Aircraft Isothermal Forging Market Drivers and Forecasts by 2031

Historic Data: 2021-2022 | Base Year: 2023 | Forecast Period: 2024-2031Aircraft Isothermal Forging Market Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Aircraft Components (Fan Blades, Turbine Disks, Shafts, and Connector Rings), Forging Material (Titanium and Nickel-based Superalloys), Fit Type (Line Fit and Retrofit), and Geography

- Report Date : Sep 2025

- Report Code : TIPRE00015983

- Category : Aerospace and Defense

- Status : Data Released

- Available Report Formats :

- No. of Pages : 150

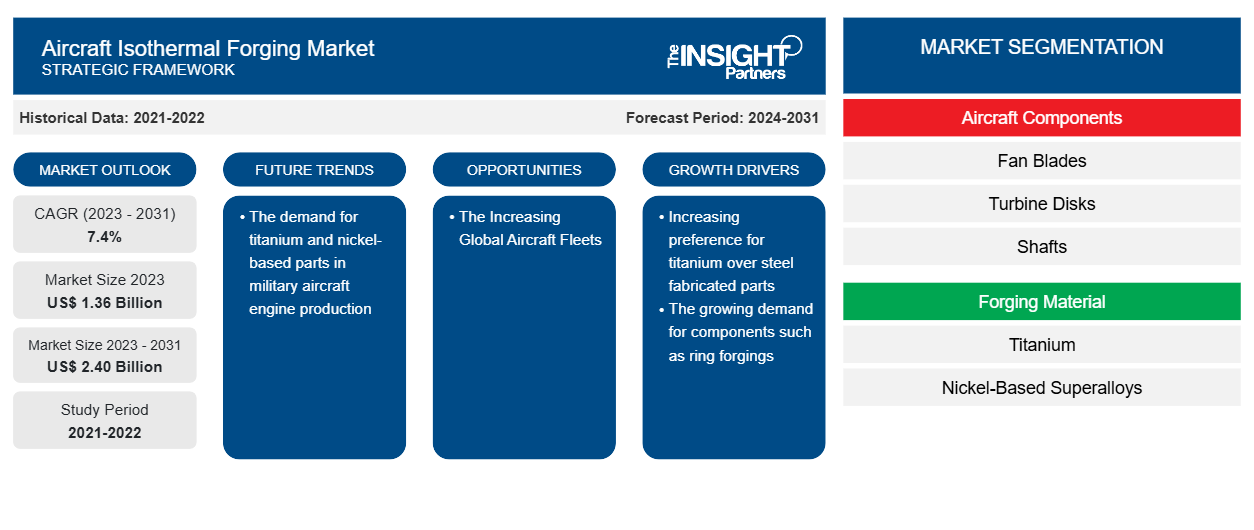

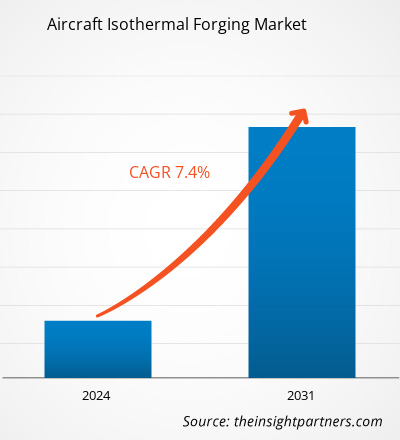

The aircraft isothermal forging market size is projected to reach US$ 2.40 billion by 2031 from US$ 1.36 billion in 2023. The market is expected to register a CAGR of 7.4% during 2023–2031. The healthy demand for Titanium and Nickel-based alloys in aircraft manufacturing is likely to remain a key trend in the market.

Aircraft Isothermal Forging Market Analysis

The market players that manufacture aircraft components through the isothermal forging process include ATI, H.C. Starck Solutions, Bharat Forge, Alcoa Corporation Schuler AG, SMT Limited, and ALD VACUUM TECHNOLOGIES. The growing initiatives for strengthening the production capacities is also aiding the market growth. For instance, in March 2022, Ramkrishna Forgings expanded its forging capacities and machining and heat treatment capabilities, including isothermal annealing, which allows the company to manufacture components for OEMs and Tier 1 companies.

Aircraft Isothermal Forging Market Overview

The major end users of the isothermal forging market include aerospace manufacturers, military & commercial aircraft MROs, and aircraft component manufacturers. These companies procure the aircraft components and parts made from the isothermal forging process for specific aircraft applications. These companies incorporate long-term contracts and supply agreements with the isothermal forging companies. Moreover, the MROs also caters to the demand for aircraft parts replacement or refurbishment that also includes engine parts such as turbine blades, disks, fasteners, etc that requires deployment of isothermally forged parts which is another major end user driving the aircraft isothermal forging market. Moreover, the rising commercial aircraft operations worldwide is also boosting the demand for isothermal forging products from MRO services.

Customize This Report To Suit Your Requirement

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

Aircraft Isothermal Forging Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

Aircraft Isothermal Forging Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Aircraft Isothermal Forging Market Drivers and Opportunities

Increasing Demand for Components Made of Titanium Alloys And Ring Forgings

The major stakeholders in the global isothermal forging market ecosystem include raw material suppliers, isothermal forging companies, and end users. The raw material supplier is the crucial stakeholder in the ecosystem of the isothermal forging market. The major raw materials are titanium, titanium alloy, and nickel-based superalloy material, primarily used to manufacture the aircraft components through isothermal forging technology. The major raw material suppliers include Metalmen Sales Inc., Ferralloy Inc., Universal Metals, Advanced Global Materials Inc., Continental Steel & Tube Co., VSMPO-AVISMA, and Siddhagiri Metals & Tubes. In November 2021, Boeing signed an agreement with VSMPO-AVISMA, a leading Russian titanium producer, to develop new titanium alloys and technologies. In addition, in February 2021, Hindustan Aeronautics Ltd. signed a contract worth US$ 15 million with GE Aviation for the development and supply of ring forgings for its aviation military and commercial engine programs. Thus, such growing initiatives from supplying raw materials are strengthening aircraft production through isothermal forging technology, which is propelling the market growth.

The Increasing Global Aircraft Fleets

According to the Market analysis, in 2022, the global commercial aircraft fleet was estimated to be around 25,578 which is further likely to reach more than 28,400 aircraft by the end of 2024. Further, the commercial aircraft fleet is expected to reach around 36,400 aircraft by the end of 2034. Moreover, according to the Boeing and Airbus’ forecasts, more than 40,800 commercial aircraft are expected to be delivered globally by the end of 2042 which is further expected to generate the demand for forging products in the coming years. Such factors are anticipated to generate new opportunities for isothermal forging market vendors in the coming years.

Aircraft Isothermal Forging Market Report Segmentation Analysis

Key segments that contributed to the derivation of the aircraft isothermal forging market analysis are aircraft component, forging material, and fit type.

- Based on aircraft component, the aircraft isothermal forging market is segmented into fan blades, turbine disks, shafts, and connector rings. The fan blade segment held a larger market share in 2023.

- Based on forging material, the aircraft isothermal forging market is segmented into titanium and nickel-based superalloys. The nickel-based superalloys segment held a larger market share in 2023.

- Based on fit type, the aircraft isothermal forging market is bifurcated into line fit and retrofit. The line fit segment held a larger market share in 2023.

Aircraft Isothermal Forging Market Share Analysis by Geography

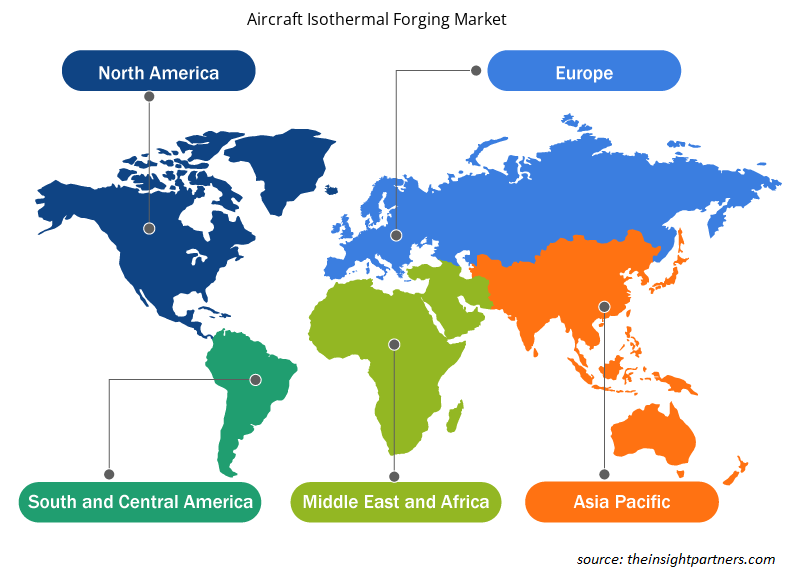

The geographic scope of the aircraft isothermal forging market report is mainly divided into five regions: North America, Europe, Asia Pacific, Middle East & Africa, and South America.

Asia Pacific has dominated the market in 2023 followed by North America and Europe regions. Further, Asia Pacific is also likely to witness highest CAGR in the coming years. One of the major reasons behind the higher market share of the region is mainly due to the increasing aircraft deliveries and the rising regional aircraft fleet. Further, the exepected deliveries of more than 18,800 new commercial aircraft across the region in the next two decades is likely to generate new market opportunities across the Asia Pacific region.

Aircraft Isothermal Forging Market Regional Insights

The regional trends and factors influencing the Aircraft Isothermal Forging Market throughout the forecast period have been thoroughly explained by the analysts at The Insight Partners. This section also discusses Aircraft Isothermal Forging Market segments and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America.

- Get the Regional Specific Data for Aircraft Isothermal Forging Market

Aircraft Isothermal Forging Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2023 | US$ 1.36 Billion |

| Market Size by 2031 | US$ 2.40 Billion |

| Global CAGR (2023 - 2031) | 7.4% |

| Historical Data | 2021-2022 |

| Forecast period | 2024-2031 |

| Segments Covered |

By Aircraft Components

|

| Regions and Countries Covered | North America

|

| Market leaders and key company profiles |

Aircraft Isothermal Forging Market Players Density: Understanding Its Impact on Business Dynamics

The Aircraft Isothermal Forging Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Market players density refers to the distribution of firms or companies operating within a particular market or industry. It indicates how many competitors (market players) are present in a given market space relative to its size or total market value.

Major Companies operating in the Aircraft Isothermal Forging Market are:

- Alcoa Corporation

- ALD Vacuum Technologies

- Allegheny Technologies Incorporated

- H.C. Starck GmbH

- Howmet Aerospace

Disclaimer: The companies listed above are not ranked in any particular order.

- Get the Aircraft Isothermal Forging Market top key players overview

Aircraft Isothermal Forging Market News and Recent Developments

The aircraft isothermal forging market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the developments in the aircraft isothermal forging market are listed below:

- India’s leading aviation company Hindustan Aeronautics Limited (HAL) and Safran Aircraft Engines, the French global leader in aero engine design, development and manufacturing, signed today a MoU (Memorandum of Understanding) announcing their intent to develop industrial cooperation in forging parts’ manufacturing for commercial engines. (Source: Safran, Press Release, Oct 2023)

Alcoa secured a 10 year agreement with Pratt & Whitney worth US$ 1.1 billion for the supply of critical components of PurePower geared turbofan jet engines that also oncludes titanium forged parts. (Source: Alcoa, Press Release, July 2014)

Aircraft Isothermal Forging Market Report Coverage and Deliverables

The “Aircraft Isothermal Forging Market Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering below areas:

- Aircraft isothermal forging market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Aircraft isothermal forging market trends as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed porter’s five forces analysis

- Aircraft isothermal forging market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the aircraft isothermal forging market

- Detailed company profiles

Frequently Asked Questions

Which region dominated the aircraft isothermal forging market in 2023?

Asia Pacific region dominated the aircraft isothermal forging market in 2023.

What are the driving factors impacting the aircraft isothermal forging market?

Increasing preference for titanium over steel fabricated parts and the growing demand for components such as ring forgings are some of the factors driving the growth for aircraft isothermal forging market.

What are the future trends of the aircraft isothermal forging market?

The demand for titanium and nickel-based parts in military aircraft engine production is one of the major trends of the market.

Which are the leading players operating in the aircraft isothermal forging market?

Alcoa Corporation, ALD Vacuum Technologies, Allegheny Technologies Incorporated, H C Starck GmbH, Howmet Aerospace LTD, Leistritz Turbinentechnik GmbH, Nanshan Forge Company, Precision Castparts Corp (Berkshire Hathaway), Schuler AG, and SMT Limited are some of the key players profiled under the report.

What would be the estimated value of the aircraft isothermal forging market by 2031?

The estimated value of the aircraft isothermal forging market by 2031 would be around US$ 2.40 billion.

What is the expected CAGR of the aircraft isothermal forging market?

The aircraft isothermal forging market is likely to register of 7.4% during 2023-2031.

Market Research & Consulting

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

- Aircraft MRO Market

- Helicopter Hoists Winches and Hooks Market

- Fixed-Base Operator Market

- Aerospace Fasteners Market

- Aerospace Stainless Steel And Superalloy Fasteners Market

- Aircraft Floor Panel Market

- Military Optronics Surveillance and Sighting Systems Market

- Smoke Grenade Market

- Airport Runway FOD Detection Systems Market

- Artillery Systems Market

Testimonials

I wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.The Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.We worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, Market ResearchThe research report delivered details on drivers and restraints, trends, and opportunities, along with strategic activities in the market. Previously, we were struggling to get reliable information.

Manager Medical Devices ManufacturingReason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Yes! We provide a free sample of the report, which includes Report Scope (Table of Contents), report structure, and selected insights to help you assess the value of the full report. Please click on the "Download Sample" button or contact us to receive your copy.

Absolutely — analyst assistance is part of the package. You can connect with our analyst post-purchase to clarify report insights, methodology or discuss how the findings apply to your business needs.

Once your order is successfully placed, you will receive a confirmation email along with your invoice.

• For published reports: You’ll receive access to the report within 4–6 working hours via a secured email sent to your email.

• For upcoming reports: Your order will be recorded as a pre-booking. Our team will share the estimated release date and keep you informed of any updates. As soon as the report is published, it will be delivered to your registered email.

We offer customization options to align the report with your specific objectives. Whether you need deeper insights into a particular region, industry segment, competitor analysis, or data cut, our research team can tailor the report accordingly. Please share your requirements with us, and we’ll be happy to provide a customized proposal or scope.

The report is available in either PDF format or as an Excel dataset, depending on the license you choose.

The PDF version provides the full analysis and visuals in a ready-to-read format. The Excel dataset includes all underlying data tables for easy manipulation and further analysis.

Please review the license options at checkout or contact us to confirm which formats are included with your purchase.

Our payment process is fully secure and PCI-DSS compliant.

We use trusted and encrypted payment gateways to ensure that all transactions are protected with industry-standard SSL encryption. Your payment details are never stored on our servers and are handled securely by certified third-party processors.

You can make your purchase with confidence, knowing your personal and financial information is safe with us.

Yes, we do offer special pricing for bulk purchases.

If you're interested in purchasing multiple reports, we’re happy to provide a customized bundle offer or volume-based discount tailored to your needs. Please contact our sales team with the list of reports you’re considering, and we’ll share a personalized quote.

Yes, absolutely.

Our team is available to help you make an informed decision. Whether you have questions about the report’s scope, methodology, customization options, or which license suits you best, we’re here to assist. Please reach out to us at sales@theinsightpartners.com, and one of our representatives will get in touch promptly.

Yes, a billing invoice will be automatically generated and sent to your registered email upon successful completion of your purchase.

If you need the invoice in a specific format or require additional details (such as company name, GST, or VAT information), feel free to contact us, and we’ll be happy to assist.

Yes, certainly.

If you encounter any difficulties accessing or receiving your report, our support team is ready to assist you. Simply reach out to us via email or live chat with your order information, and we’ll ensure the issue is resolved quickly so you can access your report without interruption.

Get Free Sample For

Get Free Sample For