Diabetic Retinopathy Market Trends, Size & Growth by 2034

Coverage: by Type (Proliferative Diabetic Retinopathy and Non-Proliferative Diabetic Retinopathy), Treatment (Anti-VEGF Drug, Steroid Injection, Laser Surgeries, and Vitrectomy), and Distribution Channel (Retail Pharmacies, Hospital Pharmacies, and Others), and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00004185

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 08, 2026

2025 Market Size

US$ 10.74 Bn

Base year value

2034 Forecast

US$ 18.08 Bn

Projected by 2034

CAGR 2026-2034

5.95 %

Growth rate

Addressable Market

US$ 130.49 Bn

(2026-2034)

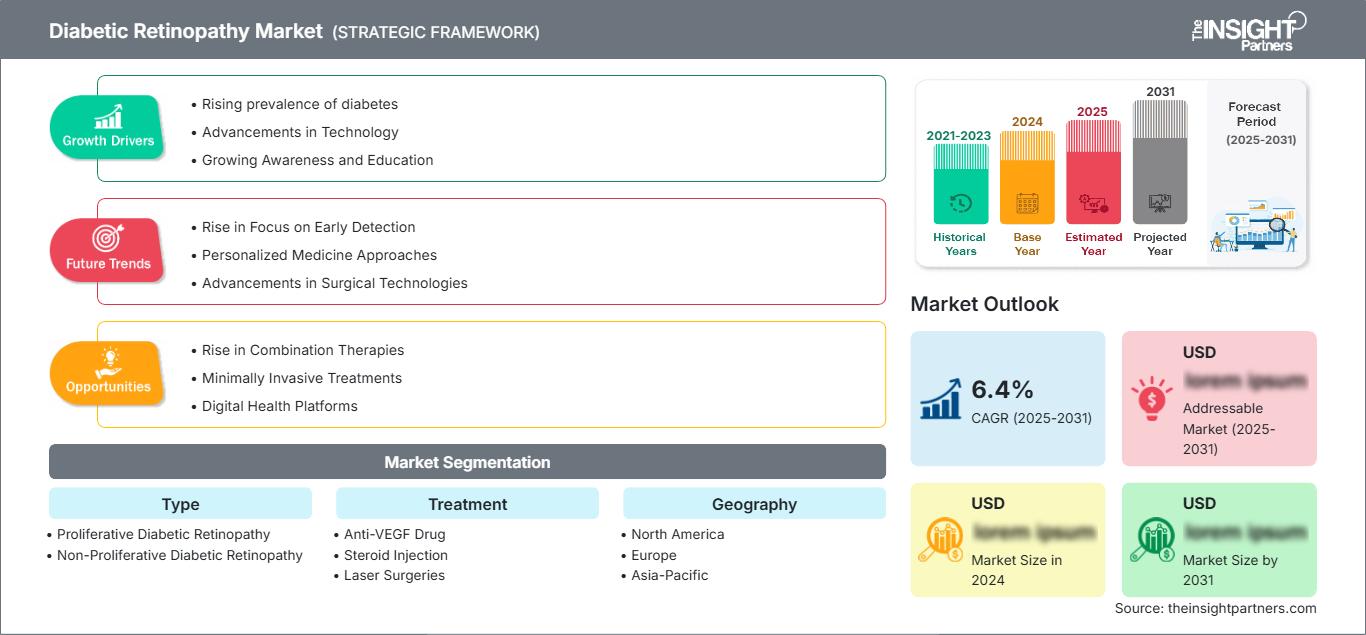

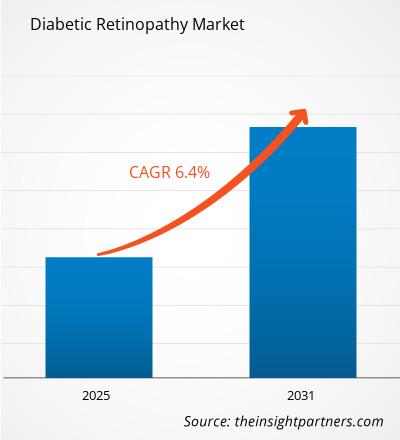

The Diabetic Retinopathy Market is witnessing steady expansion as healthcare systems intensify efforts to address diabetes-related vision impairment and blindness. The market is valued at US$10.74 billion in 2025 and is projected to reach US$18.08 billion by 2034, advancing at a CAGR of 5.95% during 2026–2034. Rising diabetes prevalence, improved retinal screening programs, and increasing adoption of targeted biologics are reshaping treatment pathways across developed and emerging healthcare markets.

North America remains a major revenue contributor to the Diabetic Retinopathy Market and is anticipated to register a CAGR of approximately 5.6% through the forecast period. Growth is supported by high diabetes incidence, widespread access to ophthalmology services, and rapid adoption of anti-VEGF therapies. Expanded reimbursement coverage, integration of AI-assisted retinal diagnostics, and growing awareness regarding early intervention continue to strengthen regional demand.

Diabetic Retinopathy Market Assessment and Insights

- North America: North America accounted for 39–43% of the diabetic retinopathy market share in 2025 and is projected to expand at a CAGR of 5.4%–6.1% during 2026–2034. Growth is driven by advanced ophthalmic care infrastructure, increasing diabetic retinopathy screening, and broad access to innovative retinal therapies.

- U.S.: The U.S. represented 31–35% of the global diabetic retinopathy market in 2025 and is anticipated to register a CAGR of 5.5%–6.2% during 2026–2034, supported by a high prevalence of diabetes, widespread adoption of anti-VEGF therapies, and favorable reimbursement for retinal disease treatment.

- Europe: Europe held 27–31% market share in 2025 and is expected to grow at a CAGR of 5.1%–5.8% during 2026–2034. Germany, the United Kingdom, and France remain the leading regional markets, supported by well-established ophthalmology services and expanding diabetic eye disease management programs.

- Asia Pacific: Asia Pacific accounted for 21–25% of the diabetic retinopathy market size in 2025 and is forecast to expand at a CAGR of 6.7%–7.5% during 2026–2034. China, Japan, and India drive regional growth through increasing diabetes prevalence, improving access to ophthalmic care, and expanding healthcare investments.

- Largest Segment – Anti-VEGF Drug: The anti-VEGF drug segment represented the largest diabetic retinopathy market share and is expected to grow at a CAGR of 6.0%–6.8% during 2026–2034, driven by proven clinical efficacy, strong physician preference, and widespread adoption in diabetic retinopathy treatment.

- High Growth Segment – Proliferative Diabetic Retinopathy: The proliferative diabetic retinopathy segment is projected to register the fastest growth with a CAGR of 6.8%–7.6% during 2026–2034, supported by increasing diagnosis of advanced-stage disease and rising demand for effective treatment options.

- Key companies analyzed in detail: Abbott Laboratories; Alimera Sciences, Inc.; AbbVie Inc.; Ampio Pharmaceuticals, Inc.; Bayer AG; F. Hoffmann-La Roche Ltd; Novartis AG; Pfizer Inc.; Regeneron Pharmaceuticals, Inc.; Bausch Health Companies Inc.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

The Diabetic Retinopathy Market report has evolved from conventional laser-based interventions toward precision treatment approaches centered on anti-VEGF biologics, sustained-release implants, and minimally invasive retinal procedures. Advances in retinal imaging technologies have improved disease detection rates, enabling earlier diagnosis and intervention before irreversible vision deterioration occurs.

Over the coming years, market development will be influenced by expanding diabetic populations, broader healthcare access in emerging economies, and continuous innovation in ophthalmic therapeutics. Companies are increasingly focusing on durable treatment regimens that reduce injection frequency while maintaining efficacy, supporting improved patient adherence and long-term disease management.

Diabetic Retinopathy Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 10.74 Billion |

| Market Size by 2034 | US$ 18.08 Billion |

| Global CAGR (2026 - 2034) | 5.95% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Diabetic Retinopathy Market Analysis

The growing prevalence of diabetes remains the primary driver of market demand. Aging populations, sedentary lifestyles, obesity trends, and rising metabolic disorders have expanded the pool of patients susceptible to diabetic retinal complications. Governments and healthcare organizations are promoting routine retinal examinations, increasing diagnosis rates and treatment uptake.

The diabetic retinopathy market ecosystem includes pharmaceutical manufacturers, ophthalmology clinics, ambulatory surgical centers, diagnostic imaging providers, and healthcare payers. Continuous collaboration among these stakeholders has improved access to treatment while supporting innovation in disease monitoring and therapeutic delivery systems.

Competition is centered on biologic therapies, innovative retinal implants, and next-generation imaging solutions. Companies such as Abbott Laboratories, Bayer AG, F. Hoffmann-La Roche, Regeneron Pharmaceuticals Inc., Novartis International AG, and Pfizer maintain strong positions through diversified ophthalmology portfolios and strategic research initiatives.

Investment activity is increasingly directed toward long-duration retinal therapies, artificial intelligence-enabled diagnostics, and digital ophthalmology platforms. Strategic partnerships between pharmaceutical developers and healthcare technology providers are accelerating product development and expanding commercial reach across both mature and emerging markets.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Diabetic Retinopathy Market: Strategic Insights

Regional Insights

North America Diabetic Retinopathy Market

North America accounts for the largest share of the Diabetic Retinopathy Market and is projected to expand at approximately 5.6% CAGR through 2034. High diabetes prevalence, advanced ophthalmic infrastructure, and favorable reimbursement mechanisms support sustained treatment demand. The region also benefits from strong adoption of retinal imaging technologies and biologic therapies.

Healthcare providers increasingly emphasize preventive eye care and early-stage intervention, strengthening patient outcomes and supporting market growth. Ongoing innovation in retinal therapeutics and AI-driven screening programs further enhances the region's competitive position.

U.S. Diabetic Retinopathy Market

The U.S. represents nearly 75–80% of North America's diabetic retinopathy market value and is expected to grow at a CAGR of around 5.7% during the forecast period. A large diabetic population, extensive healthcare expenditure, and widespread access to specialized ophthalmology services contribute to market leadership.

Major industry participants including Abbott Laboratories, Regeneron Pharmaceuticals Inc., Bayer AG, and F. Hoffmann-La Roche maintain substantial commercial presence in the country. Adoption of anti-VEGF injections, advanced retinal imaging systems, and outpatient vitreoretinal procedures continues to expand, supporting sustained demand across clinical settings.

Europe Diabetic Retinopathy Market

Europe accounts for about 25-30% of global diabetic retinopathy market revenues and is projected to grow at a CAGR of almost 5.4%. The presence of universal healthcare coverage, an efficient diabetes screening program, and high awareness of diabetic retinopathy are key factors driving steady growth in the market.

In the UK, diabetic retinopathy testing is supported through the national diabetic eye screening program and the adoption of AI-enabled retinal examinations. The increasing focus on preventive healthcare is another factor boosting the growth rate.

Germany leads in Europe due to its highly developed healthcare sector, efficient reimbursement structure, and comprehensive ophthalmology setting. Growth is additionally fueled by investment in the digital healthcare sector.

France, Italy, and Spain are important sources of demand, owing to the increasing number of patients with diabetes who use biologics. The increasing availability of specialized retinal treatment services and improved screening promotes market development in the region.

APAC Diabetic Retinopathy Market

Asia Pacific is projected to be the fastest-growing regional diabetic retinopathy market, recording a CAGR exceeding 7.0% during the forecast period while accounting for approximately 20–25% of global revenue. Rapid urbanization, increasing diabetes incidence, and improving healthcare infrastructure are creating substantial growth opportunities.

With a substantial diabetic population, increasing healthcare investments, and greater use of advanced retinal diagnostic devices, China occupies a leading position in the regional market. Government-led programs for chronic diseases are encouraging early diagnosis.

Japan, South Korea, India, and Australia will remain key drivers in boosting regional demand through their increasing healthcare investments, technological advancements, and ophthalmology. Government-led initiatives for diabetes management are projected to contribute to future market growth.

Middle East & Africa Diabetic Retinopathy Market

The Middle East & Africa diabetic retinopathy market is anticipated to register a CAGR of approximately 5.8% through 2034. Rising diabetes prevalence and healthcare modernization efforts are improving access to retinal care services across several countries.

Saudi Arabia leads regional demand due to increasing healthcare investments and comprehensive diabetes management programs. Growing adoption of advanced ophthalmic technologies is supporting market growth.

The UAE and South Africa continue to expand their retinal treatment capabilities through infrastructure development and specialist healthcare services. Broader healthcare access across the rest of the region is expected to contribute to gradual market expansion despite resource disparities.

Segmentation Analysis

Type

- Proliferative Diabetic Retinopathy: Represents the most advanced stage of diabetic retinopathy, characterized by abnormal blood vessel growth on the retina that can cause vitreous hemorrhage and retinal detachment. Market demand is driven by intensive treatment requirements, including anti-VEGF therapy, laser photocoagulation, and vitrectomy procedures to preserve vision.

- Non-Proliferative Diabetic Retinopathy: Accounts for a significant share of diagnosed diabetic retinopathy cases because it develops during the earlier stages of disease progression. Expanding diabetic screening programs, improved retinal imaging technologies, and greater awareness are enabling earlier diagnosis, timely intervention, and better long-term vision preservation outcomes.

Treatment

- Anti-VEGF Drug: Leads the treatment segment due to its proven effectiveness in reducing retinal edema, inhibiting abnormal blood vessel growth, and preserving visual acuity. Continuous advancements in long-acting formulations and improved dosing regimens are enhancing patient compliance, reducing treatment burden, and supporting favorable clinical outcomes.

- Steroid Injection: Used primarily for patients with diabetic macular edema or retinal inflammation who demonstrate inadequate response to anti-VEGF therapy. Advancements in sustained-release corticosteroid implants and injectable formulations are extending therapeutic duration, minimizing treatment frequency, and improving disease management in selected patient populations.

- Laser Surgeries: Remain a widely adopted treatment option for stabilizing diabetic retinopathy by sealing leaking blood vessels and reducing abnormal vascular growth. Innovations in laser platforms, imaging guidance, and treatment precision have enhanced procedural safety, minimized retinal damage, and improved long-term clinical effectiveness.

- Vitrectomy: Reserved for advanced diabetic retinopathy cases involving persistent vitreous hemorrhage, tractional retinal detachment, or severe retinal complications. Improvements in minimally invasive surgical techniques, visualization systems, and microsurgical instrumentation have increased procedural success rates, shortened recovery times, and enhanced postoperative visual outcomes.

Opportunity Snapshot

| Treatment | Revenue Contribution | Trend Tag | Adoption Stage |

| Anti-VEGF Drug | High | Durability | Mature |

| Steroid Injection | Medium | Sustained Release | Scaling |

| Laser Surgeries | Medium | Precision Therapy | Mature |

| Vitrectomy | Low | Surgical Innovation | Scaling |

Diabetic Retinopathy Market Growth Drivers and Impact Analysis

Rising Global Burden of Diabetes and Vision Complications

The continued rise in diabetes prevalence in both developed and emerging economies remains a key driver of growth for the Diabetic Retinopathy Market. Urban lifestyles, obesity, aging demographics, and dietary transitions have expanded the diabetic population worldwide. As diabetes duration increases, the likelihood of retinal complications rises significantly, creating sustained demand for screening, diagnosis, and treatment services.

Diabetic eye care has become a major focus for healthcare facilities, as it poses a significant economic burden on society. There have been advancements in early screening programs, which have led to an increase in the number of patients. These improvements can be seen throughout the value chain, from equipment manufacturers to pharmaceutical firms developing retinal drugs. All market players benefit from increased patient numbers, which drive ongoing treatment demand and stable revenue.

Advancements in Anti-VEGF and Long-Acting Therapeutics

Therapeutic innovation continues to transform the management of diabetic retinopathy. Anti-VEGF drugs have established themselves as the standard of care for many patients due to their ability to control disease progression and preserve visual function. Current research increasingly focuses on extending treatment durability and reducing injection frequency.

Treatment issues such as drug adherence problems are being solved by long-lasting biological drugs, refillable drug delivery to the eye, and drug release implants. A reduction in the burden of treatment increases patient satisfaction and reduces healthcare system utilization. They also present new avenues in which premium prices will be justified by clinical superiority. As new products come to market, competitive advantage becomes a function of efficacy and convenience, reshaping treatment preferences across healthcare systems.

Expansion of Screening Programs and Digital Ophthalmology

Broader implementation of diabetic retinal screening initiatives is significantly improving disease detection rates. Healthcare organizations recognize that early intervention reduces long-term treatment costs and lowers the risk of blindness. As a result, governments and providers are expanding access to retinal imaging and specialist evaluations.

Digital ophthalmology, telemedicine, and artificial intelligence-based image analysis are enhancing screening efficiency and enabling outreach to underserved communities. These tools provide a quick way to diagnose and refer the patient for further care without relying on specialist availability. The rise in diagnosed patients creates business opportunities within the diagnostics, drugs, and surgery parts of the market.

Diabetic Retinopathy Market Future Trends

Integration of Artificial Intelligence in Retinal Diagnostics

AI is now increasingly being recognized as an important part of managing diabetic retinopathy. More complex algorithms can detect retinal abnormalities in images with very high accuracy, leading to earlier detection of changes and timely management of such cases. AI systems have already been implemented in facilities that lack specialists and need improved screening capabilities.

Future implementation is anticipated to evolve from interpretation to predictive analytics, enabling the detection of patients at increased risk of progressing to more serious conditions. The combination of EHRs and remote patient monitoring technologies will further enhance population-level management. With the continued evolution of regulatory and validation processes for applications, the adoption of AI-based diagnostics is expected to increase.

Shift Toward Durable and Minimally Burdensome Therapies

Patient preferences and healthcare economics are encouraging the development of treatments that require fewer clinical visits and injections. Durable biologics, sustained-release implants, and continuous drug-delivery platforms are gaining attention as stakeholders seek more efficient approaches to disease management.

Evolving therapeutic results are expected to shape future investment choices and commercial planning. Companies offering durable treatment benefits, while maintaining efficacy, safety, and alignment with diabetic retinopathy market trends, can provide stronger therapeutic decision alternatives. A reduced treatment burden may encourage improved adherence, thereby supporting sustained, enhanced outcomes and adoption among physicians and individuals.

Diabetic Retinopathy Market Opportunities

Expansion into Underserved Emerging Healthcare Markets

Large portions of the diabetic population in emerging economies remain underdiagnosed or untreated for retinal complications. Healthcare infrastructure improvements, expanding insurance coverage, and rising awareness create significant opportunities for market participants seeking long-term growth.

Organizations can strengthen their market position by establishing local collaborations, training physicians, and delivering affordable treatment options. The expansion of screening networks and digital diagnostic solutions, alongside the diabetic retinopathy market forecast, will enable quicker patient identification and broaden the treatable population. Companies that act early within the fast-expanding healthcare ecosystem will encounter significant opportunities for sustained future growth.

Development of Combination Therapeutic Approaches

The multifaceted nature of diabetic retinopathy etiology makes it possible to develop multi-targeted therapy for this condition. The combined use of anti-VEGF, anti-inflammatory, and other molecular-targeted drugs may lead to better results and less frequent treatment.

By investing in the differentiation of treatment modalities, pharmaceutical companies will be able to cater to the needs of patients who have failed to respond to currently available therapeutic methods. Partnerships of biotech companies, universities, and medical service providers may facilitate innovation. Successful development and introduction of next-generation combined drug therapies will yield great value.

Recent Developments

- March, 2026: Kodiak Sciences Inc. announced positive topline results in the GLOW2 Phase 3 superiority study of Zenkuda for the treatment of patients with diabetic retinopathy. Zenkuda (tarcocimab tedromer) is an anti-vascular endothelial growth factor (VEGF) intravitreal biologic built on Kodiak's proprietary antibody biopolymer conjugate (ABC®) platform.

- December, 2025: The Armed Forces Medical Services announced a collaboration with the Dr. Rajendra Prasad Centre for Ophthalmic Sciences (RPC), AIIMS, and the eHealth AI Unit of the Ministry of Health & Family Welfare (MoHFW), and launched India’s first Artificial Intelligence (AI)–driven community screening programme for Diabetic Retinopathy (DR). The initiative marks a significant step towards strengthening early detection of diabetic eye disease and building a real-time national health intelligence framework.

- August, 2025: Boehringer Ingelheim and Palatin Technologies, Inc., announced a global research collaboration and licensing agreement aiming to develop an innovative therapy for retinal diseases. The collaboration strengthens Boehringer’s innovative and diversified pipeline in retinal conditions and its underlying commitment to vision preservation and protection. Many patients with diabetic retinopathy (DR) continue to experience vision loss or treatment fatigue, underscoring an unmet need.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends