Therapeutic Dog Food Market Trends, Size & Forecast by 2034

Therapeutic Dog Food Market Size and Forecast (2021 - 2034), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product Type (Dry Food, Wet/ Canned Food, Snacks/ Treats, and Others); Application (Weight Management, Digestive Care, Allergy and Immune System Health, and Others), and Geography

Historic Data: 2021-2024 | Base Year: 2025 | Forecast Period: 2026-2034- Report Date : Apr 2026

- Report Code : TIPRE00023444

- Category : Food and Beverages

- Status : Upcoming

- Available Report Formats :

- No. of Pages : 150

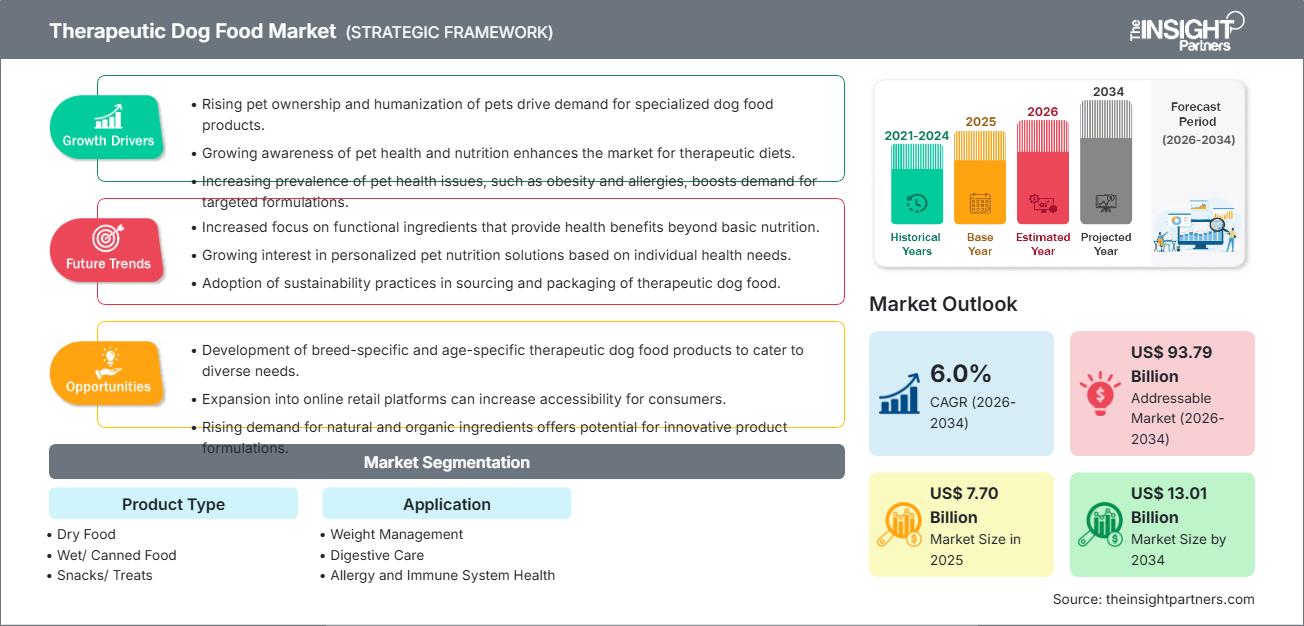

The global Therapeutic Dog Food market size is projected to reach US$ 13.01 billion by 2034 from US$ 7.70 billion in 2025. The market is anticipated to register a CAGR of 6.0% during the forecast period 2026–2034. Key market dynamics include the intensifying trend of pet humanization, where companion animals are increasingly treated as family members, and a rising prevalence of chronic health conditions such as obesity, diabetes, and gastrointestinal disorders. Additionally, the market is expected to benefit from the growing reliance on veterinary recommendations for clinical nutrition, advancements in hypoallergenic ingredient sourcing, and the expansion of specialized e-commerce platforms catering to niche dietary requirements.

Therapeutic Dog Food Market Analysis

The therapeutic dog food market analysis indicates a fundamental shift from reactive treatment to proactive wellness management through nutrition. As pet owners become more health-conscious, they are seeking functional diets that mirror human-grade health trends, such as microbiome support and anti-inflammatory ingredients. Procurement trends suggest a consolidation among large-scale clinical brands, while boutique manufacturers are finding strategic opportunities in personalized, subscription-based nutrition models. The analysis also notes that market success is heavily dependent on professional endorsements from veterinarians, as clinical validation remains the primary driver of consumer trust. Competitive differentiation is increasingly achieved through evidence-based branding, highlighting rigorous clinical trials and transparent ingredient sourcing to justify premium price points.

Therapeutic Dog Food Market Overview

Therapeutic dog food is transitioning from a specialized clinical niche into a mainstream segment of the premium pet care industry. Historically limited to prescription-only products for acute conditions, therapeutic dog food now encompasses a wide variety of maintenance diets designed for long-term health management. Both global multi-nationals and emerging biotech-focused startups are competing to provide solutions that address complex metabolic and dermatological needs. Modern consumers, particularly in North America and Western Europe, are opting for preventative therapeutic foods to extend the lifespan and quality of life for their senior pets. While dry kibble remains the dominant format due to convenience, there is a marked surge in the popularity of wet and fresh-frozen therapeutic options that offer enhanced palatability and hydration for ailing animals. For instance, the market in the US represents a mature and highly sophisticated market for therapeutic dog food, characterized by high pet ownership rates and significant per-capita spending on veterinary services. A strong preference for science-backed formulations and a high level of trust in professional dietary prescriptions define consumer behavior. The market is currently seeing a rapid expansion of digital health ecosystems where veterinary-approved nutrition is integrated with online pharmacy services, facilitating seamless home delivery for specialized diets.

Customize This Report To Suit Your Requirement

Get FREE CUSTOMIZATIONTherapeutic Dog Food Market: Strategic Insights

-

Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Therapeutic Dog Food Market Drivers and Opportunities

Market Drivers:

- Increasing Prevalence of Chronic Canine Ailments: Rising rates of obesity, joint issues, and chronic kidney disease in the aging dog population are creating a sustained demand for condition-specific nutrition. As diagnostic capabilities in veterinary medicine improve, more pets are being prescribed lifelong therapeutic diets.

- Pet Humanization and Premiumization: The emotional bond between owners and their dogs has led to a willingness to invest in high-cost, premium clinical foods. This shift is driving the adoption of human-grade ingredients and specialized formulations that offer tangible health benefits beyond basic nutrition.

- Technological Integration in Specialized Nutrition: The rise of AI-driven personalized nutrition platforms and telehealth consultations is making it easier for owners to access expert dietary advice. This digital infrastructure supports the growth of the market by providing tailored solutions for dogs with multiple health sensitivities.

Market Opportunities:

- Advancements in Novel Protein and Hypoallergenic Sources: There is a significant opportunity to develop therapeutic diets using alternative proteins, such as insect-based or lab-grown meat, to address the growing number of dogs with severe food allergies and sensitivities.

- Expansion of Preventive and Longevity Diets: Beyond treating existing illnesses, there is a burgeoning market for longevity foods designed to prevent the onset of age-related conditions in healthy adult dogs, appealing to proactive and health-conscious pet parents.

- Emerging Markets in Asia-Pacific: Developing strategic distribution networks in urban centers across China and India presents a high-margin opportunity, as the burgeoning middle class in these regions increasingly adopts Western-style pet care standards and premium nutrition habits.

Therapeutic Dog Food Market Report Segmentation Analysis

The Therapeutic Dog Food Market share is analyzed across various segments to provide a clearer understanding of its structure, growth potential, and emerging trends. Below is the standard segmentation approach used in most industry reports:

By Product Type:

- Dry Food: A widely utilized format preferred for its shelf stability and cost-effectiveness. It serves as a primary vehicle for clinical diets due to the ease of including specific fiber and mineral ratios.

- Wet/Canned Food: Favored for its high moisture content and palatability, making it ideal for dogs with renal issues or reduced appetites due to illness.

- Snacks/Treats: A growing segment focused on functional rewards that allow owners to treat pets without compromising their therapeutic dietary restrictions.

- Others: Includes emerging formats such as fresh-frozen, dehydrated, and liquid supplements used for post-operative recovery or intensive care.

By Application:

- Weight Management: Focuses on low-calorie, high-fiber formulations to combat the global rise in canine obesity and its associated metabolic risks.

- Digestive Care: Targeted at dogs with sensitive stomachs or chronic gastrointestinal issues, utilizing highly digestible ingredients and prebiotics.

- Allergy and Immune System Health: Aimed at managing dermatological and respiratory sensitivities through limited-ingredient diets and novel protein sources.

- Others: Covers specialized niche applications such as renal support, urinary tract health, diabetes management, and joint mobility.

By Geography:

- North America

- Europe

- Asia Pacific

- South & Central America

- Middle East & Africa

Therapeutic Dog Food Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2025 | US$ 7.70 Billion |

| Market Size by 2034 | US$ 13.01 Billion |

| Global CAGR (2026 - 2034) | 6.0% |

| Historical Data | 2021-2024 |

| Forecast period | 2026-2034 |

| Segments Covered |

By Product Type

|

| Regions and Countries Covered |

North America

|

| Market leaders and key company profiles |

|

Therapeutic Dog Food Market Players Density: Understanding Its Impact on Business Dynamics

The Therapeutic Dog Food Market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Therapeutic Dog Food Market Share Analysis by Geography

Asia-Pacific is expected to grow fastest in the coming years. Emerging markets in South & Central America, the Middle East, and Africa also have many untapped opportunities for premium veterinary diet producers and clinical nutrition manufacturers to expand.

The therapeutic dog food market is undergoing a significant transformation, moving from a specialized veterinary niche to a global high-value functional health category. Growth is driven by the rising prevalence of chronic canine diseases, a surge in preventative pet wellness demand, and the expansion of the luxury clinical nutrition sector. Below is a summary of market share and trends by region:

North America

- Market Share: Holds the largest share globally, anchored by a highly sophisticated veterinary infrastructure and high pet insurance penetration.

- Key Drivers:

- High consumer awareness regarding specific canine health issues, like obesity and joint mobility.

- Mainstreaming of prescription-grade fresh and frozen diets in specialty retail and direct-to-consumer channels.

- Strong presence of global market leaders driving innovation in microbiome and genomic-based nutrition.

- Trends: Rapid integration of digital health platforms for prescription management and a growing preference for human-grade, clinically validated ingredients that mirror human wellness trends.

Europe

- Market Share: Maintains a dominant position, supported by stringent regulatory frameworks for animal feed and a culture of high-quality ingredient sourcing.

- Key Drivers:

- Widespread adoption of specialized diets for aging dog populations, particularly for renal and cardiovascular care.

- Strict labeling laws and FEDIAF standards ensure the transparency and efficacy of clinical health claims.

- High demand for organic and natural clinical solutions among eco-conscious consumers in Western Europe.

- Trends: A strategic shift toward Clean Label therapeutic options and the rising inclusion of sustainably sourced proteins, such as insect or plant-based alternatives, in hypoallergenic diets.

Asia-Pacific

- Market Share: The fastest-growing region, with rapid urbanization and rising middle-class disposable income acting as the primary catalysts.

- Key Drivers:

- Explosion of pet ownership in China and India, with a specific focus on luxury and health-first pet care standards.

- Government-led modernization of the veterinary sector and expansion of professional animal hospitals in urban hubs.

- High receptivity to tech-driven personalized nutrition and e-commerce-led distribution models.

- Trends: Heavy reliance on live-stream retail and specialized online platforms, alongside a surging demand for immune-boosting and bright-eye functional formulations.

South and Central America

- Market Share: Emerging market with a growing professional sector in nations like Brazil, Argentina, and Chile.

- Key Drivers:

- Increasing pet humanization, with a growing percentage of owners viewing pets as family members requiring clinical-grade nutrition.

- Modernization of local manufacturing facilities to produce scientifically validated therapeutic recipes for regional needs.

- Rising awareness of digestive health and weight management as urban lifestyles lead to more sedentary pets.

- Trends: Growth of boutique clinical brands and the adoption of local superfood ingredients to differentiate therapeutic products from standard commercial imports.

Middle East and Africa

- Market Share: Developing market with rapid formalization of pet care services, particularly in the Gulf Cooperation Council (GCC) countries and South Africa.

- Key Drivers:

- Changing cultural norms are leading to a surge in dog ownership as companions in urban areas like Dubai and Riyadh.

- High demand for shelf-stable and premium dry therapeutic products suitable for diverse and arid climates.

- Strategic investments in high-end veterinary clinics offering specialized dietary counseling and preventative care.

- Trends: Implementation of smart logistics for high-value imports and an increasing focus on pediatric and senior-specific therapeutic nutrition to improve pet longevity.

High Market Density and Competition

Competition is intensifying due to the presence of established leaders such as Mars, Incorporated, Nestlé, Hill's Pet Nutrition, Inc., The J. M. Smucker Company, GENERAL MILLS, INC., ANIMONDA, DARWIN PET, SCHELL & KAMPETER, INC., and AFFINITY PETCARE S.A., which also contribute to a diverse and rapidly expanding market landscape.

This competitive environment pushes vendors to differentiate through:

- Evidence-Based Medical Branding: Position therapeutic dog food as a critical component of veterinary treatment by emphasizing clinical trials, microbiome-oriented upgrades, and peer-reviewed nutritional research to build trust among veterinarians and pet owners.

- Specialized Health Formulations: Expanding beyond basic life-stage diets to include highly specific clinical products. Companies now offer diets for oncology (restorative) care, renal health, diabetic management, and hypoallergenic novel protein options like insect-based or hydrolyzed diets.

- Vertical Integration and Clinical Partnerships: Leading producers manage the entire value chain, from R&D in dedicated animal science institutes to direct partnerships with veterinary hospitals. This ensures rigorous quality control and secures the prescription-only recommendation loop.

- Advanced Processing Technologies: Utilizing low-temperature extrusion, freeze-drying, and fresh-frozen technology to preserve the nutritional integrity of functional ingredients used in high-end therapeutic lines.

Opportunities and Strategic Moves

- Partner with Veterinary Telehealth and Subscription Platforms: Capitalize on the surge in digital pet health by integrating prescription-grade nutrition into auto-ship subscription models and online veterinary consultation services to ensure long-term customer retention and compliance.

- Incorporate Personalized Nutrition and Bio-Tracking: Leverage genetic and health data (e.g., Pet Biobanks) to develop customized dietary plans that address a dog's unique metabolic profile, appealing to high-spending owners seeking individualized longevity solutions.

Major Companies operating in the Therapeutic Dog Food Market are:

- Mars, Incorporated

- Nestlé

- Hill's Pet Nutrition, Inc.

- The J. M. Smucker Company

- GENERAL MILLS, INC.

- ANIMONDA

- DARWIN PET

- SCHELL & KAMPETER, INC.

- AFFINITY PETCARE S.A

- Beaphar

- WellPet

Disclaimer: The companies listed above are not ranked in any particular order.

Therapeutic Dog Food Market News and Recent Developments

- In February 2025, as part of its growth strategy to invest in faster-growing product segments adjacent to its core categories, Hill's Pet Nutrition (a division of Colgate-Palmolive Company) acquired Care TopCo Pty Ltd, owner of the Prime100 brand. This acquisition provided Hill's Pet Nutrition with a strategic entry into the fast-growing fresh segment of the Therapeutic Dog Food market, while complementing its existing science-led, veterinarian-endorsed specialty diets and strengthening its overall presence in the Australian pet food industry.

- In January 2025, private equity firm E2P acquired Bil-Jac Foods. This partnership was designed to help Bil-Jac continue delivering premium products to its customers while accelerating the brand's expansion into the high-growth Therapeutic Dog Food segment.

Therapeutic Dog Food Market Report Coverage and Deliverables

The Therapeutic Dog Food Market Size and Forecast (2021–2034) report provides a detailed analysis of the market covering below areas:

- Therapeutic Dog Food Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Therapeutic Dog Food Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST and SWOT analysis

- Therapeutic Dog Food Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments in the Therapeutic Dog Food Market.

- Detailed company profiles

Frequently Asked Questions

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Recent Reports

Testimonials

The Insight Partners' SCADA System Market report is comprehensive, with valuable insights on current trends and future forecasts. The team was highly professional, responsive, and supportive throughout. We are very satisfied and highly recommend their services.

RAN KEDEM Partner, Reali Technologies LTDsI requested a report on a very specific software market and the team produced the report in a few days. The information was very relevant and well presented. I then requested some changes and additions to the report. The team was again very responsive and I got the final report in less than a week.

JEAN-HERVE JENN Chairman, Future AnalyticaWe worked with The Insight Partners for an important market study and forecast. They gave us clear insights into opportunities and risks, which helped shape our plans. Their research was easy to use and based on solid data. It helped us make smart, confident decisions. We highly recommend them.

PIYUSH NAGPAL Sr. Vice President, High Beam GlobalThe Insight Partners delivered insightful, well-structured market research with strong domain expertise. Their team was professional and responsive throughout. The user-friendly website made accessing industry reports seamless. We highly recommend them for reliable, high-quality research services

YUKIHIKO ADACHI CEO, Deep Blue, LLC.This is the first time I have purchased a market report from The Insight Partners.While I was unsure at first, I visited their web site and felt more comfortable to take the risk and purchase a market report.I am completely satisfied with the quality of the report and customer service. I had several questions and comments with the initial report, but after a couple of dialogs over email with their analyst I believe I have a report that I can use as input to our strategic planning process.Thank you so much for taking the extra time and making this a positive experience.I will definitely recommend your service to others and you will be my first call when we need further market data.

JOHN SUZUKI President and Chief Executive Officer, Board Director, BK TechnologiesI wish to appreciate your support and the professionalism you displayed in the course of attending to my request for information regarding to infectious disease IVD market in Nigeria. I appreciate your patience, your guidance, and the fact that you were willing to offer a discount, which eventually made it possible for us to close a deal. I look forward to engaging The Insight Partners in the future, all thanks to the impression you have created in me as a result of this first encounter.

DR CHIJIOKE ONYIA MANAGING DIRECTOR, PineCrest Healthcare Ltd.Reason to Buy

- Informed Decision-Making

- Understanding Market Dynamics

- Competitive Analysis

- Identifying Emerging Markets

- Customer Insights

- Market Forecasts

- Risk Mitigation

- Boosting Operational Efficiency

- Strategic Planning

- Investment Justification

- Tracking Industry Innovations

- Aligning with Regulatory Trends

Get Free Sample For

Get Free Sample For