Aviation Headsets Market Size and Competitive Analysis by 2031

Aviation Headsets Market Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (On-Board Headsets and Ground Support Headsets), Noise Cancellation Type (Active and Passive), Application (Commercial Aircraft, Military Aircraft, and General Aviation) and Geography

Historic Data: 2021-2022 | Base Year: 2023 | Forecast Period: 2024-2031- Status : Data Released

- Report Code : TIPRE00025973

- Category : Aerospace and Defense

- No. of Pages : 150

- Available Report Formats :

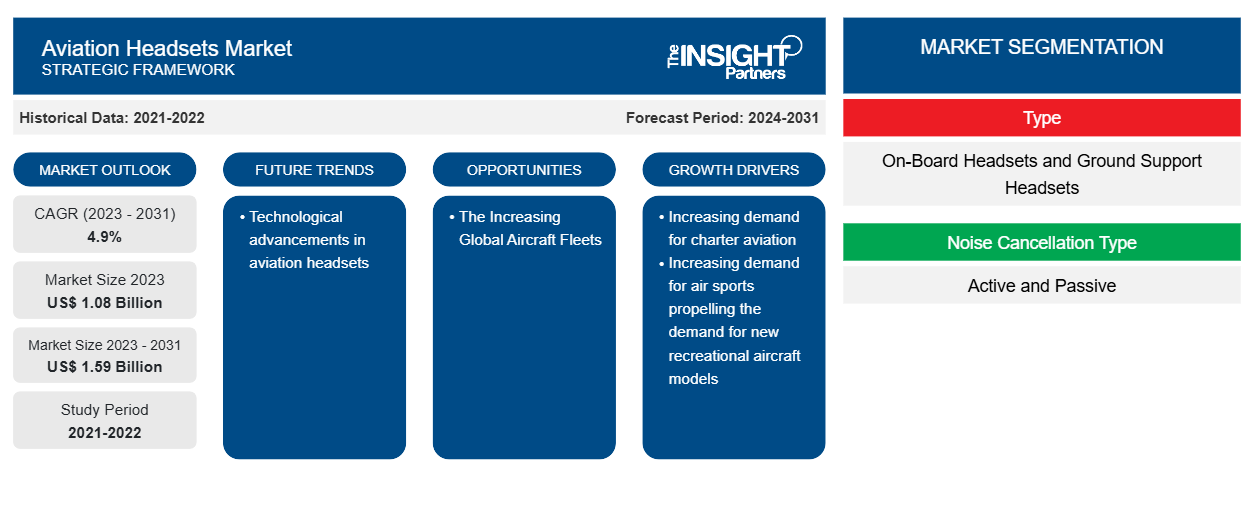

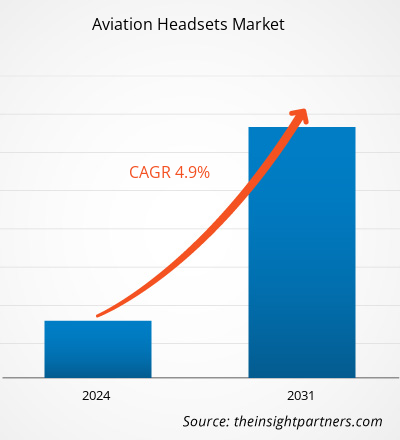

The aviation headsets market size is projected to reach US$ 1.59 billion by 2031 from US$ 1.08 billion in 2023. The market is expected to register a CAGR of 4.9% during 2023–2031. Technological advancements in aviation headsets is likely to remain a key trend in the market.

Aviation Headsets Market Analysis

The aviation headsets market ecosystem is diverse and evolving. Its stakeholders are component providers, headset manufacturers, and distributors & end-users. Major players occupy places in the various nodes of the market ecosystem. The component provider’s supply different components such as semiconductor products/chipsets, microphones, speaker components to aviation headset manufacturers who then utilize it to manufacture and design the final aviation headset products. The final product is then distributed to the end users through different mediums such as direct sales through company distributors across the aviation sector.

Aviation Headsets Market Overview

Companies such as Bosch Security & Safety Systems, Bose Corporation, David Clark Company, Lightspeed Aviation, GBH Headsets, Pilot Communications, Plantronics Inc., SEHT Limited, and Sennheiser Electronic GmbH & Co. Kg, are amongst the leading manufacturers in the aviation headsets market. These companies are engaged in design, manufacturing, and selling of wide range of aircraft headsets to end-users such as airlines, MRO companies, aviation OEMs, and defense forces respectively.

Market Assessment and Insights

- Global market for Aviation Headsets was valued at US$ 1.08 Billion in 2023

- Annual market size is expected to reach US$ 1.59 Billion by 2031

- Total addressable market (TAM) during 2024-2031 is projected to reach approximately US$ 10.78 Billion

- Market is anticipated to register a CAGR of 4.9% during the forecast period

- The United States represents a key market, supported by Increasing demand for charter aviation, Increasing demand for air sports propelling the demand for new recreational aircraft models, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as The Increasing Global Aircraft Fleets are expected to influence market dynamics and addressable market

- Report profiles industry participants, including Bosch Security and Safety Systems, Bose Corporation, David Clark Company, Faro Aviation, GBH Headsets, Lightspeed Aviation, Pilot Communications USA, Plantronics, Inc., SEHT LIMITED, Sennheiser electronic GmbH & Co. KG, while analyzing competitive strategies and innovation developments

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONAviation Headsets Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Aviation Headsets Market Drivers and Opportunities

Increasing Demand for Air Sports Propelling the Demand for New Recreational Aircraft Models

The rising number of light-sport aircraft deliveries owing to an increase in awareness for air sports among youngsters across is aiding the deployment of new generation recreational aircraft models. For instance, the rising fleet of existing LSA (light-sport aircraft) is generating the demand for new pilots and headset accessories worldwide. Moreover, the demand for LSA is mainly driven by the rising interest in recreational activities such as sky diving is paving way for new players to establish business while the existing players expanding their business by setting up a new base and buying new aircraft. Therefore, the growing fleet of light-sport aircraft worldwide is aiding the adoption of aviation headsets globally.

The Increasing Global Aircraft Fleets

As per The Insight Partners’ secondary research the global commercial aircraft fleet in 2022 was around 25,578 aircraft that is further likely to reach around 28,398 aircraft by the end of 2024 and around 36,413 aircraft by the end of 2034. Moreover, according to the forecasts disclosed by two of the major aircraft OEMs i.e., Boeing and Airbus, more than 40,800 aircraft are expected to be delivered by the end of 2042 which will further generate the demand for new pilots and headsets in the coming years.

Aviation Headsets Market Report Segmentation Analysis

Key segments that contributed to the derivation of the aviation headsets market analysis are type noise cancellation type, and application.

- Based on type, the aviation headsets market is segmented into on-board headsets and ground support headsets. The on-board headsets segment held a larger market share in 2023.

- Based on noise cancellation type, the aviation headsets market is segmented into active and passive. The active segment held a larger market share in 2023.

- Based on application, the aviation headsets market is segmented into commercial aircraft, military aircraft, and general aviation. The commercial segment held a larger market share in 2023.

Aviation Headsets Market Share Analysis by Geography

The geographic scope of the aviation headsets market report is mainly divided into five regions: North America, Europe, Asia Pacific, Middle East & Africa, and South America.

North America has dominated the market in 2023 followed by Europe and Asia Pacific regions. Further, Asia Pacific is also likely to witness highest CAGR in the coming years. This is mainly due to the expected deliveries of more than 18,800 new commercial aircraft across the region in the next two decades. Further, the rising number of airports across the Asia Pacific region is also pushing the deployment of more number of airplanes in the region which is further likely to generate new opportunities for market vendors in the coming years.

Aviation Headsets Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2023 | US$ 1.08 Billion |

| Market Size by 2031 | US$ 1.59 Billion |

| Global CAGR (2023 - 2031) | 4.9% |

| Historical Data | 2021-2022 |

| Forecast period | 2024-2031 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Aviation Headsets Market Players Density: Understanding Its Impact on Business Dynamics

The Aviation Headsets Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Aviation Headsets Market News and Recent Developments

The aviation headsets market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the developments in the aviation headsets market are listed below:

- Bose, the leader in premium aviation headset technology, today announced its latest innovation: the new A30 Aviation Headset. Unveiled at the SUN ‘n FUN Aerospace Expo in Lakeland, Fla., the A30 is an entirely new product, designed to bring pilots the best combination of comfort, noise cancellation and audio clarity of any aviation headset on the market. (Source: Bose, Press Release, Mar 2023)

Lightspeed Aviation today introduced the Lightspeed Delta Zulu – the first in the next generation of ANR headsets. This revolutionary ANR aviation headset introduces a suite of new features and heralds a new category of aviation product dubbed “Safety Wearables”. (Source: Lightspeed Aviation, Press Release, Sep 2022)

Aviation Headsets Market Report Coverage and Deliverables

The “Aviation Headsets Market Size and Forecast (2021–2031)” report provides a detailed analysis of the market covering below areas:

- Aviation headsets market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Aviation headsets market trends as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed porter’s five forces analysis

- Aviation headsets market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the aviation headsets market

- Detailed company profiles

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Unlock Exclusive Report Discounts

Enquire Now

Get Free Sample For

Get Free Sample For