Organ Care Products Market Growth & Future Prospects 2034

Coverage: By Modality (Trolley and Portable), Organ Type (Kidney, Liver, Heart, Lungs, and Others), and End User (Hospitals, Ambulatory Surgical Centers, and Others), and Geography

- Status : Data Released

- Report Code : TIPRE00027427

- Category : Life Sciences

- No. of Pages : 150

- Available Report Formats :

- Last update date : December 15, 2025

2025 Market Size

US$ 177.31 Mn

Base year value

2034 Forecast

US$ 666.22 Mn

Projected by 2034

CAGR 2026-2034

15.84 %

Growth rate

Addressable Market

US$ 3,573.70 Mn

(2026-2034)

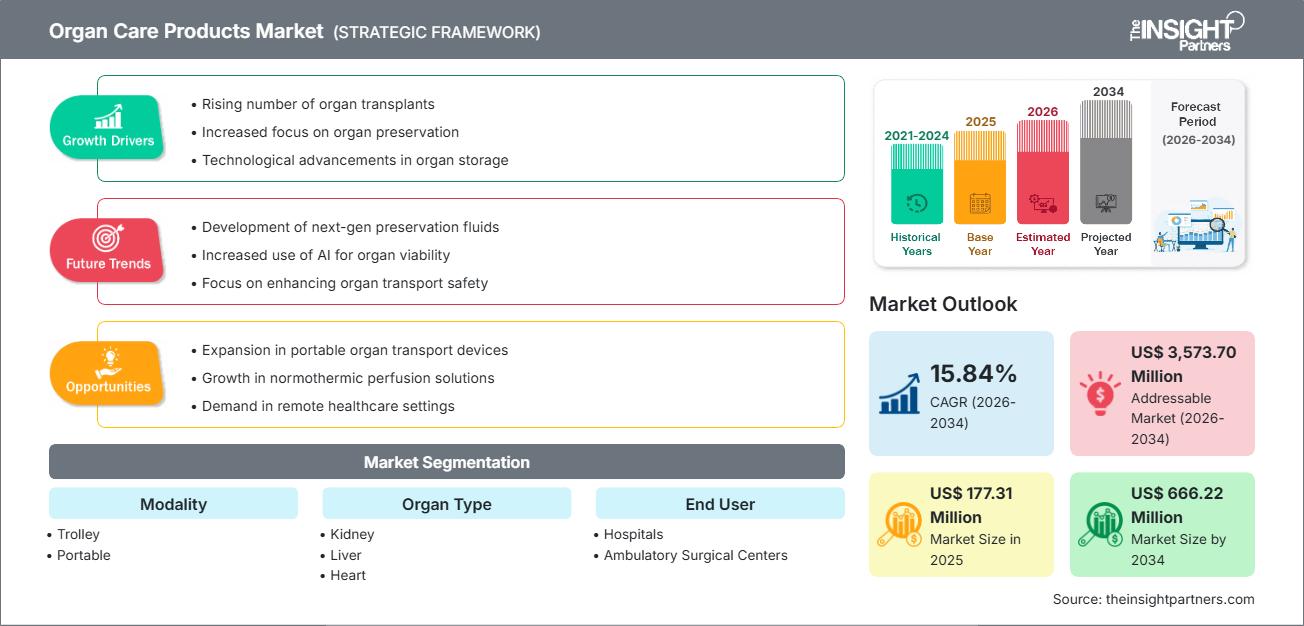

The organ care products market size is expected to reach US$ 666.22 million by 2034 from US$ 177.31 million in 2025. The market is anticipated to register a CAGR of 15.84% during 2026–2034.

Organ Care Products Market Analysis

The Organ Care Products market is expanding quickly, as a result of the growing number of organ transplants being performed globally and the rising prevalence of chronic diseases leading to organ failure. Advancements in organ preservation methods, particularly the adoption of machine perfusion systems over traditional static cold storage, are key factors in this growth. These products are crucial for extending the viability of donor organs and improving transplant success rates. The market is expected to grow rapidly with the continued focus on technological advancements in preservation techniques and supportive government initiatives promoting organ donation and transplantation.

Organ Care Products Market Overview

The implementation of advanced organ care products is essential for maintaining the viability and function of donor organs outside the body, significantly impacting the success of a transplant procedure. These systems, which include preservation solutions and machine perfusion devices, offer a dynamic environment that can mimic physiological conditions, allowing for prolonged storage and even organ repair ex vivo. At present, various products are used to safeguard organs before transplantation, as isolated organs tend to deteriorate quickly. The core concept is to enhance organ preservation time and maintain high viability, thereby reducing organ wastage and increasing the overall pool of usable organs for patients on waiting lists.

Market Research Highlights

- Global market for Organ Care Products was valued at US$ 177.31 Million in 2025

- Annual market size is expected to reach US$ 666.22 Million by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 3,573.70 Million

- Market is anticipated to register a CAGR of 15.84% during the forecast period

- The United States represents a key market, supported by Rising number of organ transplants, Increased focus on organ preservation, Technological advancements in organ storage, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Expansion in portable organ transport devices, Growth in normothermic perfusion solutions, Demand in remote healthcare settings are expected to influence market dynamics and addressable market

- Report profiles industry participants, including TransMedics, Bridge to Life Ltd, Paragonix Technologies, Inc, OrganOx Limited, Waters Medical Systems LLC, Organ Recovery Systems, Accord Healthcare, Dr. Franz Koehler Chemie GmbH, Preservation Solutions, Inc., XVIVO Perfusion, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Organ Care Products Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Organ Care Products Market Drivers and Opportunities

Market Drivers:

- Growing Burden of Chronic Diseases and Organ Failure: The increasing global prevalence of chronic conditions like kidney, liver, and heart failure significantly drives the demand for organ transplantation and, consequently, the products needed to preserve organs.

- Rising Demand for Organ Transplants & Shortage of Donor Organs: The high number of patients on transplant waiting lists and the critical gap between organs donated and organs required annually fuel the necessity for advanced preservation technologies to utilize available organs more effectively.

- Technological Advancements in Preservation Techniques: Innovations such as machine perfusion systems (hypothermic and normothermic) and refined preservation solutions (e.g., University of Wisconsin, Custodiol HTK) are extending organ viability and improving transplantation success rates.

Market Opportunities:

- Focus on Portable Organ Care Systems: The development of fully portable perfusion systems provides higher mobility and allows for safer, longer-duration transport of organs, expanding the addressable market for remote transplant centers.

- Increasing Healthcare Investments and Government Initiatives: Government and private sector investments in improving healthcare infrastructure, especially in developing regions, and initiatives to support organ donation programs are creating new avenues for product adoption.

- Development of Organ-Specific Solutions: Customized organ care systems tailored for specific organs like lungs and hearts, which have historically been challenging to preserve, offer a high-growth opportunity due to their critical nature and high demand.

Organ Care Products Market Report Segmentation Analysis

The Organ Care Products market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Modality:

- Trolley

- Portable

By Organ Type:

- Kidney

- Liver

- Heart

- Lungs

By End User:

- Hospitals

- Ambulatory Surgical Centers

By Geography:

- North America

- Europe

- Asia-Pacific

- South & Central America

- Middle East & Africa

Organ Care Products Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 177.31 Million |

| Market Size by 2034 | US$ 666.22 Million |

| Global CAGR (2026 - 2034) | 15.84% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Modality

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Organ Care Products Market Players Density: Understanding Its Impact on Business Dynamics

The Organ Care Products Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Organ Care Products Market Share Analysis by Geography

North America is expected to dominate the Organ Care Products market. The dominance of this region is gaining traction due to a well-established health infrastructure, the presence of leading market players, and a high number of organ transplant procedures performed, especially in the United States. Emerging markets in the Asia Pacific are anticipated to register the fastest growth during the forecast period, driven by the expansion of healthcare infrastructure, rising awareness, and increasing chronic disease burden in countries like China and India.

Below is a summary of market share and trends by region:

-

North America

- Market Share: Holds the largest market share, driven by high adoption of technologically advanced systems and substantial healthcare spending.

- Key Drivers:

- High incidence of organ failure and extensive transplant programs.

- Favorable reimbursement policies and sophisticated medical infrastructure.

- Presence of key technology innovators in the region.

- Trends: Rapid adoption of portable and real-time monitoring machine perfusion systems for extended preservation.

-

Europe

- Market Share: Holds a significant market share, supported by consolidated procurement systems and strong organ-donation frameworks.

- Key Drivers:

- Increasing awareness of organ donation and a supportive regulatory environment.

- Government funding for research into organ preservation.

- Focus on improving the utilization of donor organs from marginal donors.

- Trends: Increased investment in advanced preservation solutions and a move towards normothermic perfusion techniques.

-

Asia Pacific

- Market Share: Fastest-growing regional market, driven by expanding healthcare infrastructure and growing medical tourism.

- Key Drivers:

- Rapidly improving healthcare infrastructure and growing medical tourism.

- Rising prevalence of chronic lifestyle diseases and a large, aging population.

- Government-backed programs to increase organ donation rates (e.g., in China and India).

- Trends: Increasing adoption of cost-effective preservation solutions and growing demand for basic organ care products in emerging economies.

-

South and Central America

- Market Share: Emerging region with growing adoption driven by increasing healthcare modernization efforts.

- Key Drivers:

- Modernization of digital infrastructure supporting medical platforms.

- Growing efforts to improve transplant laws and donation rates in major countries.

- Trends: Focus on affordable, cloud-based preservation monitoring tools to improve logistics and coordination.

-

Middle East and Africa

- Market Share: Emerging market with strong growth potential, led by digital transformation and healthcare initiatives in the UAE and Saudi Arabia.

- Key Drivers:

- Major national digital and AI strategies fostering innovation in healthcare (e.g., UAE, Saudi Arabia).

- Increasing investments in establishing world-class transplant centers.

- Trends: Adoption of advanced perfusion technologies for high-value organ transplants to improve patient outcomes.

Organ Care Products Market Players Density: Understanding Its Impact on Business Dynamics

The Organ Care Products market is witnessing intensified competition due to the presence of specialized medical technology companies and a growing number of startups focused on next-generation preservation. Companies are actively innovating to strengthen their market position and meet the critical demand for reliable and extended organ viability solutions.

The competitive landscape is driving vendors to differentiate through:

- Organizations are developing and commercializing sophisticated machine perfusion systems (NMP and HMP) to extend organ preservation time and allow for viability assessment before transplantation.

- Solutions now include specialized preservation protocols and devices tailored to the unique physiological needs of organs like the heart and lungs, which are more sensitive to preservation time.

- Intending to reduce transport time and risk, companies are focusing on highly portable, user-friendly devices with integrated real-time monitoring and data logging capabilities.

Opportunities and Strategic Moves

- Vendors are expanding their sales and distribution networks into high-growth regions like Asia-Pacific and the Middle East, capitalizing on improving healthcare infrastructure.

- Large players are acquiring or partnering with specialized preservation technology startups to quickly integrate innovative solutions and expand their product portfolios.

- Companies are heavily investing in large-scale clinical trials (e.g., HOPE trials) to demonstrate the superior clinical efficacy of machine perfusion over static cold storage, thereby driving adoption and securing reimbursement.

Major Companies Operating in the Organ Care Products Market Are:

- TransMedics

- Bridge to Life Ltd

- Paragonix Technologies, Inc

- OrganOx Limited

- Waters Medical Systems LLC

- Organ Recovery Systems

- Accord Healthcare

- Dr. Franz Koehler Chemie GmbH

- Preservation Solutions, Inc.

Disclaimer: The companies listed above are not ranked in any particular order.

Organ Care Products Market News and Recent Developments

- For instance, on November 04, 2025, Paragonix Technologies, a pioneer in organ transplant technologies and organ procurement services, announced the launch of a first-of-its-kind supply chain initiative featuring a dedicated Paragonix Distribution Fleet.

- On October 30, 2025, OrganOx Ltd. announced the completion of its acquisition by Terumo Corporation, following satisfaction of all customary regulatory and closing conditions. OrganOx is now a wholly owned subsidiary of Terumo, positioning the company to unlock new opportunities to evolve its technology and reach more patients worldwide.

- On September 22, 2025, TransMedics Group, Inc., a medical technology company that is transforming organ transplant therapy for patients with end-stage lung, heart, and liver failure, announced a strategic collaboration with Mercedes-Benz Group AG to deploy a first-of-its-kind fleet of modern, purpose-built Mercedes-Benz V-class vehicles dedicated exclusively to organ transportation across Italy.

- For instance, August 04, 2025, TransMedics Group, Inc., a medical technology company that is transforming organ transplant therapy for patients with end-stage lung, heart, and liver failure, announced that the U.S. Food and Drug Administration (FDA) has granted conditional approval of its Investigational Device Exemption (IDE), allowing the company to proceed with the initiation of its Next-Generation OCS ENHANCE Heart trial.

- In October 2024, Paragonix Technologies, a leading organ preservation company recently acquired by Getinge, received FDA clearance for the innovative transportable perfusion device KidneyVault, to optimize the standard of care in kidney preservation.

Organ Care Products Market Report Coverage and Deliverables

The "Organ Care Products Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Organ Care Products Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Organ Care Products Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Organ Care Products Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Organ Care Products Market. Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends