Rigid Plastic Packaging Market Size, Trends & Growth by 2034

Coverage: By Material (Polystyrene (PS), Polyethylene Terephthalate (PET), Polyethylene (PE), Polypropylene (PP), Others); End-user (Food and Beverage, Personal Care, Household, Healthcare, Others) , and Geography (North America, Europe, Asia Pacific, and South and Central America)

- Status : Data Released

- Report Code : TIPRE00007845

- Category : Chemicals and Materials

- No. of Pages : 150

- Available Report Formats :

- Last update date : March 30, 2026

2025 Market Size

US$ 250.22 Bn

Base year value

2034 Forecast

US$ 387.78 Bn

Projected by 2034

CAGR 2026-2034

4.99 %

Growth rate

Addressable Market

US$ 2,895.55 Bn

(2026-2034)

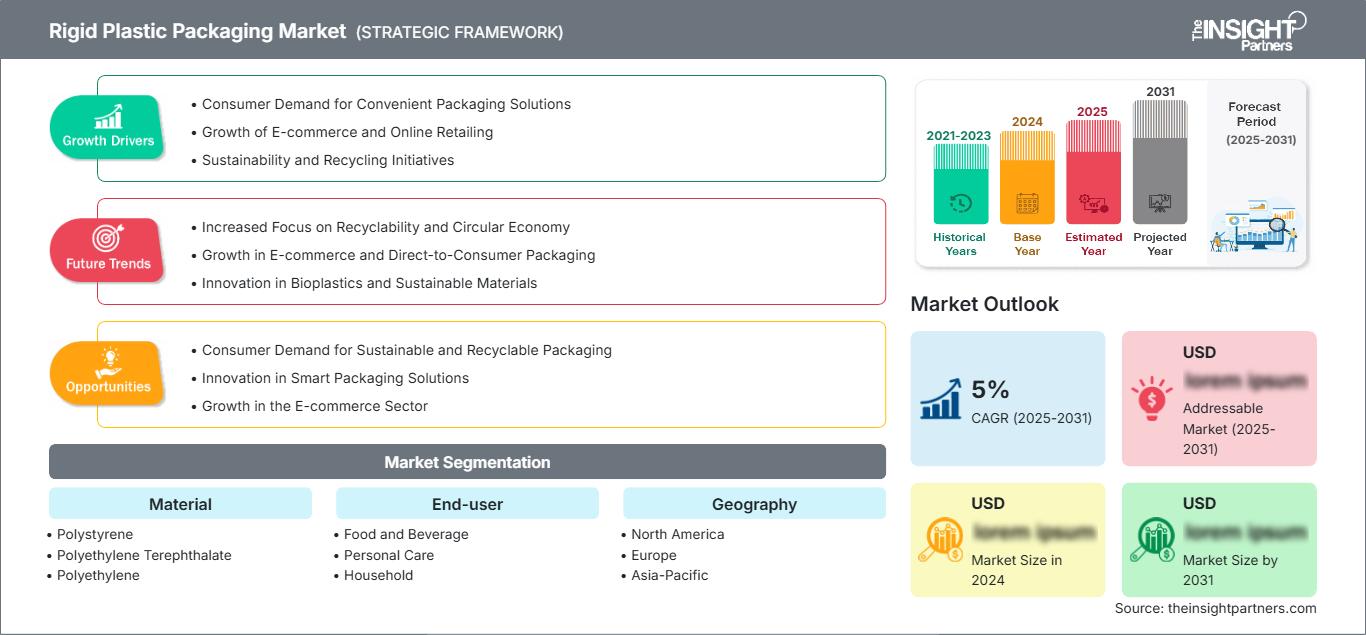

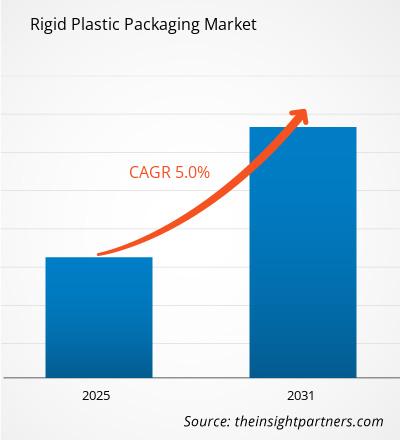

The Rigid Plastic Packaging Market size is expected to reach US$ 387.78 Billion by 2034 from US$ 250.22 Billion in 2025. The market is estimated to record a CAGR of 4.99% from 2026 to 2034.

Key market dynamics include a heightening global focus on product safety and extended shelf life, rising consumer awareness regarding the durability and lightweight advantages of plastic containers, and a significant shift toward recyclable and post-consumer recycled (PCR) materials. Additionally, the market is expected to benefit from the growing popularity of e-commerce, which demands impact-resistant packaging, the expansion of organized retail in emerging economies, and the increasing inclusion of rigid formats in high-value segments like pharmaceutical healthcare and specialty food storage.

Rigid Plastic Packaging Market Analysis

The rigid plastic packaging market analysis shows a shift toward high-performance sustainable solutions as manufacturers prioritize carbon footprint reduction without compromising structural integrity. Procurement trends indicate the market is bifurcating into cost-efficient, high-volume conventional segments and high-growth, circular-economy-driven models that utilize mono-materials and bio-based resins. Strategic opportunities are emerging in the pharmaceutical and nutraceutical sectors, where tamper-evident and moisture-barrier properties of rigid plastics offer a clear competitive advantage over traditional materials. The analysis also notes that market expansion depends on advancements in injection and blow molding technologies to create thinner, yet stronger, wall structures. Competitive differentiation now stands out depending on branding that highlights circularity, smart-packaging integration, and material efficiency, helping top-tier vendors secure long-term contracts with global FMCG brands.

Rigid Plastic Packaging Market Overview

Rigid plastic packaging is shifting from a standard utility-based industry to a sophisticated sector focused on functional innovation. While historically valued for providing basic containment and structural stability, the market is expanding into value-added solutions like smart bottles with RFID tracking, refillable systems, and specialized medical-grade containers. Both multinational conglomerates and regional specialists are part of this market, leveraging diverse manufacturing processes such as thermoforming and extrusion. More health-conscious and convenience-driven consumers in North America and Europe are looking for high-barrier protection for fresh produce and beverages, helping rigid plastic gain dominance over heavier glass and metal alternatives. Asia-Pacific remains the primary growth engine, but regions like Latin America are emerging as leaders in personal care packaging innovation. For instance, the market in the US is characterized by a mature landscape driven by a robust pharmaceutical sector and a highly developed food and beverage industry. Consumers prioritize convenience and safety, leading to high demand for tamper-evident and child-resistant formats. Innovation is currently focused on meeting state-level recycling mandates and integrating advanced lightweighting technologies to reduce transportation costs.

Market Research Highlights

- Global market for Rigid Plastic Packaging was valued at US$ 250.22 Billion in 2025

- Annual market size is expected to reach US$ 387.78 Billion by 2034

- Total addressable market (TAM) during 2026-2034 is projected to reach approximately US$ 2,895.55 Billion

- Market is anticipated to register a CAGR of 4.99% during the forecast period

- The United States represents a key market, supported by Consumer Demand for Convenient Packaging Solutions, Growth of E-commerce and Online Retailing, Sustainability and Recycling Initiatives, as well as evolving industry dynamics

- Market analysis covers North America, Europe, Asia-Pacific, South and Central America, Middle East and Africa, with growth evaluated across the forecast period

- Market opportunities such as Consumer Demand for Sustainable and Recyclable Packaging, Innovation in Smart Packaging Solutions, Growth in the E-commerce Sector are expected to influence market dynamics and addressable market

- Report profiles industry participants, including ALPLA Werke Alwin Lehner GmbH and Co KG, Amcor Plc, Berry Global Group Inc., DS Smith Plc, Kl, while analyzing competitive strategies and innovation developments

-

Source: The Insight Partners' analysis based on proprietary research, government publications, company annual reports, investor presentations, industry databases, and expert interviews.

● REPORT CUSTOMIZATION

Tailor This Report To Align With Your Specific Business Requirements

This report can be customized to align precisely with your business objectives, scope, and target markets. Customization options include tailored segmentation, geography, competitive analysis, and strategic insights to support informed decision-making.

Customize This Report →WHAT YOU CAN ADJUST

- ● Segmentations

- ● Geography

- ● Competitive Analysis

- ● Language Preferences

Rigid Plastic Packaging Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Market Drivers:

- Growth of E-commerce and Global Logistics: The surge in online shopping necessitates packaging that can withstand the rigors of transit and handling. Rigid plastic provides the necessary strength and shatter-resistance to protect goods throughout the supply chain, reducing damage rates and operational costs.

- Rising Demand for Packaged Food and Convenience: Changing consumer lifestyles and the shift toward on-the-go consumption are fueling the need for ready-to-eat meals and single-serve beverages. Rigid plastics are preferred for these applications due to their ability to maintain freshness and offer portion control.

- Advancements in Healthcare and Pharmaceutical Requirements: The pharmaceutical industry increasingly relies on rigid plastic bottles and blister packs for their superior chemical resistance and moisture barrier properties, ensuring the stability and safety of life-saving medications.

Market Opportunities:

- Expansion into Post-Consumer Recycled (PCR) Solutions: Brands are actively seeking packaging with higher recycled content to meet sustainability targets. Companies that invest in advanced recycling and high-purity PCR resins have a significant opportunity to capture premium market segments.

- Integration of Smart and Active Packaging: Incorporating QR codes, sensors, and oxygen scavengers into rigid containers allows brands to offer enhanced traceability and interactive consumer experiences, creating a high-margin niche in the food and medical sectors.

- Diversification into Bio-based and Compostable Resins: Developing rigid formats from renewable sources like corn or sugarcane offers a route to differentiate products in markets with strict single-use plastic regulations, appealing to eco-conscious Gen Z and Millennial demographics.

Rigid Plastic Packaging Market Report Segmentation

Analysis

The Rigid Plastic Packaging Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Material:

- Polyethylene Terephthalate (PET): A dominant material known for its clarity and recyclability, widely used in the beverage and personal care sectors.

- Polyethylene (PE): Includes HDPE and LDPE, valued for its toughness and chemical resistance in household and industrial containers.

- Polypropylene (PP): Preferred for its high melting point and durability, making it ideal for hot-fill food applications and microwavable containers.

- Polystyrene (PS): Utilized for its insulation properties and rigidity in food trays and dairy packaging.

- Others: Includes PVC, bio-plastics, and specialized engineering resins for niche industrial applications.

By End-user:

- Food and Beverage: The largest segment, focusing on bottles, jars, and trays that ensure food safety and shelf-life extension.

- Personal Care: Comprises premium bottles and jars for cosmetics and toiletries, where aesthetic appeal and dispensing functionality are key.

- Household: Focused on durable containers for cleaning supplies and detergents that require high chemical resistance.

- Healthcare: A high-growth area for pharmaceutical bottles and medical device trays requiring sterile and tamper-proof environments.

- Others: Includes automotive, industrial, and construction-related rigid packaging solutions.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Rigid Plastic Packaging Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 250.22 Billion |

| Market Size by 2034 | US$ 387.78 Billion |

| Global CAGR (2026 - 2034) | 4.99% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Material

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Rigid Plastic Packaging Market Players Density: Understanding Its Impact on Business Dynamics

The Rigid Plastic Packaging Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Rigid Plastic Packaging Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for industrial and consumer-grade packaging manufacturers to expand. The rigid plastic packaging market is undergoing a significant transformation, moving from a standard utility to a global high-value protective solution. Growth is driven by rapid urbanization, a surge in e-commerce, and the modernization of healthcare systems. Below is a summary of market share and trends by region:

North America

- Market Share: A mature yet evolving segment focused on high-end pharmaceutical and functional beverage packaging.

- Key Drivers:

- Increasing adoption of automation in packaging lines to enhance efficiency.

- Strong demand for premium, customized containers in the craft beverage and organic food sectors.

- Stringent FDA regulations are driving innovation in medical-grade plastic safety.

- Trends: Widespread adoption of lightweighting technologies and a shift toward 100% rPET (recycled PET) bottles to meet corporate ESG goals.

Europe

- Market Share: Holds a substantial share, characterized by a leadership role in sustainability and circular economy initiatives.

- Key Drivers:

- Strict EU plastic taxes and recycling mandates are forcing rapid material innovation.

- High consumer preference for eco-friendly and refillable packaging formats.

- Robust infrastructure for closed-loop recycling and waste management.

- Trends: Transitioning toward mono-material structures to simplify the recycling process and the rise of carbon-neutral manufacturing facilities.

Asia-Pacific

- Market Share: The largest and fastest-growing region, anchored by massive production hubs in China, India, and Southeast Asia.

- Key Drivers:

- Massive expansion of the middle-class population leading to higher consumption of packaged consumer goods.

- Rapid growth of the organized retail sector and hypermarket chains.

- Government-led Smart City and industrialization initiatives are boosting domestic manufacturing.

- Trends: Heavy reliance on digital integration (QR codes) for brand authentication and the scaling of cost-effective injection molding for mass-market food containers.

South and Central America

- Market Share: An emerging market with a growing manufacturing base in countries like Brazil and Argentina.

- Key Drivers:

- Rising urbanization and shifting lifestyles toward Western-style convenience foods.

- Modernization of the regional pharmaceutical supply chain.

- Growing interest in aesthetically premium packaging for the cosmetics industry.

- Trends: Growth of localized production to reduce import reliance and the introduction of rigid containers for traditional staples like dairy and sauces.

Middle East and Africa

- Market Share: Developing market with strategic investments in petrochemical downstream industries to localize packaging production.

- Key Drivers:

- High demand for shelf-stable UHT milk and water bottles in arid climates.

- Significant infrastructure investment in Saudi Arabia and the UAE (e.g., Vision 2030) is promoting non-oil sectors.

- Increasing formalization of the pharmaceutical retail sector.

- Trends: Implementation of high-barrier technologies to withstand extreme temperatures and a focus on cost-efficient bulk rigid containers for industrial chemicals.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Amcor PLC, Berry Global Inc., and Silgan Holdings. Regional experts and niche players like ALPLA and Pactiv Evergreen, alongside emerging innovators in the bio-plastic space, also contribute to a diverse and rapidly expanding market landscape. This competitive environment pushes vendors to differentiate through:

- Material Innovation: Developing high-performance resins that provide superior barrier properties while remaining fully recyclable, appealing to global brands seeking sustainable supply chains.

- Vertical Integration: Producers are increasingly acquiring recycling facilities to secure a steady supply of PCR (post-consumer recycled) materials, ensuring cost stability and quality control.

- Technological Leadership: Utilizing advanced molding techniques (e.g., compression injection) to create ultra-lightweight containers that reduce shipping costs and plastic resin usage.

- Customization and Design: Offering proprietary bottle shapes and smart-labeling solutions that help consumer brands stand out on crowded retail shelves.

Opportunities and Strategic Moves

- Acquisition of Niche Specialists: Major players are acquiring smaller firms specializing in sustainable or medical-grade packaging to enter high-margin sectors quickly.

- Collaborative Circularity: Partnering with waste-management companies to establish closed-loop systems, ensuring that rigid plastic waste is collected and reprocessed into new containers.

Major Companies operating in the Rigid Plastic Packaging Market are:

- ALPLA Werke Alwin Lehner GmbH and Co KG

- Amcor Plc

- Berry Global Group Inc.

- DS Smith Plc

- Klöckner Pentaplast Group

- Plastipak Holdings, Inc.

- Reynolds Group Holdings Limited

- RPC Group Plc

- Silgan Holdings Inc.

- Sonoco Products Company

Disclaimer: The companies listed above are not ranked in any particular order.

Rigid Plastic Packaging Market News and Recent Developments

- In April 2025, Amcor plc completed its all-stock combination with Berry Global. Through this transformative merger, Amcor enhanced its position as a global leader in consumer and healthcare packaging by significantly scaling its Rigid Plastic Packaging and flexible solutions portfolios. The combination integrated unique material science and innovation capabilities, which were utilized to revolutionize product development and meet the sustainability aspirations of global customers. With multiple new growth opportunities and US$650 million in identified synergies, the unified company positioned itself to deliver significant near- and long-term value for shareholders while strengthening its leadership in the global Rigid Plastic Packaging market.

- In March 2025, LyondellBasell announced the launch of Pro-fax EP649U, a new polypropylene impact copolymer designed specifically for the Rigid Plastic Packaging market. This innovative product was formulated for thin-walled injection molding, making it an ideal solution for high-performance food packaging applications.

Rigid Plastic Packaging Market Report Coverage and Deliverables

The Rigid Plastic Packaging Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Rigid Plastic Packaging Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Rigid Plastic Packaging Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Rigid Plastic Packaging Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Rigid Plastic Packaging Market.

- Detailed company profiles

Frequently Asked Questions

- Comprehensive Market Sizing and Forecast Analysis

- Detailed Segmentation Analysis

- In-Depth Market Dynamics Assessment

- Regional and Country-Level Insights

- Competitive Landscape and Company Benchmarking

- Strategic Business Intelligence

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends