Knee Implant Market Share, Trends & Outlook 2031

Coverage: By Type of Procedures (Total Knee Replacement, Partial Knee Replacement, and Revision Knee Replacement), Implant Type (Fixed Bearing Prosthesis and Mobile Bearing Prosthesis), Material (Cemented and Non-Cemented), and End User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, and Others)

- Status : Published

- Report Code : TIPHE100000780

- Category : Life Sciences

- No. of Pages : 250

- Available Report Formats :

- Last update date : February 27, 2026

2024 Market Size

US$ 14.08 Bn

Base year value

2031 Forecast

US$ 19.82 Bn

Projected by 2031

CAGR 2025-2031

5.0 %

Growth rate

Addressable Market

US$ 120.37 Bn

(2025-2031)

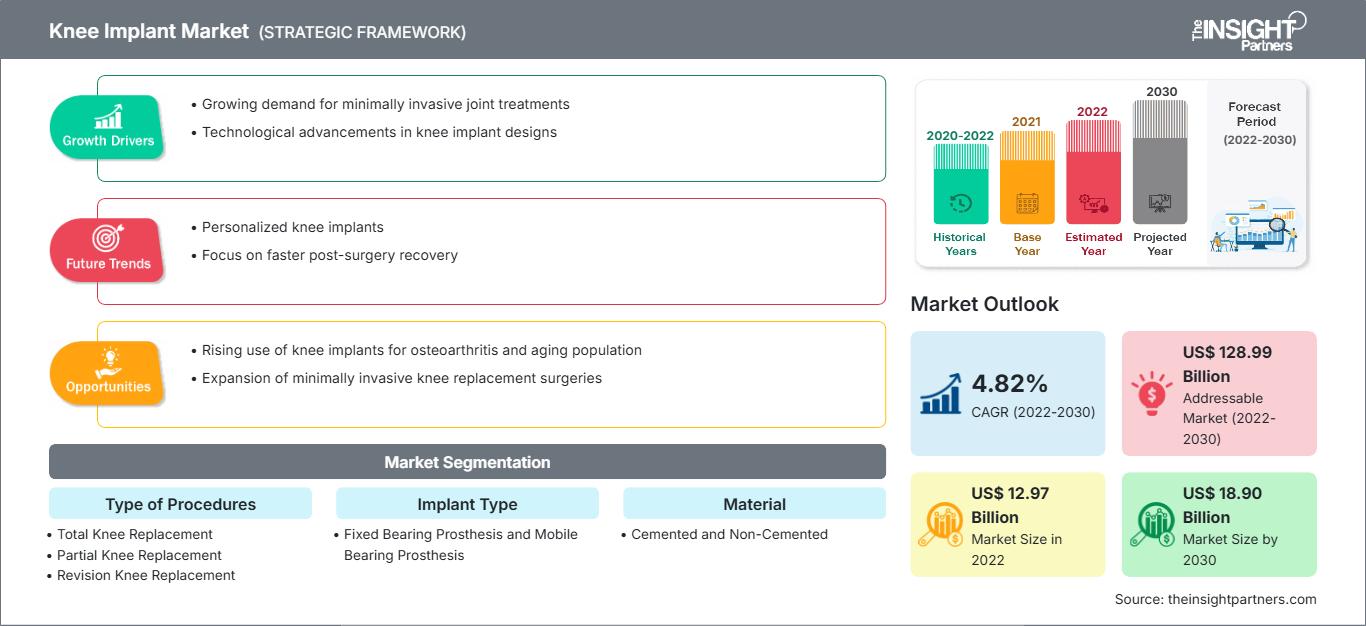

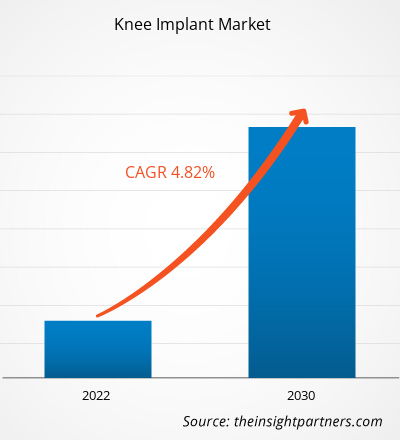

The knee implant market size is projected to reach US$ 19.82 billion by 2031 from US$ 14.08 billion in 2024. The market is expected to register a CAGR of 5.09% during 2025–2031.

Knee Implant Market Analysis

The demand for knee implants is growing due to the rising incidence of osteoarthritis and the global aging population. Innovations in biomaterials, 3D printing, and minimally invasive surgical options enhance implant durability and patient experience. Growing healthcare awareness, supportive reimbursement policies, and a rise in demand for customized knee replacement options spur market growth.

Knee Implant Market Overview

Advances in technology, including 3D-printed personalized implants and minimally invasive surgical procedures, are improving patient outcomes. Increasing healthcare spending, good reimbursement policies, and rising awareness in emerging markets make knee implants a critical segment in the orthopedic medical devices market.

Market Assessment and Insights

- North America dominated the market with 49.3% share in 2024.

- Asia Pacific is poised to grow at a CAGR of 6.7% over the forecast period.

- United States market is projected to grow at a CAGR of 4.6% over the forecast period.

- By Type Of Procedures, the Total Knee Replacement segment accounted for the largest market share of 75.1% in 2024.

- By Implant Type, the Fixed Bearing Prosthesis segment is anticipated to witness the fastest growth, registering a CAGR of 5.4% over the forecast period

- By Material, the Cemented segment accounted for the largest market share of 76.1% in 2024.

- By End User, the Hospitals segment is anticipated to witness the fastest growth, registering a CAGR of 5.6% over the forecast period

- The report profiles key industry players such as MicroPort Scientific Corp, Medtronic Plc, Stryker Corp, Zimmer Biomet Holdings Inc, Smith & Nephew Plc, Conmed Corp, Exactech Inc, B. Braun Melsungen AG, Enovis Corp, Medacta Group SA, while also analyzing key developments in novel ideas, disruptive products, and innovative services that could reshape the future market and reveal emerging themes across the industry.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Knee Implant Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Knee Implant Market Drivers and Opportunities

Market Drivers:

- Aging Population: The worldwide increase of aged populations causes over the time occurrence of degenerative joint diseases like osteoarthritis which hugely affect the need of knee replacement surgeries and implants.

- Technological Advancements: The development in the implant materials, robotics, and 3D printing technologies is the reason for the better outcomes after the operation, the longer life of the implant, and the reduced recovery time, thus making the patients more willing to undergo knee replacement surgery.

Market Opportunities:

- Emerging Markets Expansion: Developing regions such as Asia Pacific and Latin America offer untapped potential due to growing healthcare infrastructure, rising incomes, and increased awareness of joint replacement options.

- Personalized & Custom Implants: Demand is rising for patient-specific implants that are tailored using advanced imaging and manufacturing techniques, offering a better fit, improved function, and higher patient satisfaction post-surgery.

Knee Implant Market Report Segmentation Analysis

The knee implant market is segmented into various categories to provide a clearer understanding of its operation, growth potential, and current trends. Below is the standard segmentation approach used in industry reports:

By Type of Procedures:

- Total Knee Replacement

- Partial Knee Replacement

- Revision Knee Replacement

By Implant Type:

- Fixed Bearing Prosthesis

- Mobile Bearing Prosthesis

By Material:

- Cemented

- Non Cemented

By End User:

- Hospitals

- Orthopedic Clinics

- Ambulatory Surgical Centers

- Others

By Geography:

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Knee Implant Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 14.08 Billion |

| Market Size by 2031 | US$ 19.82 Billion |

| Global CAGR (2025 - 2031) | 5.0% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Type of Procedures

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Knee Implant Market Players Density: Understanding Its Impact on Business Dynamics

The Knee Implant Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Knee Implant Market Share Analysis by Geography

The knee implants industry is characterized by a variety of geographies, where North America is the front-runner that takes advantage of superior healthcare quality, rising osteoarthritis cases, and technology-related healthcare. It is trailed by Europe, where the elderly population and health insurance are the main factors influencing the market. The Asia Pacific region is unfolding rapidly, fueled by the region's rising healthcare investments and the aging populations of China and India. In addition, the Middle East & Africa and Latin America are areas with potential orthopedic care and accessibility that have not yet been explored.

The growth of the knee implant market varies across regions due to factors such as an aging population and the increasing prevalence of mobility-related disorders, which drive demand for knee implant-based therapies. Below is a summary of market share and trends by region:

1. North America

- Market Share: Holds a significant portion of the global market

- Key Drivers:

-

- Increasing Elderly Population

- Technological Advancements

-

Trends:

Joint Replacement in Outpatient

2. Europe

- Market Share: Substantial market share

-

Key Drivers:

- Favorable Reimbursement Policies

- Growing Elderly Population

- Trends: Increasing Medical Tourism

3. Asia Pacific

- Market Share: Fastest-growing region with a rising market share every year

- Key Drivers:

-

- Expanding Healthcare Access

- Increasing Osteoarthritis Cases

- Trends: Domestic Manufacturing Boom

4. South and Central America

- Market Share: Growing market with steady progress

- Key Drivers:

-

- Urbanization and Lifestyle Changes

- Growing Private Healthcare

- Trends: Health Insurance Growth

5. Middle East and Africa

- Market Share: Growing market with steady progress

-

Key Drivers:

- Rising Healthcare Investment

- Increasing Life Expectancy

- Trends: Orthopedic Centers of Excellence

Knee Implant Market Players Density: Understanding Its Impact on Business Dynamics

High Market Density and Competition

One of the competitive advantages that the competition has in this market is the presence of well-established companies among which we can mention Zimmer Biomet and Stryker Corporation.

This high level of competition urges companies to stand out by offering:

- Advanced Products

- Value-added services like customization and sustainable solutions

- Competitive pricing models

- Compliance with regulatory guidelines

Opportunities and Strategic Moves

- June 2024: Zimmer Biomet signed a distribution agreement with THINK Surgical, Inc. to broaden exposure to the TMINI Robotic Knee System for robotic bone cuts and 3D planning.

-

January 2024:

Zimmer Biomet introduced the Persona IQ smart knee implant that monitors recovery in real-time

.

Major Companies operating in the Knee Implant Market are:

- Zimmer Biomet Holdings Inc.

- Smith & Nephew plc

- DePuy Synthes (Johnson & Johnson MedTech)

- Stryker Corporation

- Medacta International SA

- Conformis Inc.

- Arthrex Inc.

- Exactech Inc.

- MicroPort Scientific Corporation

- LimaCorporate S.p.A.

- Enovis Corporation (DJO Global)

- Aesculap Implant Systems (B. Braun)

- Corin Group

- Medtronic plc

- CONMED Corporation

- THINK Surgical Inc.

- United Orthopedic Corporation

- Maxx Orthopedics Inc.

- OrthAlign Inc.

- Exatech Inc.

Disclaimer: The companies listed above are not ranked in any particular order.

Other companies analyzed during the course of research:

- ARTIQO GmbH

- Hospital for Special Surgery (HSS)

- Kinamed Inc.

- B. Braun SE

- Uteshiya Medicare

- Evonic Medical Devices

- Physica System (MicroPort)

- SurgTech Inc.

- LINK Orthopaedics

- Medial Rotation Knee (MRK)

- Waston Medical Appliance Co.

- BBRAUN Aesculap

- ATTUNE Knee (DePuy)

- JOURNEY II (Smith & Nephew)

- K-MONO System (Medacta)

- GKS PRIME Flex TRASER

- Unicompartmental (Corin)

- Columbus (Aesculap)

- Optetrak Logic (Exactech)

- iUni (Conformis)

Knee Implant Market News and Recent Developments

- October 2024: Smith+Nephew launched the LEGION Hinged Knee System in the US, targeting.

- March 2023: Stryker launched Mako Total Knee 2.0, advancing smart robotics for knee replacement.

Knee Implant Market Report Coverage and Deliverables

The "Knee Implant Market Size and Forecast (2021–2031)" report provides a detailed analysis of the market covering below areas:

- Knee Implant Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Knee Implant Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Knee Implant Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Knee Implant Market

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends