Industrial Workwear Market Overview and Growth by 2028

Industrial Workwear Market Forecast to 2028 - Analysis By Product Type (Top Wear, Bottom Wear, and Coveralls), Category (Men, Women, and Unisex), and End Use (Construction, Oil & Gas, Chemicals, Automotive, Manufacturing, and Others)

- Status : Published

- Report Code : TIPRE00014021

- Category : Consumer Goods

- No. of Pages : 157

- Available Report Formats :

- Last update date : June 19, 2024

2021 Market Size

US$ 10.96 Bn

Base year value

2028 Forecast

US$ 16.7 Bn

Projected by 2028

CAGR 2022-2028

6.3 %

Growth rate

Addressable Market

US$ 98.69 Bn

(2022-2028)

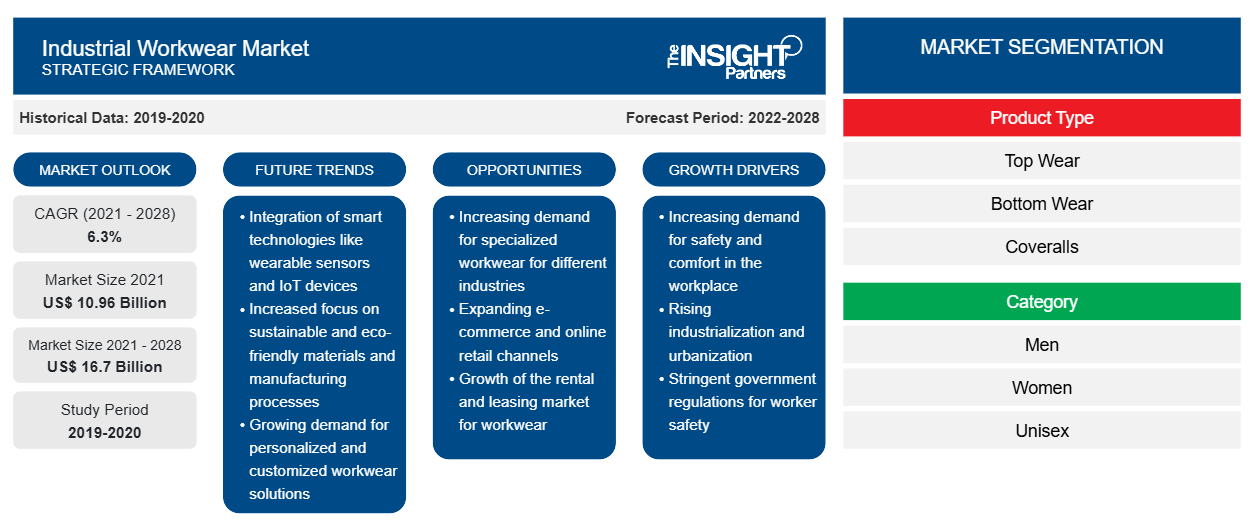

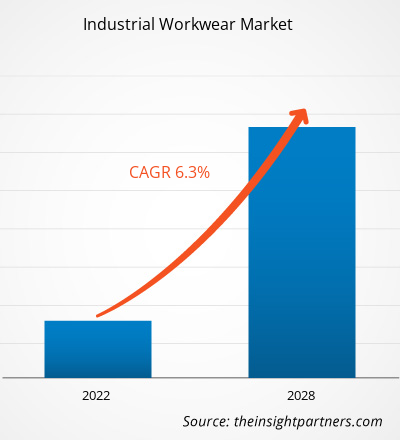

The industrial workwear market is projected to reach US$ 16,697.49 million by 2028 from US$ 10,956.69 million in 2021. It is expected to grow at a CAGR of 6.3% from 2022 to 2028.

Industrial workwear provide safety to workers and ensure a healthy working environment. Workwear is widely used in various sectors, including oil & gas, chemicals, construction, manufacturing, automotive, agriculture, and mining. Over the past few years, workers' safety concerns among industrial sectors have increased rapidly. Various government and safety associations are imposing industrial guidelines to ensure the safety of workers, which has surged the demand for workwear.

In 2020, North America held the largest share of the global industrial workwear market, and Asia Pacific is estimated to register the highest CAGR during the forecast period. The emerging countries in Asia-Pacific, including China and India, are witnessing a surge in work safety measures and expenditures, which offers ample opportunities for the key market players. Asia Pacific is a prominent industrial workwear market due to the rising number of occupational accidents, poor infrastructure, and initiatives to reduce workplace fatality rates. According to International Labour Organization (ILO), published report 2021, more than 1.1 million deaths are recorded in Asia Pacific due to occupational accidents or work-related diseases annually. Countries, such as India, have the least protected, least informed, and least trained workforce. Women, children, disabled workers, migrant workers, and ethnic minorities are among the most affected population and are often involved in occupational accidents. Hence, to reduce occupational accidents and injuries, construction, manufacturing, oil & gas, and many industries are extensively investing in the work safety of their employees. Hence, the increasing awareness regarding work safety is driving the demand for industrial workwear in Asia-Pacific.

Market Research Highlights

- Europe dominated the market with 32.6% share in 2021.

- Asia Pacific is poised to grow at a CAGR of 7% over the forecast period.

- United States market is projected to grow at a CAGR of 5.1% over the forecast period.

- By Product Type, the Top Wear segment accounted for the largest market share of 45.1% in 2021.

- By Category, the Unisex segment is anticipated to witness the fastest growth, registering a CAGR of 6.9% over the forecast period

- By End Use, the Others segment accounted for the largest market share of 37.6% in 2021.

- The report profiles key industry players such as Honeywell International Inc, 3M Co, W L Gore and Associates Inc, IFF Nutrition & Biosciences, Ansell Ltd, Lakeland Industries Inc, Aramark, Kimberly-Clark Corp, Lindström Group, VF Corp, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Industrial Workwear Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Impact of COVID-19 Pandemic on Industrial Workwear Market

The COVID-19 pandemic and extended lockdowns hampered the demand for industrial workwear products in various sectors, including oil & gas, construction, manufacturing, automotive, and chemicals. Industrial workwear are used in various industrial sectors to ensure safety of workers at the workplace. However, the industrial workwear industry faced unprecedented challenges during COVID-19 outbreak in 2020. Manufacturers of industrial workwear faced significant challenges due to supply chain constraints caused by nationwide lockdowns, trade bans, and travel restrictions. The disruptions in supply chains created a shortage of raw materials, which affected the production and distribution of various industrial workwear products.

In 2021, various economies and industries resumed operations as governments announced the relaxation of the previously imposed restrictions. Manufacturers were permitted to operate at full capacity, which helped them overcome the demand and supply gaps. Thus, the workwear manufacturers focused on increasing their production to revive their businesses.

Market Insights

Introduction of Stringent Government Regulations Drives Industrial Workwear Market

The lack of knowledge regarding workplace safety and probable health hazards at workplaces among workers is a significant concern across the world. To raise awareness regarding the same, many government and non-government organizations are introducing various programs and campaigns related to the health and safety of the workers. According to the American Standard Organization, in North America, the US Department of Labor and Occupational Safety and Health Administration (OSHA) standardizes the field of occupational safety and health standards. Organizations involved in the development of standards for protective clothing include the American Society for Testing and Materials (ASTM), National Fire Protection Association (NFPA), National Institute for Occupational Safety and Health (NIOSH), American National Standard Institute (ANSI), American Association of Textile Chemists and Colorists (AATCC), and Industrial Safety Equipment Association (ISEA). Thus, introduction of such stringent government regulation to adopt industrial workwear to ensure safety is expected to drive the growth of the market.

Product Type Insights

Based on product type, the industrial workwear market is segmented into top wear, bottom wear, and coveralls. The top wear segment would hold the largest market share during the forecast period. However, the coveralls segment is expected to register the highest CAGR during the forecast period. Coveralls are single or double pieces of clothing worn to protect the full human body at the workplace. These coveralls are mainly made from nylon, cotton, and polyamide fibers. They are generally used in chemical processing plants and industries, such as paints & coatings and oil & gas, owing to the high risk of occupational hazards. They protect workers from chemical, mechanical, thermal, and biological hazards. Moreover, the increasing occupational safety and awareness, aided by the regulations set in place by the governing bodies, has significantly propelled the demand for industrial workwear.

Category Insights

Based on category, the industrial workwear market is segmented into men, women, and unisex. The men segment would hold the largest share of the market during the forecast period, whereas the unisex segment is projected to register the highest CAGR during the forecast period. According to the World Bank Group June 2022 report, the male workforce participation was 72% in 2021 across the world. As most men work in various industrial and corporate sectors, the demand for industrial workwear is increasing. Moreover, according to the World Health Organization’s (WHO) September 17, 2021 report, almost 2 million men died from work-related causes. Hence, to protect the workforce against occupational injuries and deaths, manufacturers are focusing on new technologies, such as flame-resistant and insulated industrial workwear. The use of such workwear helps reduce the number of occupational deaths and injuries.

End Use Insights

Based on end use, the industrial workwear market is segmented into oil & gas, construction, chemicals, automotive, manufacturing, and others. The manufacturing segment accounted for the largest market share in 2020. The principal cause of industrial accidents in the manufacturing sector is the constant exposure of workers to a dangerous work environment and the unavailability of protective shoes to the workers due to which injuries occur. Protective coveralls, gloves and sleeves, caps/hats, coats, jackets, shirts, socks, softshell jackets, sweatshirts, trousers, face masks, face shields, waistcoats, and protective boots and shoes with protective toecap are specifically designed to protect and safeguard the upper and lower part of the body.

Carhartt, Inc.; ALSICO; A.LAFONT SAS; Honeywell International Inc.; Hultafors Group; Lakeland Inc; Aramark; Ansell Ltd.; VF Corporation; and Mustang Workwear are among the major players operating in the industrial workwear market. These companies are emphasizing on new product launches and geographical expansions to meet the growing consumer demand worldwide. They have a widespread global presence, which provides them to serve a large set of customers from across the world and subsequently increases their market share. These market players focus heavily on new product launches and regional expansions to increase their product range in specialty portfolios.

Industrial Workwear Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2021 | US$ 10.96 Billion |

| Market Size by 2028 | US$ 16.7 Billion |

| Global CAGR (2021 - 2028) | 6.3% |

| Historical Data | 2019-2020 |

| Forecast period | 2022-2028 |

| Segments Covered |

By Product Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Industrial Workwear Market Players Density: Understanding Its Impact on Business Dynamics

The Industrial Workwear Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Report Spotlights

- Progressive industry trends in the industrial workwear market to help companies develop effective long-term strategies

- Business growth strategies adopted by the industrial workwear market players in developed and developing countries

- Quantitative analysis of the market from 2020 to 2028

- Estimation of global demand for workwear

- Porter’s Five Forces analysis to illustrate the efficacy of buyers and suppliers in the industrial workwear market

- Recent developments to understand the competitive market scenario

- Market trends and outlook, as well as factors driving and restraining the growth of the industrial workwear market

- Assistance in the decision-making process by highlighting market strategies that underpin commercial interest

- Size of the industrial workwear market at various nodes

- A detailed overview and industrial workwear industry dynamics

- Size of the industrial workwear market in various regions with promising growth opportunities

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends