Polyphenylene Market Share, Growth & Forecast by 2034

Polyphenylene Market Size and Forecasts (2021 - 2034), Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage : by Type (Polyphenylene Sulfide, Polyphenylene Oxide, Polyphenylene Ether); End-User Industry (Electrical and Electronics, Automotive and Transportation); and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00040359

- Category : Chemicals and Materials

- No. of Pages : 150

- Available Report Formats :

- Last update date : July 03, 2026

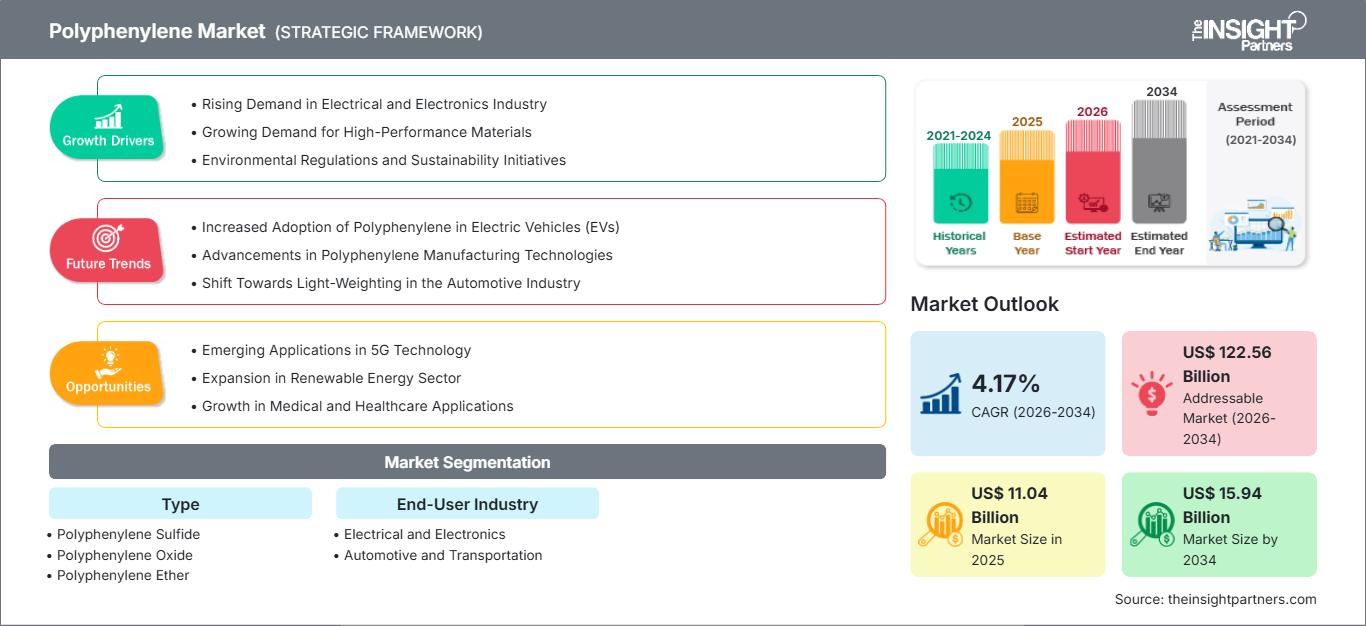

2025 Market Size

US$ 11.04 Bn

Base year value

2034 Forecast

US$ 15.94 Bn

Projected by 2034

CAGR 2026-2034

4.17 %

Growth rate

Addressable Market

US$ 122.56 Bn

(2026-2034)

The polyphenylene market was valued at US$ 11.04 billion in 2025 and is projected to reach US$ 15.94 billion by 2034, expanding at a CAGR of 4.17% during 2026–2034. Demand continues to strengthen as manufacturers increasingly adopt high-performance engineering thermoplastics for applications requiring exceptional thermal stability, dimensional accuracy, chemical resistance, and electrical insulation. Growing investments in advanced electronics, lightweight automotive components, and industrial equipment are expected to support long-term expansion while encouraging continuous material innovation and capacity optimization across global production networks.

North America is expected to remain a strategically important regional market, advancing at an estimated CAGR of 3.8–4.2% during 2026–2034. The region benefits from strong automotive electrification initiatives, increasing semiconductor manufacturing investments, and a well-established electrical equipment industry. Rising adoption of lightweight, flame-retardant polymers in electric vehicles and industrial automation systems, supported by domestic manufacturing incentives and advanced research capabilities, continues to reinforce regional demand for polyphenylene-based materials.

Polyphenylene Market Assessment and Insights

- North America: North America accounted for 31–33% share in 2025 and is projected to grow at a CAGR of 3.8–4.2% during 2026–2034. Demand is supported by expanding semiconductor manufacturing, electric vehicle production, industrial automation, and modernization of electrical infrastructure across the United States and Canada.

- U.S.: The U.S. represented 80–84% of the North American market in 2025 and is forecast to expand at a CAGR of 3.9–4.3% during 2026–2034, driven by advanced manufacturing, electronics production, and increasing use of engineering polymers in mobility applications.

- Europe: Europe held 25–27% share in 2025 and is expected to register a CAGR of 3.7–4.1% during 2026–2034. Germany leads regional demand, followed by France, Italy, and the UK, supported by automotive engineering, electrical equipment manufacturing, and sustainability-driven material substitution.

- Asia Pacific: Asia Pacific captured 36–39% share in 2025 and is anticipated to record the fastest regional expansion at a CAGR of 4.8–5.2% during 2026–2034. China, Japan, South Korea, and India continue to strengthen production capacity through investments in electronics, automotive components, and industrial manufacturing.

- Largest Segment: Electrical and Electronics represented the largest end-user segment with a market share of 44–47% in 2025 and is projected to expand at a CAGR of 4.2–4.6% during 2026–2034, reflecting sustained demand for heat-resistant and electrically insulating engineering polymers.

- High Growth Segment: Automotive and Transportation accounted for 33–36% market share in 2025 and is expected to grow at a CAGR of 4.8–5.3% during 2026–2034, supported by vehicle lightweighting, electric mobility, and increasing integration of high-performance polymer components.

- Key companies analyzed in detail: Biesterfeld AG, Celanese Corporation, Chevron Phillips Chemical Company LLC, DIC Corporation, Kureha Corporation, LG Chem Ltd., Nagase America LLC, SABIC, Sumitomo Bakelite Co., Ltd., Toray Industries, Inc., Tosoh Europe B.V.

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

Polyphenylene materials have evolved from serving specialized industrial applications to becoming essential engineering thermoplastics across high-value manufacturing sectors. Continuous improvements in polymer processing, compound formulation, and reinforcement technologies have enhanced heat resistance, chemical durability, mechanical strength, and electrical insulation properties. Manufacturers are increasingly developing customized grades for electronic connectors, battery systems, automotive under-the-hood components, and industrial equipment, while production efficiency improvements and expanded regional manufacturing capabilities continue to strengthen global supply reliability. Consequently, polyphenylene market size, polyphenylene market share, and broader commercialization continue to expand across advanced manufacturing industries.

Looking ahead, investment activity is expected to accelerate across Asia Pacific and North America as governments prioritize semiconductor production, electric mobility, and domestic industrial resilience. Environmental regulations encouraging lightweight materials and improved energy efficiency are also supporting broader adoption of advanced engineering polymers. Increasing collaboration between resin producers, compounders, automotive suppliers, and electronics manufacturers is expected to broaden the polyphenylene market scope, strengthen polyphenylene market analysis, stimulate polyphenylene market growth, and reinforce emerging polyphenylene market trends focused on sustainable material innovation and high-performance industrial applications.

Polyphenylene Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 11.04 Billion |

| Market Size by 2034 | US$ 15.94 Billion |

| Global CAGR (2026 - 2034) | 4.17% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

Polyphenylene Market Analysis

The growing preference for engineering thermoplastic resins with higher thermal stability and chemical resistance is expected to drive market growth. The use of polyphenylene-based materials by electrical and electronics manufacturers in connectors, switches, circuit breakers, sensor housings, and insulating parts is growing, as these polymers can retain their shape at higher operating temperatures. The automotive industry is also rapidly adopting polyphenylene-based products for lightweighting applications and enhanced durability in battery, powertrain, and engine parts. Automation in industries and increased usage of renewables are further boosting demand for polyphenylene-based products for components that require longevity and high resistance to adverse conditions.

The value chain for polyphenylene-based materials includes raw material suppliers, polymer manufacturers, compounders, component makers, OEMs, and aftermarket distributors. Constant development in compounding processes, glass fiber-reinforced formulations, flame-retardant formulations, and recyclable engineering plastics is enhancing product performance while meeting environmental expectations. Consistent availability of feedstocks in Asia and North America, and diversified production locations, are continuously reducing risks and improving supply chains for end-users in the industrial segment.

Competition within the Polyphenylene Market is characterized by innovation-driven product development, long-term supply partnerships, and regional manufacturing expansion. Companies including Celanese Corporation, SABIC, Toray Industries, Inc., LG Chem Ltd., and Kureha Corporation continue investing in advanced grades tailored for electric mobility, miniaturized electronics, and industrial automation. Meanwhile, Chevron Phillips Chemical Company LLC, DIC Corporation, Biesterfeld AG, Sumitomo Bakelite Co., Ltd., Nagase America LLC, and Tosoh Europe B.V. strengthen market positioning through distribution partnerships, specialty compounds, and customer-specific material solutions.

Capital investments are largely centered in Asia Pacific and North America, with producers ramping up engineering plastics production capacity to meet growing demand in the semiconductor fabrication industry, electric car production, and industry electrification. The focus has increasingly been directed toward sustainability, emissions reduction during manufacturing, and a circular materials approach. The firms are also boosting their research and development spending to improve recyclability, flame resistance, lightweighting, and precision molding properties. This will serve as the base for competitive advantage and future business opportunities.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Polyphenylene Market: Strategic Insights

Regional Insights

North America Polyphenylene Market

The North American market accounted for 31-33% of the overall market in 2025 and is projected to grow at a CAGR of 3.8-4.2% between 2026 and 2034. The robust capabilities of manufacturers in the electrical equipment, aerospace, automation, and automotive sectors are anticipated to drive demand for engineering thermoplastics. Increased investment in semiconductor fabrication plants and batteries is contributing to regional consumption of polyphenylene compounds used in electronic components and heat-dissipation systems.

Government policies supporting domestic manufacturing, modernizing energy infrastructure, and increasing electric vehicle production are encouraging innovation in material development. Material manufacturers are focusing on developing lightweight polymers that can meet safety and heat resistance standards. Consistent research collaboration between material manufacturers and OEMs is also boosting commercialization of advanced polyphenylene compounds.

U.S. Polyphenylene Market

The US accounted for 80-84% of North America's total market share in 2025 and is expected to grow at a CAGR of 3.9-4.3% through 2026-2034. The country has a highly developed industrial landscape, backed by strong automotive manufacturing, electronics, aerospace engineering, and industrial machinery sectors. Continued investments in semiconductor and electrification projects drive demand for engineering polymers that ensure reliable performance in challenging operating environments.

Key material producers from around the world have manufacturing plants, laboratories, and distribution networks across the country, allowing for the swift commercialization of specialized grades of polyphenylene. Growth in the adoption of EVs, renewables, and industrial automation systems increases consumption, while collaboration between producers and OEMs creates new applications in manufacturing.

Europe Polyphenylene Market

Europe held 25–27% of the global market in 2025 and is expected to register a CAGR of 3.7–4.1% during 2026–2034. Germany remains the leading regional market owing to its advanced automotive manufacturing base, industrial machinery production, and strong engineering expertise. Continued investments in vehicle electrification and sustainable manufacturing are encouraging wider adoption of lightweight engineering polymers across multiple industrial sectors.

The United Kingdom continues expanding demand through investments in aerospace, electrical equipment, and advanced manufacturing technologies. Growing emphasis on industrial digitalization, renewable energy infrastructure, and precision engineering has increased the use of high-performance thermoplastics capable of delivering consistent performance under challenging operating conditions.

France, Italy, and Spain collectively contribute significant regional demand through automotive production, electrical component manufacturing, and industrial equipment industries. France emphasizes electrification and sustainable transportation, Italy benefits from specialized machinery manufacturing, while Spain continues expanding renewable energy and industrial production capacity. These factors collectively support stable regional growth and increasing adoption of advanced polymer materials.

APAC Polyphenylene Market

Asia Pacific accounted for 36–39% of the global market in 2025 and is expected to record the fastest regional growth at a CAGR of 4.8–5.2% during 2026–2034. China remains the largest regional consumer because of its extensive electronics, automotive, and industrial manufacturing base.

Japan and South Korea continue leading innovation in specialty engineering polymers, while India is emerging as a significant manufacturing destination through expanding automotive and electronics production.

Supportive industrial policies, investments in semiconductor manufacturing, export-oriented production, and expanding electric vehicle supply chains continue strengthening long-term regional demand for polyphenylene materials.

Middle East & Africa Polyphenylene Market

The Middle East & Africa market is projected to grow at a CAGR of 3.6–4.0% during 2026–2034. Saudi Arabia remains the leading regional market through investments in petrochemical diversification and advanced manufacturing capabilities.

The UAE continues expanding industrial infrastructure and specialty materials consumption, while South Africa supports demand through automotive assembly and electrical equipment manufacturing.

Ongoing infrastructure development, energy diversification initiatives, and increasing industrial investments across the Rest of MEA are expected to gradually strengthen regional consumption of engineering thermoplastics over the forecast period.

Segmentation Analysis

Type

The type segment is projected to expand at a CAGR of 4.1–4.5% during 2026–2034. Product innovation continues to enhance the performance of polyphenylene materials across diverse industrial applications. Manufacturers are developing grades with improved thermal stability, chemical resistance, flame retardancy, and mechanical strength to meet evolving requirements in electronics, transportation, and industrial equipment. Increasing investments in advanced compounding technologies and precision molding capabilities are expected to support broader adoption throughout the forecast period.

- Polyphenylene Sulfide: Polyphenylene sulfide is extensively utilized in electrical connectors, automotive under-the-hood components, pumps, and industrial equipment because of its excellent heat resistance, dimensional stability, and outstanding chemical resistance under demanding operating environments.

- Polyphenylene Oxide: Polyphenylene oxide is widely adopted in electrical insulation, medical equipment, and fluid handling applications owing to its low moisture absorption, superior electrical properties, and ability to maintain mechanical integrity across varying temperatures.

- Polyphenylene Ether: Polyphenylene ether supports applications requiring lightweight construction, excellent dielectric performance, and high impact resistance. Growing utilization in electronic housings, automotive systems, and precision industrial components continues to strengthen long-term demand.

End-User Industry

The end-user industry segment is anticipated to register a CAGR of 4.2–4.7% during 2026–2034. Expanding electrification, industrial automation, and lightweight manufacturing continue to increase demand for high-performance engineering thermoplastics. Continuous product development addressing stricter safety regulations, improved thermal management, and enhanced mechanical performance is encouraging broader adoption across multiple industrial sectors. Rising investments in electric mobility and advanced electronics manufacturing further reinforce positive market prospects.

- Electrical and Electronics: As the largest application area, this segment benefits from increasing production of connectors, switches, circuit breakers, sensors, and electronic housings requiring high-temperature resistance, electrical insulation, and long operational reliability.

- Automotive and Transportation: Vehicle lightweighting, electric vehicle adoption, and growing integration of electronic systems continue driving demand for durable engineering polymers in battery components, powertrain systems, structural assemblies, and interior applications.

Opportunity Snapshot

| Segment Name | Revenue Contribution | Trend Tag | Adoption Stage |

| Electrical and Electronics | High | Power Electronics | Mature |

| Automotive and Transportation | High | EV Lightweighting | Scaling |

Polyphenylene Market Growth Drivers and Impact Analysis

Rising Electrification Across Automotive and Industrial Equipment

The ever-growing trend toward the electrification of transport and industrial equipment continues to drive the consistent need for thermoplastics capable of withstanding high-temperature and high-voltage conditions. Polyphenylene resins have good insulation properties, flame retardancy, stability, and chemical resistance, enabling their use in battery cases, connectors, sensors, charging units, and other power electronics. As the shift toward the electrification of the transportation industry, through the development of the charging network and new emission requirements, becomes increasingly popular, there is a growing tendency to substitute traditional metal-based materials with lightweight polymers. Industrial automation requires the development of reliable plastic electrical parts with an extended service life. These trends contribute to the steady expansion of the market for polyphenylene materials in high-value-added production industries.

Expansion of Semiconductor and Advanced Electronics Manufacturing

Increasing investment in semiconductor chip fabrication plants, electronics manufacturing, and telecommunication equipment is leading to rising usage of engineering polymers. The polyphenylene group of polymers offers exceptional insulating, dimensional stability, and thermal characteristics needed for making small electronic parts, connectors, switches, and precision enclosures. Governments in Asia Pacific, North America, and Europe have been consistently encouraging domestic semiconductor manufacturing through various industrial and investment policies, thereby offering greater scope for high-performance polymer producers. The growing use of artificial intelligence systems, cloud computing services, and telecommunications equipment is driving demand for superior engineering polymers. With the ongoing trend toward miniaturization and enhanced thermal performance in electronics, polyphenylene producers will likely find continued demand in sophisticated electronics.

Increasing Demand for Lightweight High-Performance Materials

Manufacturing companies in the automotive, aerospace, industrial machinery, and electrical equipment sectors are increasingly substituting metallic parts with engineering thermoplastic materials due to their energy-efficient properties and ability to reduce system weight. Materials such as polyphenylene combine mechanical strength with corrosion and heat resistance while remaining processable. Thus, complex parts can be manufactured from polyphenylene materials while retaining performance. Sustainability policies aimed at reducing fuel consumption and improving energy efficiency further support such material substitutions. Advances in glass fiber-reinforced composites and special materials broaden their applications beyond their conventional uses.

Polyphenylene Market Future Trends

Development of Sustainable and Recyclable Engineering Polymer Grades

Environmental goals are driving manufacturers to create recyclable engineering plastics with reduced environmental impact while offering high performance. Studies are leaning toward increasing recyclability, reducing manufacturing emissions, and adopting circular economy principles in the production of specialty plastics. Customers in the automotive, electronics, and industrial equipment industries are also looking for products that help them meet their environmental goals without compromising their dependability. With the introduction of stringent environmental laws, companies are expected to invest in clean manufacturing technologies and recycling processes. This is set to influence future trends in the polyphenylene industry, driven by improved sustainability and broader business acceptance.

Growing Integration with Smart Manufacturing Technologies

The use of Industry 4.0 technologies has led to changes in production processes within the engineering plastics sector. Digital quality assurance, predictive maintenance, automated compounding, and artificial intelligence-based manufacturing have resulted in efficient production while decreasing production variability. The use of process control is becoming more common among manufacturers of polyphenylene products to produce consistent specialty grades for use under rigorous conditions. Digital collaboration between material providers and OEMs is accelerating product and formulation development. With a focus on efficient operations and precision products, smart manufacturing solutions will likely be a key differentiating factor for manufacturers in the polyphenylene market.

Polyphenylene Market Opportunities

Expansion into Next-Generation Electric Mobility Applications

The continuing evolution of electric mobility presents substantial opportunities for material manufacturers to introduce specialized polyphenylene compounds for battery systems, charging infrastructure, thermal management, and lightweight structural components. Increasing production of electric passenger vehicles, commercial vehicles, and hybrid transportation platforms requires engineering materials capable of delivering long-term reliability under demanding operating conditions. Companies investing in product innovation, customer-specific formulations, and collaborative development with automotive OEMs are well positioned to capture emerging demand. Expansion into battery management systems, high-voltage connectors, and electronic control modules is expected to generate attractive long-term revenue opportunities while strengthening competitive positioning within the global engineering plastics industry.

Increasing Adoption in Renewable Energy and Industrial Electrification

Rapid expansion of renewable energy generation, smart grid infrastructure, and industrial electrification is creating new application opportunities for high-performance engineering polymers. Polyphenylene materials are increasingly utilized in electrical distribution equipment, solar energy systems, wind power components, industrial sensors, and power management devices because of their superior electrical insulation and thermal resistance. Governments worldwide continue investing in clean energy infrastructure, encouraging manufacturers to develop materials capable of meeting increasingly demanding technical specifications. Strategic partnerships with renewable energy equipment manufacturers, electrical component suppliers, and industrial automation companies are expected to create long-term growth opportunities while supporting broader diversification of end-use applications.

Recent Developments

- In June 2026: Toray Industries, Inc. announced that its subsidiary, Toray Industries (India) Private Limited, will build a new production facility for its TORELINA™ polyphenylene sulfide (PPS) resin compounds. Located in Sri City, Andhra Pradesh, this facility will boast an annual production capacity of approximately 3,000 metric tons. Slated to begin operations in early 2027, this represents Toray's first in-house PPS compounding line in India, directly targeting localized demand from automotive electrical systems, engine parts, and home appliances.

- November 2025: SABIC announced an additional expansion of its specialty polyphenylene ether (PPE) oligomers production capacity to address increasing demand from AI servers, 5G infrastructure, and advanced data-center printed circuit boards. The investment supports higher-performance electronic materials while reinforcing the company's specialty polymers business serving next-generation digital infrastructure.

- May 2025: Celanese Corporation announced global price increases for several engineered materials, including its Fortron® polyphenylene sulfide (PPS) portfolio, citing higher logistics, raw material, inventory repositioning, and operating costs. The adjustment reflects continued efforts to maintain supply continuity while supporting customers across automotive, industrial, and electrical applications.

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends