オートメーション・アズ・ア・サービス市場の成長、規模、シェア、傾向、主要プレーヤーの分析、2031年までの予測

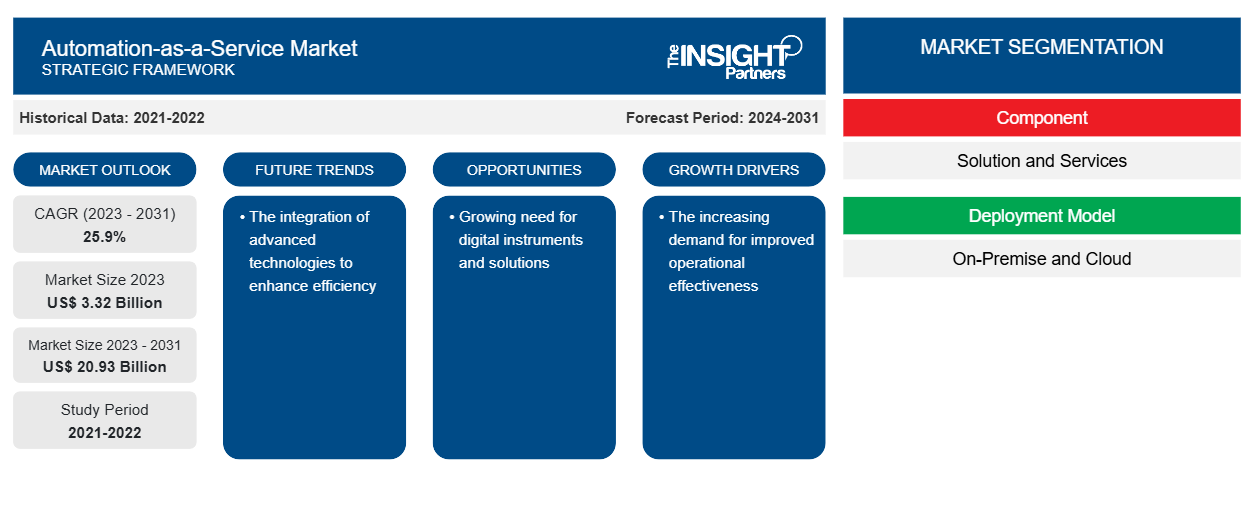

過去データ : 2021-2022 | 基準年 : 2023 | 予測期間 : 2024-2031Automation-as-a-Service 市場の規模と予測 (2021 - 2031)、世界および地域のシェア、トレンド、成長機会分析レポートの対象範囲: コンポーネント別 (ソリューションとサービス)、導入モデル別 (オンプレミスとクラウド)、ビジネス機能別 (営業・マーケティング、財務・運用、人事、情報技術)、業界別 (BFSI、IT・通信、小売、ヘルスケア・ライフサイエンス、運輸・物流、政府機関・防衛、製造、その他)、地域別

- ステータス : 公開されたデータ

- レポートコード : TIPRE00008607

- カテゴリー : テクノロジー、メディア、通信

- ページ数 : 150

- 利用可能なレポート形式 :

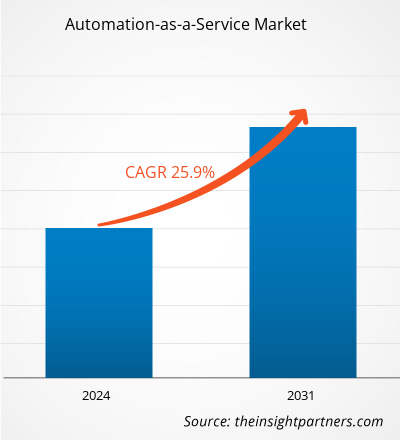

オートメーション・アズ・ア・サービス市場規模は、2023年の33億2,000万米ドルから2031年には209億3,000万米ドルに達すると予測されています。市場は2023年から2031年にかけて25.9%のCAGRを記録すると予想されています。効率性を向上させるための高度なテクノロジーの統合は、今後もオートメーション・アズ・ア・サービス市場の重要なトレンドであり続けると思われます。

オートメーション・アズ・ア・サービス市場分析

AaaS の利用が増えているため、市場は急速に拡大しています。AaaS により、企業は競争力を高め、より価値の高いタスクに集中し、より迅速かつ正確な成果を生み出すことができます。さらに、市場は AaaS の需要増加の影響を受けており、リモート ワーク文化が世界的に拡大しています。これとは別に、業界の投資家は、合理化された手順により紙の廃棄物、エネルギー消費、および炭素排出量を削減することで持続可能性の取り組みをサポートできる AaaS の普及を通じて、収益性の高い成長の見通しを提示されています。さらに、サイバー攻撃に対抗するためのセキュリティ強化の重要性が高まっていることも、市場の拡大を牽引しています。これに伴い、世界中で AaaS プロバイダーの数が増加しているため、市場は成長しています。

オートメーション・アズ・ア・サービス市場の概要

Automation as a Service (AaaS) は、多数のタスクとワークフローを自動化することで、企業がプロセスを最適化し、合理化する柔軟性を提供するクラウドベースのソリューションです。ロボティック プロセス オートメーション (RPA)、機械学習 (ML)、人工知能 (AI) など、最先端のテクノロジーを使用して、複数の部門や機能にわたる時間のかかる反復的な操作を効果的に管理します。さらに、スケーラブルで手頃な価格の自動化ソリューションを提供し、企業が手動介入をなくし、エラー率を下げ、生産性を向上させることを可能にします。

要件に合わせてレポートをカスタマイズする

このレポートの一部、国レベルの分析、Excelデータパックなど、あらゆるレポートを無料でカスタマイズできます。また、スタートアップや大学向けのお得なオファーや割引もご利用いただけます。

オートメーション・アズ・ア・サービス市場:戦略的洞察

-

このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

オートメーション・アズ・ア・サービス市場の推進要因と機会

業務効率の向上に対する需要の高まり

AaaS の利用が増えたことにより市場が拡大しており、さまざまな業界で業務効率の向上と大幅なコスト削減が実現しています。また、時間のかかる反復的なプロセスの自動化も簡単になり、肉体労働の必要性が減ります。これにより、タスクの完了が大幅にスピードアップすると同時に、人的ミスも減ります。その結果、企業はリソースを最大限に活用し、より戦略的なプロジェクトに労働者を割り当て、最終的に生産性を向上させることができます。これに加えて、AaaS ソリューションで時々使用される従量課金制またはサブスクリプション モデルでは、ソフトウェアや機器への多額の先行投資が不要になるため、市場の見通しは明るくなります。この経済的な方法により、あらゆる規模の企業が高度な自動化を利用できるようになります。AaaS, which can improve operational effectiveness and provide significant cost savings to a variety of industries. It also makes it simple to automate time-consuming and repetitive processes, which lessens the need for physical labor. This greatly speeds up task completion while simultaneously reducing human mistakes. Consequently, this allows firms to maximize the use of their resources, assign workers to more strategic projects, and eventually increase productivity. Aside from this, the pay-as-you-go or subscription model that AaaS solutions sometimes use avoids the need for significant upfront investments in software or equipment, which provides a positive market outlook. Advanced automation is accessible to companies of all sizes thanks to this economical method.

デジタル機器とソリューションに対するニーズの高まり

複数の業界でデジタルツールやソリューションの需要が高まっていることから市場が拡大しており、これがAaaSの利用増加につながっています。さまざまな企業がデジタル技術を導入し、それに合わせて業務を更新しています。企業は、変化する業務プロセスに簡単に適合する製品やサービスを必要としています。それに加え、AaaSはデジタル活動を強化する自動化機能を提供するため、この目標に最適です。さらに、AaaSを利用することで、企業はサプライチェーン管理や顧客サポートなど、さまざまな機能を自動化できます。この統合により、データに基づく意思決定がサポートされ、効率性の向上に加えて顧客体験が向上します。したがって、IoTの採用拡大により、予測期間中にオートメーション・アズ・ア・サービス市場のプレーヤーに新たな機会がもたらされると予想されます。AaaS. Various businesses are implementing digital technology and updating their operations in accordance with this. They need products and services that can easily fit into their changing work processes. Aside from that, AaaS is a fantastic fit for this goal because it provides AaaS enables businesses to automate a range of functions, including supply chain management and customer support. This integration supports data-driven decision-making and boosts client experiences in addition to increasing efficiency. Thus, the increasing adoption of IoT is anticipated to present new opportunities for the automation-as-a-service market players during the forecast period.

オートメーション・アズ・ア・サービス市場レポートのセグメンテーション分析

オートメーション・アズ・ア・サービス市場分析の導出に貢献した主要なセグメントは、コンポーネント、展開モデル、ビジネス機能、および業界垂直です。

- コンポーネントに基づいて、サービスとしての自動化市場はソリューションとサービスに分類されます。

- 展開モデル別に見ると、市場はオンプレミスとクラウドに分かれています。クラウドセグメントは2023年に大きな市場シェアを占めました。

- ビジネス機能に基づいて、サービスとしての自動化市場は、販売とマーケティング、財務と運用、人事、情報技術に分類されます。

- 業界別では、オートメーション・アズ・ア・サービス市場は、BFSI、IT および通信、小売、ヘルスケアおよびライフサイエンス、輸送および物流、政府機関および防衛、製造、業界別、その他に分類されます。BFSI, IT & telecom, retail, healthcare & life sciences, transportation & logistics, government agencies & defense, manufacturing, industry vertical, and others.

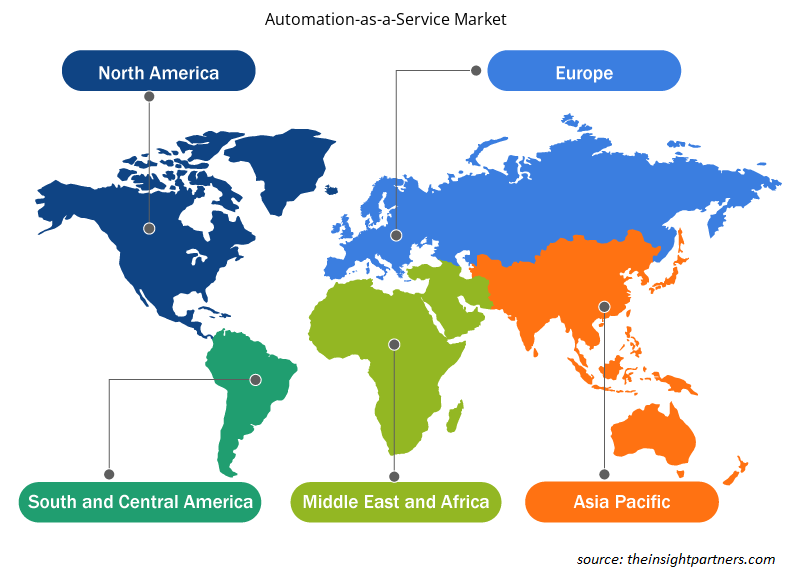

地域別オートメーション・アズ・ア・サービス市場シェア分析

オートメーション・アズ・ア・サービス市場レポートの地理的範囲は、主に北米、アジア太平洋、ヨーロッパ、中東およびアフリカ、南米/中南米の 5 つの地域に分かれています。収益の面では、北米がオートメーション・アズ・ア・サービス市場で最大のシェアを占めています。この地域の市場は、特にヘルスケアや銀行などの分野でのオートメーションの利用増加により拡大しています。これに加えて、業務の簡素化と経費の節約に対する企業の需要の高まりにより、好ましい市場見通しが提供されています。したがって、データ セキュリティに対する需要の高まりが、北米地域での市場の拡大を促進しています。

オートメーション・アズ・ア・サービス市場の地域別分析

予測期間を通じて Automation-as-a-Service 市場に影響を与える地域的な傾向と要因は、Insight Partners のアナリストによって徹底的に説明されています。このセクションでは、Automation-as-a-Service 市場のセグメントと、北米、ヨーロッパ、アジア太平洋、中東、アフリカ、南米、中米の地域についても説明します。

- オートメーション・アズ・ア・サービス市場の地域別データを入手

オートメーション・アズ・ア・サービス市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2023年の市場規模 | 33億2千万米ドル |

| 2031年までの市場規模 | 209.3億米ドル |

| 世界のCAGR(2023年~2031年) | 25.9% |

| 履歴データ | 2021-2022 |

| 予測期間 | 2024-2031 |

| 対象セグメント |

コンポーネント別

|

| 対象地域と国 |

北米

|

| 市場リーダーと主要企業プロフィール |

|

オートメーション・アズ・ア・サービス市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

Automation-as-a-Service 市場は、消費者の嗜好の変化、技術の進歩、製品の利点に対する認識の高まりなどの要因により、エンドユーザーの需要が高まり、急速に成長しています。需要が高まるにつれて、企業は提供内容を拡大し、消費者のニーズを満たすために革新を起こし、新たなトレンドを活用し、市場の成長をさらに促進しています。

市場プレーヤー密度とは、特定の市場または業界内で活動している企業または会社の分布を指します。これは、特定の市場スペースに、その市場規模または総市場価値に対してどれだけの競合相手 (市場プレーヤー) が存在するかを示します。

Automation-as-a-Service 市場で事業を展開している主要企業は次のとおりです。

- アクセンチュア

- オートメーション・エニウェア株式会社

- ブループリズムグループ

- HCLテクノロジーズリミテッド

- ヒューレット・パッカード・エンタープライズ

- IBMコーポレーション

免責事項:上記の企業は、特定の順序でランク付けされていません。

- オートメーション・アズ・ア・サービス市場のトップキープレーヤーの概要を入手

オートメーション・アズ・ア・サービス市場のニュースと最近の動向

自動化サービス市場は、主要な企業出版物、協会データ、データベースなどの一次調査と二次調査後の定性的および定量的データを収集することで評価されます。以下は、音声および言語障害の市場と戦略の動向の一覧です。

- 2024 年 1 月、Automation Anywhere は、企業がプロセス自動化の導入によるビジネス価値を評価し、最大化できるよう支援する一連の新しいベンチマーク サービスと新しい顧客ベンチマーク データベース イニシアチブを発表しました。これらのサービスにより、企業は業界における「最善の」自動化がどのようなものかを把握し、独自に決定するよりも迅速に、最も価値の高い自動化の優先順位を決定できるようになります。(出典: Automation Anywhere、プレス リリース)

- 2022 年 3 月、人を中心とした組織向けのエンタープライズ クラウド アプリケーションのリーダーである Unit4 は、顧客が人工知能とコンテキスト認識機能を活用して効率と生産性を向上できるようにするスマート オートメーション サービスの立ち上げを発表しました。これらのサービスは、Unit4 の次世代エンタープライズ リソース プランニング スイートである ERPx とその仮想アシスタントと統合され、ビジネス プロセスをさらに合理化します。これらのサービスを活用することで、ERPx はタスクの大部分を自動化し、最適化されカスタマイズされた、簡単なユーザー エクスペリエンスを実現できます。(出典: Unit4、プレス リリース)

Automation-as-a-Service 市場レポートの対象範囲と成果物

「Automation-as-a-Service 市場規模と予測 (2023~2031 年)」レポートでは、以下の分野をカバーする市場の詳細な分析を提供しています。

- 対象範囲に含まれるすべての主要市場セグメントの世界、地域、国レベルでの市場規模と予測

- 市場の動向(推進要因、制約、主要な機会など)

- 今後の主な動向

- 詳細なPEST/ポーターの5つの力とSWOT分析

- 主要な市場動向、主要プレーヤー、規制、最近の市場動向を網羅した世界および地域の市場分析

- 市場集中、ヒートマップ分析、主要プレーヤー、最近の動向を網羅した業界の状況と競争分析

- 詳細な企業プロフィール

アンキタは、テクノロジー、メディア、ICT、エレクトロニクス・半導体の各分野で8年以上の経験を持つ、ダイナミックな市場調査およびコンサルティングのプロフェッショナルです。Microsoft、Oracle、NEC、SAP、KPMG、Expeditors Internationalといったグローバルクライアントに対し、100件以上のコンサルティングおよび調査案件を主導・遂行してきました。彼女のコアコンピテンシーは、市場評価、データ分析、予測、戦略策定、競合情報、レポート作成です。

アンキタは、販売前の提案書作成やクライアントとの協議から、販売後の実用的なインサイトの提供まで、プロジェクトサイクル全体を巧みに管理することに長けています。彼女は、部門横断的なチームの管理、複雑な調査モジュールの構築、そしてクライアント固有のビジネス目標に合わせたソリューションの調整に長けています。優れたコミュニケーション能力、リーダーシップ、そしてプレゼンテーション能力により、急速に変化する市場環境において、常に価値主導の成果を生み出しています。

- 過去2年間の分析、基準年、CAGRによる予測(7年間)

- PEST分析とSWOT分析

- 市場規模価値/数量 - 世界、地域、国

- 業界と競争環境

- Excel データセット

お客様の声

Insight PartnersのSCADAシステム市場レポートは包括的で、現在のトレンドと将来の予測に関する貴重な洞察が含まれています。チームは終始、非常にプロフェッショナルで、対応が早く、サポートも充実していました。私たちは彼らのサービスに非常に満足しており、強くお勧めします。

ラン・ケデム パートナー, レアリテクノロジーズ株式会社非常に特殊なソフトウェア市場に関するレポートを依頼したところ、チームは数日でレポートを作成してくれました。情報は非常に関連性が高く、分かりやすくまとめられていました。その後、レポートにいくつか修正と追加を依頼しましたが、チームは非常に迅速に対応し、1週間も経たないうちに最終レポートを受け取ることができました。

ジャン=エルヴェ・ジェン 会長, フューチャー・アナリティカ重要な市場調査と予測のために、The Insight Partnersと協力しました。彼らは機会とリスクに関する明確な洞察を提供し、私たちの計画策定に役立ちました。彼らの調査は使いやすく、確かなデータに基づいており、賢明で自信に満ちた意思決定に役立ちました。彼らを強くお勧めします。

ピユーシュ・ナグパル 上級副社長, ハイビームグローバルInsight Partnersは、深い専門知識に基づき、洞察力に富み、構造化された市場調査を提供しました。チームは終始プロフェッショナルで、対応力も抜群でした。ユーザーフレンドリーなウェブサイトにより、業界レポートへのアクセスもスムーズでした。信頼性の高い高品質な調査サービスをお探しなら、Insight Partnersを強くお勧めします。

安達幸彦 最高経営責任者(CEO), ディープブルーLLC。The Insight Partnersから市場レポートを購入するのは今回が初めてです。最初は不安でしたが、ウェブサイトを見て、リスクを負ってでも購入してみようという気持ちになりました。レポートの品質とカスタマーサービスには大変満足しています。最初のレポートにはいくつか質問やコメントがありましたが、アナリストとメールで何度かやり取りした結果、戦略策定プロセスへのインプットとして活用できるレポートが完成しました。貴重なお時間を割いていただき、貴重な体験をさせていただき、誠にありがとうございました。他の方にもぜひお勧めしたいですし、今後さらに市場データが必要になった際には、まずThe Insight Partnersにご連絡させていただきます。

ジョン・スズキ 社長兼最高経営責任者、取締役, BKテクノロジーズナイジェリアの感染症IVD市場に関する情報提供依頼に対し、ご対応いただいた際、ご尽力とプロフェッショナルな姿勢に深く感謝申し上げます。忍耐強く、的確なアドバイスをいただき、また、最終的に取引成立に至った割引のご提供にも深く感謝申し上げます。今回の最初の出会いで得た強い印象のおかげで、今後もThe Insight Partnersとの連携を心待ちにしております。

チジオケ博士 オニア マネージングディレクター, パインクレストヘルスケア株式会社購入理由

- 情報に基づいた意思決定

- 市場動向の理解

- 競合分析

- 顧客インサイト

- 市場予測

- リスク軽減

- 戦略計画

- 投資の正当性

- 新興市場の特定

- マーケティング戦略の強化

- 業務効率の向上

- 規制動向への対応

無料サンプルを入手 - オートメーション・アズ・ア・サービス市場

無料サンプルを入手 - オートメーション・アズ・ア・サービス市場