Artificial Cervical Intervertebral Disc Market Growth & Forecast 2034

Coverage: By Material (Biopolymer Material, Metal Material ); End User (Hospitals, Ambulatory Surgical Centers (ASCs)); and Geography

- Status : Data Released

- Report Code : TIPRE00023194

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : January 23, 2026

2025 Market Size

US$ 2.67 Bn

Base year value

2034 Forecast

US$ 12.02 Bn

Projected by 2034

CAGR 2026-2034

18.18 %

Growth rate

Addressable Market

US$ 60.69 Bn

(2026-2034)

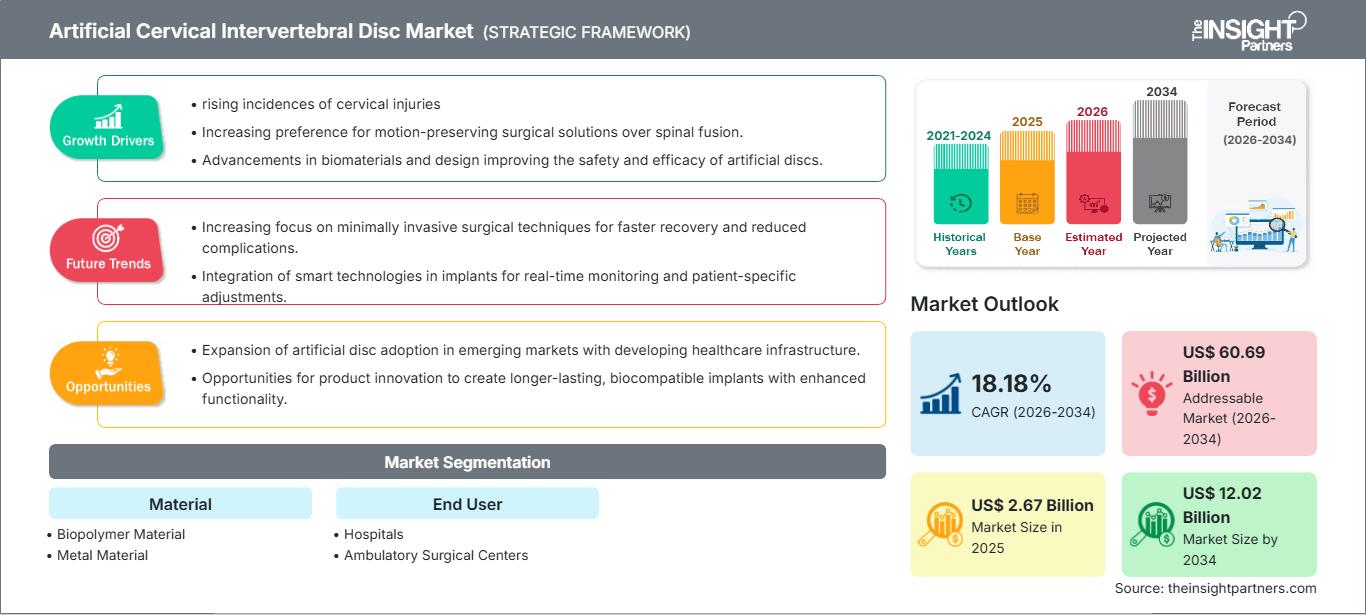

The Artificial Cervical Intervertebral Disc Market size is expected to reach a significant US$ 12.02 billion by 2034, soaring from an estimated US$ 2.67 billion in 2025. The market is anticipated to register a robust Compound Annual Growth Rate (CAGR) of 18.18% during the forecast period of 2026–2034.

Artificial Cervical Intervertebral Disc Market Analysis

The global artificial cervical intervertebral disc market forecast indicates accelerated growth, fundamentally driven by the shift away from traditional spinal fusion towards motion-preserving surgical interventions. This hyper-growth is primarily attributed to the increasing global prevalence of cervical degenerative disc disease (CDDD), often linked to aging populations and modern sedentary lifestyles. Market expansion is propelled by widespread clinical acceptance of cervical total disc replacement (TDR) as a superior alternative to anterior cervical discectomy and fusion (ACDF), as TDR aims to minimize adjacent segment disease (ASD). Continuous technological innovations, including the development of next-generation implant materials that offer enhanced biocompatibility and long-term durability, alongside advancements in minimally invasive surgical techniques, are improving patient outcomes, shortening hospital stays, and accelerating global market penetration among both hospitals and ambulatory surgical centers (ASCs).

Artificial Cervical Intervertebral Disc Market Overview

Artificial cervical intervertebral discs are sophisticated medical implants that can replace a damaged or diseased natural disc in the cervical spine (neck). Different from fusion procedures, these implants are designed to preserve the spine segment's natural range of motion and decrease the stress on the adjacent vertebrae. The general makeup consists of metal endplates-usually titanium or cobalt-chrome alloy-riding on a central core, usually made of biopolymer (polyethylene) or metal. This market is characterized by intense R&D related to biomaterials, kinematics, and longevity. Significant drivers include increasing regulatory approvals for multi-level replacement procedures and a rising preference among orthopedic surgeons and neurosurgeons for motion preservation techniques.

Market Research Highlights

- Global market for Artificial Cervical Intervertebral Disc was valued at US$ 2.67 Billion in 2025

- Annual market size is expected to reach US$ 12.02 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 60.69 Billion

- Market is anticipated to register a CAGR of 18.18% during the forecast period

- The United States represents a key market, supported by rising incidences of cervical injuries, Increasing preference for motion-preserving surgical solutions over spinal fusion., Advancements in biomaterials and design improving the safety and efficacy of artificial discs., as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Expansion of artificial disc adoption in emerging markets with developing healthcare infrastructure., Opportunities for product innovation to create longer-lasting, biocompatible implants with enhanced functionality. are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Zimmer Biomet Holdings, Inc., Globus Medical, Inc., Centinel Spine, LLC, Synergy Spine Solutions, Inc., Aditus Medical, AxioMed LLC, NuVasive, Inc., Orthofix Medical, Inc., Medtronic, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Artificial Cervical Intervertebral Disc Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Artificial Cervical Intervertebral Disc Market Drivers and Opportunities

Market Drivers:

- Rising Prevalence of Cervical Spine Disorders Globally: The increasing incidence of cervical degenerative disc disease (CDDD) due to demographic changes (aging) and lifestyle factors is creating a vast patient pool requiring surgical intervention.

- Increasing Preference for Motion-Preserving Surgical Solutions: Surgeons and patients are increasingly favoring cervical total disc replacement (TDR) over spinal fusion (ACDF) to potentially reduce the risk of adjacent segment disease (ASD) and preserve spinal functionality.

- Technological Advancements in Implant Design and Materials: Innovations in implant manufacturing, including enhanced bearing surfaces, improved articulation mechanisms, and superior biocompatible materials, are boosting long-term clinical success rates.

Market Opportunities:

- Expansion in Emerging Markets with Improving Healthcare Infrastructure: Countries in the Asia-Pacific and Latin America are rapidly modernizing their spine care centers and increasing healthcare IT investments. This creates significant untapped opportunities for disc replacement device manufacturers.

- Development of Next-Generation Biocompatible Materials for Enhanced Outcomes: Opportunities exist in developing novel bearing surfaces, such as ceramics or advanced polyethylene, to further minimize wear debris and enhance the implant's lifespan and integration with bone tissue.

- Strategic Collaborations for Innovation and Global Distribution: Partnerships between major device manufacturers and regional distributors, particularly in high-growth areas like China and India, are crucial for navigating complex local regulatory approvals and expanding market access.

Artificial Cervical Intervertebral Disc Market Report Segmentation Analysis

The market share for artificial cervical discs is segmented based on the composition of the implant and the primary setting where the surgical procedure takes place, providing a clearer understanding of adoption patterns. Below is the standard segmentation approach used in most industry reports:

By Material:

- Biopolymer Material

- Metal Material

By End User:

- Hospitals

- Ambulatory Surgical Centers (ASCs)

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Artificial Cervical Intervertebral Disc Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 2.67 Billion |

| Market Size by 2034 | US$ 12.02 Billion |

| Global CAGR (2026 - 2034) | 18.18% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Material

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Artificial Cervical Intervertebral Disc Market Players Density: Understanding Its Impact on Business Dynamics

The Artificial Cervical Intervertebral Disc Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Artificial Cervical Intervertebral Disc Market Share Analysis by Geography

Market growth is unevenly distributed globally, reflecting differences in surgical acceptance, regulatory environments, and patient payment models.

North America

- Market Share: Dominates the global market, driven by high disposable income, established reimbursement policies, and a strong presence of leading spinal device manufacturers.

- Key Drivers: Favorable regulatory pathways (FDA approval) leading to fast product adoption; high patient awareness and acceptance of motion-preserving spine surgery.

- Trends: Increasing migration of single-level TDR procedures from hospitals to cost-efficient ASCs; strong investment in clinical trials for multi-level disc replacement.

Europe

- Market Share: Holds a significant market share, supported by universal healthcare coverage and early clinical adoption of disc replacement technologies, particularly in Germany and the UK.

- Key Drivers: Supportive healthcare policies for innovative spinal technologies; established patient registries providing long-term clinical data on implant performance.

- Trends: Stringent oversight from the European Medicines Agency (EMA) and local bodies ensures high safety standards; strong push for cost-effectiveness analysis in public health systems.

Asia Pacific

- Market Share: The fastest-growing region, owing to the rising prevalence of spinal disorders, the rapidly expanding medical tourism sector, and large investments in private healthcare.

- Key Drivers: Government-supported health infrastructure expansion; rising patient volumes driven by urbanization and improved diagnostic capabilities in countries like China and India.

- Trends: Local manufacturing and licensing agreements are gaining traction to develop lower-cost, locally tailored disc implants, increasing patient demand for sophisticated surgical options.

South and Central America

- Market Share: Emerging market with low penetration but high long-term growth potential.

- Key Drivers: Expansion of private specialist clinics; growing public-private health partnerships to fund high-cost procedures.

- Trends: Adoption is slow but accelerating, primarily focused on imported, clinically proven devices; education and training for local spine surgeons are critical growth factors.

Middle East and Africa

- Market Share: Developing market, highly concentrated in wealthy Gulf Cooperation Council (GCC) nations.

- Key Drivers: Large government-funded healthcare infrastructure projects; focus on becoming regional hubs for complex specialty surgeries, including spine procedures.

- Trends: Demand for state-of-the-art implant technology; growth highly dependent on government healthcare budgets and foreign medical expertise.

Artificial Cervical Intervertebral Disc Market Players Density: Understanding Its Impact on Business Dynamics

High Market Density and Competition

The market is intensely competitive, dominated by a few large, multinational orthopedic and spine device companies. Differentiation is less about the core concept and more about subtle mechanical design, materials science, and long-term clinical data.

Differentiation is achieved through:

- Minimizing Adjacent Segment Disease (ASD): Companies compete on implant design features that best replicate natural spinal kinematics and minimize stress transfer to the segments above and below the implant.

- Long-Term Biocompatibility and Wear: Differentiation through advanced materials (e.g., highly cross-linked polyethylene) and surface coatings to reduce wear debris and improve osseointegration.

- Simplified Surgical Technique: Developing delivery systems and instrumentation that allow surgeons to perform the procedure more quickly, accurately, and with minimal invasiveness, especially in the growing ASC setting.

Major Companies operating in the Artificial Cervical Intervertebral Disc Market are:

- Zimmer Biomet Holdings, Inc.

- Globus Medical, Inc.

- Centinel Spine, LLC

- Synergy Spine Solutions, Inc.

- Aditus Medical

- AxioMed LLC

- NuVasive, Inc.

- Orthofix Medical, Inc.

- Medtronic

Disclaimer: The companies listed above are not ranked in any particular order.

Artificial Cervical Intervertebral Disc Market News and Recent Developments

- Zimmer Biomet advances Mobi-C™ cervical disc portfolio: Zimmer Biomet announced the FDA approval of a new 4.5 mm height Mobi-C™ Cervical Disc designed to match U.S. anatomical profiles better, improving prosthesis fit and reducing complication risks such as facet joint over-distraction. The company also initiated an FDA-cleared IDE hybrid study in September 2023 and has surpassed 200,000 global Mobi-C™ implants, with U.S. patient enrollment now underway.

- Globus Medical continues regulatory momentum for SECURE-C™ Cervical Artificial Disc: Globus Medical highlighted long-term IDE clinical results showing the SECURE-C™ Cervical Disc achieving statistical superiority over ACDF at 84 months in patient satisfaction outcomes. The device, which received FDA PMA approval in 2012, continues to maintain compliance through ongoing supplemental regulatory filings supporting sustained market presence.

Artificial Cervical Intervertebral Disc Market Report Coverage and Deliverables

The “Artificial Cervical Intervertebral Disc Market Size and Forecast (2021–2034)” report provides a detailed analysis of the market covering the following areas:

- Artificial Cervical Intervertebral Disc Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Artificial Cervical Intervertebral Disc Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Artificial Cervical Intervertebral Disc Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Artificial Cervical Intervertebral Disc Market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends