Aerospace Insulation Market Size, Growth & Trends by 2034

Aerospace Insulation Market Size and Forecast (2021 - 2034), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product (Thermal Insulation, Acoustic Insulation, Electric Insulation, and Vibration Insulation), Insulation Material (Mineral Wool, Ceramic-based Materials, Foamed Plastics, and Fiberglass & Others), Aircraft Type (Commercial Aircraft, Military Aircraft, and Helicopters), and Application (Engine and Airframe)

Historic Data: 2021-2024 | Base Year: 2025 | Forecast Period: 2026-2034- Report Date : Apr 2026

- Report Code : TIPRE00018327

- Category : Chemicals and Materials

- Status : Upcoming

- Available Report Formats :

- No. of Pages : 150

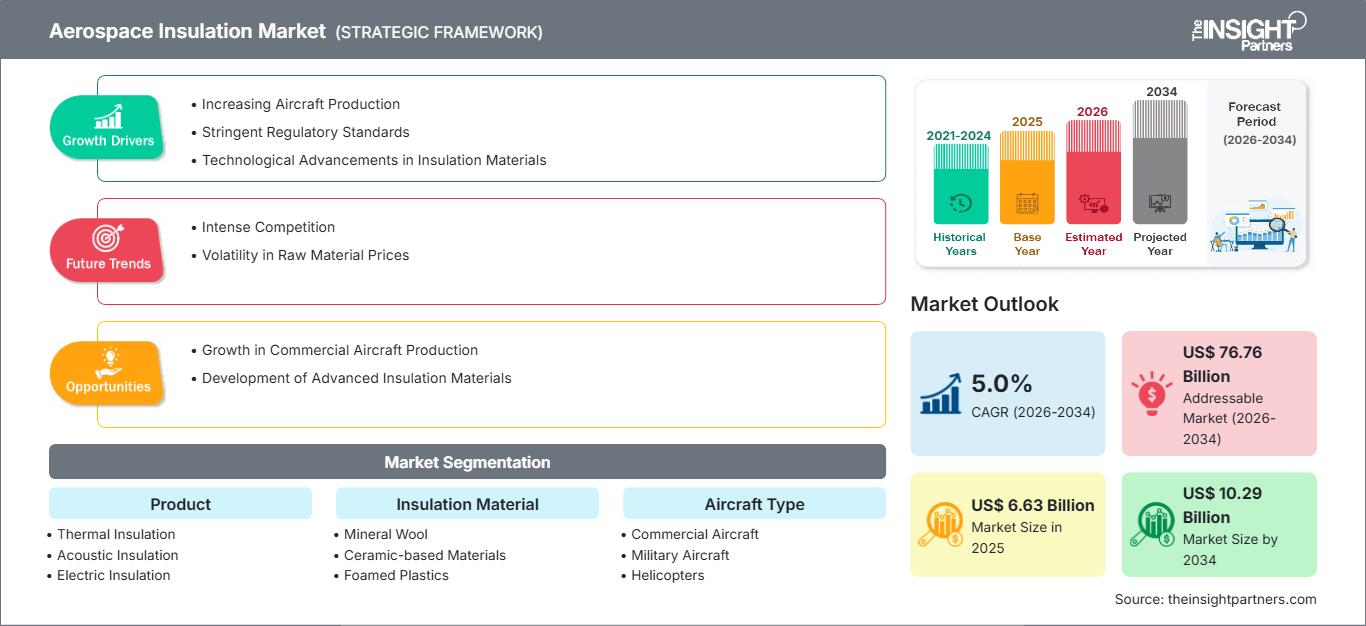

The global aerospace insulation market size is projected to reach US$ 10.29 billion by 2034 from US$ 6.63 billion in 2025. The market is anticipated to register a CAGR of 5.0% during the forecast period 2026–2034. Key market dynamics include rising demand for lightweight thermal and acoustic materials in commercial aviation, stringent regulations for fuel efficiency and noise reduction, and growing adoption of advanced composites in next-gen aircraft. Additionally, the market is expected to benefit from surging urban air mobility (UAM) projects, expansion in defense spending across emerging economies, and increasing integration of insulation in sustainable aviation fuels (SAF)-optimized fleets.

Aerospace Insulation Market Analysis

The aerospace insulation market analysis reveals that there is a change towards lightweight, multi-functional products as a result of reduced fuel and improved comfort. The procurement pattern is revealing signs that insulation markets are starting to divide between commercial OEM-sourced thermal blankets and the increasing Asia-Pacific markets. The opportunities lying in front of organizations relate to electric vertical takeoff and landing modes of aircraft. In this scenario, insulation presents an outright opportunity for competitiveness on the grounds of electric vehicle batteries and reducing noise. The opportunities of organic growth relate to ensuring insulation markets rise and fall with the reliability of fire-resistant fibers and the efficiency of vacuum formation. It has been realized that competitor brand definition is increasingly recognized on the grounds of sustainability, recyclability, and traceability of raw fibers and final product.

Aerospace Insulation Market Overview

Aerospace insulation is shifting from traditional fiberglass-based systems to a global hub for advanced composites and aerogels. While historically focused on thermal-acoustic blankets for Boeing 737 and Airbus A320 families, aerospace insulation is expanding into value-added products like phase-change materials (PCMs), vibration-dampening foams, and electric propulsion enclosures. Both OEM giants and agile aftermarket specialists are leveraging aramid fibers and ceramic matrices inherent to high-performance insulation. More efficiency-focused airlines in North America and Asia Pacific are seeking alternatives to heavy metallic barriers, helping aerospace insulation gain traction as a "lightweight enabler." North America remains the primary hub, but Europe leads in innovation for green aviation, especially through supply chains to China and India.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONAerospace Insulation Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Aerospace Insulation Market Drivers and Opportunities

Market Drivers:

- Lightweighting and Fuel Efficiency Mandates: Aerospace insulators use low-density foams and fibers to reduce the weight of the airplane by as much as 20%. This enables the airplane to comply with ICAO standards on emissions. These requirements are being fueled by the rising prices of airplane fuel.

- Stringent Noise and Thermal Regulations: Expanding urban airport infrastructure and requirements for cabin comfort have maintained demand for multi-layered acoustic panels. A growing customer insistence for quiet flights is driving volume increases for FAA and EASA-certified insulations.

- Rapid Growth in UAM and eVTOL: Digital manufacturing and digital certification procedures accelerate insulation development, as typified by the launch variants of electric flying taxis developed by Joby and Lilium.

Market Opportunities:

- Expansion into Sustainable Aviation: Beyond legacy jets, opportunities are emerging with insulation technologies that are also compatible with SAF and recyclable materials to achieve net-zero fleets.

- Growth in Emerging APAC Defense Corridors: The defense segments of the emerging APAC regions, i.e., the U.S./European suppliers and the Indian and Chinese OEMs, could be an opportunity for the company to access high-margin sectors.

- Diversification into Specialty Certifications: There are opportunities available to eVTOL producers focusing on fire-safe, low-VOC materials with the use of the FAR 25.853 and the current uptick in North American eVTOL integrations.

Aerospace Insulation Market Report Segmentation Analysis

The Aerospace Insulation Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Product:

- Thermal Insulation: Fastest-growing segment for engine nacelles and fuselage thermal barriers, driven by electrification and high-temp composites.

- Acoustic Insulation: Dominant for cabin noise reduction in commercial jets, benefiting from multi-layer foam innovations.

- Electric Insulation: Rising in eVTOL battery enclosures and wiring harnesses for high-voltage protection.

- Vibration Insulation: Key for airframe damping in helicopters and military rotors to enhance fatigue life.

By Insulation Material:

- Mineral Wool: Best used for fire resistance in the engine compartment, with stable demand in military requirements.

- Ceramic-based Materials: They have high growth potential in extreme zones of heat, like hypersonic vehicles, due to low thermal conductivity.

- Foamed Plastics: Volume leader in acoustic panels due to lightweight, cost-effective molding process.

- Fiberglass & Others: Established baseline of ‘general airframe usage,’ continually upgrading to incorporate aramid hybrids.

By Aircraft Type:

- Commercial Aircraft: Largest share from narrow-body fleets like A320neo and 737 MAX.

- Military Aircraft: Growing with stealth fighters and UAVs requiring radar-absorbent materials.

- Helicopters: Expanding for vibration control in civil and defense rotors.

By Application:

- Engine and Airframe: Core segments, with engines focusing on thermal/electric and airframes on acoustic/vibration.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Aerospace Insulation Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 6.63 Billion |

| Market Size by 2034 | US$ 10.29 Billion |

| Global CAGR (2026 - 2034) | 5.0% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Product

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Aerospace Insulation Market Players Density: Understanding Its Impact on Business Dynamics

The Aerospace Insulation Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Aerospace Insulation Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for premium insulation suppliers and UAM developers to expand.

The aerospace insulation market is undergoing a significant transformation, moving from a legacy aviation staple to a high-value enabler for electric and sustainable flight. Growth is driven by tightening emissions rules, a surge in narrow-body demand, and expansion in advanced air mobility. Below is a summary of market share and trends by region:

North America

- Market Share: Holds the largest share globally, anchored by Boeing integrations and FAA-driven innovations.

- Key Drivers:

- Strong domestic production of composites for 737 MAX and 787 fleets.

- Leadership in eVTOL via Joby Aviation and Archer.

- Robust R&D funding for fire-retardant aerogels.

- Trends: Scaling of additive-manufactured insulations and focus on recyclable materials to meet sustainability goals.

Europe

- Market Share: A mature leader, driven by Airbus A320neo and A350 ecosystems in France, Germany, and the UK.

- Key Drivers:

- EASA regulations mandate 15-20% weight reductions.

- Established supply chains for aramid-based blankets.

- EU Green Deal investments in low-emission aviation.

- Trends: Shift toward hydrogen-compatible insulations and circular economy certifications for eco-focused operators.

Asia-Pacific

- Market Share: The fastest-growing region, fueled by COMAC C919 ramp-ups and Indian Tejas expansions.

- Key Drivers:

- Massive fleet growth in China and India (projected 8,000+ new aircraft).

- Government pushes for indigenous manufacturing.

- Urbanization is driving UAM demand in megacities.

- Trends: Reliance on aftermarket MRO for legacy fleets and B2B contracts for stealth insulations in defense.

South and Central America

- Market Share: Emerging with growth in LATAM carriers like LATAM Airlines.

- Key Drivers:

- Fleet modernization for fuel savings.

- Rising business aviation in Brazil and Chile.

- Adoption of lightweight foams for regional jets.

- Trends: "OEM-to-MRO" transitions and intro of acoustic panels for high-density routes.

Middle East and Africa

- Market Share: Developing hub with Gulf carriers leading wide-body retrofits.

- Key Drivers:

- High demand for thermal protection in desert ops (e.g., Emirates A380s).

- Investments in MRO hubs like Dubai.

- Defense modernizations in the UAE and South Africa.

- Trends: Modern tech for vibration control and focus on durable panels for long-haul fleets.

High Market Density and Competition

Competition is intensifying due to established leaders such as BASF SE, 3M Company, and DuPont de Nemours. Regional specialists and niche players like Aspen Aerogels (U.S.), Zotefoams plc (UK), and Armacell International (Luxembourg), alongside innovators such as Rogers Corporation (U.S.) and Dunstone Aerogels (Australia), contribute to a diverse landscape.

This competitive environment pushes vendors to differentiate through:

- Premiumization, as well as functional brands, highlight insulation materials in weight-critical apps as superior ones having a thermal conductivity lower than 0.02W/mK as well as a sound absorption coefficient greater than 0.8 NRC.

- Products now range from blankets to include felts, syntactic foams, and EMI shielding composites used for electric VTOLs.

- The producer manages the supply chain from polyimide fiber to autoclave curing, guaranteeing that the material complies with FST requirements.

- For example, new technology such as vacuum-infused “aerogels” is leading to highly effective panels for hypersonic and space applications.

Opportunities and Strategic Moves

- Partner with OEMs and MRO networks to tap surging demand for eVTOL thermal management in Asia Pacific and North American markets.

- Incorporate sustainable, bio-based fibers and recyclability certifications to appeal to ESG-focused airlines and regulators.

Major companies operating in the Aerospace Insulation Market are:

- Duracote Corporation

- Rogers Corporation

- DuPont

- BASF SE

- 3M

- TransDigm Group Incorporated

- Triumph Inc.

- Johns Manville

- Morgan Advanced Materials Plc

Disclaimer: The companies listed above are not ranked in any particular order.

Aerospace Insulation Market News and Recent Developments

- In January 2026, TransDigm Group Incorporated announced that it had entered into a definitive agreement to purchase Jet Parts Engineering and Victor Sierra Aviation Holdings, both collectively referred to as the companies and portfolio companies of Vance Street Capital, in return for a purchase price comprising $2.2 billion and tax benefits.

- In April 2024, OROS Labs®, the company that developed the groundbreaking insulation product called Solarcore, announced that it had obtained $22 million in Series B financing under the leadership of the new investor, Airbus Ventures. OROS Labs's flagship product, Solarcore, uses the thermal characteristics of the world's least conductive solid material, called Aerogel, to create the next generation of insulating technology for a vast range of applications, from building construction to the design of cold-weather clothing and footwear. Through the synthesis of advanced technology and design innovation, OROS Labs's advanced product achieves efficiency and versatility across multiple product spaces.

Aerospace Insulation Market Report Coverage and Deliverables

The "Aerospace Insulation Market Size and Forecast (2021–2034)" report provides a detailed analysis of the market covering below areas:

- Aerospace Insulation Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Aerospace Insulation Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Aerospace Insulation Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Aerospace Insulation Market.

- Detailed company profiles

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Get Free Sample For

Get Free Sample For