Europe Automotive Logistics Market Trends and Analysis by 2027

Europe Automotive Logistics Market to 2027 - Regional Analysis and Forecasts By Type (Outsourcing and Insourcing); Services (Transportation, Warehousing, Packaging Processes, Integrated Service, and Reverse Logistics); and Sector (Passenger Vehicle, Commercial Vehicle, Tire, and Component)

- Status : Published

- Report Code : TIPRE00006272

- Category : Automotive and Transportation

- No. of Pages : 160

- Available Report Formats :

- Last update date : July 29, 2019

2018 Market Size

US$ 43.25 Bn

Base year value

2027 Forecast

US$ 80.58 Bn

Projected by 2027

CAGR 2019-2027

6.9 %

Growth rate

Addressable Market

US$ 551.50 Bn

(2019-2027)

Automotive logistics market in Europe is expected to grow from US$ 43.25 Bn in 2018 to US$ 80.58 Bn by the year 2027 with a CAGR of 6.9% from the year 2019 to 2027.

The increased focus on expanding the number of automobile manufacturing units across the globe and a significant number of partnerships among automobile manufacturers and logistics partners are the key factors driving the growth of the automotive logistics market. Moreover, the significant proliferation of vehicle manufacturing is anticipated to boost the automotive logistics market growth in the near future. The automotive industry is experiencing significant demand for vehicles, which is pressurizing the vehicle manufacturers to deliver the required amount of vehicles. However, the performance of the vehicle manufacturers remained stable in the past two years, i.e., 2017 and 2018. The rise in demand for passenger and commercial automobiles among the global mass is majorly driven by the rise in disposable income and an increase in manufacturing units in the developed countries and developing economies. Developing economies witnessed a steady growth in the post-recession era, and thus, there was a rise in the disposable incomes of consumers. In western countries, an increase in demand for commercial vehicle is witnessed, which led the countries to experience an increase in the number of commercial vehicle manufacturing units or assembly units. This factor has led the automobile manufacturers to focus on logistics of the various components and vehicle skeleton internationally.

The insourcing type dominated the automotive logistics market in the year 2018 with the highest market share and is expected to boost its dominance during the forecast period. Many companies that run small and medium scale businesses do not have the scale required or the complexity in their shipping operations for contracting logistics service providers. Moreover, maintaining a completely in-house shipping operation provides the companies with complete control over the shipping operations. These operations include negotiating carrier rates, planning and optimizing loads, and executing the distribution plans. The insourcing logistics type mandates the need for an appropriate set of transportation system capabilities as well as the human capital to manage these tasks. The advantages of insourcing logistics include the complete visibility of the supply chain operations of shipments. Increased quality control and control over operations achieved in the insourcing method is driving the insourcing type in automotive logistics market.

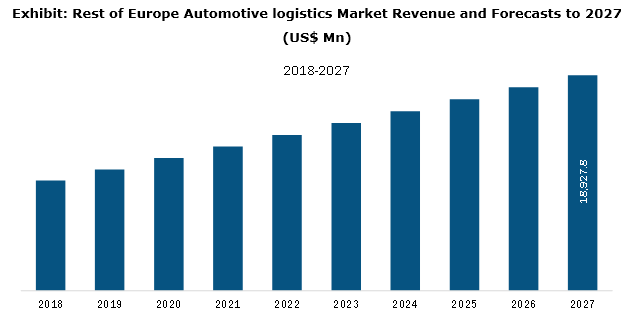

Germany dominated the automotive logistics market in 2018 and is expected to dominate the market with the highest share in the Europe region through the forecast period. Germany is a global leader in premium car production. Of all premium cars and SUVs produced globally, near about 70% is German OEM-manufactured. Also, of all vehicles produced worldwide, almost 25% were produced in Germany. Efficient logistics management has become one of the most important survival factors for the automotive sector, especially for German OEMs and automakers. The easy management and transportation of automobile materials and information in automobile assembly plants have also become the key specification to the rapid growth of German auto manufacturers in order to absorb the very strong competitive pressure of automakers in the global market. The figure given below highlights the revenue share of the rest of Europe in the automotive logistics market in the forecast period:

- This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

EUROPE AUTOMOTIVE LOGISTICS MARKET SEGMENTATION

By Type

- Outsourcing

- Insourcing

By Services

- Transportation

- Warehousing

- Packaging Processes

- Integrated Service

- Reverse Logistics

By Sector

- Passenger Vehicle

- Commercial Vehicle

- Tire

- Component

By Country

- France

- Germany

- Italy

- UK

- Russia

- Rest of Europe

Automotive logistics Market - Companies Mentioned

- CEVA Logistics AG

- DB Schenker (Deutsche Bahn AG)

- DHL International GmbH (Deutsche Post AG)

- DSV A/S

- GEODIS

- KUEHNE + NAGEL International AG

- Nippon Express Co., Ltd.

- Ryder System, Inc.

- XPO Logistics, Inc.

- United Parcel Service, Inc.

Europe Automotive Logistics Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2018 | US$ 43.25 Billion |

| Market Size by 2027 | US$ 80.58 Billion |

| CAGR (2019 - 2027) | 6.9% |

| Historical Data | 2016-2017 |

| Forecast period | 2019-2027 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

Europe

|

| Market leaders and key company profiles |

|

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends