航空宇宙用ファスナー市場戦略、主要プレーヤー、成長機会、分析、2031年までの予測

航空宇宙用ファスナー市場の規模と予測(2021年 - 2031年)、世界および地域別シェア、トレンド、成長機会分析レポートの対象範囲:材料タイプ(超合金、アルミニウム、ステンレス鋼、チタンなど)、用途(機体、エンジン、内装など)、航空機タイプ(固定翼および回転翼)、製品タイプ(ネジ、リベット、ナットまたはボルトなど)、および地域

- ステータス : 出版

- レポートコード : TIPRE00024654

- カテゴリー : 航空宇宙および防衛

- ページ数 : 245

- 利用可能なレポート形式 :

- 最終更新日 : June 02, 2025

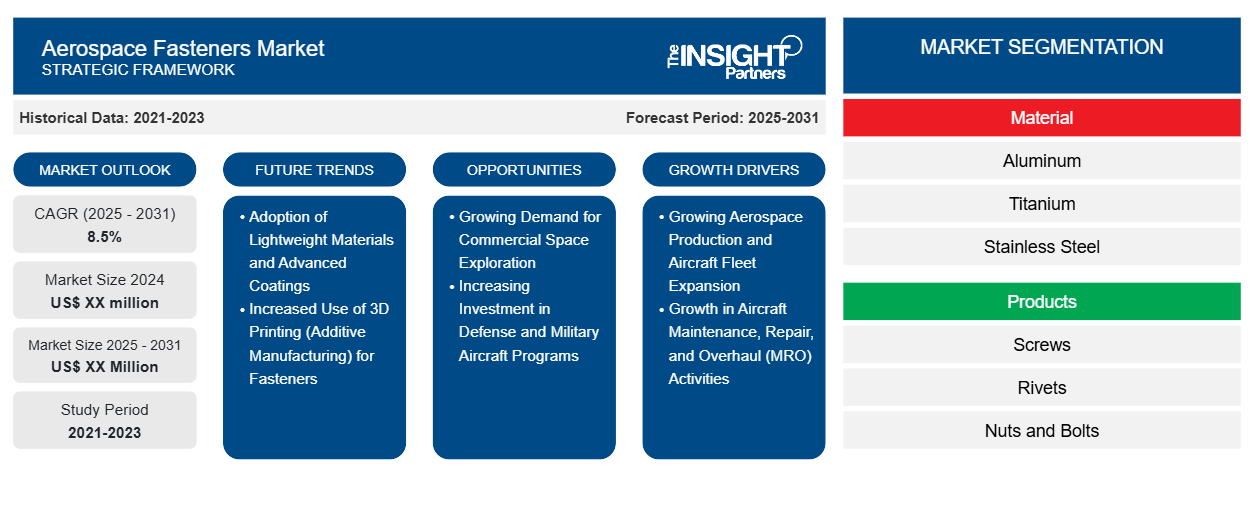

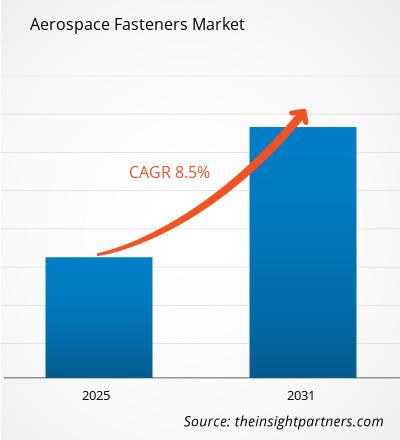

航空宇宙用ファスナー市場規模は、2024年の40億4,412万米ドルから2031年には61億6,115万米ドルに達すると予測されています。市場は2025年から2031年にかけて6.0%の年平均成長率(CAGR)を記録すると予想されています。今後数年間、老朽化した航空機の改修が市場に新たなトレンドをもたらす可能性が高いと考えられます。

航空宇宙用ファスナー市場分析

航空旅客輸送量は拡大しており、航空会社は運航路線の拡大と新機材の導入を進めています。航空機のMRO(メンテナンス・整備)活動は、部品の入手性、一貫性、そして品質の維持に不可欠です。航空会社は、航空機の安全性を確保し、燃費を向上させるためにMROサービスに依存しています。

アジア太平洋地域では、航空機部品の整備・修理の需要が急増しています。航空業界の成長は、中国とインドに集中する可能性があります。シンガポールやマレーシアを含む、その他のアジア太平洋地域の国々は、航空機MROサービスセクターの成長に大きく貢献すると予想されます。

欧州および北米における航空機フリート拡大への投資増加は、これらの地域における航空宇宙用ファスナー市場の成長に貢献しています。さらに、これらの地域の安全性向上と防衛部門の強化を目的とした、軍用・防衛航空機への融資または投資に関する政府の取り組みが増加しています。インド、インドネシア、タイ、シンガポールにおける観光産業の成長は、航空機フリートの需要を刺激しています。

航空宇宙用ファスナー市場の概要

航空宇宙用ファスナーの採用は、世界中で増加する商用機、旅客機、戦闘機によって推進されています。変化する現代戦のシナリオにより、各国政府は防衛および軍用航空部隊に多額の資金と財政援助を割り当てるようになりました。国防費予算の増加は、高まる安全保障上の要件を満たすために政府が高度な戦闘機の調達を重視していることを示しており、これが航空宇宙用ファスナーの需要を押し上げています。2022年、米国政府とロッキード・マーティンは、最大398機のF-35を300億米ドルで生産および納入する契約を締結しました。2023年には、米国はポーランドに120億米ドルのアパッチ攻撃ヘリコプターの販売を確保しました。この契約に基づき、ポーランドはボーイング社から96機のAH-64Eアパッチ攻撃ヘリコプターを受け取る予定です。

商用航空機セグメントにおけるナローボディ機とワイドボディ機の受注増加は、北米、ヨーロッパ、アジア太平洋地域の航空宇宙用ファスナー市場の成長を促進しています。2023年の一般航空の出荷全体は、2022年と比較して増加しました。出荷と予備的な航空機の納入は283億米ドルに達し、約3.3%の増加を記録しました。一般航空機製造業者協会のデータによると、2023年の航空機の出荷は2022年と比較して増加しました。ピストン式航空機の納入は1,682機で約11.8%増加しました。ビジネスジェットの納入は712機から730機に増加し、ターボプロップ機の納入は638機で約9.6%急増しました。航空機の納入額は2023年に234億米ドルで、2022年から約2.2%増加しました。

このレポートの一部、国レベルの分析、Excelデータパックなど、あらゆるレポートを無料でカスタマイズできます。また、スタートアップや大学向けのお得なオファーや割引もご利用いただけます。

航空宇宙用ファスナー市場:戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

航空宇宙用ファスナー市場の推進要因と機会

航空宇宙産業におけるチタンファスナーの利用に伴う利点

チタンファスナーは、航空宇宙産業で最も一般的に使用されている合金です。これらのファスナーは、強度やその他の望ましい特性を高めるために、多くの場合、アルミニウムとバナジウムを主な合金元素とするチタン合金から作られています。高い強度対密度比により、スチールよりも強くて軽量です。また、耐腐食性と高温性能により、航空宇宙産業に最適です。極端な温度と圧力に対する耐性が高いため、着陸装置、ジェットエンジン、ファンブレード、エンジンブレード、シャフト、胴体、翼、プロペラに使用されます。ピンまたはナットの形のチタンファスナーは、航空機アセンブリのコンポーネントを結合するために使用されます。他のどのコンポーネントよりも40%軽量であるため、軽量部品の需要がチタンファスナーの採用を世界中で促進しています。

チタンは極度の温度に耐える性質を持つため、最も過酷な使用条件下における用途が広がります。高熱下でも構造強度を維持できるため、ジェットエンジンの灼熱や大気圏再突入時の摩擦熱に耐えなければならない部品にとって重要な要件となります。一方、極低温への耐性は、宇宙探査において不可欠な要素となっています。宇宙探査では、極寒の宇宙空間が大きな課題となります。海軍航空機では、海霧や海洋大気の腐食性に耐えるため、チタンは構造、着陸装置、留め具などの材料として好まれています。

新興国におけるMRO活動の増加

航空業界の成長は、航空会社のMROサービスの需要を刺激しています。発展途上国、特にアジア太平洋地域の国々は、民間航空機および軍用航空機会社へのMROサービスの拡大に注力しています。アジア太平洋地域の主要な航空機MROビジネスは、MTUメンテナンス、中国のGuangzhou Aircraft Maintenance Engineering Co., Ltd. (GAMECO)、およびExecuJet Haite Aviation Services China Co., Ltd.です。航空インフラへの支出、経済の発展、および急増する乗客数は、航空機整備サービスの採用を促進しています。特にシンガポール、中国、インドにおける中流階級の旅行者の増加は、航空旅行の進化に貢献し、この地域での航空機整備サービスのニーズを高めています。マレーシア、シンガポール、タイは、確立されたMROハブにより、航空MROサービスから多額の収益を生み出しています。エアバス、GEアビエーション、ロールスロイスはシンガポールで大きな存在感を示しています。ウィスコンシン経済開発公社(WEDC)によると、シンガポールには120社の航空宇宙関連企業が拠点を置いており、アジア太平洋地域のMROサービスセクターの4分の1を占めています。ファスナーは、整備作業において航空機の構造的安全性と健全性を確保します。そのため、新興国における航空機の整備、修理、オーバーホール(MRO)サービスへの関心の高まりが、航空宇宙用ファスナー市場の成長を牽引しています。

航空宇宙用ファスナー市場レポート:セグメンテーション分析

航空宇宙用ファスナー市場分析の導出に貢献する主要なセグメントは、材料タイプ、用途、航空機タイプ、および製品タイプです。材料タイプに基づいて、航空宇宙用ファスナー市場は、超合金、アルミニウム、ステンレス鋼、チタン、その他に分類されています。チタンセグメントは2024年に最大の市場シェアを占めました。用途タイプ別に、航空宇宙用ファスナー市場は、機体、エンジン、内装、その他に分類されています。機体セグメントは2024年に最大の市場シェアを占めました。航空機タイプ別に、航空宇宙用ファスナー市場は固定翼と回転翼に分類されています。固定翼セグメントは2024年に最大の市場シェアを占めました。製品タイプ別に、航空宇宙用ファスナー市場は、ネジ、リベット、ナット/ボルト、その他に分類されています。ナット/ボルトセグメントは2024年に最大の市場シェアを占めました。

航空宇宙用ファスナー市場シェア分析(地域別)

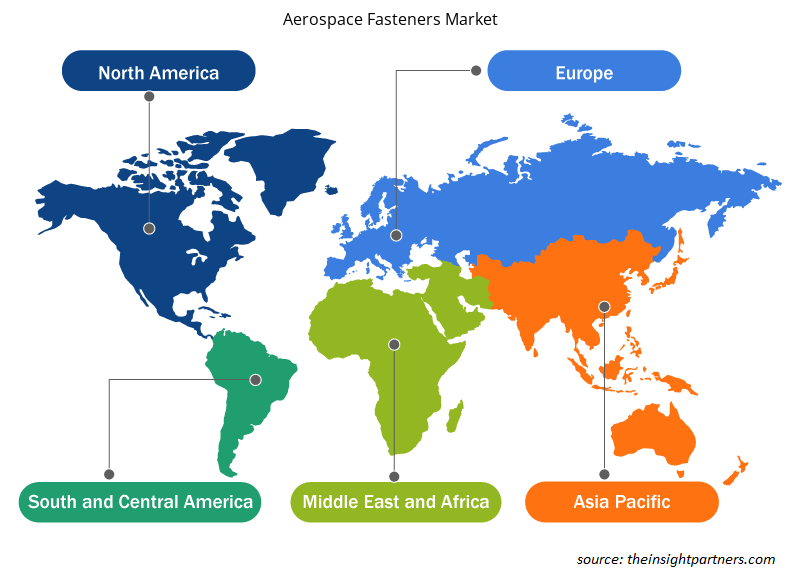

航空宇宙用ファスナー市場レポートの地理的範囲は、北米、ヨーロッパ、アジア太平洋、中東・アフリカ、南米の4つの主要地域に分かれています。世界の航空宇宙用ファスナー市場は、北米、アジア太平洋、ヨーロッパ、中東・アフリカ、南米に分類されています。北米は2024年に35.1%という最大の市場シェアを占め、予測期間中は5.5%の年平均成長率(CAGR)を記録すると予測されています。北米とヨーロッパには、ステンレス鋼および超合金ファスナーのメーカーやサプライヤーが多数存在し、市場の成長を牽引しています。TriMas、Precision Castparts Corp.、Howmet Aerospace Inc.、LISI Aerospace SAS、Saturn Fasteners, Inc.、National Aerospace Fasteners Corp.、Raychin Limitedは、北米、ヨーロッパ、アジア太平洋地域に拠点を置く主要企業です。

2024年6月、エアバスのA330-900飛行試験機(MSN1795/F-WTTN)がメキシコのトルーカ、そしてボリビアのラパスへ飛行しました。この試験は、エアバスの高高度試験キャンペーンの一環でした。エアバスはA350とA330neoの生産増加に注力しており、A330neoベースの貨物機の導入も検討しています。エアバスは2023年に735機の民間航空機を供給しており、これは2022年から約11%の増加となります。エアバスは民間航空機の受注総額2,319件を占め、そのうちA320ファミリーが1,835機、A350ファミリーが300機となっています。ボーイングは2023年に合計528機の航空機を納入し、そのうちボーイング737ジェット機が396機、ドリームライナーが73機となっています。インディゴは2024年5月、地域ネットワークの拡大を目指し、エンブラエル、ATR、エアバスと提携し、約100機の小型機を発注しました。また、航空機の新規生産数の増加とMROサービスの増加により、航空宇宙分野におけるステンレス鋼および超合金製ファスナーの需要は高まっています。

中東、アフリカ、そして南米は、航空宇宙用ファスナー市場の成長に大きく貢献しています。中東連邦航空局(FAA)によると、航空業界は年間10%の成長を遂げています。アフリカ諸国では、航空輸送協定の自由化の進展に伴い航空旅客数が増加しており、航空業界の成長が続いています。IATAは、今後20年間で年間旅客数が約5.9%増加し、2019年と比較して3億人以上の増加となると予測しています。中東およびアフリカの政府は、航空機に先進部品を実装する可能性を認識しており、部品の品質向上に注力しています。

航空宇宙用ファスナー市場の地域別分析

予測期間全体を通して航空宇宙用ファスナー市場に影響を与える地域的な動向と要因は、Insight Partnersのアナリストによって徹底的に解説されています。このセクションでは、北米、ヨーロッパ、アジア太平洋、中東・アフリカ、中南米における航空宇宙用ファスナー市場のセグメントと地域についても解説します。

- 航空宇宙用ファスナー市場の地域別データを入手

航空宇宙用ファスナー市場レポートのスコープ

| レポート属性 | 詳細 |

|---|---|

| 2024年の市場規模 | 40億4,412万米ドル |

| 2031年までの市場規模 | 61億6,115万米ドル |

| 世界のCAGR(2025年~2031年) | 6.0% |

| 履歴データ | 2021-2023 |

| 予測期間 | 2025~2031年 |

| 対象セグメント |

素材の種類別

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業の概要 |

|

航空宇宙用ファスナー市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

航空宇宙用ファスナー市場は、消費者嗜好の変化、技術の進歩、製品メリットへの認知度の向上といった要因によるエンドユーザー需要の増加に牽引され、急速に成長しています。需要の増加に伴い、企業は製品ラインナップの拡充、消費者ニーズへの対応のための革新、そして新たなトレンドの活用を進めており、これが市場の成長をさらに加速させています。

市場プレーヤー密度とは、特定の市場または業界内で事業を展開する企業または会社の分布を指します。これは、特定の市場空間における競合企業(市場プレーヤー)の数が、その市場規模または市場価値全体と比較してどれだけ多いかを示します。

航空宇宙用ファスナー市場で事業を展開している主要企業は次のとおりです。

- プレシジョンキャストパーツ株式会社

- LISIエアロスペースSAS

- トリマス・エアロスペース

- ナショナル エアロスペース ファスナーズ コーポレーション

- ハウメットエアロスペース株式会社

- STANLEYエンジニアードファスニング

免責事項:上記の企業は、特定の順序でランク付けされているわけではありません。

- 航空宇宙用ファスナー市場のトップキープレーヤーの概要を入手

航空宇宙用ファスナー市場のニュースと最近の動向

航空宇宙用ファスナー市場は、主要な企業出版物、協会データ、データベースなどを含む一次調査および二次調査を経て、定性・定量データを収集することで評価されます。航空宇宙用ファスナー市場における動向のいくつかを以下に示します。

- TriMasは、以前に発表していたGMT Gummi-Metall-Technik GmbH(以下「GMT」)の航空宇宙事業の買収を完了したことを発表しました。ドイツに拠点を置くGMTの航空宇宙部門(以下「GMT Aerospace」)は、民間および軍事航空宇宙用途向けに、幅広いタイロッドおよびゴム金属防振システムの開発・製造を行っています。GMT Aerospaceは、TriMas Aerospaceグループの一員となりました。(TriMas、プレスリリース、2025年2月)

- 株式会社メイドーは、ピルグリム・スクリュー・コーポレーション(商号:ピルグリム・エアロスペース・ファスナーズ)を買収しました。(株式会社メイドー、プレスリリース、2024年1月)

- ジェネシス・インダストリーズは、F3エアロスペース(F3)の株式を100%取得したことを発表しました。ジェネシスは、この買収が完了後3ヶ月以内に収益の増加につながると見込んでいます。この取引は、当社の長期目標に沿った株式価値の創出につながるでしょう。(ジェネシス・インダストリーズ、プレスリリース、2024年9月)

航空宇宙用ファスナー市場レポートの対象範囲と成果物

「航空宇宙用ファスナー市場の規模と予測(2021〜2031年)」レポートでは、以下の分野を網羅した市場の詳細な分析を提供しています。

- 航空宇宙用ファスナー市場の規模と予測:対象範囲に含まれるすべての主要市場セグメントの世界、地域、国レベルでの予測

- 航空宇宙用ファスナー市場の動向、および推進要因、制約、主要な機会などの市場動向

- ポーターのファイブフォースとSWOT分析の詳細

- 航空宇宙用ファスナー市場分析では、主要な市場動向、世界および地域の枠組み、主要プレーヤー、規制、最近の市場動向を網羅しています。

- 市場集中、ヒートマップ分析、主要企業の市場シェア分析、航空宇宙用ファスナー市場の最近の動向を網羅した業界の展望と競争分析

- 詳細な企業プロフィール

Naveenは、カスタム、シンジケート、コンサルティングの各プロジェクトにおいて9年以上の実績を持つ、経験豊富な市場調査およびコンサルティングのプロフェッショナルです。現在はアソシエイトバイスプレジデントを務め、プロジェクトバリューチェーン全体にわたるステークホルダー管理を成功させ、100件以上の調査レポートと30件以上のコンサルティング案件を執筆しています。産業および政府機関のプロジェクトに幅広く携わり、クライアントの成功とデータに基づく意思決定に大きく貢献しています。

Naveenは、カルナータカ州VTUで電子通信工学の学位を取得し、マニパル大学でマーケティング&オペレーションズのMBAを取得しています。IEEEの会員として9年間活動し、会議や技術シンポジウムへの参加、セクションレベルおよび地域レベルでのボランティア活動に積極的に取り組んでいます。現職以前は、IndustryARCでアソシエイト戦略コンサルタント、Hewlett Packard(HP Global)で産業用サーバーコンサルタントを務めていました。

- 包括的な市場規模および予測分析

- 詳細なセグメンテーション分析

- 市場動向(ダイナミクス)の徹底的な評価

- 地域および国別のインサイト

- 競争環境および企業ベンチマーク

- 戦略的ビジネスインテリジェンス

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応