Magnesia Chrome Brick Market Growth, Demand & Size by 2034

Magnesia Chrome Brick Market Size and Forecasts (2021 - 2034), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage : by Type (Chemically Bonded, Direct Bonded, Fused/Rebonded, Fused Cast); End Use (Power generation, Non-Ferrous metals, Cement, Glass, Iron and steel); and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00040373

- Category : Chemicals and Materials

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 16, 2026

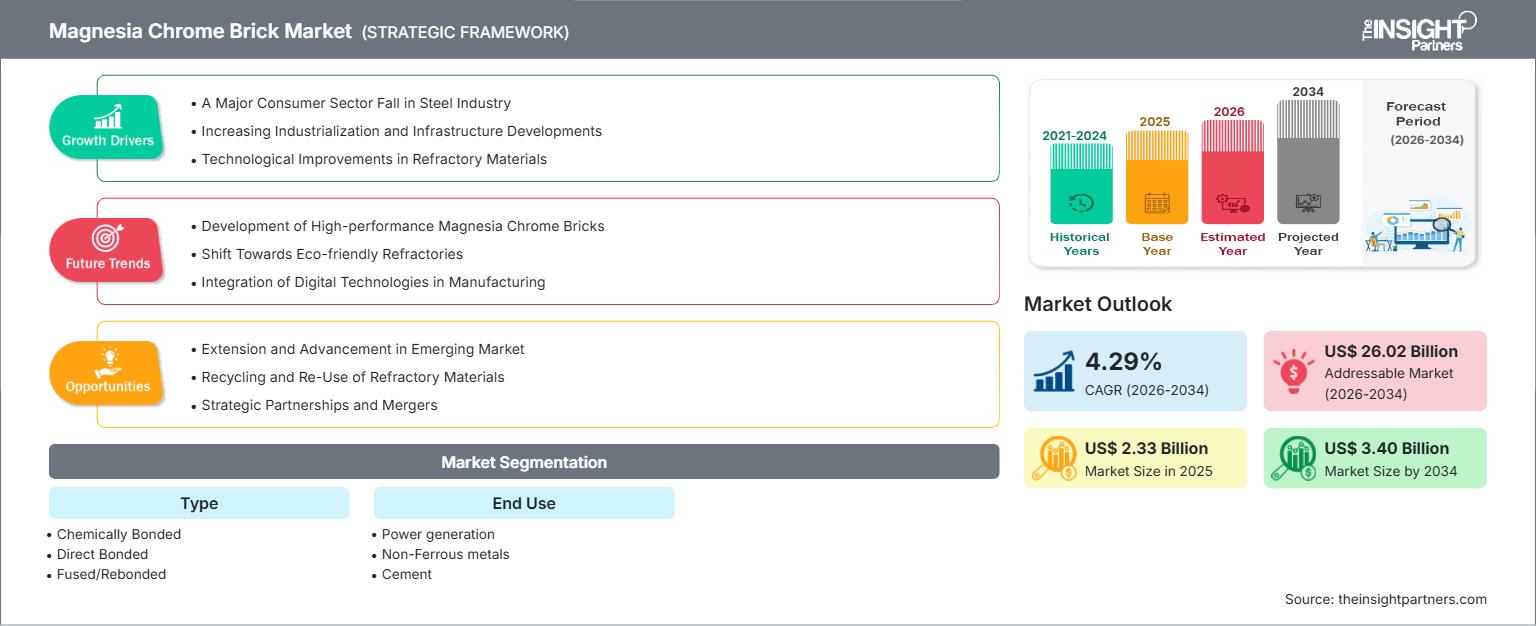

2025 Market Size

US$ 2.33 Bn

Base year value

2034 Forecast

US$ 3.40 Bn

Projected by 2034

CAGR 2026-2034

4.29 %

Growth rate

Addressable Market

US$ 26.02 Bn

(2026-2034)

The magnesia chrome brick market size was valued at US$ 2.33 Billion in 2025 and is projected to reach US$ 3.40 Billion by 2034, expanding at a CAGR of 4.29% during 2026–2034. Demand continues to be supported by the extensive use of high-performance refractory materials in steelmaking, non-ferrous metallurgy, glass manufacturing, cement production, and power generation. Increasing operating temperatures across industrial furnaces and longer maintenance cycles are encouraging manufacturers to develop refractory bricks with improved corrosion resistance, thermal shock stability, and extended service life.

Across North America, replacement demand from mature steel plants and modernization investments in cement and glass production facilities continue to support steady consumption. The magnesia chrome brick market size in the region is anticipated to expand at a CAGR of 3.6–4.2% through 2034 as furnace relining cycles become increasingly focused on lifecycle cost reduction and operational efficiency. Environmental compliance initiatives and investments in energy-efficient industrial infrastructure further strengthen long-term demand for premium refractory products.

Magnesia Chrome Brick Market Assessment and Insights

- North America: Accounted for 20–24% of the magnesia chrome brick market share in 2025 and is expected to grow at a CAGR of 3.6–4.2% during 2026–2034. Stable steel production, modernization of cement facilities, and increasing investments in industrial energy infrastructure continue to support refractory replacement demand.

- US: Represented 72–76% of North American demand in 2025 and is projected to register a CAGR of 3.7–4.3% during 2026–2034, supported by integrated steel mills, electric arc furnace expansion, and infrastructure-related industrial investments.

- Europe: Held 24–28% share in 2025 and is anticipated to expand at a CAGR of 3.4–4.0% during 2026–2034. Germany, Italy, France, and Spain remain major consuming countries owing to advanced metallurgical and glass manufacturing industries.

- Asia Pacific: Captured 42–46% share in 2025 and is forecast to grow at a CAGR of 4.8–5.4% during 2026–2034. China, India, Japan, and South Korea continue to dominate regional consumption through expanding steelmaking and industrial manufacturing capacity.

- Largest Segment: Iron and steel accounted for 48–52% market share in 2025 and is expected to grow at a CAGR of 4.4–4.9% during 2026–2034, driven by continuous refractory replacement requirements in basic oxygen and electric arc furnaces.

- High Growth Segment: Non-Ferrous metals represented 15–19% market share in 2025 and is projected to register the fastest CAGR of 5.2–5.8% during 2026–2034, supported by increasing aluminum, copper, and nickel processing capacity.

- Key companies analyzed in detail: Calderys, Gita Refractories, HarbisonWalker International, JBTC, KT Refractories, Lanexis, Liaoning Lian Refractories Co., Ltd., Magnezit Group, Mayerton Refractories, and Puyang Refractories Group Co., Ltd.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

Refractory manufacturing in the industrial setting has undergone much change as manufacturers place increasing emphasis on optimizing raw materials, computerized quality control, and improved bonding brick formulations. Changes in grain processing, impurity removal, and kilns have resulted in better thermal stability and corrosion resistance as well as lower life-cycle operating expenses. This trend has positively affected the future growth prospects for magnesia chrome brick products, especially for use in the harsh conditions prevalent in metallurgy where furnace availability has an impact on plant output and maintenance.

Countries in their economic development stage are investing in integrated steel plants, copper refineries, cement lines, and glass manufacturing facilities, thereby offering opportunities to the refractory industry. Efforts towards sustainable growth are driving up demand for durable refractories that would keep the number of furnace shutdowns down and reduce material usage. Expansion in Asia, the Middle East, as well as certain African countries, along with modernization efforts in developed countries, will foster balanced long-term growth in the sector.

Magnesia Chrome Brick Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 2.33 Billion |

| Market Size by 2034 | US$ 3.40 Billion |

| Global CAGR (2026 - 2034) | 4.29% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Magnesia Chrome Brick Market Analysis

Increased production of steel, expansions of capacity in non-ferrous metals processing, as well as modernizations of plants engaged in cement and glass production support increased demand for high-quality refractories globally. The segment of magnesia chrome bricks profits from the need for refractory lining capable of withstanding temperatures above 1,700°C and resistance to chemical attack, slag intrusion and thermal stress. According to the magnesia chrome brick market analysis, steel companies are becoming more focused on products with enhanced campaign life as the performance of refractories has direct impact on furnace availability and productivity. Moreover, increased investments in electric arc furnaces and advanced kilns generate stable demand for innovative types of chemically bonded and direct bonded magnesia chrome bricks.

Value chain in the market starts with the supply of raw materials for magnesia chrome bricks, including magnesite ore, chromite, and fused refractory materials, as well as processes of crushing, enrichment, sintering, brick formation, firing, testing and distribution to customers. Consistent supply of raw materials, rigorous quality control and collaboration between producers of refractories and furnace users are still crucial for the stability of the performance of the products. Increased adoption of digital monitoring systems by furnace operators helps to plan the schedule.

The competition in the magnesia chrome brick market report is based on the constant introduction of new products, geographic expansions of manufacturing, and the signing of long-term contracts for the supplies to large steel producers. The market leaders such as Calderys, HarbisonWalker International, Magnezit Group, Liaoning Lian Refractories Co., Ltd., and Puyang Refractories Group Co., Ltd. remain engaged in manufacturing innovations, application engineering, and developing specific solutions to high-temperature applications. At the same time, there are also Gita Refractories, KT Refractories, Mayerton Refractories, Lanexis, and JBTC that add to the competition by delivering their services and specific products in various industries.

The increasing strategic investments are oriented towards the manufacturing process automation, the securing of raw materials sources, spent refractory recycling, and environmental production processes development. Moreover, the technical services of manufacturers are constantly expanded due to close cooperation with customers to optimize furnace linings designs and prolong the operating cycles. The joint ventures with steel, cement, glass, and non-ferrous metal manufacturers become more and more common as customers require full refractory management solutions, rather than mere products.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Magnesia Chrome Brick Market: Strategic Insights

Regional Insights

North America Magnesia Chrome Brick Market

North America accounted for 20–24% of the global market in 2025 and is anticipated to expand at a CAGR of 3.6–4.2% during 2026–2034. Market share of magnesia chrome brick in the region is driven by consistent investments in steel making, cement production, glass fabrication and power generation. The replacement demand continues to be an important driver of growth as refractory bricks that increase the efficiency of the furnaces are preferred by industries. Modernization projects in integrated steel plants and electric arc furnaces keep driving consumption.

Increasing focus on decarbonizing industries and efficient furnace technologies is propelling the use of superior direct-bonded and fused/rebonded refractory bricks. The U.S. is leading the demand in the region, whereas the demand from Canada is coming from metallurgical and mining industries. Refractory companies are also working on improving their technical assistance services as well as inventory management capabilities to assure constant supply of products to continuous process industries. Increasing infrastructure investments and industrial output will help sustain stable long-term demand for refractory bricks.

U.S. Magnesia Chrome Brick Market

The United States represented 72–76% of North American demand in 2025 and is projected to record a CAGR of 3.7–4.3% during 2026–2034. Domestic demand is primarily generated by integrated steel mills, electric arc furnace operations, specialty alloy manufacturing, glass production, and cement plants. Continuous modernization of industrial facilities and increasing adoption of automation technologies are encouraging the use of durable refractory materials capable of supporting higher production efficiency and extended furnace campaigns.

Several leading refractory suppliers maintain manufacturing, distribution, or technical service operations across the country, enabling close collaboration with steel and cement producers. Growth in infrastructure projects, manufacturing reshoring initiatives, and increasing investment in non-ferrous metal processing further support market expansion. The availability of advanced engineering expertise and strong industrial maintenance practices is expected to sustain replacement demand throughout the forecast period.

Europe Magnesia Chrome Brick Market

Europe accounted for 24–28% of the global magnesia chrome brick market report market in 2025 and is forecast to register a CAGR of 3.4–4.0% during 2026–2034. Germany remains the largest regional market owing to its advanced steel, glass, and industrial manufacturing sectors. Ongoing investments in energy-efficient production technologies and furnace modernization continue to support demand for premium refractory solutions with improved operational life.

The United Kingdom maintains steady consumption through specialty steel production, cement manufacturing, and industrial furnace refurbishment activities. France, Italy, and Spain collectively contribute significant demand supported by established glass manufacturing, metallurgical processing, and cement industries. Across Europe, stricter environmental regulations are encouraging manufacturers to adopt longer-lasting refractory products that reduce maintenance frequency, improve thermal efficiency, and support sustainability objectives while maintaining high-temperature process reliability.

APAC Magnesia Chrome Brick Market

Asia Pacific captured 42–46% of the global market in 2025 and is expected to expand at a CAGR of 4.8–5.4% during 2026–2034. China remains the largest consumer owing to its dominant steelmaking capacity, followed by India, Japan, and South Korea. Growing industrialization, urban infrastructure development, and investments in non-ferrous metallurgy continue to stimulate refractory demand.

Government initiatives supporting domestic manufacturing, capacity expansion in cement production, and modernization of industrial furnaces further strengthen regional growth. Australia contributes through mining and mineral processing operations requiring high-performance refractory linings for smelting and refining applications.

Middle East & Africa Magnesia Chrome Brick Market

The Middle East & Africa is anticipated to record a CAGR of 4.5–5.1% during 2026–2034, supported by investments in steelmaking, cement manufacturing, and non-ferrous metal processing. Saudi Arabia and the United Arab Emirates continue expanding industrial capacity through large-scale infrastructure and manufacturing projects, while South Africa remains an important market due to its mining and metallurgical industries.

Increasing industrial diversification strategies, coupled with investments in energy infrastructure and downstream metal processing, are expected to strengthen regional refractory consumption. Demand is also supported by modernization of existing industrial plants and the construction of new high-temperature processing facilities across selected Middle Eastern and African economies.

Segmentation Analysis

Type

The Type segment is projected to grow at a CAGR of 4.1–4.7% during 2026–2034. Product selection depends on furnace operating conditions, thermal load, slag chemistry, and maintenance requirements. The magnesia chrome brick market scope continues to expand as industrial users adopt advanced brick technologies that improve corrosion resistance and extend furnace campaign life. Manufacturers are increasingly focusing on optimized bonding techniques and higher-purity raw materials to enhance durability while lowering lifecycle operating costs.

- Chemically Bonded – Widely used where moderate thermal performance and cost efficiency are priorities. These bricks offer reliable mechanical strength and are commonly selected for secondary furnace applications and maintenance projects requiring economical refractory solutions.

- Direct Bonded – Manufactured using high-purity raw materials to achieve excellent corrosion resistance and thermal stability. They are extensively adopted in steelmaking vessels and cement kilns operating under severe chemical and thermal conditions.

- Fused/Rebonded – Designed for highly demanding furnace environments, these products provide superior resistance to slag attack, thermal shock, and structural degradation. They are increasingly preferred in copper smelters, nickel processing, and high-temperature metallurgical operations.

- Fused Cast – Engineered for applications requiring exceptional density, wear resistance, and dimensional stability. Their performance under prolonged exposure to aggressive molten materials makes them suitable for specialized glass and metallurgical processing equipment.

End Use

The End Use segment in the magnesia chrome brick market is expected to expand at a CAGR of 4.4–5.0% during 2026–2034. Consumption patterns are influenced by industrial production volumes, furnace operating temperatures, maintenance intervals, and capital investments across heavy industries. Steel manufacturing remains the dominant consumer, while non-ferrous metallurgy is emerging as the fastest-growing application due to increasing production of aluminum, copper, and battery-related metals.

- Power generation – Refractory bricks are utilized in high-temperature boilers, waste-to-energy plants, and thermal processing systems where resistance to heat, abrasion, and chemical attack contributes to reliable long-term plant operation.

- Non-Ferrous metals – Growing investments in aluminum, copper, nickel, and critical mineral processing are driving increased adoption of premium refractory materials capable of withstanding aggressive smelting and refining environments.

- Cement – Rotary kilns require refractory linings that tolerate continuous thermal cycling and clinker-related chemical exposure. Long service life and reduced shutdown frequency remain key purchasing considerations for cement manufacturers.

- Glass – Glass furnaces operate continuously under extremely high temperatures, creating demand for refractory bricks offering excellent dimensional stability, corrosion resistance, and extended operational durability throughout production campaigns.

- Iron and steel – The largest application segment due to continuous refractory replacement in basic oxygen furnaces, electric arc furnaces, ladles, converters, and secondary metallurgy units. Increasing steel production and plant modernization continue supporting long-term demand.

Opportunity Snapshot

| Segment Name | Revenue Contribution | Trend Tag | Adoption Stage |

| Power generation | Medium | Boiler Upgrade | Mature |

| Non-Ferrous metals | High | Battery Metals | Scaling |

| Cement | High | Kiln Modernization | Mature |

| Glass | Medium | Furnace Rebuild | Mature |

| Iron and steel | High | EAF Expansion | Mature |

Magnesia Chrome Brick Market Growth Drivers and Impact Analysis

Expansion of Steel Production and Furnace Modernization

The global producers of steel keep on investing in the upgrades of blast furnaces, installing electric arc furnaces, and secondary metallurgy facilities in order to enhance productivity and reduce energy consumption. This results in an increased need for refractory lining materials, which can work under harsh conditions. The magnesia chrome bricks have been found to be the ideal solution for such furnaces due to its superior capability to withstand slag erosion, thermal shock, and mechanical abrasion. The requirement of longevity and low maintenance costs in furnaces has brought about the focus on lifetime performance of the products instead of their cost at procurement time. The continued growth of infrastructure, automobile production, renewable energy initiatives, and industry in developing nations is expected to keep the demand for refractories going for the forecast period.

Growth in Non-Ferrous Metal Smelting Capacity

Increasing global demand for aluminum, copper, nickel, and other strategic metals is encouraging investments in new smelters and capacity expansion projects. The transition toward electric vehicles, renewable energy systems, transmission infrastructure, and battery manufacturing has accelerated consumption of non-ferrous metals, requiring reliable high-temperature processing equipment. Magnesia chrome bricks provide the corrosion resistance and structural integrity necessary for these aggressive operating environments. As producers strive to maximize furnace availability and improve metal recovery rates, premium refractory solutions become increasingly valuable. Growing investments across Asia Pacific, the Middle East, and selected African countries are expected to strengthen long-term demand while encouraging refractory manufacturers to develop application-specific products for advanced metallurgical processes.

Increasing Focus on Operational Efficiency and Asset Life

Industrial operators are placing greater emphasis on minimizing unplanned shutdowns and reducing total maintenance expenditure through improved refractory performance. Longer-lasting furnace linings contribute directly to higher production efficiency, lower replacement frequency, and improved energy utilization. Manufacturers are responding by developing products with enhanced purity, optimized bonding technology, and improved resistance to chemical attack. Technical service capabilities, including furnace inspection, installation support, and predictive maintenance, have become important competitive differentiators. As industrial facilities adopt digital monitoring systems and performance-based maintenance strategies, demand for premium refractory materials capable of delivering consistent operational reliability is expected to increase steadily throughout the forecast period.

Magnesia Chrome Brick Market Future Trends

Development of Sustainable Refractory Manufacturing Technologies

Environmental regulations and corporate sustainability objectives are encouraging refractory manufacturers to reduce energy consumption, increase recycled material utilization, and improve manufacturing efficiency. The Magnesia Chrome Brick Market trends increasingly reflect increasing investments in cleaner production technologies, optimized firing processes, and responsible raw material sourcing to reduce environmental impact. Research into alternative raw materials and improved recycling of spent refractories is expected to gain momentum. These initiatives will enable manufacturers to support customers' decarbonization goals while maintaining the high mechanical strength and corrosion resistance required for demanding industrial applications. Sustainability will increasingly influence purchasing decisions across steel, cement, and glass industries during the coming decade.

Digitalization of Refractory Performance Management

Industrial companies are increasingly integrating digital technologies into furnace operations to improve refractory management and maintenance planning. Predictive analytics, real-time temperature monitoring, and digital inspection tools allow operators to optimize replacement schedules and maximize campaign life. Refractory suppliers are expanding technical services by offering performance monitoring, installation guidance, and lifecycle optimization programs. The integration of operational data with refractory engineering is expected to improve furnace efficiency, reduce operational interruptions, and strengthen long-term customer partnerships. Digital service capabilities are likely to become an important competitive advantage across the global refractory industry.

Magnesia Chrome Brick Market Opportunities

Expansion in Emerging Industrial Economies

Industrialization across India, Southeast Asia, the Middle East, and Africa continues to create significant investment opportunities for refractory manufacturers. Growing steelmaking capacity, cement production, glass manufacturing, and non-ferrous metal processing require reliable high-temperature refractory materials. Local manufacturing partnerships, regional distribution centers, and technical service capabilities can strengthen supplier competitiveness while reducing delivery times. Companies capable of offering customized refractory solutions and comprehensive engineering support are well positioned to benefit from increasing industrial investment. Magnesia Chrome Brick Market Forecasts indicate that emerging economies will remain key contributors to incremental demand over the long term as industrial production continues expanding.

High-Performance Product Innovation

Continuous research into higher-purity raw materials, optimized bonding technologies, and advanced manufacturing processes presents substantial opportunities for product differentiation. Industrial customers increasingly seek refractory solutions that deliver longer furnace campaigns, lower maintenance costs, and improved thermal efficiency. Manufacturers investing in application-specific product development, digital engineering support, and integrated refractory management services can strengthen customer relationships and improve profitability. Innovation focused on enhanced corrosion resistance, thermal shock performance, and sustainability will remain central to future competitive positioning, particularly as industrial operators continue prioritizing operational efficiency and lifecycle value over initial procurement costs.

Recent Developments

- July 2026: Gouda Refractories Group BV with its headquarters in Gouda, the Netherlands (hereinafter referred to as 'Gouda') acquired Revestimientos Refractarios located in Madrid, Spain. The cooperation between Gouda and Revestimientos Refractarios goes back many years. In recent years both companies have intensified their cooperation which, due to a natural moment of succession, has led to this acquisition.

- March 2026: The Institute of Minerals and Materials Technology (IMMT), Bhubaneswar, developed a technology to convert bauxite mining waste into high-performance refractory bricks, unlocking the potential of a long-neglected resource in mineral-rich Odisha.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends