3D Printing In Healthcare Market Growth, Trends, and Analysis by 2031

3D Printing in Healthcare Market Size and Forecasts (2021 - 2031), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Component (System and Material); Type (Selective Laser Sintering, Photopolymerization, Thermal Inkjet Printers, Fused Deposition Modeling, Stereo lithography, Electron Beam Melting and Others); and Application (Tissues & Organs, Implants & Prostheses, Orthopedics, Hearing Aids, Drug Delivery Devices and Others), and Geography (North America, Europe, Asia Pacific, and South and Central America)

Historic Data: 2021-2023 | Base Year: 2024 | Forecast Period: 2025-2031- Status : Data Released

- Report Code : TIPTE100000717

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

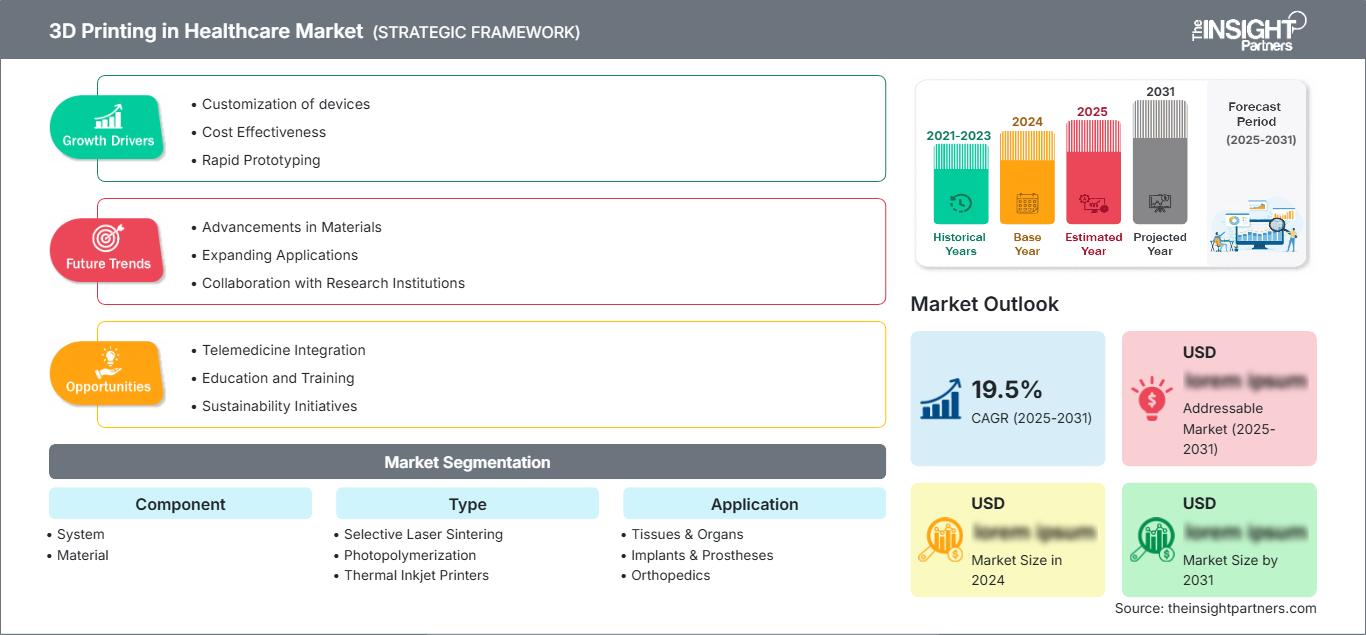

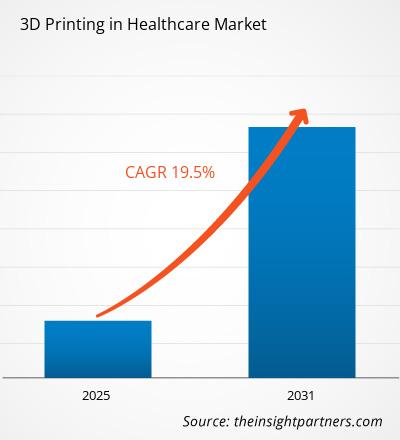

The 3D Printing In Healthcare Market size is expected to reach US$ 21.14 Billion by 2031. The market is anticipated to register a CAGR of 18.3% during 2025-2031.

The report is segmented by Component (System, and Material). The report further presents analysis based on the vascular grafts type Type (Selective Laser Sintering, Photopolymerization, Thermal Inkjet Printers, Fused Deposition Modeling, Stereo lithography, Electron Beam Melting, and Others). Further, the market is segmented on the basis of Application (Tissues & Organs, Implants & Prostheses, Orthopedics, Hearing Aids, Drug Delivery Devices, and Others). The global analysis is further broken-down at regional level and major countries. The Report Offers the Value in USD for the above analysis and segments.

Purpose of the Report

The report 3D Printing in Healthcare Market by The Insight Partners aims to describe the present landscape and future growth, top driving factors, challenges, and opportunities. This will provide insights to various business stakeholders, such as:

- Technology Providers/Manufacturers: To understand the evolving market dynamics and know the potential growth opportunities, enabling them to make informed strategic decisions.

- Investors: To conduct a comprehensive trend analysis regarding the market growth rate, market financial projections, and opportunities that exist across the value chain.

- Regulatory bodies: To regulate policies and police activities in the market with the aim of minimizing abuse, preserving investor trust and confidence, and upholding the integrity and stability of the market.

3D Printing in Healthcare Market Segmentation Component

- System

- Material

Type

- Selective Laser Sintering

- Photopolymerization

- Thermal Inkjet Printers

- Fused Deposition Modeling

- Stereo lithography

- Electron Beam Melting

- Others

Application

- Tissues & Organs

- Implants & Prostheses

- Orthopedics

- Hearing Aids

- Drug Delivery Devices

- Others

Geography

- North America

- Europe

- Asia-Pacific

- South and Central America

- Middle East and Africa

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATION3D Printing in Healthcare Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

3D Printing in Healthcare Market Growth Drivers

- Customization of devices: 3D printing allows for development of personalized medical solutions such as custom prosthetics and implants tailored to individual patient anatomy. Increasing demand for customized medical solutions by patients due to increasing awareness about 3D printing is driving growth of the 3D printing in healthcare market.

- Cost Effectiveness: As the medical devices are made according to the need of patient, there is decrease in manufacturing costs and wastage by producing only what is needed. As this is a cost effective method for manufacturing of device, it is an attractive option for healthcare providers thus increasing demand for 3D printing.

- Rapid Prototyping: As the products are developed time to time it accelerates the development of medical devices and surgical tools, which enables faster innovation and time-to-market. Using medical models built with Rapid Prototyping (RP) technologies represents a new approach for surgical planning and simulation. These techniques allow one to reproduce anatomical objects as 3D physical models, which give the surgeon a realistic impression of complex structures before a surgical intervention.

3D Printing in Healthcare Market Future Trends

- Advancements in Materials: Continuous improvements in 3D printing materials and techniques enhances the quality and safety of printed products. For instance, metal 3D printing is used for development of medical devices designers to produce implants that perform better, match better and last longer, for knees, spine, skull or hips.

- Expanding Applications: Growing use of 3D printing in various fields such as orthopedics, dentistry, and surgical planning presents new market trends. In addition, 3D printing can be used by specialists to create reference models using MRI scans and CT in order to help surgeons prepare better for surgeries.

- Collaboration with Research Institutions: Collaboration of companies with research institutes can lead to innovative applications and advancements in 3D printing technologies. Companies can develop printers according to the need of the particular research institutes which develops products according to their requirement.

3D Printing in Healthcare Market Opportunities

- Telemedicine Integration: The incorporation of 3D printing in the telemedicine cycle could result in pharmacists designing and manufacturing personalized medicines based on the electronic prescription received. Hence, the rise of telehealth creates opportunities for remote patient-specific solutions using 3D printing.

- Education and Training: For use of 3D printing tools, the healthcare professional must be trained properly for development of required medical devices and pharmaceuticals. Developing training programs for healthcare professionals on 3D printing technology can enhance adoption and usage. In addition, government are focusing on training healthcare professionals for 3D printing technology.

- Sustainability Initiatives: Increasing focus on eco-friendly practices provides opportunities for developing sustainable materials and processes in 3D printing. 3D printing reduces carbon footprints in a few different ways such as less energy and material waste and no carbon-heavy supply chains.

3D Printing in Healthcare Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 6.52 Billion |

| Market Size by 2031 | US$ 21.14 Billion |

| Global CAGR (2025 - 2031) | 18.3% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Component

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

3D Printing in Healthcare Market Players Density: Understanding Its Impact on Business Dynamics

The 3D Printing in Healthcare Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Key Selling Points

- Comprehensive Coverage: The report comprehensively covers the analysis of products, services, types, and end users of the 3D Printing in Healthcare Market, providing a holistic landscape.

- Expert Analysis: The report is compiled based on the in-depth understanding of industry experts and analysts.

- Up-to-date Information: The report assures business relevance due to its coverage of recent information and data trends.

- Customization Options: This report can be customized to cater to specific client requirements and suit the business strategies aptly.

The research report on the 3D Printing in Healthcare Market can, therefore, help spearhead the trail of decoding and understanding the industry scenario and growth prospects. Although there can be a few valid concerns, the overall benefits of this report tend to outweigh the disadvantages.

Frequently Asked Questions

1. Customization of devices.

2. Rapid Prototyping

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Unlock Exclusive Report Discounts

Enquire Now

Get Free Sample For

Get Free Sample For