Polyolefin Powders Market Demand, Size & Forecast by 2034

Polyolefin Powders Market Size and Forecasts (2021–2034), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage : by Type (Polyethylene Powder, Polypropylene Powder, EVA Powder); Applications (Rotomolding, Masterbatch); End-user Industry (Automotive and Transportation, Battery, Building and Construction, Cosmetics and Personal Care, Paints and Coatings, Tanks and Containers); and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00040358

- Category : Chemicals and Materials

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 03, 2026

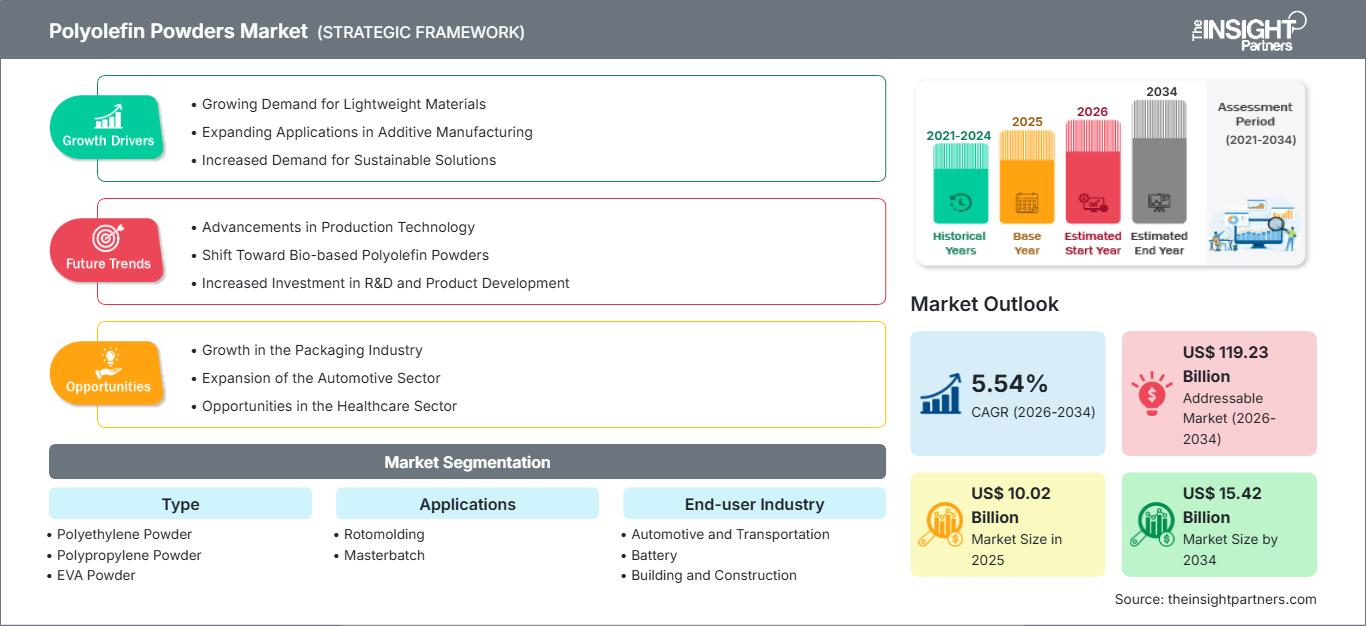

2025 Market Size

US$ 10.02 Bn

Base year value

2034 Forecast

US$ 15.42 Bn

Projected by 2034

CAGR 2026-2034

5.54 %

Growth rate

Addressable Market

US$ 119.23 Bn

(2026-2034)

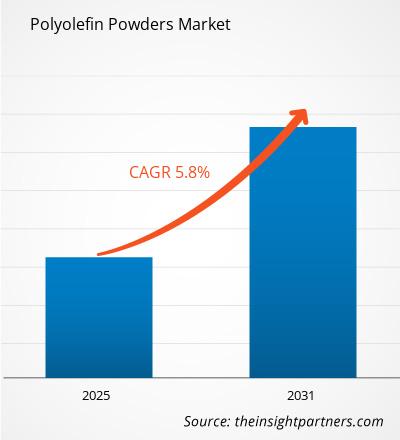

The polyolefin powders market was valued at US$ 10.02 Billion in 2025 and is projected to reach US$ 15.42 Billion by 2034, expanding at a CAGR of 5.54% during 2026–2034. Market expansion is supported by rising adoption of lightweight polymer materials across industrial manufacturing, increasing demand for high-performance powder processing technologies, and broader utilization of polyolefin powders in rotational molding, coatings, and specialized compounding applications serving diverse end-use industries.

North America is expected to maintain a stable growth trajectory throughout the forecast period, recording a CAGR of 4.8–5.3%. The region benefits from an advanced polymer manufacturing ecosystem, established rotational molding capacity, and continuous investments in automotive lightweighting initiatives. Strong demand from infrastructure modernization, industrial packaging, and advanced coatings applications further supports long-term consumption of high-quality polyolefin powder materials.

Polyolefin Powders Market Assessment and Insights

- North America: North America accounted for 30–34% of the market share in 2025 and is anticipated to expand at a CAGR of 4.8–5.3% during 2026–2034. Strong rotational molding capacity, continued investments in advanced manufacturing, and increasing adoption of lightweight automotive materials are expected to support sustained regional market growth.

- U.S.: The U.S. represented 78–82% of the North American market in 2025 and is projected to register a CAGR of 4.9–5.4% during 2026–2034, driven by expanding industrial manufacturing, growing rotational molding applications, and rising demand for high-performance polymer powders.

- Europe: Europe held 24–28% market share in 2025 and is expected to grow at a CAGR of 4.6–5.1% during 2026–2034. Germany, France, and the United Kingdom remain leading markets, supported by advanced industrial manufacturing, coatings innovation, and sustainable polymer processing initiatives.

- Asia Pacific: Asia Pacific accounted for 36–40% market share in 2025 and is forecast to expand at a CAGR of 6.5–7.1% during 2026–2034. China, India, and Japan continue to lead regional demand, driven by expanding manufacturing capacity, infrastructure investment, and increasing industrial polymer consumption.

- Largest Segment: Polyethylene Powder represented the largest market segment and is expected to record a CAGR of 5.3–5.8% during 2026–2034, reflecting its extensive use in rotational molding, coatings, and a wide range of industrial applications.

- High Growth Segment: Battery is projected to grow at a CAGR of 6.9–7.5% during 2026–2034, driven by growing electric mobility investments and increasing demand for durable, chemically resistant polymer components used in battery systems.

- Key companies analyzed in detail: Borealis AG; LyondellBasell Industries N.V.; Eastman Chemical Company; Coperion GmbH; Exxon Mobil Corporation; INEOS Group Limited; Micro Powders, Inc.; Mitsui Chemicals, Inc.; Saudi Basic Industries Corporation (SABIC); Moretex Chemical Co., Ltd.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

The development of polyolefin powders has shifted from meeting traditional demands for rotational molding to producing more innovative products capable of performing in sophisticated industrial applications. Innovations in resin formulations, micronization techniques, particle-size control, and additive use have improved the process efficiency of these powders while making it easier for companies to meet stringent demands across industries, including automotive, construction, coatings, batteries, and specialized consumer goods.

In the future, the trend toward increased investment is likely to intensify in countries developing their industrial base and building infrastructure, resulting in higher demand for polymers. Focus on material efficiency, recyclability, and low-emissions manufacturing is driving innovations in polyolefin powder manufacturing technologies. Capacity expansion, regional logistics, and strategic partnerships between resin makers and processors are expected to enhance competitiveness through 2034.

Polyolefin Powders Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 10.02 Billion |

| Market Size by 2034 | US$ 15.42 Billion |

| Global CAGR (2026 - 2034) | 5.54% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Polyolefin Powders Market Analysis

Need for polyolefin powders has been increasing in the market due to the increasing need for light weight, durable and cost-effective material that can perform well in different industries. Rotational molding has become one of the major applications of the product owing to the capability of the process to create hollow and durable parts.

Value chain of the industry starts from raw material suppliers, resin producers, powder processors, equipment providers, compounders, distributors and end-use manufacturers. Increasing efforts towards production optimization and improvement of logistics has helped the producers to supply the product reliably and respond to regional demand dynamics and customer-specific product needs.

Market competition involves product innovation, production capacity increase and long-term business relationships with customers rather than pure price competition. Major players keep distinguishing themselves from their competitors by developing unique product grades and sustainable manufacturing practices as well as providing technical assistance in the applications. Investments into research and process development improve product consistency and efficiency of manufacturing processes in global facilities.

Major participants including Borealis AG, LyondellBasell Industries N.V., Exxon Mobil Corporation, INEOS Group Limited, Saudi Basic Industries Corporation (SABIC), Mitsui Chemicals, Inc., Eastman Chemical Company, Coperion GmbH, Micro Powders, Inc., and Moretex Chemical Co., Ltd. continue to expand their competitive positioning through portfolio diversification, manufacturing upgrades, collaborative product development, and geographic expansion strategies. Their investments increasingly focus on high-performance materials that address evolving sustainability requirements while supporting industrial customers with reliable global supply capabilities.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Polyolefin Powders Market: Strategic Insights

Regional Insights

North America Polyolefin Powders Market

North America constituted 30–34% of the global market for polyolefin powders in 2025 and is expected to grow at a CAGR of 4.8–5.3% from 2026 to 2034. Factors driving the growth of the regional market include stable industrial production, superior polymer processing facilities, and the use of rotational molding technology.

Companies are investing in lightweight products for use in vehicles, buildings, and other industrial packaging applications. Innovation in products, stable resin supply, and growth in demand for molded goods contribute to regional competitive strength.

U.S. Polyolefin Powders Market

The United States represented 78–82% of North American demand in 2025 and is anticipated to register a CAGR of 4.9–5.4% through 2034. The country benefits from a mature petrochemical industry, advanced manufacturing capabilities, and significant investments in polymer processing technologies.

The presence of major producers and technology suppliers supports continuous innovation across rotational molding, masterbatch production, industrial coatings, and specialty polymer applications. Rising demand for lightweight transportation components and durable storage solutions continues to reinforce domestic market expansion.

Europe Polyolefin Powders Market

Europe captured 24–28% of global revenue in 2025 and is forecast to grow at a CAGR of 4.6–5.1% through the assessment period. Increasing emphasis on recyclable materials, industrial modernization, and efficient manufacturing processes continues to stimulate regional consumption of engineered polyolefin powders.

Germany leads the market due to its large automobile manufacturing and chemical industries, as well as its heavy investment in high-performance polymers. Industrial automation and high-quality products will continue to ensure demand for processing applications. The UK has specialized polymer processing facilities and growing investments in advanced materials used in manufacturing industries. France, Italy, and Spain contribute to Europe's diversified demand landscape through construction, coatings manufacturing, consumer goods manufacturing, and rotational molding applications.

APAC Polyolefin Powders Market

Asia Pacific accounted for 36–40% of global market revenue in 2025 and is expected to record the fastest regional expansion with a CAGR of 6.5–7.1%. Rapid industrialization, manufacturing relocation, and increasing infrastructure investments continue to accelerate consumption across multiple end-use industries.

China has a dominant market position due to its large-scale polymer production and downstream processing industries. Industrial development has been aided by government support, making the country more competitive in manufacturing. In Japan and South Korea, there is specialization in polymer production for use in the automotive and electronics industries. In India, industrial and manufacturing production has grown due to the construction of infrastructure facilities in the region.

Middle East & Africa Polyolefin Powders Market

The Middle East & Africa market is projected to expand at a CAGR of 5.2–5.8% between 2026 and 2034. Growing investments in petrochemical production, industrial diversification, and infrastructure development are supporting increased utilization of polyolefin powders across manufacturing sectors.

Saudi Arabia leads regional production through its integrated petrochemical industry and expanding downstream polymer manufacturing capabilities. Continued investments in industrial clusters encourage higher-value polymer processing and export opportunities.

The United Arab Emirates is strengthening advanced manufacturing capacity through industrial diversification initiatives, while South Africa supports demand from construction and industrial applications. The remaining MEA countries are gradually expanding polymer processing capacity alongside infrastructure and manufacturing development projects.

Segmentation Analysis

Type

Type remains the largest segment of the polyolefin powders market, supported by broad adoption across industrial manufacturing and polymer processing applications. Polyethylene Powder, the leading sub-segment, is anticipated to register a CAGR of 5.3–5.8% during 2026–2034 because of its excellent chemical resistance, processability, and suitability for rotational molding and coatings.

- Polyethylene Powder: Widely utilized in rotational molding, storage tanks, industrial containers, and protective coatings owing to excellent impact resistance, chemical stability, and consistent powder characteristics suitable for large-scale manufacturing.

- Polypropylene Powder: Increasingly adopted for lightweight automotive components, specialty compounding, and engineered plastics requiring improved stiffness, thermal resistance, and enhanced mechanical performance under demanding operating conditions.

- EVA Powder: Gains demand across adhesives, sealants, flexible coatings, and specialty formulations because of superior flexibility, strong adhesion properties, and compatibility with multiple polymer processing techniques.

Applications

- Rotomolding: Represents the dominant application due to extensive use in manufacturing tanks, containers, playground equipment, industrial products, and automotive components requiring seamless, durable, and corrosion-resistant structures.

- Masterbatch: Growing utilization reflects increasing demand for efficient pigment dispersion, additive incorporation, UV stabilization, and customized polymer formulations supporting advanced manufacturing processes across several industries.

End-user Industry

- Automotive and Transportation: Demand is supported by lightweight vehicle components, fuel efficiency initiatives, durable molded products, and increasing adoption of engineered polymer materials across transportation equipment manufacturing.

- Battery: Rapid expansion is driven by electric vehicle production, energy storage systems, and the need for chemically resistant polymer components capable of supporting demanding operating environments.

- Building and Construction: Polyolefin powders are increasingly utilized in infrastructure products, protective coatings, piping systems, and molded construction materials requiring durability and weather resistance.

- Cosmetics and Personal Care: Manufacturers utilize specialty powders in packaging solutions and selected formulation applications where material consistency, processability, and product safety remain critical considerations.

- Paints and Coatings: Demand continues to rise with increasing use of powder-based coatings offering improved abrasion resistance, corrosion protection, and extended service life for industrial equipment and infrastructure.

- Tanks and Containers: Extensive adoption reflects growing requirements for chemical storage, water management, agricultural applications, and industrial transport systems requiring durable rotationally molded products.

Opportunity Snapshot

| Segment Name | Revenue Contribution | Trend Tag | Adoption Stage |

| Automotive and Transportation | High | Lightweight Mobility | Mature |

| Battery | Medium | Energy Storage | Scaling |

| Building and Construction | High | Infrastructure Build | Mature |

| Cosmetics and Personal Care | Low | Premium Packaging | Emerging |

| Paints and Coatings | Medium | Powder Coatings | Scaling |

| Tanks and Containers | High | Water Storage | Mature |

Polyolefin Powders Market Growth Drivers and Impact Analysis

Expansion of Rotational Molding Across Industrial Manufacturing

The need for polyolefin powders has been growing on account of the rising requirement for a light-weight, durable, and economical substance that would be effective across different industrial sectors. One of the main uses of polyolefin powders has been rotational molding as a result of the ability of the process to produce hollow and durable parts.

Value chain of the industry is comprised of raw material suppliers, resin manufacturers, powder processors, machinery manufacturers, compounders, distributors, and end-users. The optimization of production and the improvement of logistics has made it possible for the manufacturers to deliver the product effectively and react to the changes in regional demand dynamics and product needs.

Competition in the market is about product innovation, production expansion, and building of long-term partnerships with the customers instead of price competition. Major manufacturers have been constantly trying to differentiate themselves from other manufacturers through the creation of unique product grades, sustainable manufacturing practices, and technical support for the applications. Research and process developments lead to better product quality and efficiency of manufacturing processes globally.

Growing Demand for Lightweight Polymer Materials in Transportation

Vehicle and transportation manufacturers are using more lightweight polymers in their products for reasons such as improved fuel economy, reduction in emission levels, and better performance levels. The polyolefin powders help in the manufacturing of strong molds that have high chemical and mechanical resistance, and also reduce the weight of the vehicle. There is an increase in the use of polymeric components in commercial vehicles, electric mobility platforms, and off-road equipment where polymer components are used instead of traditional materials. This creates the need for powder products that can meet the durability needs of manufacturers.

Advancements in Polymer Processing and Powder Technology

Improvements in micronization, compounding, and powder classification are enhancing the quality and scope of use of polyolefin powders. The producers have begun launching products with improved control over particle size, better flow properties, and greater compatibility with modern processing systems. Such technological developments have resulted in increased production efficiency, reduced raw material wastage, and improved surface finishes. The developments in digital monitoring and automated quality control systems have enabled manufacturers to operate more efficiently and reliably.

Polyolefin Powders Market Future Trends

Development of Sustainable and Circular Polyolefin Powder Solutions

Sustainability goals are expected to influence product development approaches in the polyolefin powder industry over the next ten years. Companies are now focusing on recyclable resins, resource efficiency, and low-emission manufacturing techniques that correspond with the existing environmental policies and consumers' needs. The more recycled polymers are used through advanced production technologies, the better it will be for the circular economy without affecting material characteristics. As industrial consumers pay closer attention to environmental policies across their value chains, companies providing sustainable polyolefin powders will be able to compete more effectively.

Expansion of High-Performance Specialty Powder Grades

Market demand is increasingly geared toward the formulation of special-purpose polyolefin powders tailored to industry needs rather than commodity products. Sophisticated formulations with high thermal stability, resistance to wear and chemicals, and consistent processing capability are being developed to meet customer needs. Specialty polyolefins intended for use in advanced coatings, batteries, plastic engineering, and moldings are expected to be preferred. Cooperation between resin suppliers, equipment providers, and customers will fast-track the development of differentiated products.

Polyolefin Powders Market Opportunities

Expansion of Rotational Molding Across Industrial Manufacturing

The need for polyolefin powders has been growing on account of the rising requirement for a light-weight, durable, and economical substance that would be effective across different industrial sectors. One of the main uses of polyolefin powders has been rotational molding as a result of the ability of the process to produce hollow and durable parts.

Value chain of the industry is comprised of raw material suppliers, resin manufacturers, powder processors, machinery manufacturers, compounders, distributors, and end-users. The optimization of production and the improvement of logistics has made it possible for the manufacturers to deliver the product effectively and react to the changes in regional demand dynamics and product needs.

Competition in the market is about product innovation, production expansion, and building of long-term partnerships with the customers instead of price competition. Major manufacturers have been constantly trying to differentiate themselves from other manufacturers through the creation of unique product grades, sustainable manufacturing practices, and technical support for the applications. Research and process developments lead to better product quality and efficiency of manufacturing processes globally.

Growing Demand for Lightweight Polymer Materials in Transportation

Vehicle and transportation manufacturers are using more lightweight polymers in their products for reasons such as improved fuel economy, reduction in emission levels, and better performance levels. The polyolefin powders help in the manufacturing of strong molds that have high chemical and mechanical resistance, and also reduce the weight of the vehicle. There is an increase in the use of polymeric components in commercial vehicles, electric mobility platforms, and off-road equipment where polymer components are used instead of traditional materials. This creates the need for powder products that can meet the durability needs of manufacturers.

Advancements in Polymer Processing and Powder Technology

Improvements in micronization, compounding, and powder classification are enhancing the quality and scope of use of polyolefin powders. The producers have begun launching products with improved control over particle size, better flow properties, and greater compatibility with modern processing systems. Such technological developments have resulted in increased production efficiency, reduced raw material wastage, and improved surface finishes. The developments in digital monitoring and automated quality control systems have enabled manufacturers to operate more efficiently and reliably.

Recent Developments

- July 2025: Borealis AG advanced its strategic transformation through the announced merger of its polyolefin business with Borouge to create Borouge Group International, a transaction backed by OMV and ADNOC. The combination is designed to strengthen global production capacity, expand innovation capabilities, and enhance the companies' position across advanced polyolefin materials and specialty polymer solutions.

- In first quarter of 2024, LyondellBasell expanded its flagship Microthene™ and Microthene™ F microfine polyolefin powder portfolios. These spherical, ultra-fine polyethylene powders are engineered using a specialized manufacturing process that yields particle sizes down to 20 microns. The company launched these new grades to target advanced automotive interior coatings, textile binders, and compounding additives requiring high dispersion and smooth thermal binding.

- In October 2023, Dow Inc. officially rolled out a series of high-performance polyolefin dispersion powders under its specialty packaging and adhesives division. Unlike standard pellets, these polyolefin powders are manufactured to easily disperse in water or apply dry, allowing manufacturers to create solvent-free heat-seal coatings for flexible packaging. This development directly answers municipal infrastructure demands for fully recyclable food and industrial paper barriers.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends