Marktwachstum, Größe, Anteil, Trends, Analyse der wichtigsten Akteure und Prognose für industrielle Arbeitskleidung bis 2028

Marktprognose für industrielle Arbeitskleidung bis 2028 – Auswirkungen von COVID-19 und globale Analyse nach Produkttyp (Oberbekleidung, Unterbekleidung und Overalls), Kategorie (Männer, Frauen und Unisex) und Endverwendung (Bau, Öl und Gas, Chemie, Automobil, Fertigung und andere)

- Status : Veröffentlicht

- Berichtscode : TIPRE00014021

- Kategorie : Konsumgüter

- Anzahl der Seiten : 157

- Verfügbare Berichtsformate :

- Datum der letzten Aktualisierung : June 19, 2024

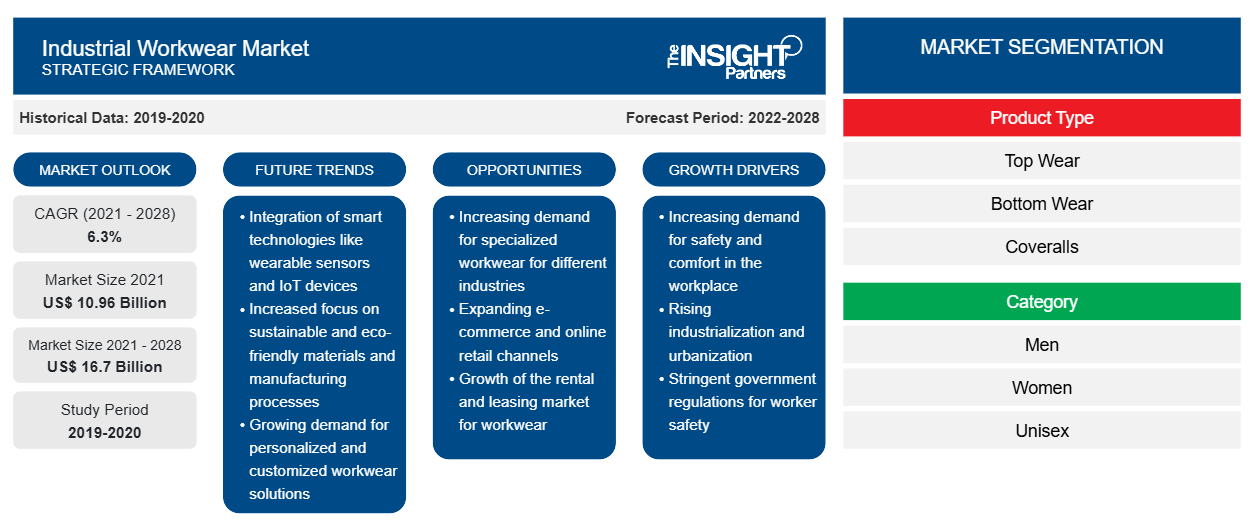

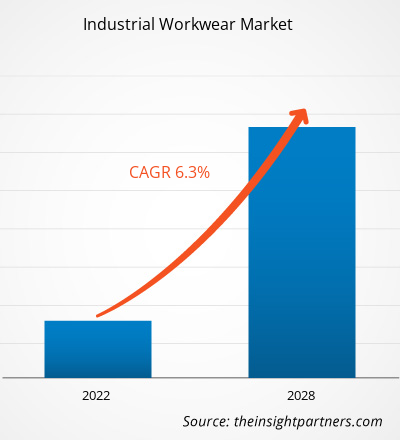

Der Markt für industrielle Arbeitskleidung soll von 10.956,69 Millionen US-Dollar im Jahr 2021 auf 16.697,49 Millionen US-Dollar im Jahr 2028 anwachsen. Von 2022 bis 2028 wird mit einer durchschnittlichen jährlichen Wachstumsrate von 6,3 % gerechnet.

Industrielle Arbeitskleidung bietet den Arbeitern Sicherheit und sorgt für eine gesunde Arbeitsumgebung. Arbeitskleidung wird in vielen Branchen eingesetzt, darunter Öl und Gas, Chemie, Bauwesen, Fertigung, Automobilindustrie, Landwirtschaft und Bergbau. In den letzten Jahren haben die Sicherheitsbedenken der Arbeiter in den Industriezweigen stark zugenommen. Verschiedene Regierungen und Sicherheitsverbände erlassen industrielle Richtlinien, um die Sicherheit der Arbeiter zu gewährleisten, was die Nachfrage nach Arbeitskleidung in die Höhe getrieben hat.

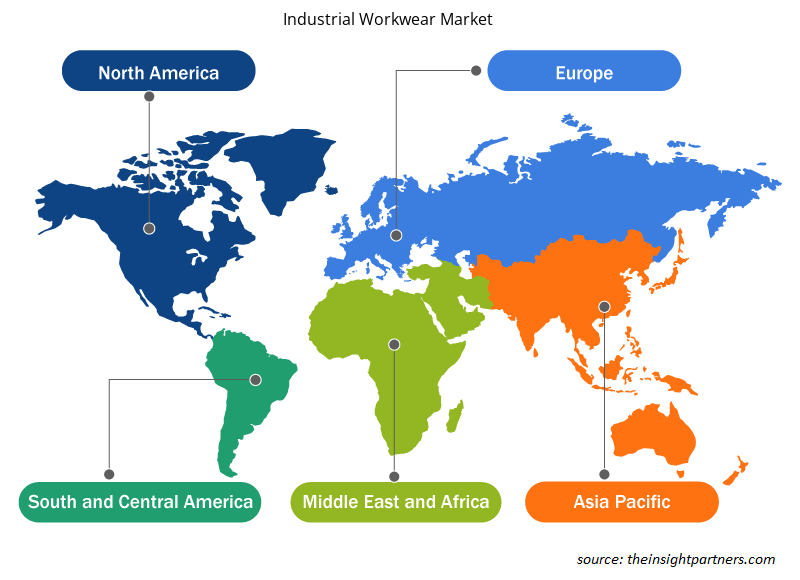

Im Jahr 2020 hatte Nordamerika den größten Anteil am globalen Markt für industrielle Arbeitskleidung , und der asiatisch-pazifische Raum wird im Prognosezeitraum voraussichtlich die höchste durchschnittliche jährliche Wachstumsrate verzeichnen. Die Schwellenländer im asiatisch-pazifischen Raum, darunter China und Indien, erleben einen Anstieg der Arbeitssicherheitsmaßnahmen und -ausgaben, was den wichtigsten Marktteilnehmern reichlich Chancen bietet. Der asiatisch-pazifische Raum ist aufgrund der steigenden Zahl von Arbeitsunfällen, der schlechten Infrastruktur und der Initiativen zur Senkung der Todesrate am Arbeitsplatz ein bedeutender Markt für industrielle Arbeitskleidung. Laut dem veröffentlichten Bericht 2021 der Internationalen Arbeitsorganisation (ILO) werden im asiatisch-pazifischen Raum jährlich mehr als 1,1 Millionen Todesfälle aufgrund von Arbeitsunfällen oder arbeitsbedingten Erkrankungen verzeichnet. Länder wie Indien haben die am wenigsten geschützte, am wenigsten informierte und am wenigsten ausgebildete Belegschaft. Frauen, Kinder, behinderte Arbeitnehmer, Wanderarbeiter und ethnische Minderheiten gehören zu den am stärksten betroffenen Bevölkerungsgruppen und sind häufig in Arbeitsunfälle verwickelt. Um Arbeitsunfälle und Verletzungen zu reduzieren, investieren das Baugewerbe, die Fertigung, die Öl- und Gasindustrie und viele andere Branchen daher umfassend in die Arbeitssicherheit ihrer Mitarbeiter. Daher treibt das zunehmende Bewusstsein für Arbeitssicherheit die Nachfrage nach industrieller Arbeitskleidung im asiatisch-pazifischen Raum an.

Passen Sie diesen Bericht Ihren Anforderungen an

Sie erhalten kostenlos individuelle Anpassungen an jedem Bericht, einschließlich Teilen dieses Berichts oder einer Analyse auf Länderebene, eines Excel-Datenpakets sowie tolle Angebote und Rabatte für Start-ups und Universitäten.

Markt für industrielle Arbeitskleidung: Strategische Einblicke

-

Holen Sie sich die wichtigsten Markttrends aus diesem Bericht.Dieses KOSTENLOSE Beispiel umfasst eine Datenanalyse von Markttrends bis hin zu Schätzungen und Prognosen.

Auswirkungen der COVID-19-Pandemie auf den Markt für industrielle Arbeitskleidung

Die COVID-19-Pandemie und die verlängerten Lockdowns bremsten die Nachfrage nach Arbeitskleidung für Industriebetriebe in verschiedenen Branchen, darunter Öl und Gas, Bauwesen, Fertigung, Automobil und Chemie. Arbeitskleidung für Industriebetriebe wird in verschiedenen Industriezweigen eingesetzt, um die Sicherheit der Arbeitnehmer am Arbeitsplatz zu gewährleisten. Während des COVID-19-Ausbruchs im Jahr 2020 stand die Branche für Arbeitskleidung für Industriebetriebe jedoch vor beispiellosen Herausforderungen. Die Hersteller von Arbeitskleidung für Industriebetriebe standen aufgrund von Lieferketteneinschränkungen aufgrund landesweiter Lockdowns, Handelsverbote und Reisebeschränkungen vor erheblichen Herausforderungen. Die Unterbrechungen in den Lieferketten führten zu einem Mangel an Rohstoffen, der die Produktion und den Vertrieb verschiedener Arbeitskleidungsprodukte für Industriebetriebe beeinträchtigte.

Im Jahr 2021 nahmen zahlreiche Volkswirtschaften und Branchen ihre Arbeit wieder auf, nachdem die Regierungen Lockerungen der zuvor verhängten Beschränkungen ankündigten. Den Herstellern wurde gestattet, mit voller Kapazität zu arbeiten, was ihnen half, die Nachfrage- und Angebotslücken zu überwinden. Daher konzentrierten sich die Hersteller von Arbeitskleidung darauf, ihre Produktion zu steigern, um ihre Geschäfte wiederzubeleben.

Markteinblicke

Einführung strenger staatlicher Vorschriften treibt den Markt für industrielle Arbeitskleidung an

Der Mangel an Wissen über die Sicherheit am Arbeitsplatz und mögliche Gesundheitsrisiken bei Arbeitnehmern ist weltweit ein großes Problem. Um das Bewusstsein dafür zu schärfen, führen viele staatliche und nichtstaatliche Organisationen verschiedene Programme und Kampagnen zur Gesundheit und Sicherheit der Arbeitnehmer ein. Laut der American Standard Organization standardisieren in Nordamerika das US-Arbeitsministerium und die Occupational Safety and Health Administration (OSHA) den Bereich der Arbeitssicherheits- und Gesundheitsstandards. Zu den Organisationen, die an der Entwicklung von Standards für Schutzkleidung beteiligt sind, gehören die American Society for Testing and Materials (ASTM), die National Fire Protection Association (NFPA), das National Institute for Occupational Safety and Health (NIOSH), das American National Standard Institute (ANSI), die American Association of Textile Chemists and Colorists (AATCC) und die Industrial Safety Equipment Association (ISEA). Daher wird erwartet, dass die Einführung solch strenger staatlicher Vorschriften zur Einführung von Arbeitskleidung zur Gewährleistung der Sicherheit das Wachstum des Marktes vorantreiben wird.

Einblicke in Produkttypen

Basierend auf dem Produkttyp ist der Markt für industrielle Arbeitskleidung in Oberbekleidung, Unterbekleidung und Overalls unterteilt. Das Segment Oberbekleidung dürfte im Prognosezeitraum den größten Marktanteil halten. Allerdings wird erwartet, dass das Segment Overalls im Prognosezeitraum die höchste durchschnittliche jährliche Wachstumsrate verzeichnet. Overalls sind ein- oder zweiteilige Kleidungsstücke, die zum Schutz des gesamten menschlichen Körpers am Arbeitsplatz getragen werden. Diese Overalls werden hauptsächlich aus Nylon-, Baumwoll- und Polyamidfasern hergestellt. Aufgrund des hohen Risikos berufsbedingter Gefahren werden sie im Allgemeinen in chemischen Verarbeitungsanlagen und Industrien wie Farben und Lacke sowie Öl und Gas verwendet. Sie schützen Arbeiter vor chemischen, mechanischen, thermischen und biologischen Gefahren. Darüber hinaus hat die zunehmende Arbeitssicherheit und das Bewusstsein, unterstützt durch die von den Verwaltungsbehörden erlassenen Vorschriften, die Nachfrage nach industrieller Arbeitskleidung erheblich angekurbelt.

Kategorie-Einblicke

Der Markt für industrielle Arbeitskleidung ist nach Kategorien in Männer, Frauen und Unisex unterteilt. Das Männersegment wird im Prognosezeitraum den größten Marktanteil halten, während das Unisexsegment im Prognosezeitraum voraussichtlich die höchste durchschnittliche jährliche Wachstumsrate verzeichnen wird. Laut dem Bericht der Weltbankgruppe vom Juni 2022 lag die männliche Erwerbsbeteiligung im Jahr 2021 weltweit bei 72 %. Da die meisten Männer in verschiedenen Industrie- und Unternehmenssektoren arbeiten, steigt die Nachfrage nach industrieller Arbeitskleidung. Darüber hinaus starben laut dem Bericht der Weltgesundheitsorganisation (WHO) vom 17. September 2021 fast 2 Millionen Männer an arbeitsbedingten Ursachen. Um die Belegschaft vor Arbeitsunfällen und Todesfällen zu schützen, konzentrieren sich die Hersteller daher auf neue Technologien wie flammhemmende und isolierte industrielle Arbeitskleidung. Der Einsatz solcher Arbeitskleidung trägt dazu bei, die Zahl der berufsbedingten Todesfälle und Verletzungen zu verringern.

Erkenntnisse zur Endnutzung

Basierend auf der Endnutzung ist der Markt für industrielle Arbeitskleidung in Öl und Gas, Bauwesen, Chemie, Automobil, Fertigung und andere unterteilt. Das Fertigungssegment hatte im Jahr 2020 den größten Marktanteil. Die Hauptursache für Arbeitsunfälle im Fertigungssektor ist die ständige Belastung der Arbeitnehmer durch eine gefährliche Arbeitsumgebung und die fehlende Verfügbarkeit von Schutzschuhen für die Arbeitnehmer, wodurch Verletzungen auftreten. Schutzoveralls, Handschuhe und Ärmel, Mützen/Hüte, Mäntel, Jacken, Hemden, Socken, Softshell-Jacken, Sweatshirts, Hosen, Gesichtsmasken, Gesichtsschutz, Westen sowie Schutzstiefel und -schuhe mit Zehenschutzkappe sind speziell zum Schutz und zur Sicherung des Ober- und Unterkörpers konzipiert.

Carhartt, Inc.; ALSICO; A.LAFONT SAS; Honeywell International Inc.; Hultafors Group; Lakeland Inc; Aramark; Ansell Ltd.; VF Corporation; und Mustang Workwear gehören zu den wichtigsten Akteuren auf dem Markt für industrielle Arbeitskleidung. Diese Unternehmen legen Wert auf die Einführung neuer Produkte und die geografische Expansion, um die weltweit steigende Verbrauchernachfrage zu erfüllen. Sie sind weltweit präsent, sodass sie eine große Anzahl von Kunden auf der ganzen Welt bedienen und so ihren Marktanteil steigern können. Diese Marktteilnehmer konzentrieren sich stark auf die Einführung neuer Produkte und die regionale Expansion, um ihr Produktangebot in Spezialportfolios zu erweitern.

Regionale Einblicke in den Markt für industrielle Arbeitskleidung

Die regionalen Trends und Faktoren, die den Markt für industrielle Arbeitskleidung während des Prognosezeitraums beeinflussen, wurden von den Analysten von Insight Partners ausführlich erläutert. In diesem Abschnitt werden auch die Marktsegmente und die Geografie für industrielle Arbeitskleidung in Nordamerika, Europa, im asiatisch-pazifischen Raum, im Nahen Osten und Afrika sowie in Süd- und Mittelamerika erörtert.

- Erhalten Sie regionale Daten zum Markt für industrielle Arbeitskleidung

Umfang des Marktberichts über industrielle Arbeitskleidung

| Berichtsattribut | Details |

|---|---|

| Marktgröße im Jahr 2021 | 10,96 Milliarden US-Dollar |

| Marktgröße bis 2028 | 16,7 Milliarden US-Dollar |

| Globale CAGR (2021 - 2028) | 6,3 % |

| Historische Daten | 2019-2020 |

| Prognosezeitraum | 2022–2028 |

| Abgedeckte Segmente |

Nach Produkttyp

|

| Abgedeckte Regionen und Länder |

Nordamerika

|

| Marktführer und wichtige Unternehmensprofile |

|

Dichte der Marktteilnehmer für industrielle Arbeitskleidung: Die Auswirkungen auf die Geschäftsdynamik verstehen

Der Markt für Industriearbeitskleidung wächst rasant, angetrieben durch die steigende Nachfrage der Endverbraucher aufgrund von Faktoren wie sich entwickelnden Verbraucherpräferenzen, technologischen Fortschritten und einem größeren Bewusstsein für die Vorteile des Produkts. Mit steigender Nachfrage erweitern Unternehmen ihr Angebot, entwickeln Innovationen, um die Bedürfnisse der Verbraucher zu erfüllen, und nutzen neue Trends, was das Marktwachstum weiter ankurbelt.

Die Marktteilnehmerdichte bezieht sich auf die Verteilung der Firmen oder Unternehmen, die in einem bestimmten Markt oder einer bestimmten Branche tätig sind. Sie gibt an, wie viele Wettbewerber (Marktteilnehmer) in einem bestimmten Marktraum im Verhältnis zu seiner Größe oder seinem gesamten Marktwert präsent sind.

Die wichtigsten Unternehmen auf dem Markt für industrielle Arbeitskleidung sind:

- Carhartt, Inc.

- Aramark

- Alsico-Gruppe

- A. LAFONT SAS

- Honeywell International, Inc.

Haftungsausschluss : Die oben aufgeführten Unternehmen sind nicht in einer bestimmten Reihenfolge aufgeführt.

- Überblick über die wichtigsten Akteure auf dem Markt für industrielle Arbeitskleidung

Bericht-Spotlights

- Fortschrittliche Branchentrends auf dem Markt für industrielle Arbeitskleidung unterstützen Unternehmen bei der Entwicklung wirksamer langfristiger Strategien

- Geschäftswachstumsstrategien der Akteure auf dem Markt für industrielle Arbeitskleidung in Industrie- und Entwicklungsländern

- Quantitative Analyse des Marktes von 2020 bis 2028

- Schätzung der weltweiten Nachfrage nach Arbeitskleidung

- Porters Fünf-Kräfte-Analyse zur Veranschaulichung der Wirksamkeit von Käufern und Lieferanten auf dem Markt für industrielle Arbeitskleidung

- Aktuelle Entwicklungen zum Verständnis des Wettbewerbsmarktszenarios

- Markttrends und -aussichten sowie Faktoren, die das Wachstum des Marktes für industrielle Arbeitskleidung vorantreiben und bremsen

- Unterstützung im Entscheidungsprozess durch Aufzeigen von Marktstrategien, die das kommerzielle Interesse untermauern

- Größe des Marktes für industrielle Arbeitskleidung an verschiedenen Knotenpunkten

- Ein detaillierter Überblick und die Dynamik der Industriearbeitskleidungsbranche

- Größe des Marktes für industrielle Arbeitskleidung in verschiedenen Regionen mit vielversprechenden Wachstumschancen

- Umfassende Analyse der Marktgröße und Prognosen

- Detaillierte Segmentierungsanalyse

- Tiefgehende Bewertung der Marktdynamik

- Einblicke auf regionaler und nationaler Ebene

- Wettbewerbslandschaft und Unternehmens-Benchmarking

- Strategische Business Intelligence

Erfahrungsberichte

Der SCADA-Systemmarktbericht von Insight Partners ist umfassend und bietet wertvolle Einblicke in aktuelle Trends und Zukunftsprognosen. Das Team war durchweg hochprofessionell, reaktionsschnell und hilfsbereit. Wir sind sehr zufrieden und können die Dienstleistungen wärmstens empfehlen.

RAN KEDEM Partner, Reali Technologies LTDsIch habe einen Bericht über einen sehr spezifischen Softwaremarkt angefordert, und das Team hat ihn innerhalb weniger Tage erstellt. Die Informationen waren sehr relevant und gut präsentiert. Anschließend habe ich einige Änderungen und Ergänzungen zum Bericht angefordert. Das Team reagierte erneut sehr schnell, und ich erhielt den Abschlussbericht in weniger als einer Woche.

JEAN-HERVE JENN Vorsitzende, Future AnalyticaWir haben mit The Insight Partners für eine wichtige Marktstudie und Prognose zusammengearbeitet. Sie gaben uns klare Einblicke in Chancen und Risiken, die uns bei der Gestaltung unserer Pläne halfen. Ihre Recherchen waren benutzerfreundlich und basierten auf soliden Daten. Sie halfen uns, kluge und sichere Entscheidungen zu treffen. Wir können sie wärmstens empfehlen.

PIYUSH NAGPAL Sr. Vizepräsident, Fernlicht GlobalDie Insight Partners lieferten aufschlussreiche, gut strukturierte Marktforschung mit fundierter Fachkompetenz. Ihr Team war durchweg professionell und reaktionsschnell. Die benutzerfreundliche Website ermöglichte den Zugriff auf Branchenberichte. Wir empfehlen sie wärmstens für zuverlässige und hochwertige Forschungsdienstleistungen.

YUKIHIKO ADACHI Geschäftsführer, Deep Blue, LLC.Dies ist das erste Mal, dass ich einen Marktbericht von The Insight Partners erworben habe. Obwohl ich zunächst unsicher war, besuchte ich die Website und fühlte mich dann sicherer, das Risiko einzugehen und einen Marktbericht zu kaufen. Ich bin mit der Qualität des Berichts und dem Kundenservice rundum zufrieden. Ich hatte einige Fragen und Anmerkungen zum ersten Bericht, aber nach einigen E-Mail-Gesprächen mit dem Analysten bin ich überzeugt, dass ich einen Bericht habe, den ich als Input für unseren strategischen Planungsprozess verwenden kann. Vielen Dank, dass Sie sich die Zeit genommen und dies zu einer positiven Erfahrung gemacht haben. Ich werde Ihren Service auf jeden Fall weiterempfehlen und Sie werden meine erste Anlaufstelle sein, wenn wir weitere Marktdaten benötigen.

JOHN SUZUKI Präsident und Chief Executive Officer, Vorstandsmitglied, BK TechnologiesIch möchte mich für Ihre Unterstützung und die Professionalität bedanken, die Sie bei der Bearbeitung meiner Informationsanfrage zum IVD-Markt für Infektionskrankheiten in Nigeria gezeigt haben. Ich schätze Ihre Geduld, Ihre Beratung und die Tatsache, dass Sie bereit waren, einen Rabatt anzubieten, der uns schließlich den Abschluss eines Geschäfts ermöglichte. Ich freue mich darauf, The Insight Partners in Zukunft wieder zu beauftragen, dank des Eindrucks, den Sie bei dieser ersten Begegnung bei mir hinterlassen haben.

DR. CHIJIOKE ONYIA GESCHÄFTSFÜHRERIN, PineCrest Healthcare Ltd.Grund zum Kauf

- Fundierte Entscheidungsfindung

- Marktdynamik verstehen

- Wettbewerbsanalyse

- Kundeneinblicke

- Marktprognosen

- Risikominimierung

- Strategische Planung

- Investitionsbegründung

- Identifizierung neuer Märkte

- Verbesserung von Marketingstrategien

- Steigerung der Betriebseffizienz

- Anpassung an regulatorische Trends