2,5-Furandicarboxylic Acid Market Size, Growth & Trends by 2034

2, 5-Furandicarboxylic Acid Market Size and Forecasts (2021 - 2034), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Application (Polyamides, Polyesters, Plasticizers, Polycarbonates, Others) , and Geography (North America, Europe, Asia Pacific, and South and Central America)

Historic Data: 2021-2024 | Base Year: 2025 | Forecast Period: 2026-2034- Status : Data Released

- Report Code : TIPRE00021612

- Category : Chemicals and Materials

- No. of Pages : 150

- Available Report Formats :

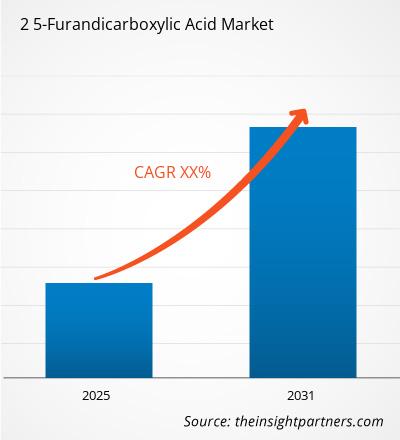

The global 2,5-Furandicarboxylic Acid (FDCA) market size is projected to reach US$ 3,860.00 million by 2034 from US$ 1,930.33 million in 2025. The market is anticipated to register a CAGR of 8.00% during the forecast period 2026–2034.

Key market dynamics include an accelerating global transition toward bio-based platform chemicals, rising industrial demand for Polyethylene Furanoate (PEF) as a superior alternative to PET, and stringent government regulations targeting the reduction of fossil-based plastic carbon footprints. Additionally, the market is expected to benefit from breakthroughs in catalytic oxidation processes, significant capacity expansions by bio-refinery leaders, and the increasing adoption of FDCA in high-performance applications such as automotive engineering and specialty textiles.

2,5-Furandicarboxylic Acid Market Analysis

The 2,5-Furandicarboxylic Acid market analysis reveals a strategic pivot from pilot-scale research to large-scale commercialization, particularly in the production of 100% bio-based polymers. The market trends indicate a massive shift in the packaging and beverage industries, where FDCA-derived PEF is favored for its superior oxygen and carbon dioxide barrier properties, which extend product shelf life. Strategic opportunities are emerging in the pharmaceutical and nutraceutical industries, where FDCA is being explored as a sustainable building block for drug delivery systems and active pharmaceutical ingredients. The analysis also notes that market expansion is heavily reliant on the cost-efficiency of biomass conversion, specifically the dehydration of C6 sugars into 5-HMF, and the stability of heterogeneous catalysts. Competitive differentiation now hinges on green-tier branding, where companies highlight the lifecycle carbon reduction of their products and the use of non-food crop feedstocks to avoid competition with the food supply chain.

2,5-Furandicarboxylic Acid Market Overview

Bio-based chemicals have evolved from niche laboratory curiosities to essential industrial commodities. The FDCA encompasses a wide range of derivatives, including polyesters, polyamides, and plasticizers. Both established chemical giants and specialized biotech startups compete in this market, utilizing renewable feedstocks such as corn, sugarcane, and lignocellulosic biomass. Growing demand for sustainable packaging in North America and Europe has catalyzed the adoption of FDCA as a Top 12 value-added chemical from biomass. Europe currently leads in market share due to robust Green Deal policies, while Asia-Pacific is advancing rapidly through massive industrial investments in China and Thailand. The US market is characterized by high innovation in FDCA-based engineering plastics and a broad push for domestic bio-manufacturing. Competition is fueling the development of continuous-flow reactor technologies to lower the currently high production premiums compared to petroleum-derived terephthalic acid.

Market Assessment and Insights

- Global market for 2, 5-Furandicarboxylic Acid was valued at US$ 1,930.33 Million in 2025

- Annual market size is expected to reach US$ 3,860.00 Million by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 26,033.52 Million

- Market is anticipated to register a CAGR of 8% during the forecast period

- The United States represents a key market, supported by Unlocking Sustainable Solutions: 5-Furandicarboxylic Acid's Rise, Innovative Applications Propel 5-Furandicarboxylic Acid Demand, Green Chemistry Revolution: 5-Furandicarboxylic Acid Leads the Way, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Sustainable Materials: 5-Furandicarboxylic Acid Takes Center Stage, Bioplastics Revolution: The Rise of 5-Furandicarboxylic Acid, Green Chemistry: 5-Furandicarboxylic Acid Fuels Eco-Friendly Innovations are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Tokyo Chemical Industry Co., Ltd., R and D Synbias Ltd, Eastman Chemical Company, SATACHEM, Toronto Research Chemicals Inc., Avantium Technologies, Biosynth Carbosynth, Alfa Aesar GmbH and Co KG, Toronto Research Chemicals Inc, Corbion NV, while analyzing competitive strategies and innovation developments

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATION2, 5-Furandicarboxylic Acid Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

2,5-Furandicarboxylic Acid Market Drivers and Opportunities

Market Drivers:

- Superior Gas Barrier Properties of PEF: FDCA is the primary monomer for PEF, which offers 10x better oxygen barriers and 2x better moisture barriers than traditional PET. This performance advantage, combined with recyclability, is a major driver for the beverage and food packaging sectors.

- Stringent Decarbonization Mandates: Global policies, such as the EU’s Circular Economy Action Plan, are forcing manufacturers to replace fossil-based aromatics with bio-based alternatives, directly benefiting the FDCA demand curve.

- Advancements in Catalytic Efficiency: Recent shifts toward non-noble metal catalysts and continuous-flow chemistry are reducing manufacturing overheads, making FDCA more price-competitive with conventional petrochemicals.

Market Opportunities:

- Expansion into Automotive and Electronics: FDCA-based polyamides and polycarbonates offer enhanced thermal stability and mechanical strength, presenting significant growth opportunities in lightweight vehicle components and heat-resistant electronic housings.

- High-Growth Asia-Pacific Manufacturing Hubs: Strategic partnerships between Western technology providers and Asian chemical producers are opening doors to high-volume manufacturing that requires sustainable textile fibers.

- Development of Green Plasticizers: There is a growing opportunity to replace phthalate-based plasticizers, often under regulatory scrutiny, with FDCA-derived alternatives in medical tubing and consumer products.

2,5-Furandicarboxylic Acid Market Report Segmentation Analysis

The 2,5-Furandicarboxylic Acid Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in industry reports:

By Application:

- Bioplastics: The largest and most dominant segment, primarily focused on the production of Polyethylene Furanoate (PEF) for sustainable bottles, films, and containers.

- Resins and Coatings: A high-growth niche where FDCA-based resins offer superior UV resistance and durability for architectural and industrial protective coatings.

By End-User Industry:

- Packaging Industry: Remains the primary volume driver due to the urgent need for recyclable, bio-based alternatives to traditional PET in the food and beverage industry.

- Automotive Industry: An emerging segment utilizing FDCA-based polyamides for engine components and interior parts to reduce vehicle weight and carbon footprint.

By Formulation:

- Granules and Powders: The standard commercial form for large-scale industrial use, facilitating easy transport and integration into existing plastic manufacturing extrusion lines.

- Concentrated Solutions: Specialized formulations used in high-precision chemical synthesis and liquid-phase coating applications.

By Production Technology:

- Chemical Synthesis: The most established route involving the catalytic oxidation of 5-HMF, currently favored for high-purity industrial outputs.

- Biosynthesis: An emerging, highly sustainable route utilizing engineered microbes or enzymes to convert sugars directly into FDCA, aimed at reducing the heat and pressure requirements of traditional chemical methods.

By Distribution Channel:

- Direct Sales: The primary channel for high-volume offtake agreements between chemical producers and major brand owners or large-scale plastic converters.

- Distributors: Provides access to small and medium-sized enterprises (SMEs) and research institutions requiring smaller quantities for specialty applications.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

2, 5-Furandicarboxylic Acid Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 1,930.33 Million |

| Market Size by 2034 | US$ 3,860.00 Million |

| Global CAGR (2026 - 2034) | 8.00% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Application

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

2, 5-Furandicarboxylic Acid Market Players Density: Understanding Its Impact on Business Dynamics

The 2, 5-Furandicarboxylic Acid Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

2,5-Furandicarboxylic Acid Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for bio-based chemical producers and green packaging manufacturers to expand.

The 2,5-Furandicarboxylic Acid market is undergoing a significant transformation, moving from a laboratory-scale specialty chemical to a global high-value building block for sustainable plastics. Growth is driven by the rising demand for 100% recyclable bioplastics, a surge in fossil-free material requirements, and the expansion of the high-performance PEF (Polyethylene Furanoate) sector. Below is a summary of market share and trends by region:

1. North America

- Market Share: A robust and technology-driven segment, driven by industrial R&D and the presence of major beverage brand owners.

- Key Drivers:

- Strong corporate commitments from FMCG leaders to transition from PET to bio-based PEF

- Significant investment in domestic bio-refinery infrastructure and 5-HMF conversion technologies

- Government incentives for bio-based manufacturing and carbon footprint reduction

- Trends: Scaling of industrial-grade powders for the automotive sector and the successful adoption of FDCA in high-performance coatings for the construction industry.

2. Europe

- Market Share: Holds the largest share globally, anchored by the world’s first commercial-scale FDCA production facilities in the Netherlands and Italy.

- Key Drivers:

- Strict regulatory frameworks such as the EU Single-Use Plastics Directive and Circular Economy Action Plan

- Established ecosystem of bio-based chemistry pioneers and academic research clusters

- High consumer awareness and willingness to pay a premium for sustainable packaging

- Trends: A strategic shift toward fully integrated supply chains that convert agricultural waste into high-purity FDCA. There is also an increasing focus on second-generation feedstocks to meet strict sustainability criteria.

3. Asia-Pacific

- Market Share: The fastest-growing region, with China and Thailand acting as the primary manufacturing for global export.

- Key Drivers:

- Massive industrial capacity expansion and government-supported green chemistry initiatives

- Rising demand from the regional textile industry for bio-based polyester fibers

- Rapid urbanization and the presence of the world’s largest consumer base for bottled beverages

- Trends: Heavy reliance on direct sales models and B2B contracts for high-volume FDCA supply used in the electronics and automotive industries.

4. South and Central America

- Market Share: Emerging market with significant potential due to the vast availability of sugarcane and biomass feedstocks.

- Key Drivers:

- Abundant raw materials for first-generation sugar-to-FDCA conversion

- Modernization of the regional chemical sector to produce high-value exports

- Trends: Growth of boutique bio-plastic ventures and the introduction of FDCA-based resins for the regional maritime and protective coatings markets.

5. Middle East and Africa

- Market Share: Developing market focusing on economic diversification and the reduction of reliance on traditional petrochemicals.

- Key Drivers:

- Strategic investments in smart manufacturing and green industrial zones

- High demand for advanced materials with superior thermal stability for local climates

- Government-led initiatives to establish bio-manufacturing hubs as part of national sustainability visions

- Trends: Implementation of advanced catalytic oxidation technologies to formalize local bio-chemical production, coupled with a focus on FDCA-based plasticizers for the construction segment.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Avantium, Origin Materials, and Corbion. Regional experts and specialized chemical innovators also contribute to a diverse and rapidly expanding market landscape.

This competitive environment pushes vendors to differentiate through:

- Premiumization and functional branding: Positioning FDCA as a superior structural upgrade to traditional fossil-based monomers by emphasizing its 10x better gas barrier properties and 100% bio-based origin.

- Integrated Supply Chains: Producers managing the conversion from biomass to 5-HMF and finally to high-purity FDCA to ensure quality, transparency, and ethical clean-label standards.

- Processing Technology: Utilizing AI and advanced catalysis to optimize reaction conditions, reducing waste and increasing yields.

Opportunities and Strategic Moves

- Partner with global beverage and textile giants to secure long-term offtake agreements, tapping into the surging demand for 100% bio-based and recyclable PEF packaging in the European and Asian markets.

- Incorporate second-generation feedstock technologies and carbon-capture-integrated manufacturing to appeal to environmentally conscious regulators and investors seeking carbon-negative material solutions.

Major Companies operating in the 2,5-Furandicarboxylic Acid Market are:

- Tokyo Chemical Industry Co., Ltd.

- R and D Synbias Ltd

- Eastman Chemical Company

- SATACHEM

- Toronto Research Chemicals Inc.

- Avantium Technologies

- Biosynth Carbosynth

- Alfa Aesar GmbH and Co KG

- Toronto Research Chemicals Inc

- Corbion NV

Disclaimer: The companies listed above are not ranked in any particular order.

2,5-Furandicarboxylic Acid Market News and Recent Developments

- In April 2026, GS Biomats signed a kiloton-level supply agreement with Henan Yinjinda Group, marking one of the largest commercial deals for bio-derived plastic ingredients in Asia. The contract covers 2,5-Furandicarboxylic acid (FDCA), a chemical building block used to make bio-based plastics. FDCA can replace petroleum-derived components in packaging materials and fibers.

- In February 2026, Avantium N.V., a pioneer in renewable and circular polymers, and Will & Co B.V., a distributor of specialty chemicals, launched a collaboration to accelerate the use of FDCA (furandicarboxylic acid) in Coatings, Adhesives, Sealants, and Elastomers (CASE). FDCA is a versatile, bio‑based building block that enhances the performance of synthetic materials - including alkyd resins, surfactants, and polyester polyols - used in everyday applications such as paints, adhesives, flooring, roofing, tubing, automotive components, and construction materials. This partnership leverages Will & Co’s strong position and expertise in the CASE industry and Avantium’s patented YXY® Technology to produce and promote FDCA as a sustainable, bio-based chemical building block.

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Unlock Exclusive Report Discounts

Enquire Now

Get Free Sample For

Get Free Sample For