North America Data Center Colocation Market Analysis and Forecast by Size, Share, Growth, Trends 2031

Coverage: By Type (Retail Colocation, Wholesale Colocation, and Hybrid Cloud-based Colocation), Enterprise Size (Large Enterprises and SMEs), and Industry Vertical (IT and Telecom, BFSI, Healthcare, Retail, and Others)

- Status : Published

- Report Code : TIPRE00026082

- Category : Technology, Media and Telecommunications

- No. of Pages : 168

- Available Report Formats :

- Last update date : April 02, 2026

2024 Market Size

US$ 27,969.1 Mn

Base year value

2031 Forecast

US$ 61,966.8 Mn

Projected by 2031

CAGR 2025-2031

12.2 %

Growth rate

Addressable Market

US$ 318,562.53 Mn

(2025-2031)

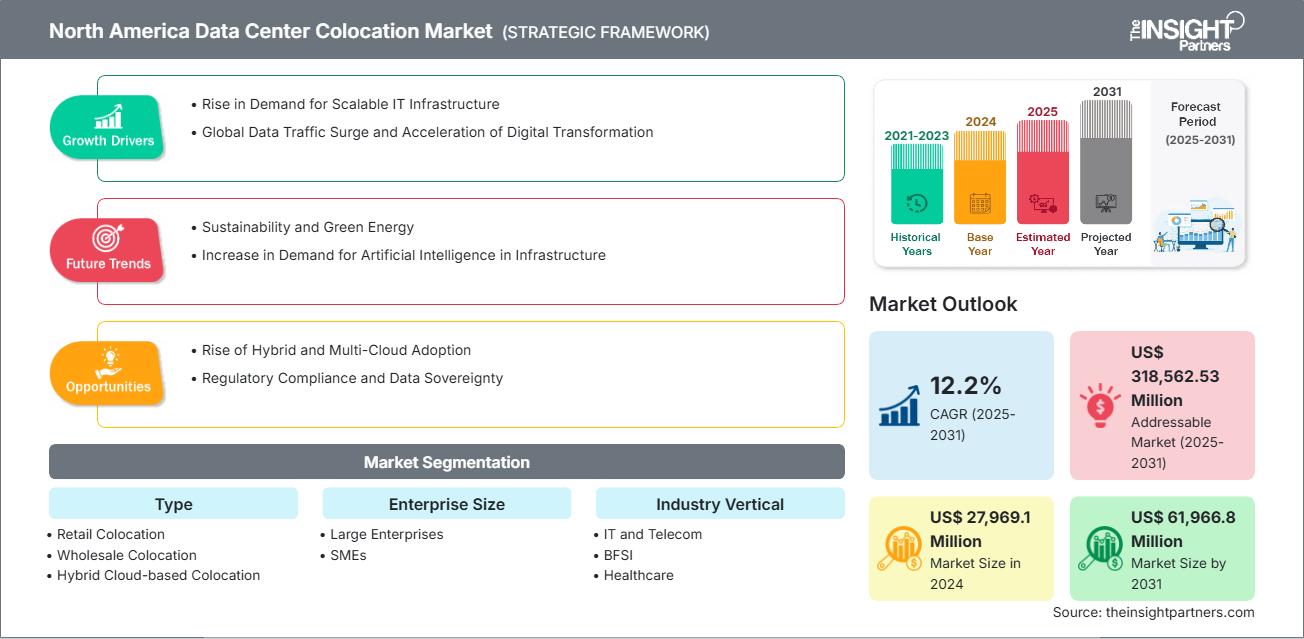

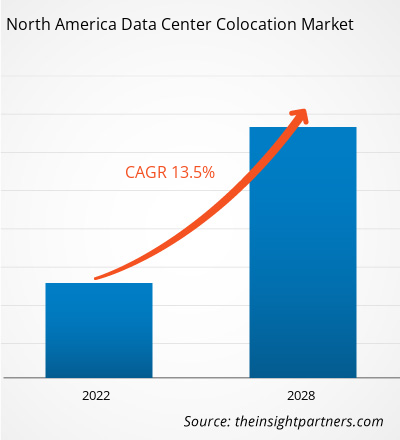

The North America Data Center Colocation Market size is expected to reach US$ 61,966.8 Million by 2031 from US$ 27,969.1 Million in 2024. The market is estimated to record a CAGR of 12.2% from 2025 to 2031.

Executive Summary and North America Data Center Colocation Market Analysis:

North America remains the world's largest data center colocation market, with the US responsible for nearly half of global data center electricity use. In 2024, US data centers consumed roughly 180 TWh, representing more than 4% of total US electricity, and this figure is projected to rise to about 260 TWh by 2026, i.e., ~6% of national demand. This explosive growth is largely propelled by AI workloads, cloud services, and edge applications that demand high-density and low-latency infrastructure. Several structural factors are driving expansion. One key factor is the availability of abundant and competitively priced electricity, especially in power-rich zones such as Northern Virginia, which hosts thousands of colocation facilities.

Additionally, rising energy costs and municipal pressure are forcing providers to adopt renewable sourcing and improve efficiency. In Eastern U.S. grids (e.g., PJM), surging demand has contributed to significant capacity auction price hikes and regulatory mandates for data centers to contribute to grid upgrade costs. Moreover, consumer and corporate ESG imperatives are increasing the demand for green-certified colocation. Many providers now offer auditgrade power metrics, carbon-neutral sourcing, and certifications such as LEED and ISO 50001. Grid capacity planning is increasingly becoming a strategic issue. Utilities and regulators are tightening rules around data center connections to ensure sustainable load growth while maintaining access to electricity for local communities.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

North America Data Center Colocation Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

North America Data Center Colocation Market Segmentation Analysis:

- By Type, the North America Data Center Colocation Market is segmented into Retail Colocation, Wholesale Colocation, and Hybrid Cloud-based Colocation. Retail Colocation held the largest share of the market in 2024.

- By Enterprise Size, the North America Data Center Colocation Market is segmented into Large Enterprises and SMEs. Large Enterprises held the largest share of the market in 2024.

- By Industry Vertical, the North America Data Center Colocation Market is segmented into IT and Telecom, BFSI, Healthcare, Retail, and Others. IT and Telecom held the largest share of the market in 2024.

North America Data Center Colocation Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ 27,969.1 Million |

| Market Size by 2031 | US$ 61,966.8 Million |

| CAGR (2025 - 2031) | 12.2% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

North America Data Center Colocation Market Players Density: Understanding Its Impact on Business Dynamics

The North America Data Center Colocation Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

North America Data Center Colocation Market Outlook

The surging demand for scalable IT infrastructure is a fundamental driver behind the expanding global data center colocation market. Enterprises, especially in sectors such as financial services, healthcare, software, and telecommunications, are increasingly turning to colocation providers instead of building and operating their data centers. This shift enables organizations to scale rapidly, avoid significant upfront capital expenditure, and convert fixed costs into variable ones, gaining operational flexibility. A key impetus for this growth is the rise in digital workloads driven by AI, IoT, edge computing, and cloud-native services, all requiring high-density, resilient infrastructure. Data from the Uptime Institute's 2023 Capacity Trends Survey shows that 64% of enterprise data center operators are expanding capacity, with 20% growing at rates exceeding 20% annually, underscoring robust internal demand. At the same time, 82% of enterprises expect increased demand for higher power densities, but over a third report that their current facilities cannot support this without upgrades, creating a clear opportunity for colocation providers with advanced power and cooling infrastructure.

On the energy front, the U.S. Energy Information Administration (EIA) reports that data centers consumed 4.4% of U.S. electricity in 2023, and this figure is projected to rise to nearly 12% by 2028. Total U.S. electricity demand is expected to grow from 4,097 billion kWh in 2024 to 4,283 billion kWh in 2026, largely driven by expanding data center activity. Globally, the International Energy Agency forecasts that data center power consumption will grow from 415 TWh in 2024 to about 945 TWh by 2030, reflecting doubling capacity needs in only a few years.

Colocation facilities are ideally positioned to meet these requirements: offering modular rack deployments, high-density power and cooling, carrier-neutral interconnectivity, and geographical flexibility. Many providers now support hyperscale and edge colocation models, enabling businesses to rapidly expand infrastructure in new regions or in response to changing workloads. This scalability-from incremental rack space to full-footprint expansion-aligns with hybrid IT strategies, reducing lead times and capital risk while ensuring infrastructure reliability.

North America Data Center Colocation Market Country Insights

By country, the North America Data Center Colocation Market is segmented into the United States, Canada, and Mexico. The United States held the largest share in 2024.

The US data center colocation market is driven by the surging demand for AI, cloud computing, and enterprise digital services. According to the US Department of Energy, data centers accounted for approximately 4.4% of national electricity consumption in 2023, projected to rise to 6.7-12% by 2028. In response, federal initiatives are actively promoting infrastructure that supports AI development. A January 2025 executive order directs agencies to open federal lands for the construction of gigawatt-scale AI data centers that comply with clean energy mandates. States such as Virginia, Texas, Ohio, and Pennsylvania are offering tax incentives and streamlined permitting to attract hyperscale deployments, particularly in energy-efficient clusters outside traditional hubs such as Ashburn and Dallas. Meanwhile, utilities are implementing andldquo;large customerandrdquo; tariff frameworks, ensuring major data center operators contribute fairly to grid upgrades and power infrastructure costs. The rising compute demand, supportive federal energy policy, and economic incentives that favor both retail and wholesale deployments combine to create a strong foundation for growth in the data center colocation market.

North America Data Center Colocation Market Company Profiles

Some of the key players operating in the market include International Business Machines Corp, Rittal GmbH & Co KG, Equinix Inc, Digital Realty Trust Inc, CoreSite Realty Corporation, CyrusOne Inc, Telehouse, NTT Data Corp, AT&T, and Iron Mountain Inc.

These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

North America Data Center Colocation Market Research Methodology

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research

The research process begins with comprehensive secondary research, utilizing internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

- Company websites, annual reports, financial statements, broker analyses, and investor presentations

- Industry trade journals and other relevant publications

- Government documents, statistical databases, and market reports

- News articles, press releases, and webcasts specific to companies operating in the market

Note:

All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.Primary Research

The Insight Partners conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis and gain valuable insights. These research interviews are designed to:

- Validate and refine findings from secondary research

- Enhance the expertise and market understanding of the analysis team

- Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

- Industry stakeholders: Vice Presidents, Business Development Managers, Market Intelligence Managers, and National Sales Managers

- External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends