルチプレイヤーモバイルゲーム、工場ロボット、自動運転車アプリケーションなど、迅速な応答が強力な基準と見なされる新しい機会への道が開かれます。 このように、5Gテクノロジーの大きな利点により、多くの国がそれを採用しており、2Gおよび3Gスイッチオフ市場の成長を促進しています。

2Gおよび3Gスイッチオフ市場のセグメント分析:

2Gおよび3Gスイッチオフ市場は、タイプとアプリケーションに基づいて分類されています。 タイプに基づいて、2Gおよび3Gスイッチオフ市場は2Gと3Gに分かれています。 3Gセグメントは2020年に大きな市場シェアを占めましたが、2Gセグメントはより急速に減少しています。 アプリケーションの観点から、市場はメッセージ、音声、データ、およびIoTに分割されています。業界が5G対応デバイスに移行しているため、IoTセグメントは最も速いペースで減速しています。 地域別に見ると、2Gおよび3Gスイッチオフ市場は、北米、ヨーロッパ、アジア太平洋(APAC)、中東およびアフリカ(MEA)、南米(SAM)に分割されています。 APACは5Gの導入が最も早く、2Gおよび3Gスイッチオフ市場の減少率も速いです。

通信事業者は2Gおよび3Gネットワークをシャットダウンして4Gおよび5G周波数帯域を解放し、2Gおよび3Gスイッチオフ市場を活性化させています。 ただし、4Gや5Gなどの高速ネットワークをインストールするには、スペクトル、サイト、ファイバーなどの特定のインフラストラクチャが必要であり、これらのインフラストラクチャのインストールにはかなりのコストがかかります。 5G基地局の展開には、土地または屋上スペースの取得、機器の購入と設置、許可の取得、電源とバックホール接続の確保など、多額の初期費用がかかります。これらのコストは、通信事業者と政府の両方にとって障壁となる可能性があります。通信事業者は、5Gに必要な周波数帯域を取得するために、コストのかかるスペクトルオークションに参加する必要があります。これらのオークションコストは、全体的なインフラ支出を増加させます。

5Gネットワークでは、範囲が短く周波数帯域が高いため、より高密度の基地局展開が必要です。したがって、同じエリアをカバーするにはより多くの基地局が必要になり、インフラコストが増加します。それにもかかわらず、5Gには多くの利点があるため、2Gおよび3G技術に取って代わり、驚異的なペースで導入されています。インド、中国、マレーシア、メキシコ、南アフリカ、ブラジルなどの発展途上国では、5Gサブスクリプションの導入率が上昇しており、2Gおよび3Gスイッチオフ市場の成長につながっています。

2Gおよび3Gスイッチオフ市場の地域分析:

APACの2Gおよび3Gスイッチオフ市場は、2Gおよび3Gスイッチオフ市場の地域分析に基づいています。 3Gスイッチオフ市場規模は2020年に37億1,000万米ドルと評価され、2030年までに1億1,000万米ドルに達すると予測されています。また、2022年から2030年にかけてCAGR - -29.4%で成長すると見込まれています。 アジア太平洋地域の2Gおよび3Gスイッチオフ市場は、オーストラリア、インド、中国、日本、韓国、その他のアジア太平洋地域に区分されています。世界的な技術調査およびITアドバイザリ会社のISGによると、アジア太平洋地域の29の事業者が2025年までに2G / 3Gネットワークを廃止すると予測されています。インドは2023年末までに2Gを廃止する予定です。Vodafoneは2022年に2Gを廃止し、日本は2012年に全国的な2G廃止を宣言しました。このような事例はすべて、2Gおよび3Gの普及を促進しています。 3Gスイッチオフ市場の成長。

複数の地域通信事業者が2Gおよび3Gネットワークの停止を進めており、2Gおよび3Gスイッチオフ市場の成長にプラスの影響を与えています。例えば、2021年2月現在、「Vi」ブランドでサービスを提供している通信事業者であるVodafone Idea Ltd(VIL)は、2022年度までにインド国内の全ネットワークで3Gサービスを完全に停止し、4Gに移行しました。このネットワーク事業者は5Gを提供する準備ができています。したがって、この地域での2Gおよび3Gネットワークの複数の停止は、2Gおよび3Gスイッチオフ市場を促進するでしょう。

2G & 3Gスイッチオフ市場における主要プレーヤー分析:

本調査では、AT&T Inc、BCE Inc、China Mobile Ltd、Deutsche Telekom AG、KDDI Corp、NTT Data Corp、Orange SA、Telefonica SA、Telenor ASA、Vodafone Group Plcといった主要2G・3Gスイッチオフ市場プレーヤーをプロファイルしています。さらに、世界の2G・3Gスイッチオフ市場とそのエコシステムの全体像を把握するため、その他の主要2G・3Gスイッチオフ市場プレーヤーについても調査・分析を行いました。

2Gおよび3Gスイッチオフ市場の地域別分析

予測期間を通じて2Gおよび3Gスイッチオフ市場に影響を与える地域的な傾向と要因については、The Insight Partnersのアナリストが詳細に解説しています。このセクションでは、北米、ヨーロッパ、アジア太平洋、中東・アフリカ、中南米における2Gおよび3Gスイッチオフ市場のセグメントと地域についても解説します。

2Gおよび3Gスイッチオフ市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| の市場規模 2020 | US$ 28.75 Billion |

| 市場規模別 2030 | US$ 3.65 Billion |

| 世界的なCAGR (2020 - 2030) | -18.6% |

| 過去データ | 2018-2019 |

| 予測期間 | 2021-2030 |

| 対象セグメント |

By タイプ

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業の概要 |

|

2Gと3Gのスイッチオフ市場におけるプレーヤー密度:ビジネスダイナミクスへの影響を理解する

2Gおよび3Gスイッチオフ市場は、消費者の嗜好の変化、技術の進歩、製品メリットへの認知度の高まりといった要因によるエンドユーザー需要の増加に牽引され、急速に成長しています。需要の増加に伴い、企業は製品ラインナップの拡充、消費者ニーズへの対応のためのイノベーション、そして新たなトレンドの活用を進めており、これが市場の成長をさらに加速させています。

- 入手 2Gと3Gのスイッチオフ市場 主要プレーヤーの概要

2Gおよび3Gスイッチオフ市場の最新動向:

- 2023年12月、O2スロバキアは、利用量の減少と最新の4Gおよび5Gテクノロジーに注力することを理由に、2024年1月から3Gネットワークを段階的に廃止する計画を発表しました。同社は、2024年1月末にスロバキアの指定地域で3Gネットワークのスイッチオフを開始し、今後2年間で段階的に国全体にシャットダウンを拡大します。O2は、4Gおよび5Gテクノロジーの登場により、3Gの利用が大幅に減少し、現在は最小限のレベルに達していると指摘しました。

- 2023年7月、Singtel、StarHub、M1は、2024年7月31日からシンガポールで3Gネットワークをシャットダウンする計画を発表しました。3社とも、5Gサービスを改善するためにスペクトルを再利用します。共同声明の中で、通信事業者らは近年、3Gの顧客に対し4Gまたは5Gサービスへの移行を強く求めており、今後数カ月以内にユーザーが他のネットワークに移行できるよう支援する措置を実施する予定だと指摘した。

アンキタは、テクノロジー、メディア、ICT、エレクトロニクス・半導体の各分野で8年以上の経験を持つ、ダイナミックな市場調査およびコンサルティングのプロフェッショナルです。Microsoft、Oracle、NEC、SAP、KPMG、Expeditors Internationalといったグローバルクライアントに対し、100件以上のコンサルティングおよび調査案件を主導・遂行してきました。彼女のコアコンピテンシーは、市場評価、データ分析、予測、戦略策定、競合情報、レポート作成です。

アンキタは、販売前の提案書作成やクライアントとの協議から、販売後の実用的なインサイトの提供まで、プロジェクトサイクル全体を巧みに管理することに長けています。彼女は、部門横断的なチームの管理、複雑な調査モジュールの構築、そしてクライアント固有のビジネス目標に合わせたソリューションの調整に長けています。優れたコミュニケーション能力、リーダーシップ、そしてプレゼンテーション能力により、急速に変化する市場環境において、常に価値主導の成果を生み出しています。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応