Gas Engine Market Trends, Size & Forecast by 2034

Coverage: By Fuel Type (Natural Gas and Special Gas), Power Output (100-300 KW, 300-500 KW, 0.5-1 MW, 1-2 MW, 2-5 MW, 5-10 MW, and 10-15 MW), End User (Remote, Mid-Stream Oil and Gas, Heavy Industries, Light Manufacturing, Utilities, Biogas, Datacenters, MUSH, Commercial), and Geography (North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America)

- Status : Published

- Report Code : TIPRE00015324

- Category : Energy and Power

- No. of Pages : 603

- Available Report Formats :

- Last update date : March 25, 2026

2025 Market Size

US$ 5.84 Bn

Base year value

2034 Forecast

US$ 9.51 Bn

Projected by 2034

CAGR 2026-2034

5.6 %

Growth rate

Addressable Market

US$ 69.71 Bn

(2026-2034)

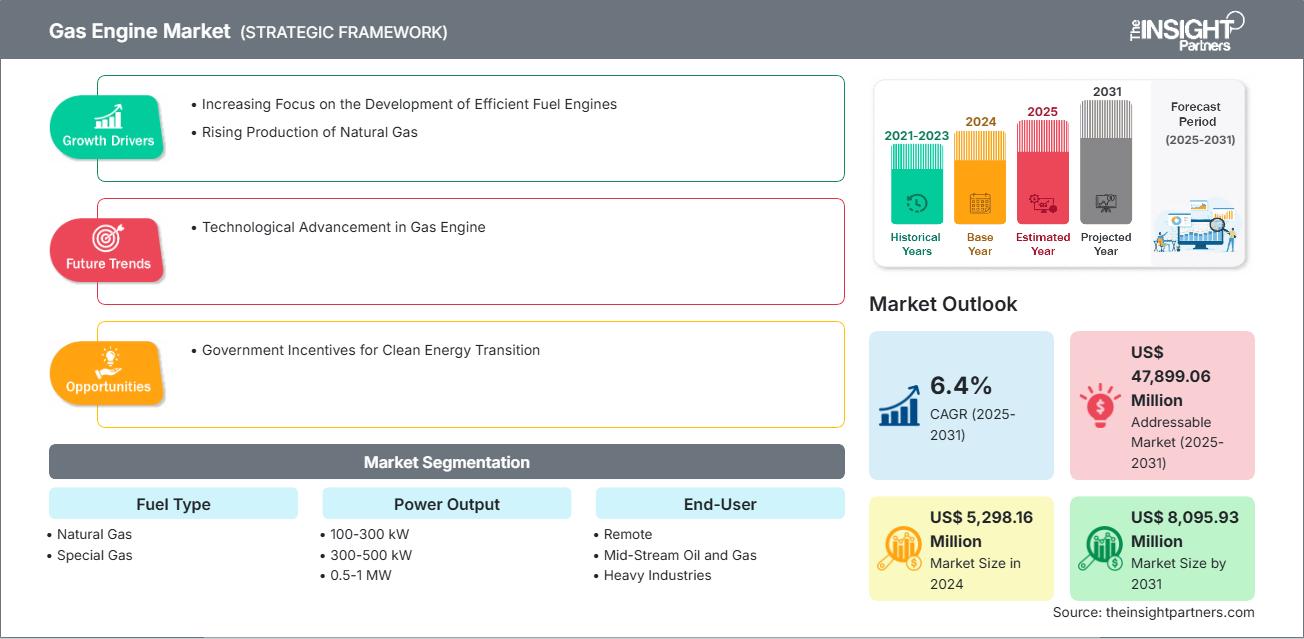

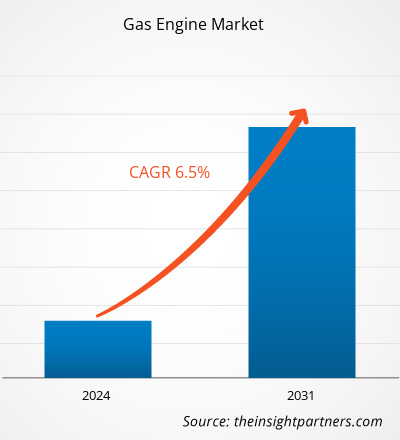

The gas engine market size is expected to reach US$ 9.51 billion by 2034 from US$ 5.84 billion in 2025. The market is anticipated to register a CAGR of 5.6% during 2026 to 2034.

Gas Engine Market Analysis

There is a strong push for developing efficient fuel engines that save energy and cut costs. The rising production of natural gas, along with increased exploration and production activities, is set to drive higher demand for gas engines in the coming years. Governments are offering incentives and support for transitioning to clean energy sources, which will open up promising opportunities for major companies in the market.

Gas Engine Market Overview

Growing demand for low-emission, fuel-efficient engines helps cut air pollution, especially in manufacturing, utilities, and remote power generation. Biogas-powered engines offer better electric efficiency and low emissions. Manufacturers are developing advanced products for high power output that match diesel engine performance. Heavy industries, remote power plants, and factories prefer these high-power gas engines for their efficiency and lower fuel costs. Natural gas combustion in these engines solves emission issues and helps meet tough new regulations.

Market Assessment and Insights

- Europe dominated the market with 36.2% share in 2024.

- Asia Pacific is poised to grow at a CAGR of 7.3% over the forecast period.

- US market is projected to grow at a CAGR of 7.4% over the forecast period.

- By Fuel Type, the Natural Gas segment accounted for the largest market share of 70.3% in 2024.

- By Power Output, the 0.5-1 MW segment is anticipated to witness the fastest growth, registering a CAGR of 7.6% over the forecast period

- By End-User, the Heavy Industries segment accounted for the largest market share of 20.4% in 2024.

- By Remote1, the Drilling segment is anticipated to witness the fastest growth, registering a CAGR of 8.6% over the forecast period

- By Heavy Industries1, the Metals segment accounted for the largest market share of 28.7% in 2024.

- By Utilities1, the IPP segment is anticipated to witness the fastest growth, registering a CAGR of 8.5% over the forecast period

- The report profiles key industry players such as Rolls-Royce Holdings Plc, Cummins Inc, Caterpillar Inc, Liebherr, Mitsubishi Heavy Industries Ltd, IHI Corp, Wartsila Corp, Kawasaki Heavy Industries Ltd, INNIO, Fairbanks Morse, LLC, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Gas Engine Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Gas Engine Market Drivers and Opportunities

Market Drivers:

- Growing demand for reliable, high-efficiency gas engines in power generation and industrial uses: Manufacturers are using advanced materials and designs to deliver longer life, better fuel efficiency, corrosion resistance, and compliance with safety standards for customers.

- Rising energy needs and infrastructure projects worldwide: Regions such as Asia, Africa, and South America are investing in power plants, factories, and remote grids, creating demand for durable gas engines that handle tough conditions.

- Shift to advanced fuels like biogas and tech innovations such as smart engines: Companies are incorporating biogas compatibility, composites, and sensors into gas engines to boost flexibility, cut emissions, and improve performance.

Market Opportunities:

- Expansion across power, industrial, and transportation sectors, driving steady demand for gas engines: These sectors rely on tough gas engines as core components that endure harsh conditions without breaking down.

- Growth potential in emerging markets like Asia and Africa from infrastructure upgrades and power projects: Government plans for modernizing grids, building new plants, and remote electrification are fueling the ongoing need for high-output gas engines.

- Rising emphasis on sustainability, clean fuels, and meeting global emission regulations: As industries shift to green energy transitions, demand continues to grow for eco-friendly gas engines using biogas or hydrogen that are recyclable, low-emission, and energy-efficient.

Gas Engine Market Report Segmentation Analysis

The gas engine market is categorized into distinct segments to understand its structure, growth prospects, and emerging trends. Below is the standard segmentation approach used in industry reports:

By Fuel Type:

- Natural Gas: Industrial power generation in key regions relies on natural gas engines for their high efficiency, abundant supply, and lower emissions compared to diesel.

- Special Gas: Manufacturers are adopting biogas and hydrogen blends, valued for their ultra-low emissions, renewability, and support for green regulations.

By Power Output:

- 100-300 KW: Gas engines with the power output of 100–300 kW are extensively installed in high-rise buildings as well as in industries.

- 300 to 500 kW: These gas engines are used to cover the industrial and commercial load requirements and to generate energy for machine equipment.

- 500 kW to 1 MW: Gas engines with power output from 0.5 to 1 MW are applied to industrial applications.

- 1 MW to 2 MW:

- 2 MW to 5 MW:

- 5 MW-10MW:

- 10 MW to 15 MW

By End User:

- Remote

- Mid-Stream Oil and Gas

- Heavy Industries

- Light Manufacturing

- Utilities

- Biogas

- Datacenters

- MUSH

- Commercial

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Gas Engine Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 5.84 Billion |

| Market Size by 2034 | US$ 9.51 Billion |

| Global CAGR (2026 - 2034) | 5.6% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Fuel Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Gas Engine Market Players Density: Understanding Its Impact on Business Dynamics

The Gas Engine Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Gas Engine Market Share Analysis by Geography

The gas engine market is divided into North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. Europe led the market in 2025, trailed by Asia Pacific and North America.

Europe's gas engine market covers Germany, France, the UK, Russia, and Italy. The region leads in renewable energy adoption, with a shift to cleaner sources strongly driving gas engine growth. Germany, Italy, and the UK are moving to sustainable options, blending natural gas and hydrogen in green strategies. MWM's new TCG 3020 series engine, which handles hydrogen mixes, highlights Europe's push for these fuels. The UK's 2050 carbon-neutral goal and tech investments show a rising need for low-emission gas engines. EU's 2030 emission cuts spur demand in power, transport, and industry.

The gas engine market growth differs in each region due to variations in power infrastructure development, industrialization levels, energy policies, and renewable energy adoption. Below is a summary of market share and trends by region:

1. North America

- Market Share: Holds a significant portion of the global market

- Key Drivers:

- Demand from the oil & gas, automotive, construction, and manufacturing sectors.

- Non-residential construction growth and sustainable solutions in energy management.

- Trends: Continuous research and development activities

2. Europe

- Market Share: Accounted for the largest share, owing to stringent EU regulations

- Key Drivers:

- Robust manufacturing in automotive, chemicals, food & beverages, and construction.

- Utilities, remote sectors, and industrial equipment have notably adopted gas engines; as a result, the demand for gas engines is expected to be multifold in the region.

- Trends: Product development and partnership activities by gas engine manufacturers

3. Asia Pacific

- Market Share: Fastest-growing region with 2nd dominant market share

- Key Drivers:

- Rapid urbanization, infrastructure projects, and manufacturing in China, India, and Japan.

- High demand from automotive, oil & gas, agriculture, and chemicals.

- Trends: Cost-effective, customized gas engines for expanding industrial corridors and exports, and increasing demand for power generation applications

4. Middle East and Africa

- Market Share: Small market share, growing at a rapid pace

- Key Drivers:

- Oil & gas expansion, infrastructure, and construction projects.

- Electrification and industrialization initiatives.

- Trends: Investments in the manufacturing and energy sectors

5. South & Central America

- Market Share: A growing market with steady progress

- Key Drivers:

- Rapid industrialization has contributed to the region’s economic growth. As a result, the energy demand has increased in the manufacturing, oil & gas, and transportation sectors.

- Trends: Carbon emissions norms set by the government for 2030

High Market Density and Competition

Competition is intense due to the presence of major global players such as INNIO; Caterpillar Inc; Cummins Inc; Fairbanks Morse, LLC; Kawasaki Heavy Industries Ltd; Liebherr; Everllence (MAN Energy Solutions SE; Mitsubishi Heavy Industries Ltd; R Schmitt Enertec GmbH; Wartsila Corp; 2G ENERGY AG; IHI Corp; Guascor Energy S.A.U.; Ningbo C.S.I. Power & Machinery Group Co., Ltd.; and Rolls-Royce Holdings Plc.

This high level of competition urges companies to stand out by offering:

- Advanced product features such as efficient fuel consumption, low emissions of nitrogen oxides, and multiple fuel options (biogas, liquefied natural gas, compressed natural gas).

- Value creation services embracing remote monitoring, on-the-spot diagnostics, predictive maintenance, and power plants.

- Custom solutions with integration options for combined heat and power (CHP) applications, microgrid controls, and compatibility with hydrogen fuels.

Opportunities and Strategic Moves

- Manufacturers are collaborating with EPC companies, distributed energy providers, and industrial automation firms to co-develop sector-specific solutions.

- Industry leaders are developing modular engine prototypes and digitization, encouraging retrofitting, rapid upgrades, and API/IoT-enabled connectivity with distributed energy resources and grid management software.

- The increase in local manufacturing and product customization, compliance with local emission standards (Euro VI, EPA Tier 4, China VI), and the use of local service networks.

Other companies analyzed during the course of research:

- General Electric Company (GE)

- Siemens Energy AG

- JFE Engineering Corporation

- Hyundai Heavy Industries Co. Ltd.

- Deutz AG

- Yanmar Co., Ltd.

- Kirloskar Oil Engines Ltd. (India)

- Arrow Engine Company (US)

- Power Solutions International (PSI) (USA)

- Isotta Fraschini Motori S.p.A. (Italy)

- Perkins Engines Company Limited (UK)

- Scania CV AB (Sweden)

Gas Engine Market News and Recent Developments

- INNIO Group launched a new Waukesha VHP Engine Upgrade – In September 2024, INNIO Group announced its newest Waukesha VHP P9390X engine upgrade, designed for simpler operation and increased reliability. The VHP P9390X upgrade offers operators the latest engine technology, extending the life of the equipment by 60% while lowering downtime and reducing emissions across operating conditions.

- In March 2023, MHI launched SGP M2000 natural gas engine system - Mitsubishi Heavy Industries Engine & Turbocharger, Ltd. (MHIET), a part of Mitsubishi Heavy Industries (MHI) Group, launched SGP M2000, a new natural gas engine cogeneration system with a generation output of 2,000 kW. The new package encloses a 16-cylinder natural gas-fired engine, modeled G16NB, that boasts an electrical efficiency of 44.3%, the highest level in the world for a 2,000 kW-class engine, and makes a cogeneration system in compact packaging.

Gas Engine Market Report Coverage and Deliverables

The "Gas Engine Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering the following areas:

- Gas engine market size and forecast at global, regional, and country levels for all the segments covered under the scope

- Gas engine market trends, as well as dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Gas engine market For Healthcare analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the gas engine market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends